Global Advanced High-strength Steel Market - Outlook 2020-2034

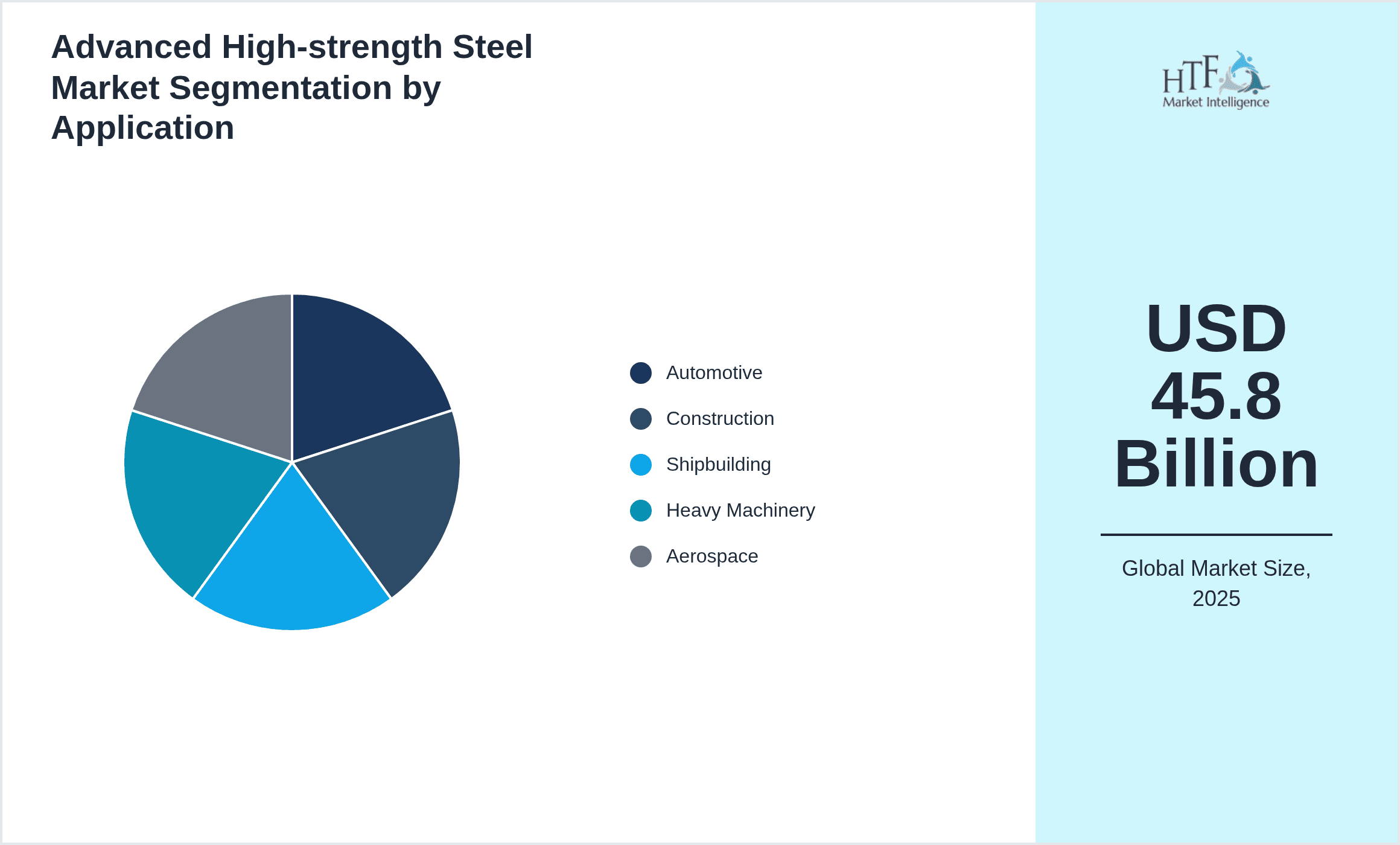

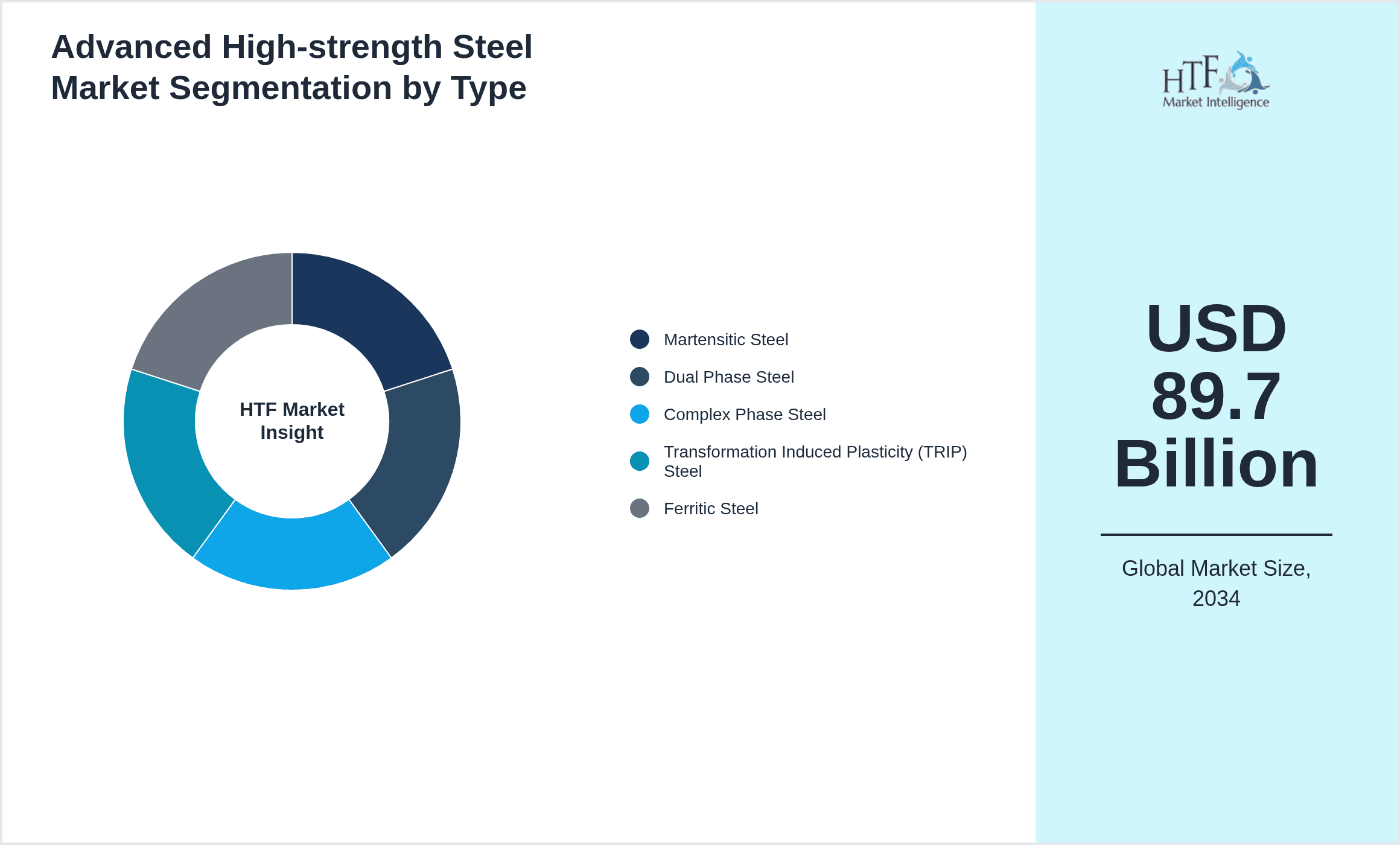

Global Advanced High-strength Steel Market is segmented by Type (Martensitic Steel, Dual Phase Steel, Complex Phase Steel, Transformation Induced Plasticity (TRIP) Steel, Ferritic Steel), Application (Automotive, Construction, Shipbuilding, Heavy Machinery, Aerospace), Product Form (Coils, Sheets, Plates, Bars), Coating Type (Galvanized, Galvalume, Electrolytic, Uncoated), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •Advanced High-strength Steel (AHSS) represents a critical innovation in metallurgical engineering, providing a unique combination of strength, ductility, and corrosion resistance. This steel category is predominantly used in sectors requiring materials that balance weight reduction with enhanced performance, such as automotive manufacturing, construction, aerospace, heavy machinery, and shipbuilding. The global AHSS market has witnessed substantial growth from 2020 to 2025, propelled by increasing environmental regulations and the automotive industry's shift towards fuel-efficient and safer vehicles. The forecast period through 2034 anticipates sustained growth driven by advancements in steel processing technologies and expanding applications in emerging economies. The market segmentation includes types such as martensitic, dual phase, complex phase, transformation induced plasticity (TRIP), and ferritic steels, each serving distinct engineering needs. Regionally, North America leads the market in terms of size due to the presence of established automotive manufacturing hubs, while Asia-Pacific is projected to be the fastest growing region, supported by rapid industrialization and infrastructure development. The market's strategic importance spans multiple industries seeking to optimize performance and sustainability through advanced materials, positioning AHSS as a key enabler of next-generation engineering solutions.

