Southeast Asia Inverting Filter Centrifuge Market - Outlook 2020-2034

Southeast Asia Inverting Filter Centrifuge Market is segmented by Inverting Filter Centrifuge Type (Batch Inverting Filter Centrifuge, Continuous Inverting Filter Centrifuge, Fully Automated Inverting Filter Centrifuge, Semi-Automated Inverting Filter Centrifuge, Manual Inverting Filter Centrifuge), Application Sector (Chemical Processing, Mining, Wastewater Treatment, Food & Beverage, Pharmaceuticals), Service Offering (Installation and Commissioning, Maintenance and Repair, Spare Parts Supply, Technical Support and Training), Deployment Model (On-Premise, Rental Solutions, Leasing Models), and Geography (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines, Others)

Pricing

Report Overview

Executive Summary

- •The Southeast Asia Inverting Filter Centrifuge market is defined by the production and utilization of centrifugal filtration equipment designed to separate solid particles from liquids through inversion of the filter element, facilitating efficient cake discharge and high separation purity. This market covers a broad spectrum of centrifuge types including batch, continuous, fully automated, semi-automated, and manual variants, each tailored to meet specific operational demands in industries such as chemical processing, mining, wastewater treatment, food and beverage, and pharmaceuticals. End users range from large-scale manufacturers to municipal utilities, all seeking improved process efficiency, reduced operational costs, and compliance with environmental standards. The value chain extends from raw material procurement for filter media and centrifuge components to manufacturing, distribution, and after-sales service, encompassing installation, maintenance, and technical support. The market is characterized by technological innovation, particularly in automation and smart monitoring systems, which enhances operational reliability and throughput. Southeast Asia's rapid industrialization and increasing environmental regulations have further fueled demand for efficient solid-liquid separation technologies, positioning the inverting filter centrifuge as a critical component in process optimization and sustainability efforts across multiple sectors.

