Global Automotive Starter Motor and Alternator Market Size, Growth & Revenue 2025-2034

Global Automotive Starter Motor and Alternator Market is segmented by Application (Passenger Cars, Commercial Vehicles, Electric Vehicles, Two Wheelers, Off-Highway Vehicles), Type (Starter Motors, Alternators, Integrated Starter Alternators, Brushless Starter Motors, High Output Alternators), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global automotive starter motor and alternator market is a critical component of the automotive industry that focuses on the electrical systems responsible for engine ignition and electrical energy management. The market comprises starter motors which convert electrical energy from the battery into mechanical energy to start the engine and alternators that recharge the battery and power electrical accessories during engine operation. It spans multiple vehicle types, including passenger cars, commercial vehicles, electric vehicles, two wheelers, and off-highway vehicles, reflecting its broad application scope. The increasing demand for fuel-efficient and emission-compliant vehicles has propelled the adoption of advanced starter motor and alternator technologies such as integrated starter alternators and brushless motors. These components are pivotal to vehicle reliability, performance optimization, and meeting stringent environmental regulations globally. The market involves key players investing in research and development to innovate and cater to evolving automotive electrical system requirements, positioning it as essential to automotive electrification and hybridization strategies.

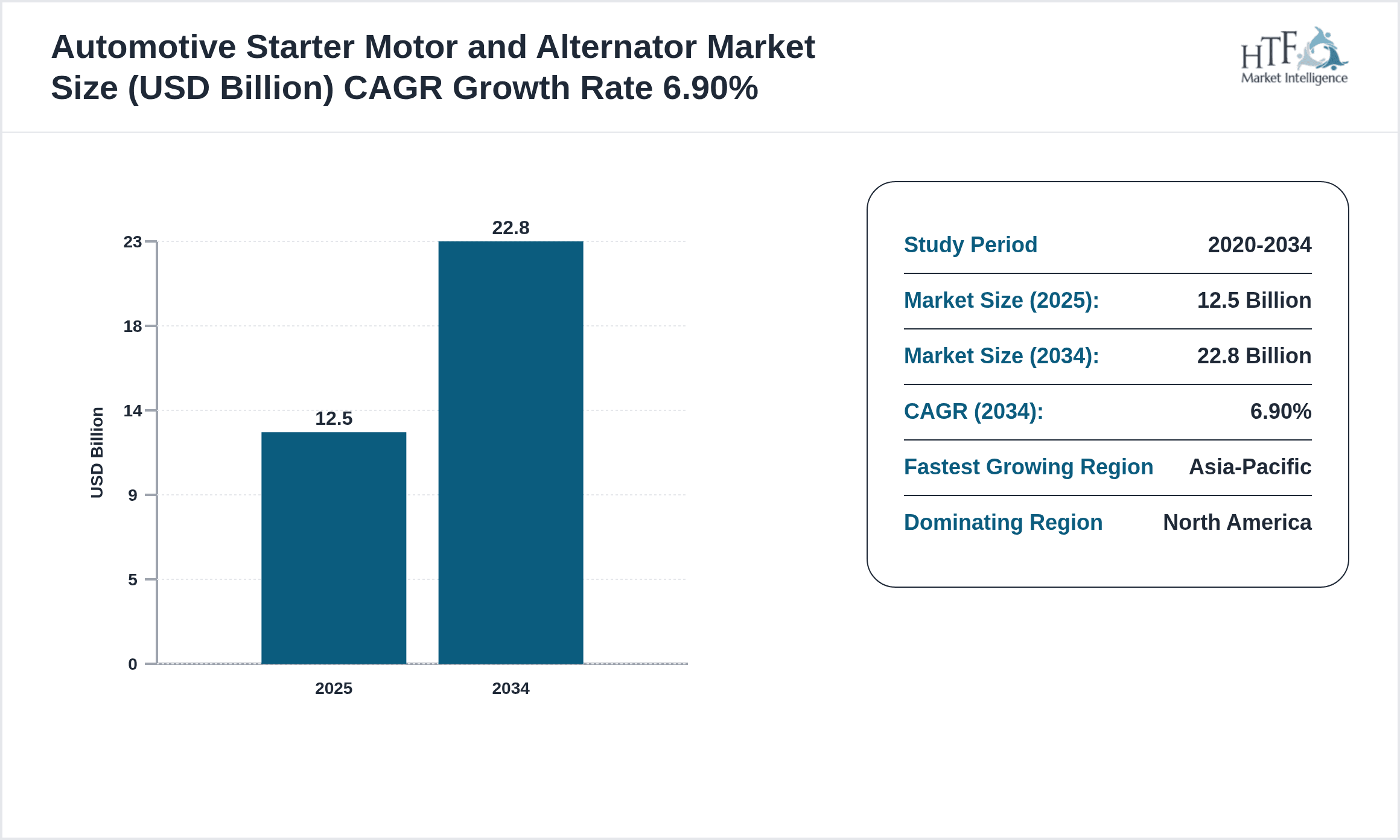

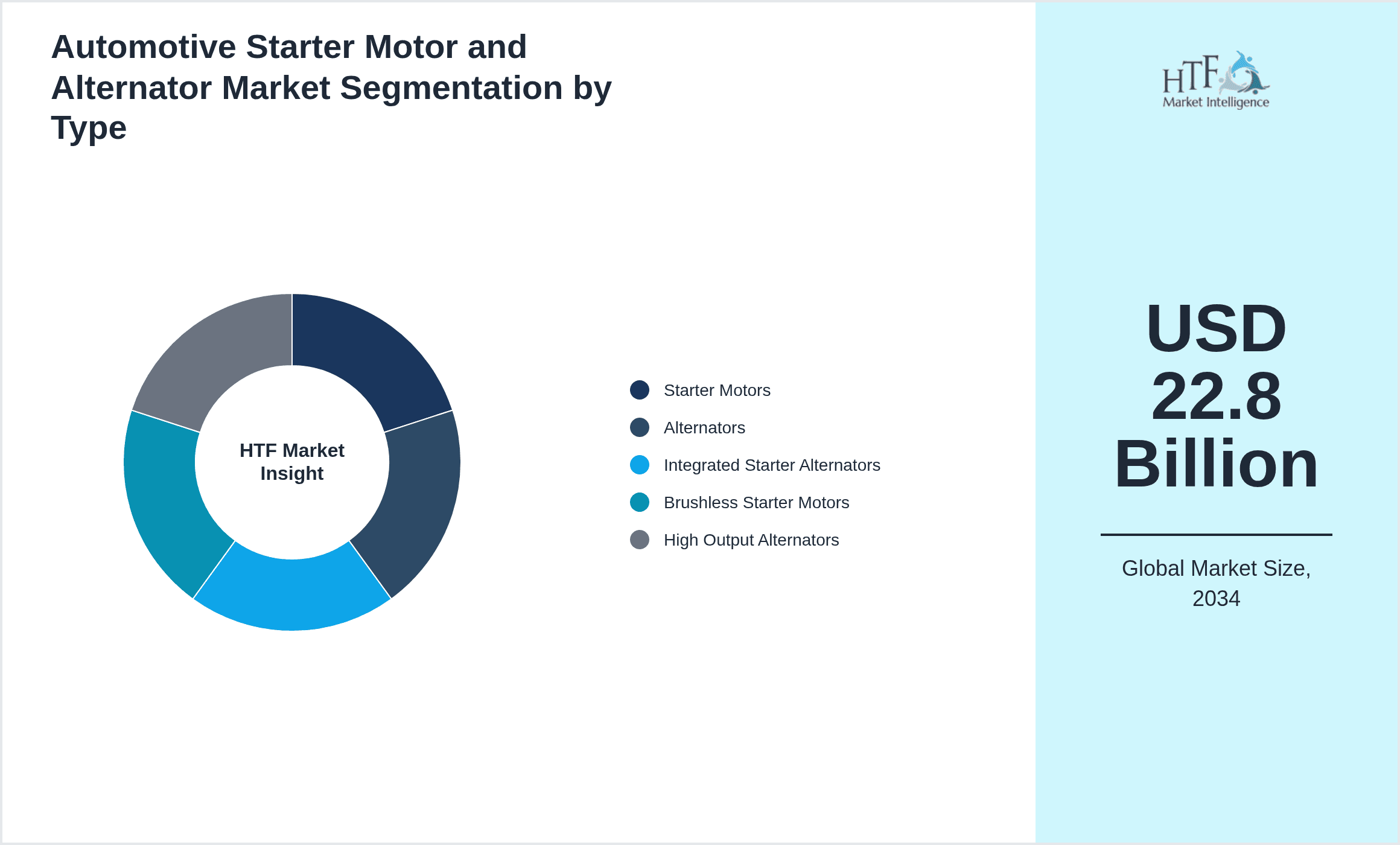

- •Market highlights reveal a robust growth trajectory with a compound annual growth rate of 6.9% projected from 2025 to 2034, driven by accelerating vehicle production worldwide and the transition toward electrification. The base market size in 2025 stands at USD 12.5 billion, expected to reach USD 22.8 billion by 2034, reflecting increased adoption of advanced starter-alternator systems. North America currently dominates the market due to high vehicle output and technological advancements, while Asia-Pacific exhibits the fastest growth, fueled by rapid automotive sector expansion and increasing electric vehicle penetration. Starter motors maintain the largest share due to their fundamental role, but integrated starter alternators are gaining traction with superior efficiency and emission benefits, marking them as the fastest growing product type. Passenger cars remain the predominant application segment, supported by commercial vehicles and electric vehicles, which are anticipated to ramp up demand significantly in the forecast period.

