North America Hemoglobin Analyzers Market Size, Growth & Revenue 2025-2034

North America Hemoglobin Analyzers Market is segmented by Hemoglobin Analyzer Type (Automated Hemoglobin Analyzers, Semi-Automated Hemoglobin Analyzers, Portable Hemoglobin Analyzers, Microprocessor-Based Hemoglobin Analyzers, Spectrophotometric Hemoglobin Analyzers), Application Area (Clinical Diagnostics, Point-of-Care Testing, Blood Banks, Research Laboratories, Home Healthcare), Service Delivery Model (Direct Sales, Distributor Sales, Online Retail, After-Sales Support & Maintenance), Deployment Setting (Hospital Laboratories, Diagnostic Centers, Mobile Clinics), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Hemoglobin Analyzers market involves the production and distribution of medical devices designed to quantify hemoglobin levels in blood samples. This market covers a broad range of analyzer types including automated, semi-automated, portable, microprocessor-based, and spectrophotometric analyzers, each tailored for specific clinical and diagnostic needs. Key applications span clinical diagnostics in hospitals, point-of-care testing for immediate results, blood banks for donor screening, research laboratories for experimental assessments, and home healthcare settings enabling patient self-monitoring. The value chain includes raw material suppliers, manufacturers, distributors, healthcare institutions, and end-users. Technological innovations have improved device accuracy, speed, and ease of use, facilitating better patient outcomes. Regulatory frameworks in North America, including FDA approvals, ensure device safety and standardization. Market growth is driven by rising prevalence of anemia and chronic diseases, increasing healthcare expenditure, and the demand for rapid diagnostic tools. The market also reflects a shift towards portable and user-friendly analyzers to support decentralized healthcare services. This comprehensive market analysis covers historical data from 2020, base year 2025, and forecasts through 2034, highlighting growth drivers, challenges, competitive landscape, and emerging opportunities in the region.