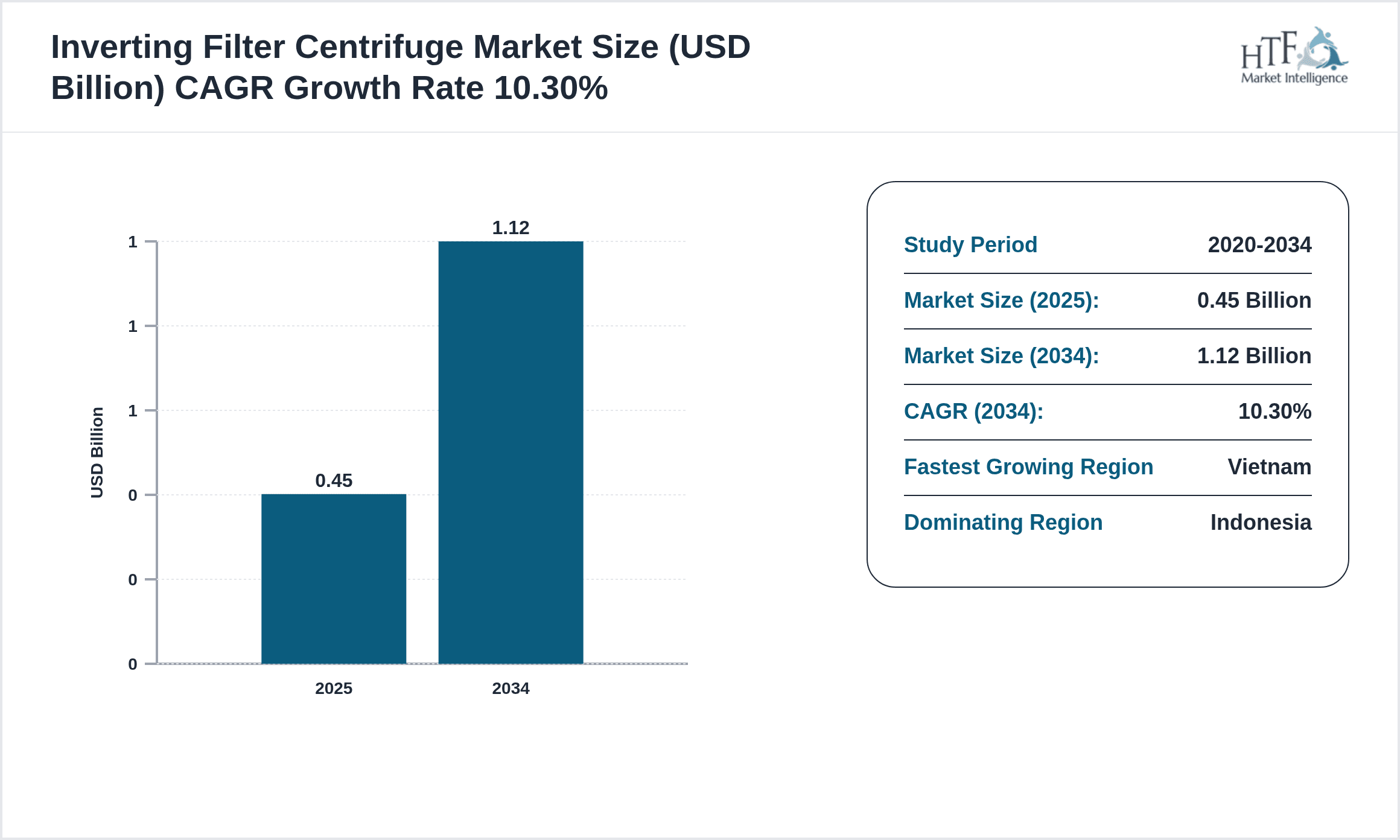

- •Key market highlights include a base market size of USD 0.45 Billion in 2025, expanding to USD 1.12 Billion by 2034 at a robust CAGR of 10.3%. The market has demonstrated consistent growth since 2020, driven by rising industrial activities and stringent effluent treatment regulations across Southeast Asian countries. Automation and digitalization trends have accelerated adoption rates, while the increasing need for wastewater treatment solutions in urbanizing regions also propels market expansion. Notably, Indonesia leads in market share, while Vietnam is identified as the fastest-growing country, reflecting its aggressive industrial growth and infrastructure developments. Batch inverting filter centrifuges currently dominate the market due to their versatility and cost-effectiveness, though fully automated variants are gaining rapid traction owing to enhanced operational efficiencies.

- •The market holds significant strategic importance for chemical, mining, pharmaceutical, and municipal sectors by enabling efficient solid-liquid separation that reduces downtime, improves product quality, and ensures compliance with environmental mandates. For stakeholders including manufacturers, suppliers, and end users, investing in advanced inverting filter centrifuge technologies offers opportunities to optimize resource utilization and reduce operational expenses. The evolving regulatory landscape and rising environmental consciousness further amplify market relevance, positioning it as a key driver in sustainable industrial processes throughout Southeast Asia.

Competitive Landscape

The Southeast Asia Inverting Filter Centrifuge market features a competitive environment characterized by a blend of global corporations and regional manufacturers focusing on innovation, quality, and service excellence. Market participants employ diverse strategies including product differentiation through automation and energy efficiency, strategic partnerships with local distributors to expand market reach, and competitive pricing to capture emerging industrial customers. Technological advancements in filtration media and smart process controls have become critical competitive differentiators, enabling companies to deliver superior dewatering performance and operational reliability. Mergers and acquisitions, though limited in this region, serve as strategic tools to augment product portfolios and geographic presence. Additionally, manufacturers emphasize after-sales services such as maintenance contracts and remote monitoring to foster long-term customer relationships and reduce churn. Pricing strategies are calibrated to balance upfront equipment costs with lifecycle operational savings, appealing to cost-sensitive Southeast Asian markets. Market entry barriers include capital-intensive R&D and adherence to stringent local regulatory standards, which favor established players with robust compliance capabilities. Regional competition is intensifying as emerging economies in Southeast Asia ramp up industrial activities, driving demand for efficient filtration solutions. Future competitive trends indicate a shift towards integrated filtration and waste management systems, leveraging IoT and Industry 4.0 technologies to enhance process automation and data-driven decision-making, thereby further intensifying the rivalry among leading players.

