Global Chromite Market Size, Growth & Revenue 2025-2034

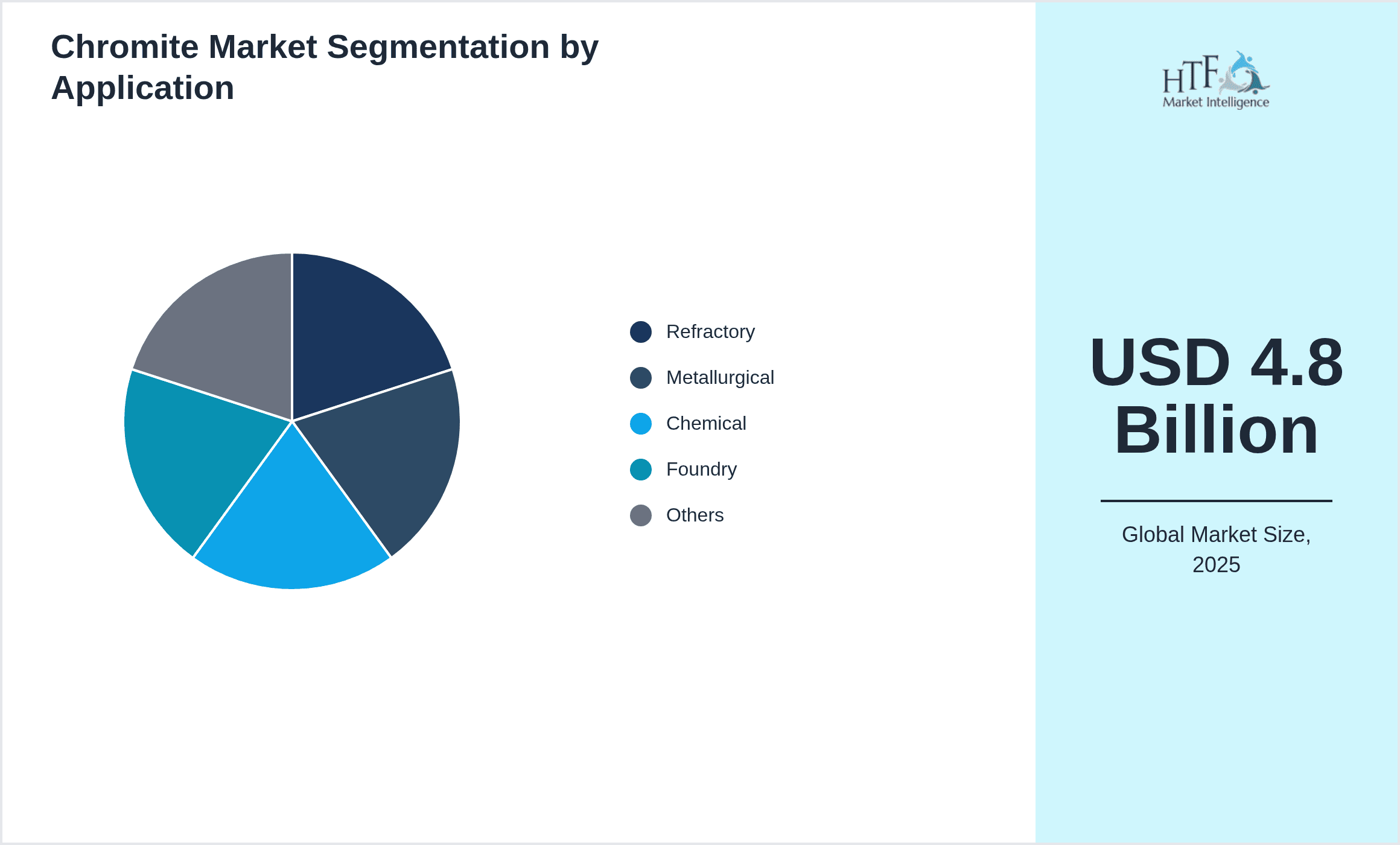

Global Chromite Market is segmented by Application (Refractory, Metallurgical, Chemical, Foundry, Others), Type (Lumpy Chromite, Fines Chromite, Concentrate Chromite, Pelletized Chromite, Others), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global chromite market is defined by the mining, processing, and application of chromite ore, a vital raw material predominantly used in the production of ferrochrome for stainless steel manufacturing. Chromite's exceptional resistance to heat and chemical corrosion makes it indispensable in refractory industries, where it is used to manufacture bricks and linings for high-temperature furnaces. Additionally, chromite serves as a key input in chemical industries for producing chromium compounds utilized in pigments, leather tanning, and wood preservation. The market is segmented by product types such as lumpy chromite, fines, concentrates, and pelletized chromite, each strategically developed for specific industrial applications. Geographically, the market spans major regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, reflecting diverse mining capacities and consumption patterns. The market growth is driven by rising demand from metallurgical sectors, rapid urbanization, and expansions in automotive and infrastructure industries globally. However, regulatory frameworks targeting sustainable mining practices and environmental protection present challenges that necessitate innovation and adaptation within the industry. The market outlook indicates a robust CAGR fueled by technological improvements in ore beneficiation and increasing investments in mining capacities, positioning chromite as a critical material in the global industrial ecosystem.

- •Key market highlights include a base market size of USD 4.8 Billion in 2025, projected to nearly double to USD 9.6 Billion by 2034, exhibiting a CAGR of 7.9%. The Asia-Pacific region dominates the market, accounting for the largest share due to abundant chromite reserves and extensive stainless steel production. Latin America is identified as the fastest growing region, attributed to rising mining activities and expanding metallurgical industries. Lumpy chromite remains the leading product type due to its widespread use in furnace linings and metallurgical processes, while pelletized chromite is the fastest growing segment, driven by innovations in pellet preparation improving furnace efficiencies. Year-on-year growth averages 7.7%, underscoring consistent market expansion fueled by infrastructure developments and industrialization across emerging economies.

