United States Switchable Smart Film Market - United States Size & Outlook 2025-2034

United States Switchable Smart Film Market is segmented by Application (Privacy Glass, Sunroofs, Partition Walls, Electronic Displays, Smart Windows), Type (Polymer Dispersed Liquid Crystal, Suspended Particle Devices, Micro-Blinds, Electrochromic, Thermochromic), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

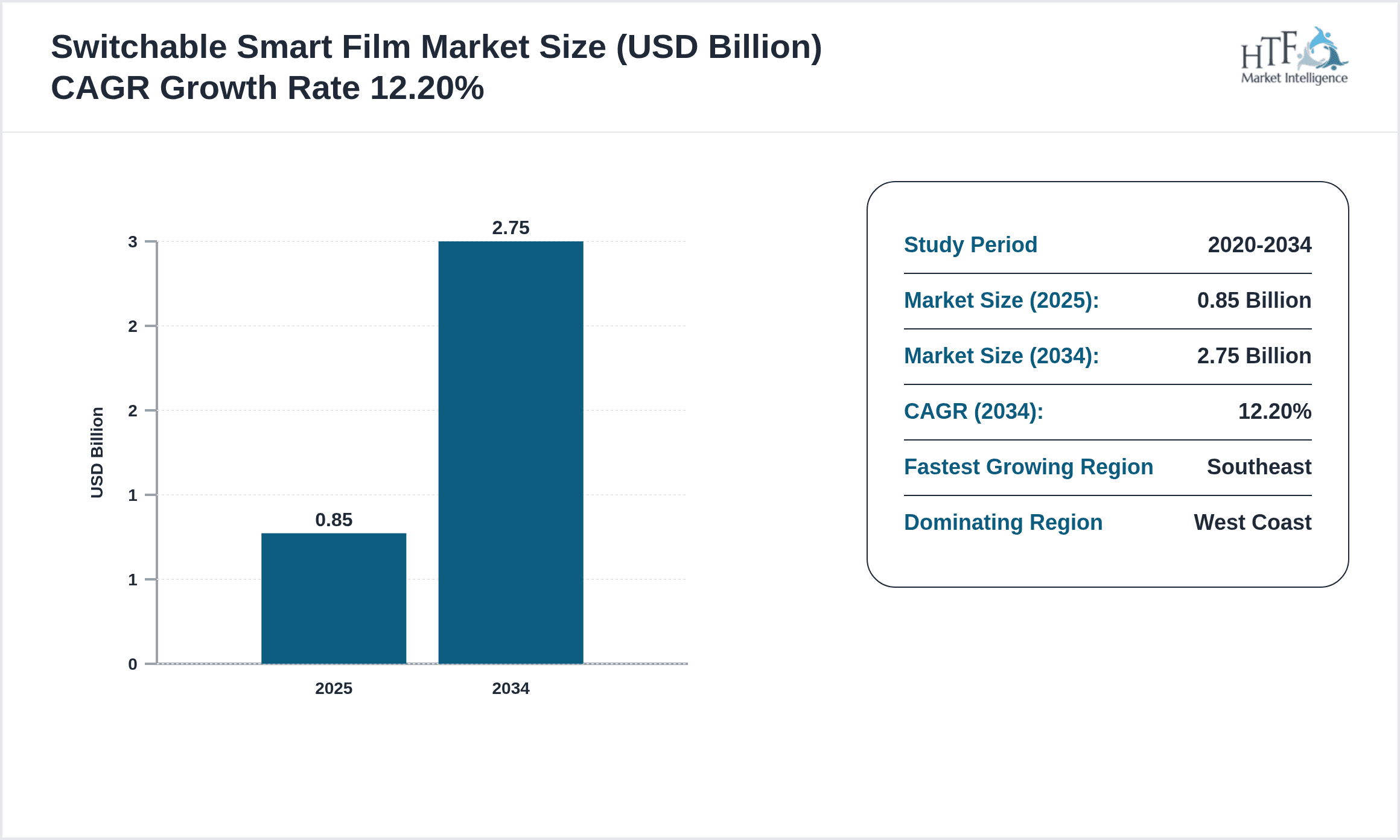

- •The United States Switchable Smart Film Market is characterized by innovative technologies enabling dynamic control of transparency and privacy on glass surfaces across diverse sectors including commercial buildings, automotive, residential, and electronics. Key product types include polymer dispersed liquid crystal (PDLC), suspended particle devices (SPD), electrochromic films, micro-blinds, and thermochromic variants, each offering unique mechanisms for light modulation. These films serve applications such as privacy glass, sunroofs, partition walls, electronic displays, and smart windows, providing enhanced energy efficiency, privacy, and aesthetic appeal. The market is shaped by rising urbanization, increasing demand for green building solutions, and regulatory incentives promoting energy conservation. Technological advancements, including improved film durability and integration with IoT systems, further propel adoption. Leading companies continue investing in R&D to develop cost-effective, high-performance films tailored to end-user requirements. This market’s growth trajectory is supported by evolving consumer preferences for smart living environments and expanding commercial infrastructure in the United States. The scope covers material innovation, application expansion, and regulatory compliance within the domestic market.