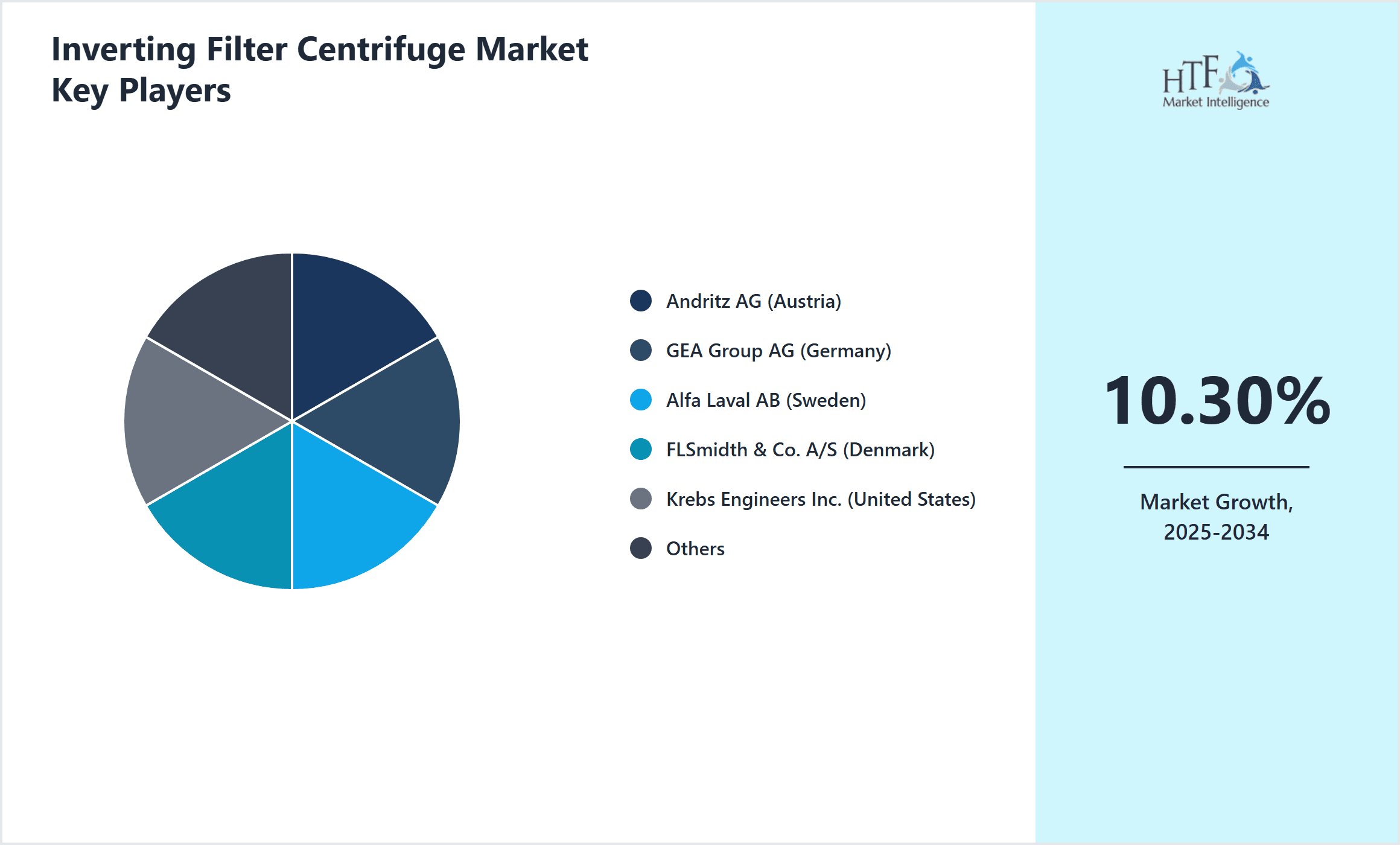

Prominent Players in Inverting Filter Centrifuge Market

- •Andritz AG (Austria)