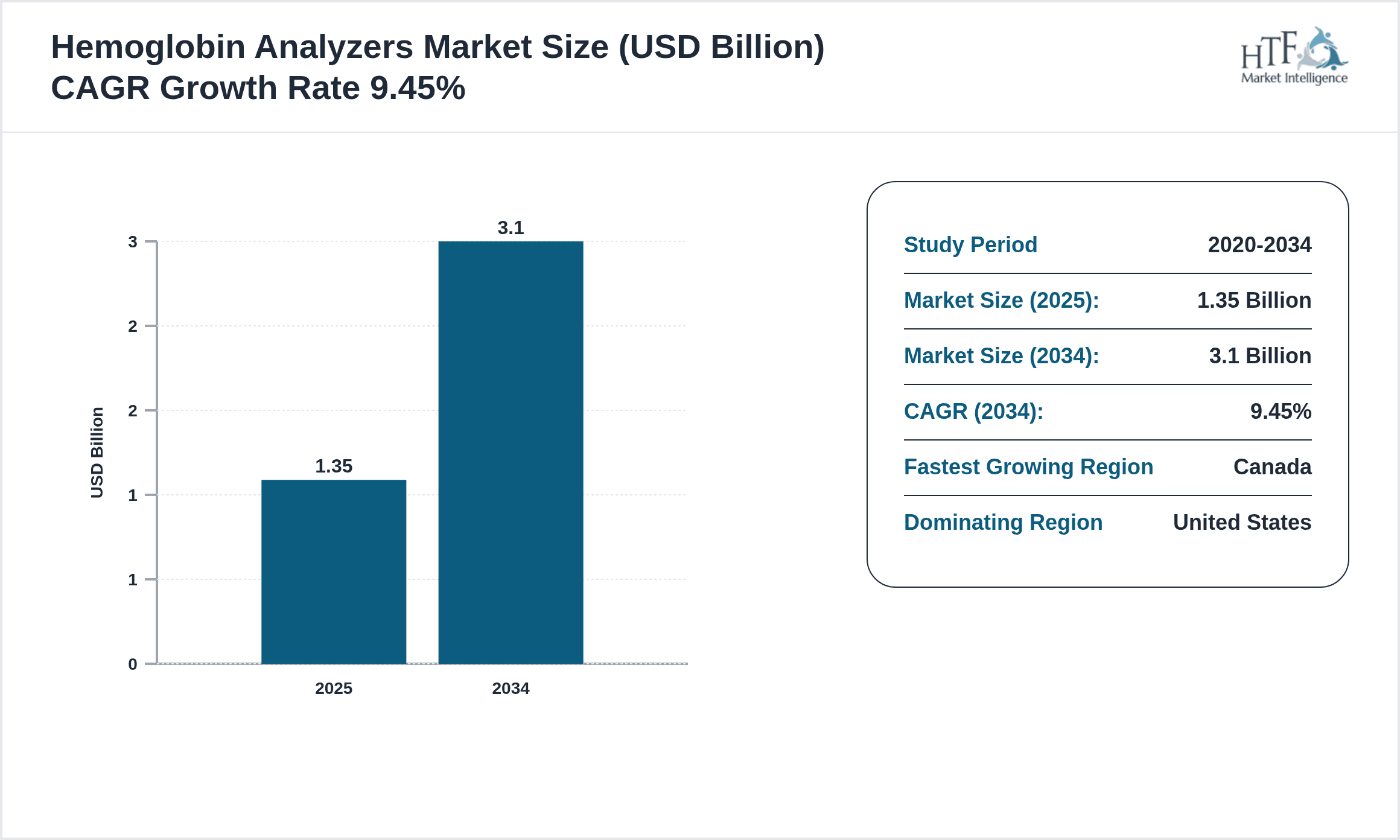

- •Key highlights of the North America Hemoglobin Analyzers market include a base year market valuation of USD 1.35 billion in 2025, with a forecasted expansion to USD 3.10 billion by 2034, reflecting a robust CAGR of 9.45%. The United States dominates the regional market due to its advanced healthcare infrastructure and higher adoption of automated analyzers. Canada is identified as the fastest growing country within the region, driven by increasing investments in healthcare technology and rising rural healthcare access. The leading product segment is automated hemoglobin analyzers, favored for their precision and high throughput, whereas portable analyzers exhibit the fastest growth due to expanding point-of-care testing demands. These trends underscore the growing emphasis on rapid, accurate hemoglobin measurement solutions to enhance patient care and operational efficiency across North American healthcare systems.

- •The North America Hemoglobin Analyzers market presents a significant value proposition for healthcare providers, device manufacturers, and investors. Efficient hemoglobin testing facilitates early diagnosis and management of anemia and related blood disorders, reducing healthcare costs and improving patient outcomes. Strategic importance is heightened by the growing elderly population and rising incidence of chronic conditions requiring frequent blood monitoring. Additionally, advancements in portable and point-of-care analyzers enable decentralized testing, aligning with trends in personalized medicine and home healthcare. Stakeholders benefit from understanding evolving regulatory environments, technological innovations, and market dynamics to capitalize on growth opportunities while addressing challenges such as reimbursement policies and device standardization.

Competitive Landscape

The North America Hemoglobin Analyzers market is characterized by intense competition among established multinational corporations and emerging regional players. Market dynamics are shaped by continuous innovation, strategic partnerships, and mergers and acquisitions aimed at enhancing product portfolios and expanding geographic outreach. Leading companies focus on differentiating through advanced technologies such as microprocessor integration, improved spectrophotometric analysis, and user-friendly interfaces that facilitate rapid and accurate hemoglobin measurement. Pricing strategies are competitive, balancing affordability with high performance and regulatory compliance. Distribution channels are diversified, including direct sales to hospitals and clinics, partnerships with distributors, and growing online platforms for point-of-care devices. Market entry barriers include stringent regulatory approvals, high R&D costs, and the need for clinical validation. Regional competition also influences product customization to meet specific healthcare infrastructure needs and reimbursement frameworks. Future competitive trends will likely emphasize digital connectivity, data integration with electronic health records, and enhanced portable analyzer capabilities to capture expanding market segments and foster patient-centric care.