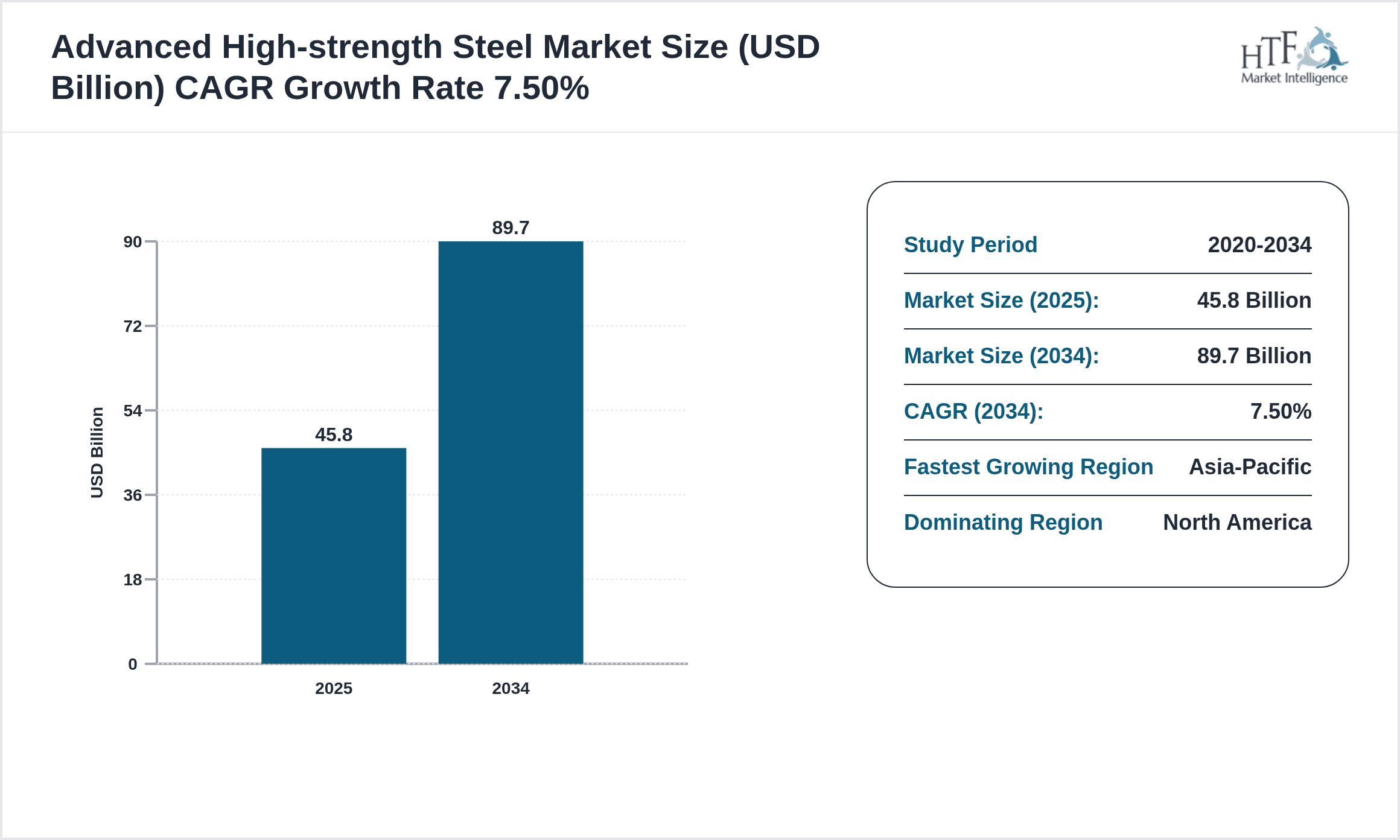

- •The global AHSS market recorded a base size of USD 45.8 Billion in 2025, growing from USD 30.4 Billion in 2020, and is forecasted to reach USD 89.7 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 7.5%. Year-on-year growth sustains at approximately 7.2%, highlighting robust demand across automotive, construction, and heavy machinery applications. The market dynamics are characterized by technological innovation, increasing regulatory pressures for lightweight materials, and expanding end-use industries, all contributing to market expansion. Key market highlights include the dominance of martensitic steel type in terms of revenue, and the fastest adoption of transformation induced plasticity steel due to its superior formability and strength balance. Strategic initiatives by market players, including product development and capacity expansions, further enhance market competitiveness.

