Europe Cranial Stabilisation Devices Market - Outlook 2020-2034

Europe Cranial Stabilisation Devices Market is segmented by Product Type (Rigid Fixation Devices, Non-rigid Fixation Devices, Hybrid Systems, Adjustable Stabilisation Devices, Disposable Stabilisation Devices), Application (Neurosurgery, Trauma Care, Spinal Surgery, Orthopedic Surgery, Research & Development), Service Type (Preoperative Planning Services, Intraoperative Support Services, Postoperative Monitoring Services, Device Maintenance and Support Services), Deployment Model (Cloud-based Surgical Planning, On-premise Device Management, Hybrid Deployment Models), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

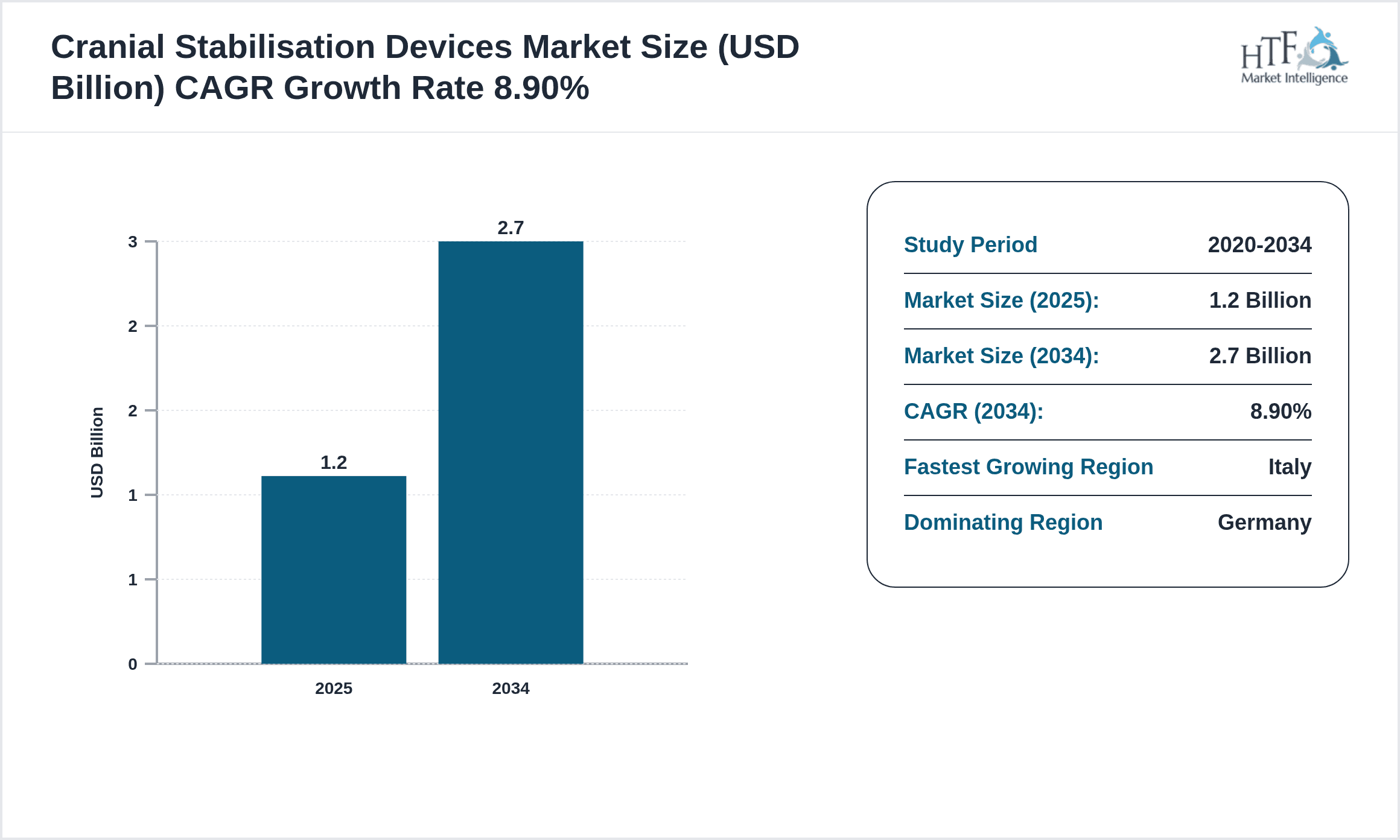

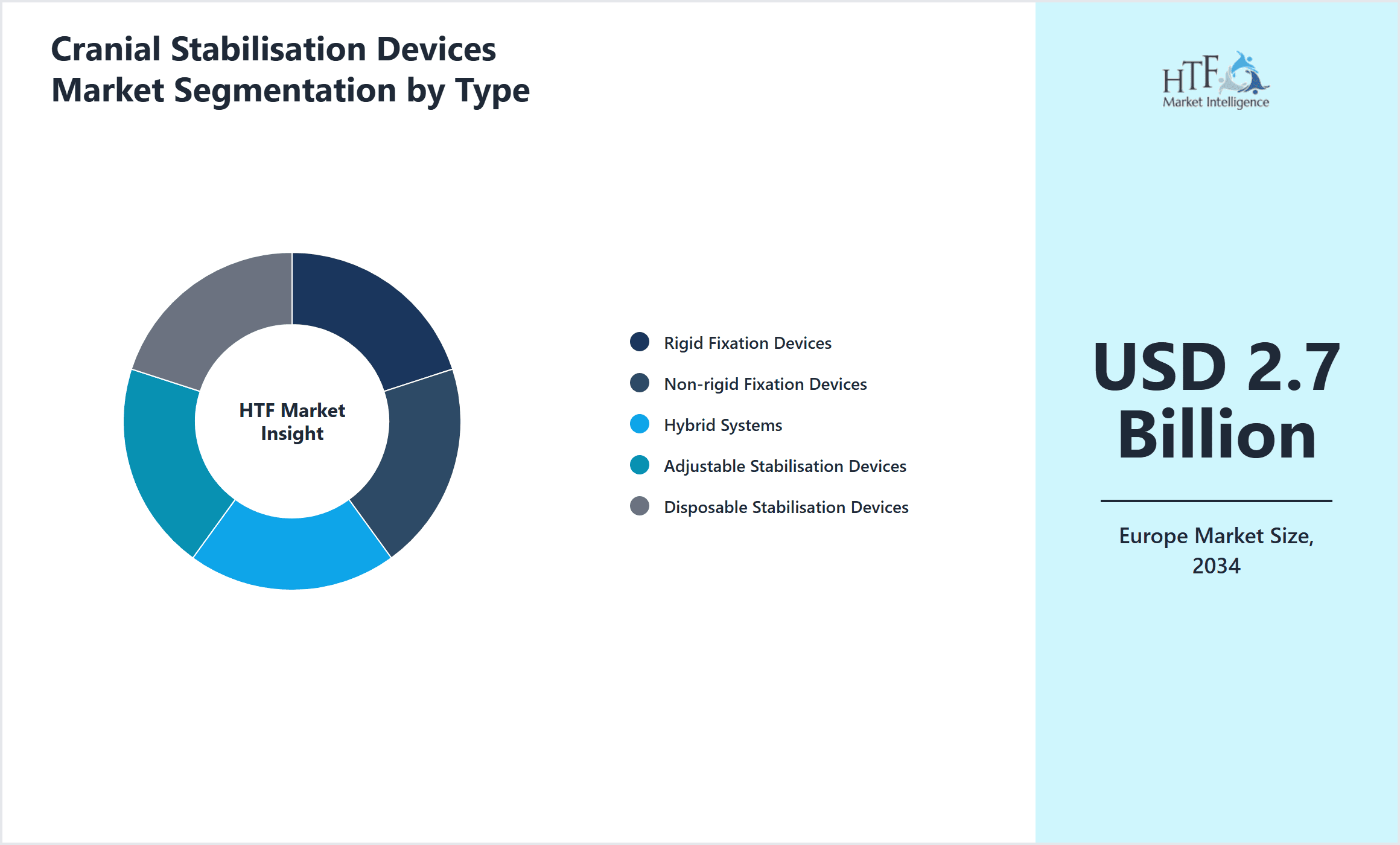

- •The Europe Cranial Stabilisation Devices Market is defined by the production and utilization of specialized devices that provide cranial support during surgical and trauma interventions. This market covers a broad scope including rigid and non-rigid fixation devices, hybrid systems, adjustable and disposable stabilisation products, catering primarily to neurosurgery, trauma care, spinal and orthopedic surgeries, and R&D sectors. End users comprise hospitals, trauma centers, and specialized surgical units that demand high precision and reliability for patient safety. The value chain integrates manufacturers, suppliers, distributors, and healthcare providers, ensuring delivery of advanced medical solutions. Technological innovations like biocompatible materials, improved ergonomics, and minimally invasive device designs are pivotal in enhancing surgical outcomes. Regional regulatory frameworks and healthcare infrastructure developments further shape market dynamics. The market witnessed steady growth from 2020 to 2025, with a base market size of USD 1.2 Billion, and is forecasted to reach USD 2.7 Billion by 2034, driven by increasing neurosurgical procedures, rising trauma incidences, and an aging population. Germany dominates the market with the largest share, while Italy is identified as the fastest-growing country within Europe. The leading product type remains rigid fixation devices, though adjustable stabilisation devices are gaining rapid traction due to their customizable features. The market is poised for considerable expansion influenced by technological advancements and rising healthcare expenditure, serving critical clinical needs across Europe.