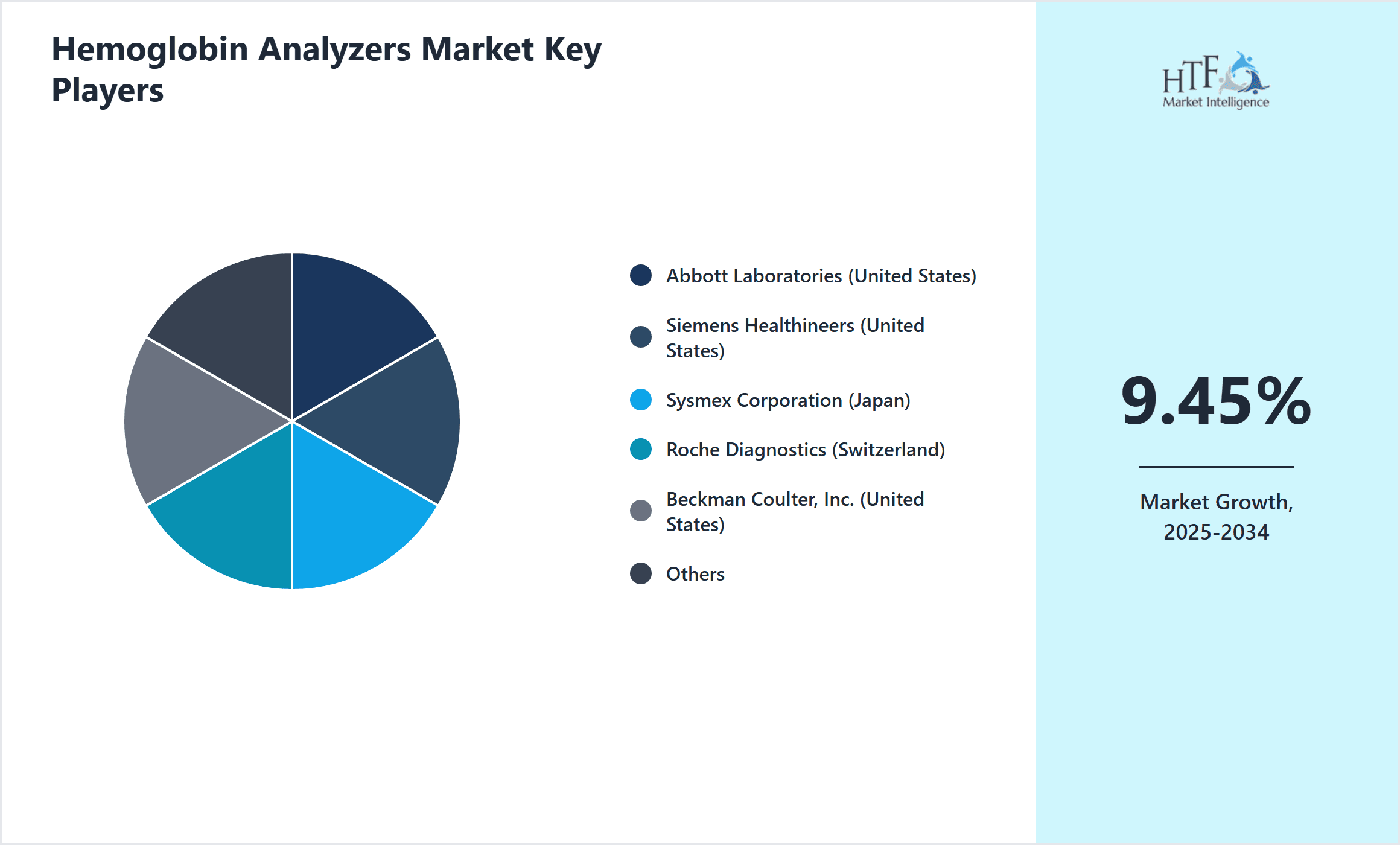

Leading Companies in North America Hemoglobin Analyzers Market

- •Abbott Laboratories (United States)

- •Siemens Healthineers (United States)

- •Sysmex Corporation (Japan)

- •Roche Diagnostics (Switzerland)

- •Beckman Coulter, Inc. (United States)

- •Nova Biomedical Corporation (United States)

- •Horiba, Ltd. (Japan)

- •EKF Diagnostics Holdings Plc (United Kingdom)

- •Becton, Dickinson and Company (United States)

- •HemoCue AB (Sweden)

- •Mindray Medical International Limited (China)

- •Analytik Jena AG (Germany)

- •Siemens AG (Germany)

- •OrSense Ltd. (Israel)

- •Sarstedt AG & Co. KG (Germany)

- •DiaSpect Medical Holding AG (Switzerland)

- •Ortho Clinical Diagnostics (United States)

- •Luminex Corporation (United States)

- •Quidel Corporation (United States)

- •Trivitron Healthcare (India)

- •Siemens Healthcare Diagnostics Inc. (United States)

- •Peloton Advantage, Inc. (United States)

- •Arkray, Inc. (Japan)