- •The value proposition of AHSS lies in its ability to deliver significant weight reduction while maintaining or improving mechanical performance, enabling manufacturers to meet stringent emissions and safety standards without compromising structural integrity. This translates into cost savings, improved fuel efficiency, and enhanced product durability, thereby benefiting automotive OEMs, construction firms, aerospace manufacturers, and heavy machinery producers. From a strategic standpoint, AHSS facilitates innovation in design and functionality, contributing to sustainable manufacturing practices and lifecycle cost optimization. Its increasing adoption worldwide presents lucrative opportunities for stakeholders including raw material suppliers, steel producers, and end-use industries, making AHSS a critical element in the global transition towards advanced materials.

Competitive Landscape

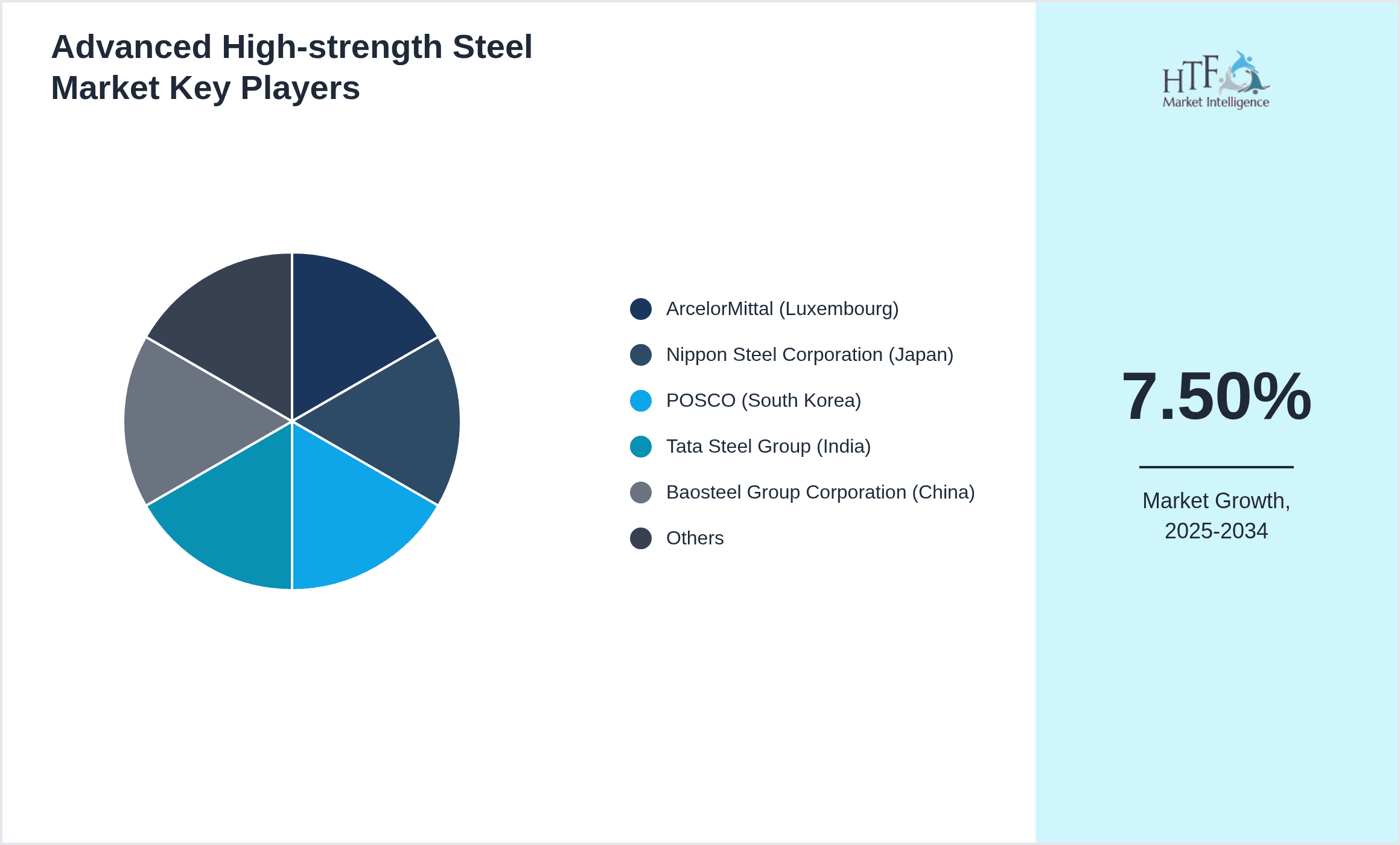

The global Advanced High-strength Steel market is highly competitive with dynamic market participants focusing on innovation, product differentiation, and strategic partnerships to strengthen their market position. Companies deploy diverse competitive strategies including extensive R&D investments to develop new grades of AHSS with improved mechanical properties and cost efficiencies. Market players actively engage in mergers and acquisitions to consolidate their footprint and expand geographical reach, while also forming collaborations with automakers and construction firms to co-develop application-specific steel solutions. Pricing strategies are influenced by raw material costs, production efficiency, and regional demand fluctuations. Distribution channels are optimized for timely delivery and customization to meet client-specific requirements. Technological adoption, such as advanced coating and processing techniques, offers competitive advantages by enhancing product quality and performance. Entry barriers are significant due to high capital investment and technical expertise required, which protects incumbent leaders. Regional competition varies with North America and Europe hosting mature markets, while Asia-Pacific experiences rapid growth fueled by infrastructure development and industrialization. Future trends point to increased focus on sustainability and lightweighting, driving continuous innovation and strategic realignment within the competitive landscape.