- •The chromite market offers significant value propositions across multiple industries, notably in metal production, refractory manufacturing, and chemical processing. Its strategic importance lies in enabling stainless steel production, which is essential for construction, automotive, and manufacturing sectors worldwide. Stakeholders including mining companies, ferrochrome producers, chemical manufacturers, and end-users benefit from the market's expansion through supply chain integration, technological advancements, and evolving applications. The market’s resilience against economic fluctuations and alignment with sustainability initiatives further enhance its attractiveness for investment and innovation, positioning chromite as a cornerstone mineral resource for industrial growth and technological progress globally.

Competitive Landscape

The global chromite market exhibits a moderately concentrated competitive environment characterized by key mining companies, ferrochrome producers, and chemical manufacturers striving for market share through strategic expansion, innovation, and sustainability initiatives. Industry players focus on enhancing beneficiation techniques to improve product quality and reduce environmental impact, aligning with tightening regulatory norms. Competitive strategies include vertical integration to secure raw material supply, investments in green mining technologies, and diversification of product portfolios to cater to varied industrial applications. Market positioning revolves around geographic presence in chromite-rich regions, cost-efficient operations, and establishing long-term supply agreements with stainless steel manufacturers. Mergers and acquisitions, joint ventures, and partnerships are prevalent to consolidate market position and access emerging markets. Pricing strategies are influenced by global chromium ore availability, demand fluctuations in stainless steel production, and geopolitical factors affecting trade. Distribution networks leverage both direct contracts and third-party intermediaries to optimize reach and service levels. Technological adoption such as advanced mineral processing and digital monitoring enhances operational efficiency and product consistency. Future competitive trends point toward increased focus on sustainability, circular economy integration, and expanding downstream applications, driving innovation and reshaping market dynamics globally.