- •Partec GmbH (Germany)

- •Tosoh Bioscience, Inc. (United States)

Market Breakdown

- •By Hemoglobin Analyzer Type

- ◦Automated Hemoglobin Analyzers

- ◦Semi-Automated Hemoglobin Analyzers

- ◦Portable Hemoglobin Analyzers

- ◦Microprocessor-Based Hemoglobin Analyzers

- ◦Spectrophotometric Hemoglobin Analyzers

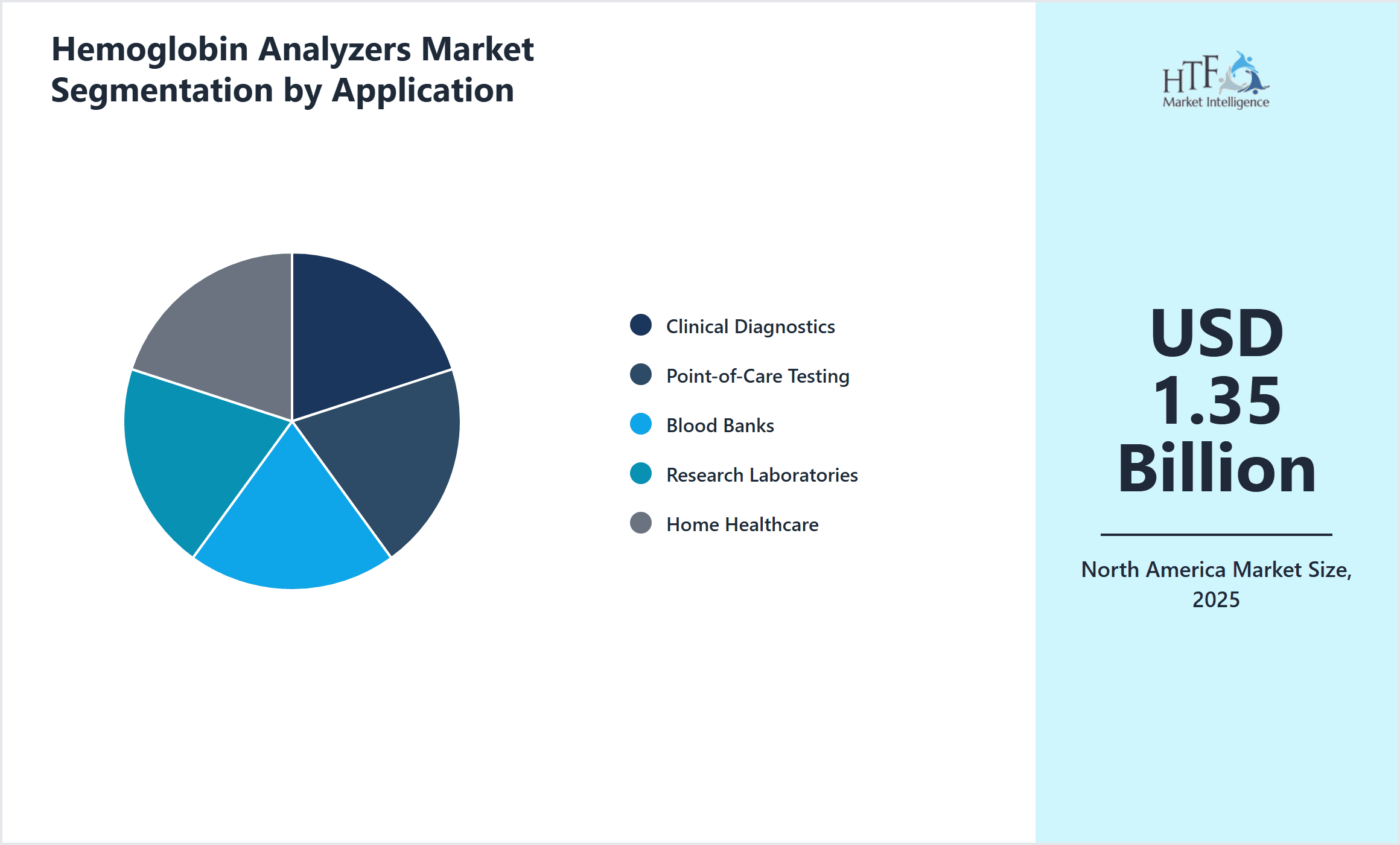

- •By Application Area

- ◦Clinical Diagnostics

- ◦Point-of-Care Testing

- ◦Blood Banks

- ◦Research Laboratories

- ◦Home Healthcare

- •By Service Delivery Model

- ◦Direct Sales

- ◦Distributor Sales

- ◦Online Retail