Leading Companies in Advanced High-strength Steel Market

- •ArcelorMittal (Luxembourg)

- •Nippon Steel Corporation (Japan)

- •POSCO (South Korea)

- •Tata Steel Group (India)

- •Baosteel Group Corporation (China)

- •ThyssenKrupp AG (Germany)

- •United States Steel Corporation (United States)

- •JSW Steel Ltd. (India)

- •Voestalpine AG (Austria)

- •JFE Steel Corporation (Japan)

- •SSAB AB (Sweden)

- •Nucor Corporation (United States)

- •Severstal (Russia)

- •Gerdau S.A. (Brazil)

- •Metinvest Holding (Ukraine)

- •Evraz plc (United Kingdom)

- •Salzgitter AG (Germany)

- •Hyundai Steel Company (South Korea)

- •China Steel Corporation (Taiwan)

- •Maanshan Iron and Steel Company (China)

- •Kobe Steel, Ltd. (Japan)

- •Ternium S.A. (Luxembourg)

- •Cleveland-Cliffs Inc. (United States)

- •Dongkuk Steel Mill Co., Ltd. (South Korea)

- •SeAH Steel Holdings Corporation (South Korea)

Market Breakdown

- •By Type

- ◦Martensitic Steel

- ◦Dual Phase Steel

- ◦Complex Phase Steel

- ◦Transformation Induced Plasticity (TRIP) Steel

- ◦Ferritic Steel

- •By Application

- ◦Automotive

- ◦Construction

- ◦Shipbuilding

- ◦Heavy Machinery

- ◦Aerospace

- •By Product Form

- ◦Coils

- ◦Sheets

- ◦Plates

- ◦Bars

- •By Coating Type

- ◦Galvanized

- ◦Galvalume

- ◦Electrolytic

- ◦Uncoated

Growth Dynamics

The global Advanced High-strength Steel market growth is primarily driven by the automotive industry's increasing demand for lightweight materials to improve fuel efficiency and comply with stringent emission norms. Manufacturers leverage AHSS to achieve vehicle weight reduction without compromising safety, which is critical for meeting global regulatory standards. Additionally, rapid urbanization and infrastructure development worldwide propel demand in the construction sector, where AHSS contributes to durable and cost-effective building solutions. Technological advancements in steel processing and coating techniques enhance product performance, enabling expanded applications across heavy machinery and aerospace industries. Furthermore, rising consumer awareness about environmental sustainability fosters adoption of AHSS as a greener alternative to conventional steel grades. Government initiatives promoting advanced materials and investments in manufacturing capabilities further support market expansion. Collectively, these factors establish a strong foundation for sustained market growth through the forecast period.