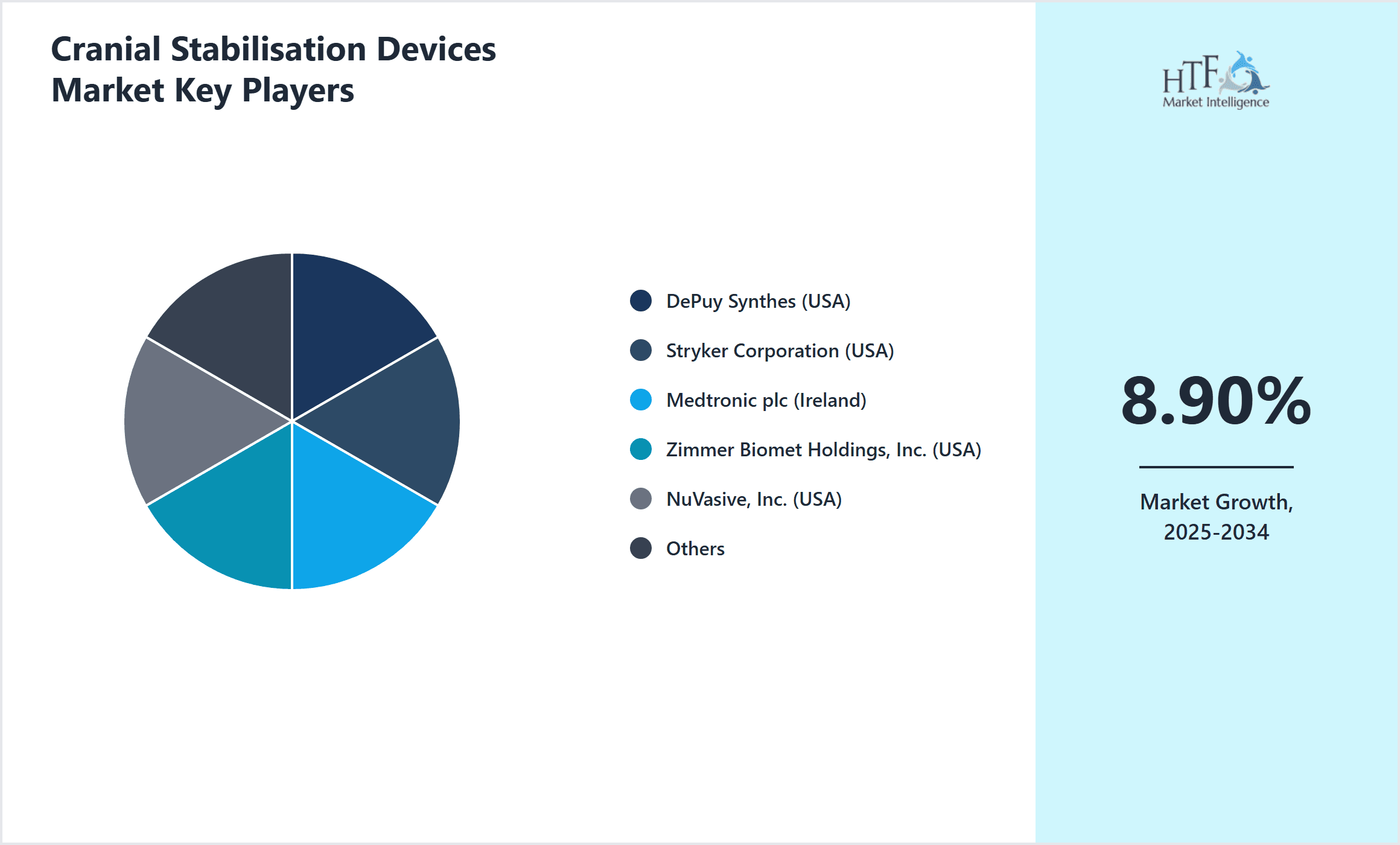

- •Key highlights include a forecast CAGR of 8.9% between 2025 and 2034, reflecting robust growth driven by increasing adoption of advanced cranial stabilisation technologies and expanding surgical volumes in Europe. The market’s value proposition lies in enhancing surgical precision, reducing operative time, and improving patient recovery outcomes. Strategic importance is underscored by the critical role these devices play in neurosurgical and trauma care procedures, making them indispensable to healthcare providers and device manufacturers. Investment in R&D and regulatory compliance remains central to sustaining competitive advantages and addressing emerging clinical needs across diverse healthcare settings.

- •The market offers significant value to stakeholders including medical device companies, healthcare practitioners, and policy makers through its capability to address complex cranial stabilization challenges. Its strategic relevance extends to improving patient safety, supporting minimally invasive surgical techniques, and enabling rapid response in trauma care. The growing demand for innovative, patient-specific solutions and expanding healthcare infrastructure in Europe further contribute to the market’s attractiveness for investors and industry participants alike.

Competitive Landscape

The Europe Cranial Stabilisation Devices Market is characterized by intense competition among established global players and emerging regional manufacturers focusing on innovation, quality, and regulatory compliance. Competitive strategies revolve around product differentiation, including the development of biocompatible materials and adjustable, minimally invasive devices that cater to evolving surgical techniques. Market participants leverage strategic partnerships, mergers