- •GEA Group AG (Germany)

- •Alfa Laval AB (Sweden)

- •FLSmidth & Co. A/S (Denmark)

- •Krebs Engineers Inc. (United States)

- •Mitsubishi Kakoki Kaisha Ltd. (Japan)

- •Bucher Unipektin AG (Switzerland)

- •Schenck Process GmbH (Germany)

- •Thermopac Engineering Pvt. Ltd. (India)

- •Shanghai Centrifuge Co., Ltd. (China)

- •JH Equipment Pty Ltd. (Australia)

- •Shanghai Jiao Tong University Centrifuge Technology Co., Ltd. (China)

- •Pall Corporation (United States)

- •Hiller GmbH (Germany)

- •Ljungstrom Group AB (Sweden)

- •Tridev Process Equipment Pvt. Ltd. (India)

- •Schenck Process (Singapore) Pte Ltd. (Singapore)

- •Aarchem Engineering Pvt. Ltd. (India)

- •Rosedowns Ltd. (United Kingdom)

- •Andritz Southeast Asia Pte Ltd. (Singapore)

- •Shanghai Zhenhua Heavy Industries Co., Ltd. (China)

- •Nanjing Filter Tech Co., Ltd. (China)

- •Tianjin Centrifuge Co., Ltd. (China)

- •Krebs Engineers Asia Pacific (Singapore)

- •Nanjing Huachang Filter Press Co., Ltd. (China)