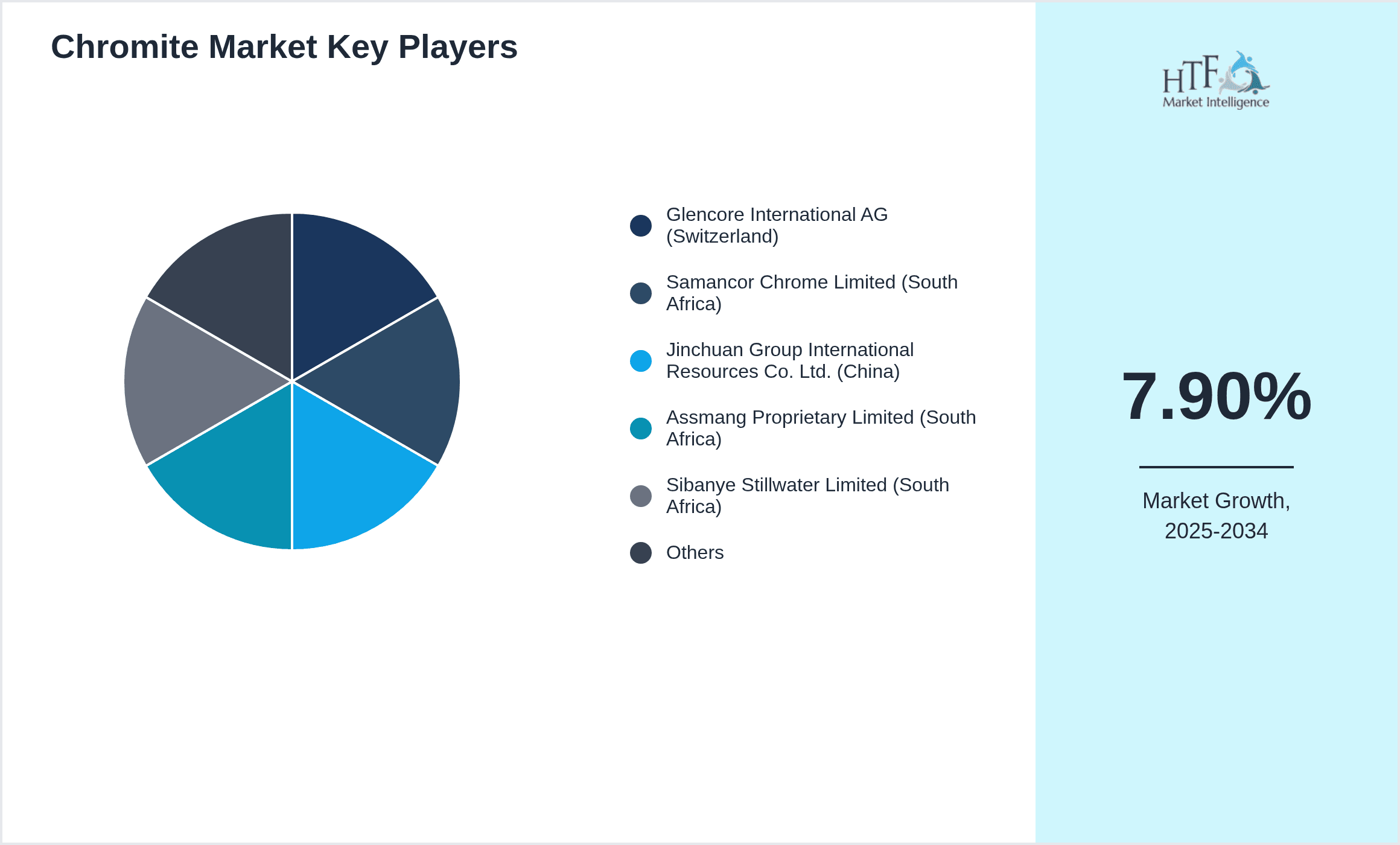

Prominent Players in Chromite Market

- •Glencore International AG (Switzerland)

- •Samancor Chrome Limited (South Africa)

- •Jinchuan Group International Resources Co. Ltd. (China)

- •Assmang Proprietary Limited (South Africa)

- •Sibanye Stillwater Limited (South Africa)

- •Eramet Group (France)

- •Tata Steel Limited (India)

- •Jindal Stainless Limited (India)

- •Xstrata Plc (Switzerland)

- •China Zirconium Limited (China)

- •FerroAlloy Resources Limited (South Africa)

- •International Ferro Metals Limited (Australia)

- •Victorian Mines Pty Ltd. (Australia)

- •Eastern Chrome Mines (South Africa)

- •International Minerals Corporation (South Africa)

- •Nalco Champion (USA)

- •Vale S.A. (Brazil)

- •Anglo American Platinum Limited (South Africa)

- •Pacific Metals Co. Ltd. (Japan)

- •Zijin Mining Group Co. Ltd. (China)

- •Norilsk Nickel (Russia)

- •Eramet SA (France)

- •Metalloinvest Holding Company (Russia)

- •Baosteel Group Corporation (China)

- •Shandong Provincial Mining Group (China)