and acquisitions, and geographic expansion to enhance their market presence and distribution networks. Pricing strategies balance cost-effectiveness with advanced technological features to address diverse healthcare budgets across Europe. Distribution channels are expanding, with increased emphasis on direct hospital engagements and specialized surgical centers. The competitive environment also reflects significant investments in R&D to accelerate product pipeline development and respond promptly to regulatory changes. Market entry barriers include stringent certification requirements and the need for clinical validation, which favor incumbents with established reputations. Regional competition is influenced by the healthcare infrastructure and reimbursement policies of individual European countries, with Germany and France exhibiting high device adoption rates. Looking ahead, the market is expected to witness further consolidation and innovation-driven growth as companies strive to meet the rising demand for precise and reliable cranial stabilization solutions.

Leading Companies in Cranial Stabilisation Devices Market

- •DePuy Synthes (USA)

- •Stryker Corporation (USA)

- •Medtronic plc (Ireland)

- •Zimmer Biomet Holdings, Inc. (USA)

- •NuVasive, Inc. (USA)

- •Aesculap AG (Germany)

- •Integra LifeSciences Corporation (USA)

- •Orthofix Medical Inc. (USA)

- •B. Braun Melsungen AG (Germany)

- •Medacta International SA (Switzerland)

- •KLS Martin Group (Germany)

- •Surgalign Holdings, Inc. (USA)

- •Globus Medical, Inc. (USA)

- •Smith & Nephew plc (UK)

- •Alphatec Holdings, Inc. (USA)

- •Orthopedic Synergy, Inc. (USA)

- •Nuvasive Specialized Orthopedics (USA)

- •Medicon eG (Germany)

- •Richards Manufacturing Company (USA)

- •Biedermann Motech GmbH (Germany)

- •Stryker GmbH (Germany)