Market Breakdown

- •By Inverting Filter Centrifuge Type

- ◦Batch Inverting Filter Centrifuge

- ◦Continuous Inverting Filter Centrifuge

- ◦Fully Automated Inverting Filter Centrifuge

- ◦Semi-Automated Inverting Filter Centrifuge

- ◦Manual Inverting Filter Centrifuge

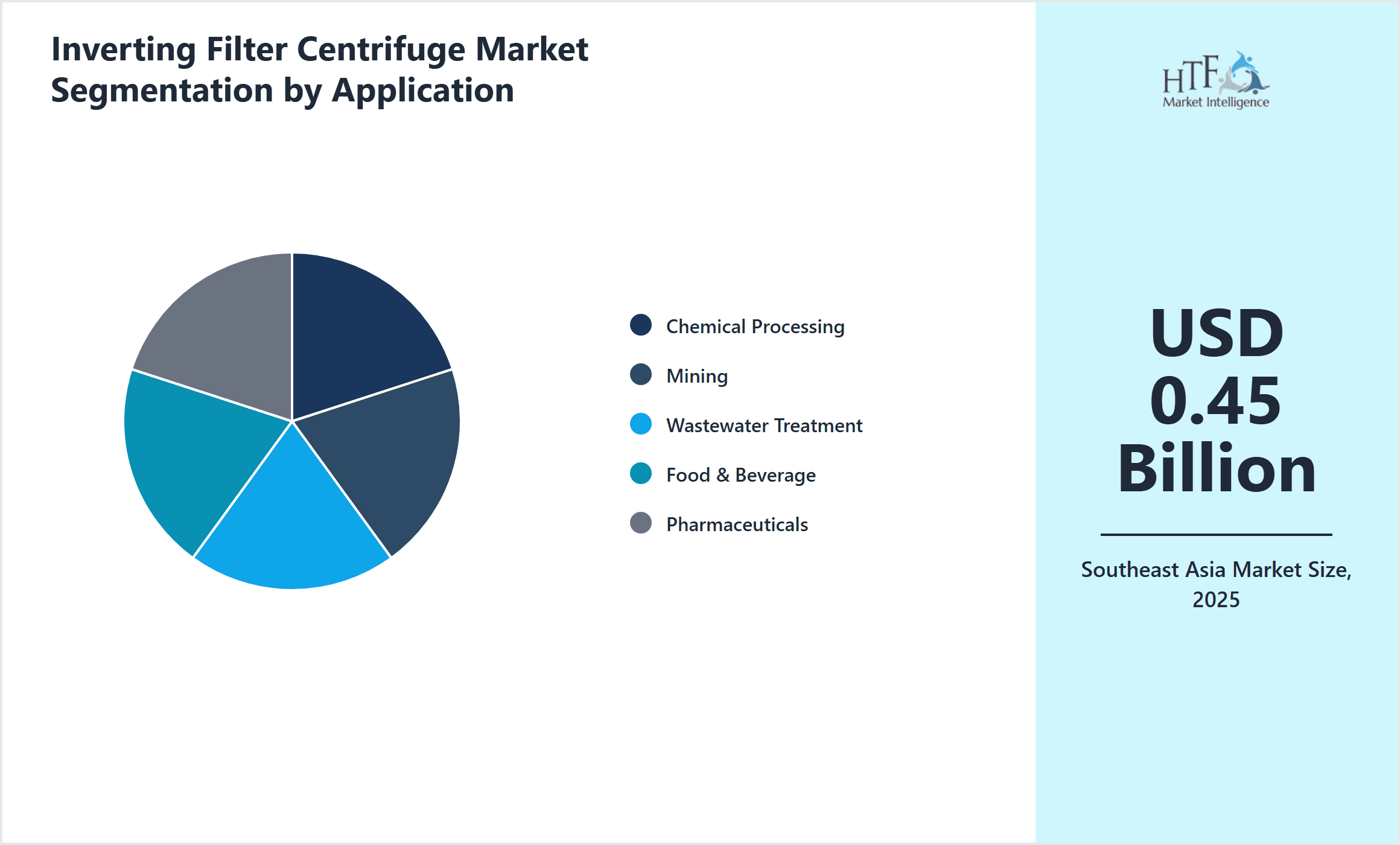

- •By Application Sector

- ◦Chemical Processing

- ◦Mining

- ◦Wastewater Treatment

- ◦Food & Beverage

- ◦Pharmaceuticals

- •By Service Offering

- ◦Installation and Commissioning

- ◦Maintenance and Repair

- ◦Spare Parts Supply

- ◦Technical Support and Training

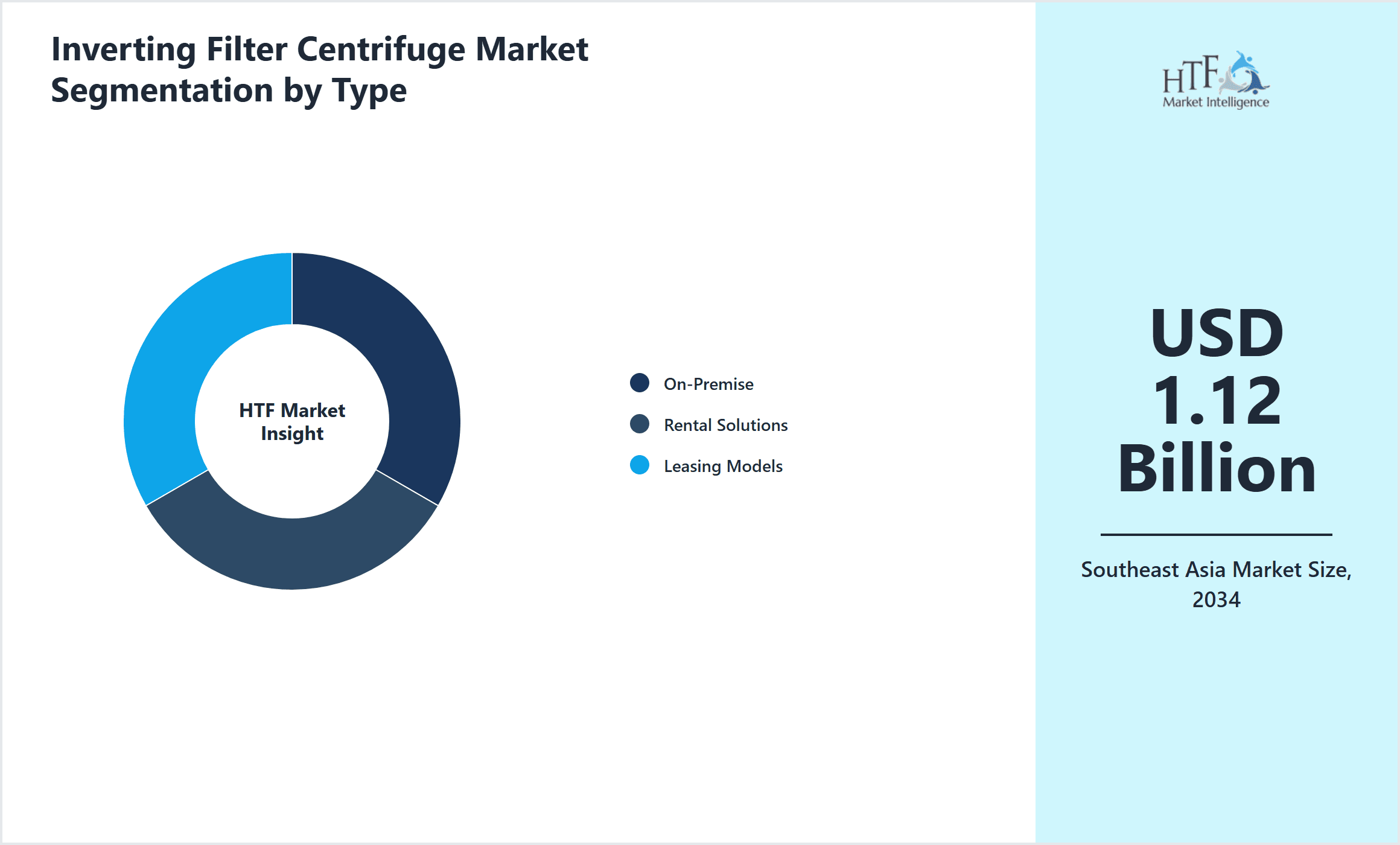

- •By Deployment Model

- ◦On-Premise

- ◦Rental Solutions

- ◦Leasing Models

Growth Dynamics

- •Industrialization in Southeast Asia is rapidly expanding, especially in countries like Indonesia and Vietnam, driving demand for efficient solid-liquid separation technologies such as inverting filter centrifuges in sectors like chemical processing and mining. This growth is supported by government initiatives promoting infrastructure development and industrial upgrades, which contribute to increased capital expenditure on advanced filtration equipment.

- •Increasing environmental regulations across Southeast Asian nations mandate stringent wastewater treatment and effluent discharge standards, compelling industries to adopt inverting filter centrifuges that provide superior dewatering and filtration performance to meet compliance requirements effectively.

- •Technological advancements including automation, remote monitoring, and integration with Industry 4.0 systems are enhancing operational efficiency and reliability of inverting filter centrifuges, encouraging manufacturers and end users to invest in next-generation equipment for optimized production processes.

- •Rising urbanization and industrial waste generation in Southeast Asia have created significant demand for wastewater treatment solutions, where inverting filter centrifuges play a pivotal role in solid-liquid separation, thereby supporting sustainable development goals and improving water reuse.

- •The expansion of the pharmaceutical and food & beverage processing industries in the region is increasing the need for hygienic and efficient filtration equipment, positioning inverting filter centrifuges as essential for maintaining product quality and purity.