- ◦After-Sales Support & Maintenance

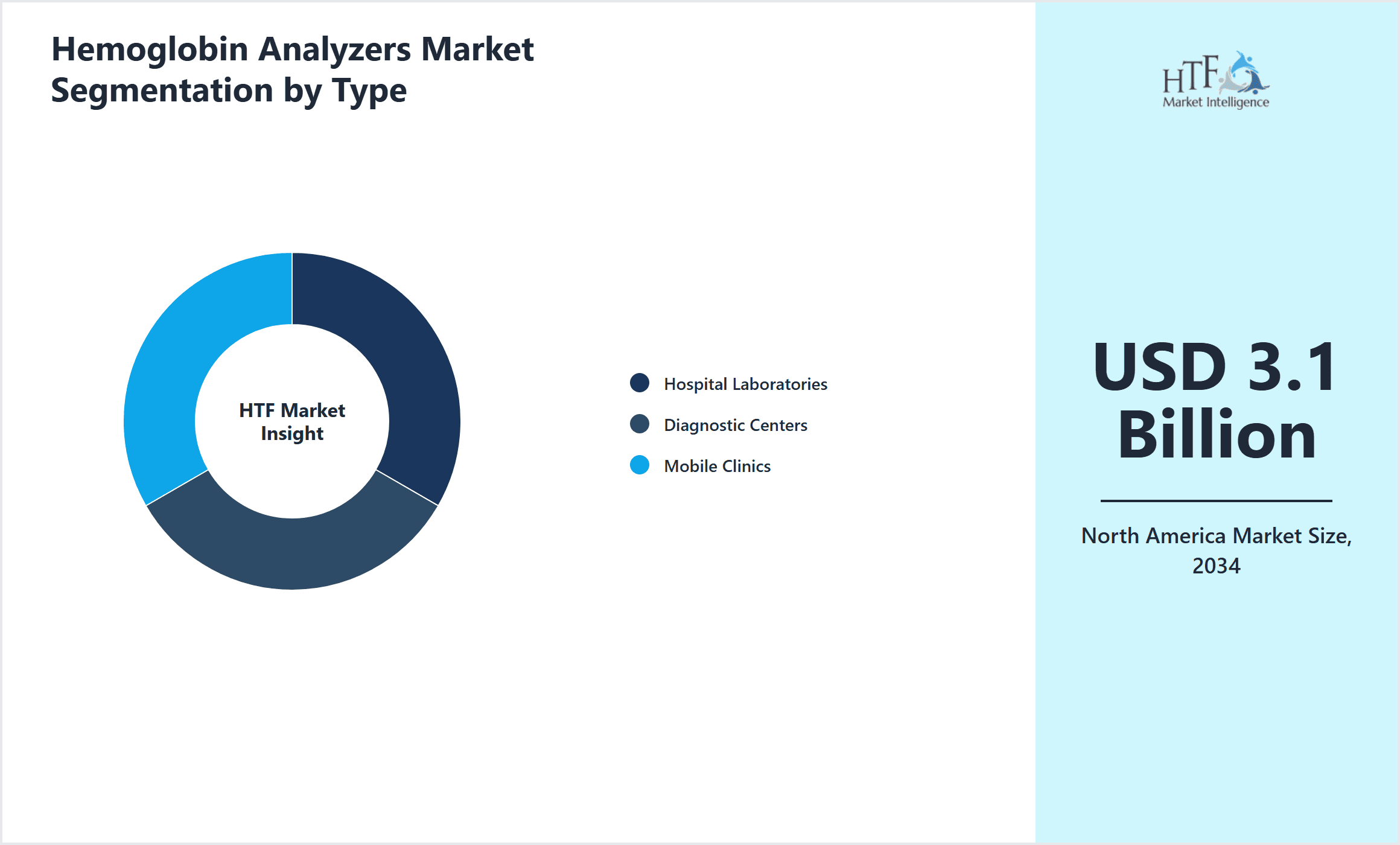

- •By Deployment Setting

- ◦Hospital Laboratories

- ◦Diagnostic Centers

- ◦Mobile Clinics

Growth Dynamics

- •The increasing prevalence of anemia and chronic diseases such as diabetes and kidney disorders in North America is a key growth driver, fueling demand for reliable hemoglobin analyzers to enable timely diagnosis and treatment monitoring. Healthcare providers are adopting advanced automated analyzers to improve accuracy and throughput, significantly enhancing patient management efficiency.