- •Zimmer Biomet Deutschland GmbH (Germany)

- •Amedica Corporation (USA)

- •Orthopediatrics Corp. (USA)

- •Linvatec Corporation (USA)

Market Breakdown

- •By Product Type

- ◦Rigid Fixation Devices

- ◦Non-rigid Fixation Devices

- ◦Hybrid Systems

- ◦Adjustable Stabilisation Devices

- ◦Disposable Stabilisation Devices

- •By Application

- ◦Neurosurgery

- ◦Trauma Care

- ◦Spinal Surgery

- ◦Orthopedic Surgery

- ◦Research & Development

- •By Service Type

- ◦Preoperative Planning Services

- ◦Intraoperative Support Services

- ◦Postoperative Monitoring Services

- ◦Device Maintenance and Support Services

- •By Deployment Model

- ◦Cloud-based Surgical Planning

- ◦On-premise Device Management

- ◦Hybrid Deployment Models

Growth Dynamics

- •The rising incidence of traumatic brain injuries across Europe is a primary growth driver, boosting the demand for advanced cranial stabilisation devices that enhance surgical outcomes and patient safety in trauma care settings.

- •Technological advancements such as the introduction of adjustable stabilisation devices and biocompatible materials have improved device efficacy and patient comfort, driving adoption in both neurosurgery and spinal surgery applications.

- •Increasing healthcare expenditure and expanding surgical infrastructure in key European countries, including Germany and France, have facilitated greater access to sophisticated cranial stabilisation solutions.

- •Regulatory approvals and harmonization of medical device standards within the European Union have reduced market entry barriers, enabling faster commercialization of innovative cranial stabilisation products.

- •Growing awareness among surgeons and healthcare providers about the benefits of minimally invasive surgical techniques has propelled the demand for specialized cranial stabilisation devices designed for such procedures.

- •Collaborations between device manufacturers and research institutions have accelerated product development cycles, leading to the introduction of tailored solutions that address specific clinical challenges.

- •The aging population in Europe, with increasing prevalence of neurodegenerative conditions, is expanding the patient pool requiring cranial stabilisation interventions, underpinning long-term market growth.

Market Trends

- •There is a growing trend towards the use of patient-specific cranial stabilisation devices developed through 3D printing technologies, enabling customized fit and enhanced surgical precision.

- •Integration of digital surgical planning software with cranial stabilisation devices is increasingly adopted, facilitating precise preoperative visualization and intraoperative guidance.

- •Sustainability considerations are influencing device design, with manufacturers focusing on biodegradable and reusable materials to reduce environmental impact.

- •Emerging business models include bundled service offerings combining devices with comprehensive surgical support services, enhancing value for healthcare providers.

- •Expansion of telemedicine and remote surgical consultation services is driving demand for cloud-based deployment models for device management and surgical planning.

- •Increasing collaborations between neurosurgeons and device engineers are fostering innovation in minimally invasive cranial stabilisation techniques.

- •Regulatory emphasis on post-market surveillance is encouraging continuous improvement and safety monitoring of cranial stabilisation devices across Europe.

Market Opportunities

- •Expansion into underserved Eastern European markets presents significant growth potential due to rising healthcare investments and increasing surgical procedure volumes in the region.

- •Development of innovative adjustable and hybrid cranial stabilisation devices tailored to complex surgical cases can capture niche market segments with unmet clinical needs.

- •Opportunities exist in integrating AI-driven analytics with device management platforms to enhance surgical planning and postoperative outcome prediction.

- •Increasing government funding for trauma care infrastructure improvements offers avenues for collaboration and device adoption in public hospitals.

- •Emerging trends in personalized medicine encourage investment in customizable cranial stabilisation solutions, aligning with precision healthcare initiatives.

- •Strategic partnerships with academic institutions can accelerate R&D efforts and facilitate clinical validation, strengthening product credibility and market acceptance.

- •Growing demand for minimally invasive surgical procedures expands the market for advanced cranial stabilisation devices that support such techniques.

Market Challenges

- •Stringent regulatory requirements and lengthy approval processes within the European Union pose significant challenges for new entrants and innovation timelines.