- •The automotive starter motor and alternator market offers significant value to original equipment manufacturers, aftermarket suppliers, and end users by enhancing vehicle functionality and sustainability. Its strategic importance is underscored by the integration of cutting-edge technologies that improve fuel economy and reduce emissions, aligning with global environmental mandates. The market supports multiple stakeholders by fostering innovation in hybrid and electric vehicle platforms, enabling seamless engine starts and efficient power management. Investments in advanced materials, manufacturing processes, and smart electrical components are transforming market dynamics, providing competitive advantages and new revenue streams. This market's growth prospects encourage partnerships across the supply chain, from component manufacturers to vehicle assemblers, ensuring resilience and adaptability in a rapidly evolving automotive landscape.

Competitive Landscape

The global automotive starter motor and alternator industry operates within a highly competitive environment where companies leverage diverse strategies to strengthen market presence and sustain growth. Key players focus on continuous product innovation, incorporating advanced technologies such as integrated starter alternators and brushless motor designs to meet stringent emission norms and fuel efficiency requirements. Strategic partnerships and collaborations with automotive OEMs enable tailored solutions that enhance vehicle performance and reliability. Global expansion through establishing manufacturing facilities and distribution networks in emerging markets, particularly in Asia-Pacific and Latin America, supports broader customer reach and cost optimization. Mergers and acquisitions facilitate consolidation, allowing companies to expand product portfolios and technological capabilities. Emphasis on sustainability and integration of smart electrical systems reflects in R&D investments, while competitive pricing and quality differentiation remain critical for market share retention. Companies also adopt digital transformation in supply chain management and customer engagement to enhance operational efficiency and responsiveness. Overall, the competitive landscape is characterized by innovation-driven growth, strategic alliances, and regional diversification to capitalize on evolving automotive trends worldwide.

Major Automotive Starter Motor and Alternator Industry Players

- •Delphi Technologies (United States)

- •Denso Corporation (Japan)

- •Bosch Automotive (Germany)

- •Valeo SA (France)

- •Magneti Marelli (Italy)

- •Hitachi Automotive Systems (Japan)

- •Mitsubishi Electric Corporation (Japan)

- •Johnson Electric Holdings (Hong Kong)

- •ACDelco (United States)

- •Calsonic Kansei (Japan)

- •Lucas TVS (India)

- •Nippon Denso (Japan)

- •Valeo Siemens eAutomotive (France)

- •Magneti Marelli Powertrain (Italy)

- •Hitachi Automotive Electric Motor Systems (Japan)

- •Johnson Controls (United States)

- •Stanley Electric Co. (Japan)

- •Robert Bosch GmbH (Germany)

- •Denso International America (United States)

- •Prestolite Electric Inc. (United States)

Market Segmentation

- •By Type

- ◦Starter Motors

- ◦Alternators

- ◦Integrated Starter Alternators

- ◦Brushless Starter Motors

- ◦High Output Alternators

- •By Application

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Two Wheelers

- ◦Off-Highway Vehicles

- •By Vehicle Technology

- ◦Internal Combustion Engine Vehicles

- ◦Hybrid Electric Vehicles

- ◦Battery Electric Vehicles

- •By Distribution Channel

- ◦OEM

- ◦Aftermarket

Growth Dynamics

Robust growth in automotive production and rising adoption of electric and hybrid vehicles propel demand for advanced starter motors and alternators. The shift toward integrated starter alternator systems enhances fuel efficiency and reduces emissions, aligning with global regulations and consumer expectations. Increasing replacement needs in mature vehicle markets stimulate aftermarket growth, while OEMs focus on lightweight and compact designs to improve overall vehicle performance. Technological advancements such as brushless starter motors introduce higher durability and lower maintenance, attracting significant industry investment. Government incentives for electrification and stringent emission norms particularly in North America and Europe catalyze market expansion. Strategic collaborations between automotive component manufacturers and vehicle producers foster innovation and accelerate deployment of next-generation electrical systems. The growth is further supported by rapid urbanization and rising disposable incomes in Asia-Pacific, fueling vehicle sales and electrification trends. Real-time examples include Denso's launch of integrated starter generator systems in hybrid vehicles and Bosch's development of brushless starter motors enhancing engine start-stop functionality.