- •Technological advancements including the development of portable and point-of-care hemoglobin analyzers are expanding accessibility in remote and underserved regions. These compact devices allow rapid, on-site testing, reducing turnaround time and supporting decentralized healthcare delivery models.

- •Rising healthcare expenditure and increased government initiatives to modernize diagnostic infrastructure have stimulated investments in advanced hemoglobin analysis equipment. This economic support facilitates procurement by hospitals and diagnostic centers, accelerating market growth.

- •Growing awareness among consumers and healthcare professionals regarding early detection of blood disorders is leading to higher adoption rates of hemoglobin analyzers, especially in outpatient and home healthcare settings where frequent monitoring is critical.

- •Integration of data analytics and connectivity features in hemoglobin analyzers enhances clinical decision-making and streamlines workflow, attracting healthcare providers to upgrade existing equipment and adopt new solutions.

Market Trends

- •There is a significant shift towards portable and handheld hemoglobin analyzers that support point-of-care testing, driven by the need for rapid diagnostics and patient-centric care models in North America. These devices are gaining traction in emergency care and home healthcare due to convenience and accuracy.

- •Manufacturers are increasingly incorporating microprocessor technology and advanced spectrophotometric methods to enhance analyzer precision and reduce sample volume requirements, aligning with clinical demands for minimal invasiveness.

- •Digital health integration is becoming prevalent, with hemoglobin analyzers offering connectivity options to electronic health records (EHRs) and hospital information systems (HIS), facilitating seamless data sharing and improved patient monitoring.

- •Sustainability and eco-friendly designs are emerging trends, with companies focusing on reducing reagent waste and enhancing energy efficiency in analyzer operations to comply with environmental regulations and appeal to environmentally conscious consumers.

- •Collaborations between device manufacturers and healthcare providers are increasing to co-develop tailored hemoglobin analyzer solutions that meet specific clinical workflow needs, enhancing adoption rates and customer satisfaction.

Market Opportunities

- •Expanding telemedicine and home healthcare services in North America present opportunities for portable hemoglobin analyzers that empower patients to conduct self-monitoring, thereby improving chronic disease management and reducing hospital visits.

- •Emerging applications of hemoglobin analyzers in blood banks and research laboratories open avenues for specialized device development, including enhanced accuracy and rapid throughput features tailored to high-volume testing environments.

- •Investment in integrating artificial intelligence and machine learning algorithms within hemoglobin analyzers can optimize diagnostics accuracy and predictive analytics, offering competitive advantages for manufacturers.

- •Geographic expansion within underserved regions of North America, such as rural areas and smaller clinics, represents a growth opportunity by addressing gaps in diagnostic accessibility with affordable, easy-to-use analyzers.

- •Strategic partnerships and collaborations between technology firms and healthcare providers can accelerate innovation cycles and market penetration for new hemoglobin analyzer models featuring enhanced connectivity and usability.

Market Challenges

- •Stringent regulatory requirements and lengthy approval processes in North America can delay the introduction of new hemoglobin analyzer models, affecting time-to-market and competitive positioning for manufacturers.

- •High costs associated with advanced automated hemoglobin analyzers and maintenance services can limit adoption in smaller healthcare facilities and budget-constrained settings, restraining market growth.

- •Variability in reimbursement policies across states and healthcare providers creates uncertainty for end-users, impacting purchasing decisions and overall market demand for hemoglobin analyzers.

- •Technical challenges such as calibration requirements, sample handling complexity, and device interoperability issues may hinder seamless integration into existing clinical workflows, affecting user satisfaction.

- •Competition from alternative diagnostic technologies and methods, including non-invasive anemia screening tools, poses a risk by potentially reducing reliance on traditional hemoglobin analyzers.

Regulatory Framework

- •The U.S. Food and Drug Administration (FDA) regulates hemoglobin analyzers under medical device classification, with premarket notification (510(k)) or premarket approval (PMA) required depending on device risk classification. Between 2020 and 2025, the FDA has tightened guidelines on device accuracy and labeling to enhance patient safety.