- •High costs associated with advanced cranial stabilisation devices limit accessibility, particularly in low-resource healthcare settings across Europe.

- •Limited surgeon training and awareness regarding novel stabilisation technologies can hinder adoption and integration into standard surgical protocols.

- •Competition from alternative treatment methodologies and device types creates pressure on pricing and market share for cranial stabilisation devices.

- •Supply chain disruptions and dependence on specialized raw materials may cause production delays and increased manufacturing costs.

- •Challenges in demonstrating long-term clinical benefits and safety profiles can affect payer reimbursement and market acceptance.

- •Fragmented healthcare systems and reimbursement policies across European countries complicate market entry and expansion strategies.

Regulatory Framework

- •The EU Medical Device Regulation (MDR) implemented in 2021 has established stringent requirements for device safety, clinical evaluation, and post-market surveillance, significantly impacting the cranial stabilisation devices market by raising compliance standards and ensuring higher patient safety.

- •The In Vitro Diagnostic Regulation (IVDR) complements MDR by regulating diagnostic components associated with device usage, enhancing the overall regulatory landscape for cranial stabilisation products between 2020 and 2025.

- •National agencies such as Germany’s Federal Institute for Drugs and Medical Devices (BfArM) and France’s National Agency for the Safety of Medicines and Health Products (ANSM) enforce localized regulatory mandates, requiring additional certifications and audits from 2020 through 2025.

- •The European Database on Medical Devices (EUDAMED) was introduced to improve transparency and traceability of medical devices, including cranial stabilisation devices, facilitating regulatory compliance and market surveillance since 2022.

- •Government initiatives supporting harmonization of standards across member states aim to streamline approval processes and encourage innovation while maintaining high safety and efficacy benchmarks.

Market Intelligence

- •15th March 2024, Medtronic plc announced the launch of a next-generation cranial stabilisation system featuring adaptive fixation technology that allows for intraoperative adjustability, enhancing surgical precision and patient outcomes. The system integrates with digital surgical planning platforms and is targeted at European neurosurgical centers aiming to improve procedure efficiency. This innovation is expected to expand Medtronic's market share in Europe significantly. Source: Medtronic Official Press Release

- •10th January 2025, Stryker Corporation unveiled its new line of biodegradable cranial fixation devices designed to minimize long-term complications and reduce the need for secondary surgeries. The products comply with the latest EU MDR standards and are positioned to capture growing demand for sustainable medical devices across Europe. This development reflects Stryker's commitment to innovation aligned with environmental considerations. Source: Stryker Corporate News

- •22nd August 2024, DePuy Synthes initiated a strategic partnership with a leading European research university to co-develop AI-powered cranial stabilisation solutions aimed at personalized surgical planning. This collaboration focuses on integrating machine learning algorithms to optimize device configuration for individual patients, enhancing clinical outcomes and expanding product capabilities. The initiative positions DePuy Synthes as a pioneer in digital integration within the cranial stabilisation market. Source: DePuy Synthes Official Announcement

- •5th November 2024, Zimmer Biomet Holdings, Inc. completed the acquisition of a specialized European medical device firm focusing on adjustable cranial stabilisation technologies. This acquisition enhances Zimmer Biomet’s portfolio and strengthens its presence in the European market by adding innovative products designed for minimally invasive procedures. The deal is expected to generate significant synergies and accelerate growth in the region. Source: Zimmer Biomet Investor Relations

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Italy is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.2 Billion |

| Forecast Year Market Size | USD 2.7 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Product Type (Rigid Fixation Devices, Non-rigid Fixation Devices, Hybrid Systems, Adjustable Stabilisation Devices, Disposable Stabilisation Devices), Application (Neurosurgery, Trauma Care, Spinal Surgery, Orthopedic Surgery, Research & Development), Service Type (Preoperative Planning Services, Intraoperative Support Services, Postoperative Monitoring Services, Device Maintenance and Support Services), Deployment Model (Cloud-based Surgical Planning, On-premise Device Management, Hybrid Deployment Models) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | DePuy Synthes (USA), Stryker Corporation (USA), Medtronic plc (Ireland), Zimmer Biomet Holdings, Inc. (USA), NuVasive, Inc. (USA) |

Europe Cranial Stabilisation Devices Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.