Chromite Market Segmentation Overview

- •By Product Type

- ◦Lumpy Chromite

- ◦Fines Chromite

- ◦Concentrate Chromite

- ◦Pelletized Chromite

- ◦Others

- •By Application Area

- ◦Refractory

- ◦Metallurgical

- ◦Chemical

- ◦Foundry

- ◦Others

- •By Mining Process

- ◦Surface Mining

- ◦Underground Mining

- ◦Open Pit Mining

- •By End-Use Industry

- ◦Steel Manufacturing

- ◦Chemical Manufacturing

- ◦Construction

- ◦Automotive

- ◦Others

Growth Dynamics

The global chromite market is propelled by the increasing demand for stainless steel across various end-use industries, including construction, automotive, and consumer goods. The metallurgical sector's expansion, especially in Asia-Pacific, drives significant chromite consumption as ferrochrome production scales up. Technological advancements in chromite beneficiation and pelletization improve yield and reduce waste, enhancing market attractiveness. Additionally, rising infrastructure development in emerging economies fuels demand for refractory products, which rely heavily on chromite. Government initiatives promoting industrial growth and urbanization further stimulate market expansion, while growing environmental awareness prompts adoption of sustainable mining practices, fostering innovation and competitiveness. These factors collectively underpin robust market growth, supported by consistent investment in mining capacities and downstream processing technologies.

Emerging Market Trends

The chromite market is witnessing a shift towards environmentally sustainable mining and processing techniques, driven by stringent regulatory frameworks and corporate social responsibility mandates. Companies are increasingly investing in green beneficiation technologies that minimize water usage and reduce emissions. Digitalization and automation are gaining traction in mining operations, enhancing efficiency and safety. Pelletized chromite is emerging as a preferred product due to its superior furnace performance and reduced energy consumption. Furthermore, the diversification of chromite applications into chemical and specialty refractory segments reflects evolving market dynamics. Strategic alliances and joint ventures aimed at securing raw material supply chains are becoming common, indicating a trend towards consolidation and collaboration within the industry.

Market Opportunities

The growing demand for high-grade refractory materials in the steel and foundry industries presents significant growth opportunities for chromite producers. Expansion into emerging markets with increasing industrialization offers untapped potential. Technological innovation in pelletization and beneficiation processes enables product differentiation and new application development. Increasing focus on circular economy practices opens avenues for recycling chromite-containing materials. Additionally, strategic partnerships between mining companies and end-users can enhance supply chain stability and foster product customization. Government incentives supporting mining infrastructure and sustainable practices further create a conducive environment for market expansion and investment.

Industry Challenges

The chromite market faces challenges including environmental concerns related to mining operations, such as land degradation, water pollution, and carbon emissions. Regulatory compliance costs and evolving international standards impose operational constraints. Fluctuating chromium ore prices and geopolitical tensions affect supply chain stability and pricing strategies. Limited availability of high-grade chromite ores in certain regions restricts production scalability. Additionally, competition from alternative refractory materials and recycling initiatives may impact demand. The capital-intensive nature of mining projects and lengthy permitting processes present barriers to new entrants and expansion. Addressing these challenges requires technological innovation, sustainable practices, and strategic risk management to ensure long-term market viability.

Regulatory Landscape

- •Between 2020 and 2025, several key regulations have shaped the chromite market globally. The Mine Safety and Health Administration (MSHA) in the United States enforced stricter safety protocols in mining operations to reduce accidents and occupational hazards. The European Union introduced the REACH regulation focusing on chemical safety, impacting the handling and processing of chromium compounds derived from chromite. Environmental Protection Agencies across major producing regions implemented more rigorous emission standards to curb pollution from mining and beneficiation activities. Countries in Asia-Pacific adopted sustainable mining frameworks mandating environmental impact assessments and community engagement before project approvals. Additionally, import-export regulations and tariffs influenced global trade flows, requiring companies to adapt compliance strategies. These regulatory developments promote responsible mining practices, enhance worker safety, and encourage environmental stewardship, directly affecting production costs, operational planning, and market competitiveness.

- •The enforcement mechanisms for these regulations include regular audits, mandatory reporting, and penalties for non-compliance, compelling market participants to invest in compliance infrastructure and technologies. Stakeholders have responded by adopting advanced dust control systems, water treatment solutions, and energy-efficient beneficiation processes. The market has also seen increased transparency and reporting standards aligned with global sustainability goals. In regions like Latin America and Africa, governments have introduced incentives for mining companies that demonstrate environmental responsibility and community development contributions. These policies encourage industry players to integrate sustainability into their core business models, fostering innovation and reducing risks associated with environmental liabilities. The evolving regulatory landscape continues to influence strategic decision-making, investment priorities, and operational methodologies within the chromite market.