Market Trends

The trend toward electrification is reshaping the automotive starter motor and alternator market with increasing integration of starter-alternator units in mild hybrid vehicles. Innovations in brushless motor technology improve efficiency and reduce noise, supporting enhanced driver comfort and regulatory compliance. Growing adoption of smart electrical systems enables real-time monitoring and diagnostics, facilitating predictive maintenance and reducing downtime. Manufacturers emphasize lightweight materials and compact designs to meet the demands of electric and hybrid vehicle platforms. Digitalization in manufacturing processes and supply chain optimization enhance product quality and reduce lead times. Market participants also explore renewable energy sources and sustainable manufacturing practices to align with environmental priorities. Recent developments such as Valeo’s launch of a 48V integrated starter alternator for hybrid electric vehicles exemplify the market’s technological evolution. Additionally, collaborations between startups and established players foster innovation ecosystems focused on next-generation automotive electrical components.

Market Opportunities

Expanding electric vehicle markets present significant opportunities for integrated starter alternators that optimize energy recovery and improve fuel economy. Geographic expansion into emerging markets with growing automotive demand offers avenues for increased sales and manufacturing investments. Advancements in brushless starter motor technologies enable entry into commercial vehicle and off-highway segments requiring higher durability and efficiency. The aftermarket segment benefits from rising vehicle parc and demand for replacement parts, especially in regions with aging fleets. Strategic partnerships with OEMs facilitate tailored solutions for hybrid and electric platforms, unlocking new revenue streams. Technological convergence with IoT and connected vehicle systems opens avenues for smart starter and alternator diagnostics and predictive maintenance. Industry initiatives toward sustainability encourage adoption of eco-friendly materials and manufacturing processes, enhancing brand reputation and compliance. Recent collaborations such as Bosch and automotive OEMs developing integrated starter-alternator systems for hybrid trucks illustrate the market’s untapped potential across segments and geographies.

Market Challenges

High costs associated with developing and integrating advanced starter motor and alternator technologies pose significant barriers, especially for cost-sensitive segments and emerging markets. Complex regulatory requirements across different regions create compliance challenges and increase operational expenses. The transition to fully electric vehicles threatens to reduce demand for traditional starter motors and alternators, pressuring manufacturers to innovate or diversify product portfolios. Supply chain disruptions, including semiconductor shortages and raw material price volatility, impact production schedules and profitability. Competition from low-cost manufacturers pressures pricing strategies and margins. Additionally, technical challenges in ensuring compatibility and reliability of integrated starter-alternator systems in diverse vehicle platforms require continuous R&D investment. Recent industry reports highlight delays in product launches due to component shortages, exemplified by supply constraints faced by major players during global semiconductor crises. These challenges necessitate strategic agility and innovation to maintain competitiveness in a rapidly evolving market landscape.

Regulatory Framework

Recent regulatory developments emphasize stringent emission standards and fuel efficiency mandates globally, directly influencing the design and adoption of automotive starter motors and alternators. The European Union’s Euro 7 emission standards, introduced between 2022 and 2025, require more efficient electrical systems to reduce pollutant output, promoting integrated starter alternator technologies. Similarly, the U.S. Corporate Average Fuel Economy standards revised in 2023 mandate improvements in vehicle powertrain efficiency, encouraging manufacturers to deploy advanced starter motor and alternator solutions. China’s New Energy Vehicle policies enacted in 2021 incentivize adoption of electrified vehicle components, including integrated starter-alternator systems. Safety and performance regulations also require compliance with international standards such as ISO 26262 for functional safety of electrical systems in vehicles. These regulations drive innovation and standardization efforts while increasing compliance costs for manufacturers, shaping product development strategies and market dynamics worldwide.

Recent Industry Insights

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Recent Merger and Acquisition

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 22.8 Billion |

| CAGR | 6.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.7% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Delphi Technologies (United States), Denso Corporation (Japan), Bosch Automotive (Germany), Valeo SA (France), Magneti Marelli (Italy), Hitachi Automotive Systems (Japan), Mitsubishi Electric Corporation (Japan), Johnson Electric Holdings (Hong Kong), ACDelco (United States), Calsonic Kansei (Japan), Lucas TVS (India), Nippon Denso (Japan), Valeo Siemens eAutomotive (France), Magneti Marelli Powertrain (Italy), Hitachi Automotive Electric Motor Systems (Japan), Johnson Controls (United States), Stanley Electric Co. (Japan), Robert Bosch GmbH (Germany), Denso International America (United States), Prestolite Electric Inc. (United States) |

Global Automotive Starter Motor and Alternator Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Market market is projected to grow at a steady CAGR from 2025 to 2030, driven by increasing demand and expansion in various applications.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.