Market Trends

The Advanced High-strength Steel market is witnessing a trend towards increased integration of transformation induced plasticity (TRIP) steels due to their superior balance of strength and ductility, which supports complex automotive designs and enhanced crashworthiness. There is also rising adoption of coated AHSS products that improve corrosion resistance and longevity, especially in harsh environmental conditions. Digitization and Industry 4.0 technologies are influencing production processes, enabling real-time quality monitoring and process optimization. Sustainability trends are encouraging steel producers to focus on eco-friendly manufacturing practices and recycled content incorporation. Moreover, collaborations between steelmakers and automakers are becoming more prevalent, aimed at co-developing innovative materials tailored to future mobility needs such as electric and autonomous vehicles.

Market Opportunities

Emerging economies in Asia-Pacific and Latin America present significant growth opportunities for AHSS owing to rapid industrialization, increasing automotive production, and infrastructure expansion. There is potential to develop new AHSS grades with enhanced formability and strength for electric vehicle applications, addressing the growing demand for battery safety and lightweight chassis components. Expansion into aerospace and heavy machinery sectors by offering customized steel solutions can diversify the market base. Advances in coating and surface treatment technologies provide opportunities to enhance corrosion resistance and durability, opening new application avenues. Strategic partnerships between steel producers and end-users can facilitate market penetration and accelerate product innovation. Additionally, government incentives promoting lightweight materials and sustainable manufacturing create favorable investment landscapes.

Market Challenges

The AHSS market faces challenges including high production costs associated with advanced processing and coating technologies, which can limit adoption in cost-sensitive applications. Technical complexities in welding and forming AHSS require specialized equipment and expertise, posing barriers for smaller manufacturers. Fluctuating raw material prices and supply chain disruptions impact profitability and production stability. Regulatory uncertainties and variations across regions complicate compliance and standardization efforts. Intense competition from alternative lightweight materials such as aluminum and composites presents substitution threats. Additionally, limited recycling infrastructure for AHSS grades can constrain sustainability objectives. Addressing these challenges requires investment in technology, workforce training, and collaborative industry efforts to optimize cost and performance balance.

Regulatory Framework

- •Between 2020 and 2025, governments worldwide have implemented stringent vehicle emission regulations such as Euro 6 and EPA Tier 3 standards, compelling automotive manufacturers to adopt lightweight materials like Advanced High-strength Steel to reduce carbon emissions. Safety regulations, including crashworthiness standards, demand materials that enhance occupant protection, further driving AHSS usage. In construction, building codes increasingly emphasize fire resistance and structural integrity, favoring AHSS applications. Environmental policies focusing on lifecycle emissions and recyclability influence steel manufacturing processes, encouraging sustainable production practices. Regional mandates in North America, Europe, and Asia-Pacific promote advanced material usage through incentives and subsidies. Compliance with REACH and RoHS directives for hazardous substances affects material selection and processing. These regulatory landscapes shape market dynamics by mandating performance criteria and sustainability benchmarks, fostering AHSS innovation and adoption.

- •Enforcement of safety standards such as FMVSS in the United States and NCAP in Europe requires automotive components to meet high-performance thresholds, which AHSS grades effectively support. Anti-dumping duties and trade policies also impact steel supply chains and pricing structures globally. Implementation of ISO standards related to steel quality and environmental management ensures product reliability and corporate responsibility. The regulatory framework continues to evolve with increasing focus on carbon footprint reduction and circular economy principles, influencing R&D priorities. Governments actively support steel industry modernization through grants and funding for green technologies, facilitating AHSS production scalability. Compliance challenges and regional variations necessitate adaptive strategies by manufacturers to align products with diverse regulatory requirements.

- •Environmental regulations targeting reduction of greenhouse gas emissions in steel production, such as the EU Emissions Trading System, have incentivized adoption of energy-efficient manufacturing processes. Regulations promoting use of recycled steel content drive circularity in the AHSS market. Product certification and testing requirements ensure material performance consistency and safety. These frameworks collectively foster development of advanced steel grades with lower environmental impact and superior mechanical properties, enhancing market attractiveness.

- •Country-specific mandates in emerging markets are increasingly aligning with global standards, promoting AHSS adoption in automotive and construction sectors. Governments implement policies to support domestic steel production capabilities with environmental compliance, strengthening regional supply chains. These initiatives contribute to market expansion and competitive advantage for compliant manufacturers.