Market Trends

- •Adoption of fully automated inverting filter centrifuges is gaining momentum across Southeast Asia due to enhanced process control, reduced labor costs, and minimized downtime, reflecting a shift towards Industry 4.0-driven manufacturing environments.

- •Sustainability is a key market trend with manufacturers focusing on energy-efficient centrifuge designs and recyclable filter media to reduce environmental impact and operational costs, aligning with regional green initiatives.

- •Collaborations between local distributors and global centrifuge manufacturers are increasing, facilitating customized solutions that address specific industrial challenges and regulatory requirements in Southeast Asia.

- •Integration of IoT-enabled sensors and predictive maintenance software in inverting filter centrifuges is improving equipment uptime and reliability, enabling real-time monitoring and proactive service interventions.

- •The market is witnessing a rising trend towards modular and portable centrifuge units which cater to small and medium enterprises, enhancing accessibility and operational flexibility across diverse applications.

Market Opportunities

- •Expanding mining activities in countries like Indonesia and the Philippines offer significant growth opportunities for inverting filter centrifuge manufacturers to supply robust and reliable dewatering solutions tailored to mineral processing applications.

- •Increasing investments in wastewater treatment infrastructure across urban centers in Southeast Asia present opportunities to deploy advanced inverting filter centrifuges that enhance effluent quality and support water reuse programs.

- •Emerging demand from the pharmaceutical sector for hygienic and efficient filtration solutions creates avenues for innovation and market penetration by manufacturers offering specialized centrifuge models meeting stringent quality standards.

- •Government incentives and subsidies promoting clean technology adoption in Southeast Asia can be leveraged by market players to accelerate product development and regional expansion strategies.

- •The growth of the food & beverage processing industry in the region encourages the development of customized centrifuge solutions that address specific filtration challenges such as high throughput and product purity requirements.

Market Challenges

- •High capital expenditure associated with fully automated inverting filter centrifuges limits adoption among small and medium-sized enterprises, constraining market penetration in certain Southeast Asian countries with price-sensitive customers.

- •Scarcity of skilled technicians and maintenance personnel in some regional markets poses challenges to effective operation and upkeep of sophisticated centrifuge systems, impacting equipment longevity and customer satisfaction.

- •Variability in regional regulatory frameworks and enforcement levels across Southeast Asian countries creates complexity for manufacturers in ensuring consistent compliance and market access.

- •Competition from low-cost centrifuge alternatives and second-hand equipment affects pricing dynamics and profitability for established players focusing on high-quality inverting filter centrifuges.

- •Supply chain disruptions, including delays in critical component procurement, can adversely impact manufacturing schedules and delivery timelines, hindering market growth.

Regulatory Framework

- •Between 2020 and 2025, Southeast Asian countries have progressively implemented environmental regulations mandating enhanced wastewater treatment and solid waste management. For instance, Indonesia's Ministry of Environment and Forestry introduced stricter effluent discharge standards in 2023 requiring industries to deploy advanced filtration systems to limit pollutant release. Compliance with such regulations has driven the adoption of inverting filter centrifuges with superior dewatering efficiency.

- •Malaysia's Environmental Quality Act amendments in 2021 introduced compulsory periodic reporting on industrial wastewater treatment efficacy, fostering increased investments in reliable solid-liquid separation technologies including centrifuges. Enforcement mechanisms through fines and operational permits have incentivized manufacturers to upgrade filtration capabilities.

- •In the Philippines, the Clean Water Act revisions effective from 2022 established clear guidelines on sludge management and treatment plant performance, encouraging adoption of technologically advanced centrifuges to meet these norms and avoid penalties. Industry stakeholders have responded by integrating automated filtration equipment to ensure compliance.

- •Thailand's Pollution Control Department introduced operational guidelines in 2024 focusing on industrial effluent control, emphasizing equipment certification and performance validation for centrifuge manufacturers. This framework enhances quality assurance and promotes market growth of certified inverting filter centrifuge products.