- •The Clinical Laboratory Improvement Amendments (CLIA) set quality standards for laboratory testing, including hemoglobin analyzers. Compliance with CLIA regulations ensures reliability of test results and is mandatory for diagnostic laboratories in North America.

- •Health Canada enforces medical device regulations for hemoglobin analyzers, requiring device licensing and adherence to safety and performance standards. Between 2020 and 2025, regulatory updates have emphasized post-market surveillance and adverse event reporting.

- •The U.S. Centers for Medicare & Medicaid Services (CMS) influences market dynamics through reimbursement policies tied to hemoglobin testing procedures, shaping device adoption in clinical settings.

- •Government initiatives to support medical device innovation include expedited review pathways and grants for developing point-of-care diagnostic tools, fostering market growth and technological advancement within the hemoglobin analyzer segment.

Market Intelligence

- •15th January 2025, Abbott Laboratories launched its next-generation portable hemoglobin analyzer designed for point-of-care testing in outpatient clinics and home healthcare settings. The device features advanced microprocessor technology enabling rapid analysis with high precision, minimal sample volume, and seamless integration with electronic health records. Abbott’s strategic objective is to capture the growing demand for decentralized diagnostic solutions in North America, particularly targeting rural and underserved populations. The product rollout is supported by comprehensive training programs and a robust after-sales service network to ensure optimal adoption and patient care improvements. Source: Abbott Laboratories official press release.

- •10th March 2025, Siemens Healthineers introduced an automated hemoglobin analyzer with enhanced spectrophotometric capabilities, delivering faster throughput and improved accuracy suitable for high-volume hospital laboratories. The device incorporates AI-powered data analytics to assist clinicians in interpreting results and predicting anemia-related complications. Positioned as a premium offering, this innovation aims to strengthen Siemens’ leadership in the clinical diagnostics space across North America. The launch was accompanied by strategic partnerships with leading healthcare providers to facilitate early adoption and real-world validation. Source: Siemens Healthineers corporate announcement.

- •22nd June 2025, Roche Diagnostics announced a strategic collaboration with a major telehealth provider to integrate its portable hemoglobin analyzers with remote patient monitoring platforms. This initiative targets chronic disease management programs by enabling patients to perform home-based hemoglobin testing with real-time data transmission to healthcare professionals. The partnership is expected to accelerate adoption of point-of-care analyzers and expand Roche’s market share in North America’s evolving healthcare ecosystem. The collaboration aligns with broader trends in digital health and personalized medicine. Source: Roche Diagnostics press release.

- •Market Intelligence: Recent developments and industry insights are being monitored. For the latest updates, consult official company announcements and industry publications.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.35 Billion |

| Forecast Year Market Size | USD 3.1 Billion |

| CAGR | 9.45% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.08% |

| Scope of Report | Market is segmented by Hemoglobin Analyzer Type (Automated Hemoglobin Analyzers, Semi-Automated Hemoglobin Analyzers, Portable Hemoglobin Analyzers, Microprocessor-Based Hemoglobin Analyzers, Spectrophotometric Hemoglobin Analyzers), Application Area (Clinical Diagnostics, Point-of-Care Testing, Blood Banks, Research Laboratories, Home Healthcare), Service Delivery Model (Direct Sales, Distributor Sales, Online Retail, After-Sales Support & Maintenance), Deployment Setting (Hospital Laboratories, Diagnostic Centers, Mobile Clinics) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Abbott Laboratories (United States), Siemens Healthineers (United States), Sysmex Corporation (Japan), Roche Diagnostics (Switzerland), Beckman Coulter, Inc. (United States), Nova Biomedical Corporation (United States), Horiba, Ltd. (Japan), EKF Diagnostics Holdings Plc (United Kingdom), Becton, Dickinson and Company (United States), HemoCue AB (Sweden), Mindray Medical International Limited (China), Analytik Jena AG (Germany), Siemens AG (Germany), OrSense Ltd. (Israel), Sarstedt AG & Co. KG (Germany), DiaSpect Medical Holding AG (Switzerland), Ortho Clinical Diagnostics (United States), Luminex Corporation (United States), Quidel Corporation (United States), Trivitron Healthcare (India), Siemens Healthcare Diagnostics Inc. (United States), Peloton Advantage, Inc. (United States), Arkray, Inc. (Japan), Partec GmbH (Germany), Tosoh Bioscience, Inc. (United States) |

North America Hemoglobin Analyzers Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.