- •Safety standards specific to chromite mining have been enhanced, addressing potential exposure to chromium dust and associated health risks. Environmental norms emphasize rehabilitation of mined land and conservation of biodiversity in mining zones. Operational guidelines now recommend the use of cleaner technologies and best practices to minimize ecological footprints. Regional mandates vary, with developed economies typically enforcing stricter standards and developing regions progressively adopting similar frameworks. The policy framework also includes government-backed programs promoting research and development in sustainable mining technologies, supporting industry modernization. These regulatory measures collectively contribute to mitigating environmental and social impacts, ensuring the chromite market aligns with global sustainability trends and stakeholder expectations.

- •Country-specific mandates such as South Africa's Mining Charter and India's National Mineral Policy have set benchmarks for mining equity, community development, and environmental protection. Timelines for implementation of these mandates have been phased to allow industry adaptation while maintaining compliance rigor. Governments have also established dedicated regulatory bodies to oversee mining activities, enforce standards, and facilitate stakeholder engagement. These institutional frameworks enhance governance and accountability in the chromite sector, fostering a stable and transparent market environment. The interplay of international conventions and local regulations shapes the operational landscape, requiring companies to adopt comprehensive compliance strategies.

- •Government initiatives such as tax rebates, subsidies for clean technology adoption, and funding for mining infrastructure development provide critical support to the chromite industry. Incentive programs encourage exploration activities and capacity expansion, particularly in emerging markets. Public-private partnerships are increasingly employed to drive innovation and address infrastructural bottlenecks. These policy frameworks aim to balance economic growth with environmental and social responsibilities, positioning the chromite market for sustainable expansion. Continuous regulatory evolution demands proactive engagement from industry participants to capitalize on policy benefits and mitigate compliance risks.

Market Intelligence

- •15th January 2025, Glencore International AG announced the launch of a new high-efficiency beneficiation plant in South Africa aimed at increasing chromite concentrate output by 20%. The facility incorporates advanced dry separation technology that reduces water usage by 30% and lowers energy consumption, aligning with the company’s sustainability goals. This strategic investment is expected to enhance Glencore’s supply capabilities to stainless steel manufacturers globally while reducing environmental impact. The move positions the company competitively in the growing chromite market, responding to rising demand in Asia-Pacific and Latin America. Source: Glencore Official Press Release

- •10th March 2025, Jinchuan Group International Resources Co. Ltd. introduced an innovative pelletized chromite product designed to improve furnace efficiency and reduce carbon emissions during ferrochrome production. The new product utilizes proprietary pelletizing techniques that enhance thermal stability and reduce sintering time. Jinchuan aims to capture expanding markets in Europe and North America by offering environmentally friendly alternatives to traditional chromite forms. This launch is part of the company’s broader strategy to lead in sustainable metallurgical inputs and strengthen partnerships with major steel producers. Source: Jinchuan Group Corporate Website

- •22nd June 2025, Samancor Chrome Limited announced a joint venture with a European refractory manufacturer to develop customized chromite-based refractory bricks optimized for high-temperature industrial applications. This collaboration combines Samancor’s premium chromite supply with cutting-edge ceramic technology to enhance product durability and performance. The partnership aims to expand market reach in Latin America and Asia-Pacific regions, leveraging growing industrial infrastructure investments. The initiative underscores the trend towards product innovation and value-added solutions within the chromite industry. Source: Industry Publication - Mining Weekly

- •30th September 2025, Eramet Group completed the acquisition of a minority stake in a mining technology startup specializing in automated chromite ore sorting and real-time quality monitoring. This strategic investment supports Eramet’s commitment to digital transformation and operational excellence. The technology promises to increase chromite recovery rates and reduce processing costs, enhancing competitiveness in the global market. The acquisition is aligned with the company’s sustainability objectives, aiming to minimize environmental footprints while improving product quality. Source: Eramet Group Annual Report 2025

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 9.6 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.7% |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Glencore International AG (Switzerland), Samancor Chrome Limited (South Africa), Jinchuan Group International Resources Co. Ltd. (China), Assmang Proprietary Limited (South Africa), Sibanye Stillwater Limited (South Africa) |

Global Chromite Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.