- •Government initiatives across Southeast Asia, including incentives for green technology adoption and subsidies for wastewater treatment infrastructure, have bolstered market expansion by reducing financial barriers for equipment procurement and encouraging sustainable industrial practices.

Market Intelligence

- •15th February 2025, Andritz AG announced the launch of its latest fully automated inverting filter centrifuge model designed specifically for the Southeast Asian chemical processing industry. The product features enhanced automation capabilities, including remote operation and predictive maintenance powered by AI algorithms, aimed at reducing downtime and operational costs. The centrifuge supports high throughput while maintaining energy efficiency, aligning with regional environmental regulations. Andritz aims to capitalize on growing demand from countries such as Indonesia and Vietnam by offering tailored solutions that address local industrial challenges and compliance needs. This launch strengthens Andritz's competitive position in the Southeast Asia market, emphasizing innovation and customer-centric design. Source: Official Andritz AG Press Release

- •3rd April 2025, GEA Group AG introduced an advanced continuous inverting filter centrifuge optimized for mining and wastewater treatment applications in Southeast Asia. The new centrifuge incorporates IoT-enabled sensors for real-time monitoring of filtration parameters, enabling proactive maintenance and operational optimization. GEA's strategic objective is to support the rapid industrial growth in the region by providing scalable and customizable filtration solutions that improve process efficiency and environmental compliance. The product launch included partnership agreements with local distributors in Malaysia and Thailand to enhance after-sales support and technical service coverage. This initiative reflects GEA’s commitment to sustainable industrial solutions and digital transformation in the region. Source: GEA Group Official Announcement

- •12th June 2024, Alfa Laval AB completed the acquisition of a regional filtration equipment manufacturer based in Singapore, aiming to expand its footprint in the Southeast Asia inverting filter centrifuge market. This strategic move enables Alfa Laval to leverage local manufacturing capabilities and accelerate product customization for key industries such as pharmaceuticals and food & beverage processing. The acquisition is expected to enhance Alfa Laval’s supply chain efficiency and reduce lead times, thereby improving customer responsiveness. This consolidation also supports Alfa Laval’s sustainability goals by promoting cleaner production technologies across the region. Source: Alfa Laval Corporate Communications

- •29th August 2024, FLSmidth & Co. A/S announced a strategic partnership with a leading wastewater treatment firm in Vietnam to deploy inverting filter centrifuge systems for municipal sludge dewatering projects. The collaboration focuses on integrating FLSmidth’s advanced centrifuge technology with local expertise to deliver cost-effective and environmentally compliant solutions. This partnership aligns with Vietnam’s increasing investment in wastewater infrastructure and commitment to environmental sustainability. The initiative includes training programs for local operators and technical support to ensure optimal equipment performance. This development highlights FLSmidth’s proactive approach in tapping emerging Southeast Asian markets through collaborative models. Source: FLSmidth Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Indonesia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Vietnam is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Singapore

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Philippines

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.45 Billion |

| Forecast Year Market Size | USD 1.12 Billion |

| CAGR | 10.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.9% |

| Scope of Report | Market is segmented by Inverting Filter Centrifuge Type (Batch Inverting Filter Centrifuge, Continuous Inverting Filter Centrifuge, Fully Automated Inverting Filter Centrifuge, Semi-Automated Inverting Filter Centrifuge, Manual Inverting Filter Centrifuge), Application Sector (Chemical Processing, Mining, Wastewater Treatment, Food & Beverage, Pharmaceuticals), Service Offering (Installation and Commissioning, Maintenance and Repair, Spare Parts Supply, Technical Support and Training), Deployment Model (On-Premise, Rental Solutions, Leasing Models) |

| Regions Covered | Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines, Others |

| Key Companies | Andritz AG (Austria), GEA Group AG (Germany), Alfa Laval AB (Sweden), FLSmidth & Co. A/S (Denmark), Krebs Engineers Inc. (United States) |

Southeast Asia Inverting Filter Centrifuge Market - Outlook 2020-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.