- •Policy frameworks incorporating incentives for lightweight material integration in transportation and infrastructure projects stimulate AHSS demand. Support programs for research and innovation in advanced materials enhance competitive positioning. Continuous updates to regulatory provisions ensure that AHSS manufacturers maintain alignment with evolving industry requirements, securing market relevance.

Market Intelligence

- •15th January 2025, ArcelorMittal announced the launch of a new generation of transformation induced plasticity (TRIP) steels designed specifically for electric vehicle battery enclosures, offering enhanced strength and corrosion resistance while reducing weight by up to 15%. This product aims to address the growing demand for safer and lighter EV components, supporting automotive manufacturers' sustainability goals. The steel incorporates advanced coating technology to improve durability in harsh environments, positioning ArcelorMittal as a leader in AHSS innovation for next-generation mobility solutions. The strategic initiative aligns with global trends towards electrification and lightweighting, expected to impact market dynamics significantly. Source: ArcelorMittal Official Press Release

- •10th March 2025, POSCO introduced a new complex phase steel grade featuring superior formability and tensile strength, targeting the heavy machinery and construction sectors. The innovation integrates proprietary metallurgical enhancements to deliver improved weldability and fatigue resistance, facilitating longer equipment life and operational efficiency. POSCO's launch is part of its strategy to expand AHSS applications beyond the automotive market, leveraging growing infrastructure investments worldwide. The company emphasized its commitment to sustainability by reducing carbon emissions in the production process. This development is projected to bolster POSCO's competitive positioning in the global AHSS market. Source: POSCO Corporate Announcement

- •20th June 2025, Nippon Steel Corporation announced a strategic partnership with major automotive OEMs to co-develop martensitic steel grades optimized for autonomous vehicle chassis. The collaboration focuses on enhancing crash safety and weight reduction through advanced steel formulations and processing techniques. This initiative reflects the increasing integration of AHSS in emerging mobility technologies and the necessity for tailored material solutions. Nippon Steel aims to accelerate market adoption by aligning product development closely with end-user requirements, thereby driving innovation and strengthening industry ties. The partnership is expected to influence competitive dynamics and foster sustainable growth. Source: Nippon Steel Official Website

- •5th September 2025, Tata Steel Group completed capacity expansion of their AHSS production lines in India, increasing output by 25% to meet rising domestic and export demand. The investment includes modernization of manufacturing facilities to incorporate energy-efficient technologies, reducing environmental impact. Tata Steel's expansion supports the growing infrastructure and automotive sectors in Asia-Pacific, positioning the company to capitalize on the fastest growing regional market. The enhanced production capabilities enable Tata Steel to offer a broader portfolio of AHSS products, strengthening its market presence and competitive advantage. Source: Tata Steel Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.8 Billion |

| Forecast Year Market Size | USD 89.7 Billion |

| CAGR | 7.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.2% |

| Scope of Report | Market is segmented by Type (Martensitic Steel, Dual Phase Steel, Complex Phase Steel, Transformation Induced Plasticity (TRIP) Steel, Ferritic Steel), Application (Automotive, Construction, Shipbuilding, Heavy Machinery, Aerospace), Product Form (Coils, Sheets, Plates, Bars), Coating Type (Galvanized, Galvalume, Electrolytic, Uncoated) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | ArcelorMittal (Luxembourg), Nippon Steel Corporation (Japan), POSCO (South Korea), Tata Steel Group (India), Baosteel Group Corporation (China), ThyssenKrupp AG (Germany), United States Steel Corporation (United States), JSW Steel Ltd. (India), Voestalpine AG (Austria), JFE Steel Corporation (Japan), SSAB AB (Sweden), Nucor Corporation (United States), Severstal (Russia), Gerdau S.A. (Brazil), Metinvest Holding (Ukraine), Evraz plc (United Kingdom), Salzgitter AG (Germany), Hyundai Steel Company (South Korea), China Steel Corporation (Taiwan), Maanshan Iron and Steel Company (China), Kobe Steel, Ltd. (Japan), Ternium S.A. (Luxembourg), Cleveland-Cliffs Inc. (United States), Dongkuk Steel Mill Co., Ltd. (South Korea), SeAH Steel Holdings Corporation (South Korea) |

Global Advanced High-strength Steel Market - Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.