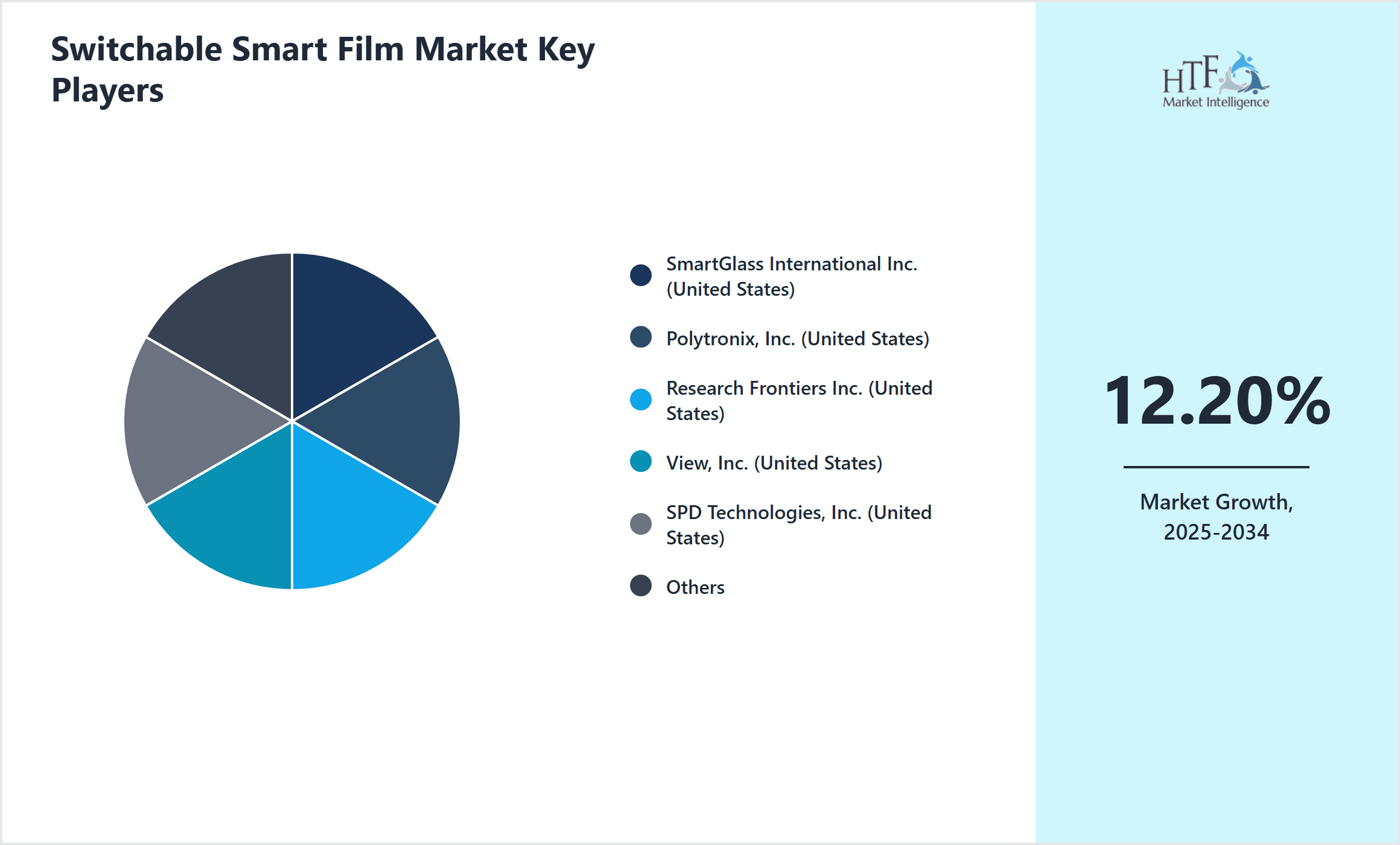

- •Key highlights include a robust CAGR of approximately 12.2% projected from 2025 to 2034, with market size expanding from USD 0.85 billion in 2025 to USD 2.75 billion by 2034. The polymer dispersed liquid crystal type dominates market share due to its early commercialization and versatility, while suspended particle devices are the fastest-growing segment owing to their superior optical performance. The West Coast region leads market revenue driven by high construction activity and stringent energy codes, whereas the Southeast shows the fastest growth propelled by increasing commercial developments and automotive applications. Market adoption is accelerated by consumer demand for privacy and energy savings, alongside governmental policies supporting smart building technologies.

- •The value proposition of switchable smart films lies in their ability to offer energy-efficient and customizable solutions for privacy and light control, reducing reliance on blinds or curtains and lowering HVAC costs. Strategic importance extends across architects, automotive manufacturers, interior designers, and technology integrators seeking innovative, sustainable materials. The integration of smart films into IoT ecosystems enhances building automation capabilities, offering stakeholders competitive advantages through improved occupant comfort and operational efficiency. As environmental regulations tighten and end-users prioritize sustainability, the market is poised for significant expansion, backed by continuous innovation and strategic collaborations among key players. This positions the United States Switchable Smart Film Market as a critical component in the broader smart materials and energy-efficient construction industries.

Competitive Landscape

The competitive environment of the United States Switchable Smart Film Market is marked by intense rivalry among global and regional players focusing on innovation, product differentiation, and strategic partnerships. Market leaders invest heavily in R&D to advance film performance, durability, and integration capabilities, aiming to capture diverse application segments such as architectural, automotive, and electronics. The competition also centers on cost optimization and scaling manufacturing to meet increasing demand. Strategic alliances and collaborations with glass manufacturers, automakers, and technology firms are prevalent, facilitating market penetration and new product introductions. Additionally, mergers and acquisitions help consolidate market share and expand technology portfolios. Pricing strategies are influenced by raw material costs and technological complexity, while firms emphasize sustainable and eco-friendly production processes to comply with stringent environmental regulations. Regional competition is influenced by localized customer preferences and regulatory frameworks, with West Coast companies leading innovation, and Southeast firms rapidly expanding operations. Future trends indicate a shift towards smart films integrated with IoT and energy management systems, intensifying competition in technology-driven segments.

Leading Companies in United States Switchable Smart Film Market

- •SmartGlass International Inc. (United States)

- •Polytronix, Inc. (United States)

- •Research Frontiers Inc. (United States)

- •View, Inc. (United States)

- •SPD Technologies, Inc. (United States)

- •Switch Materials, Inc. (United States)

- •Innovative Glass Corp. (United States)

- •Gentex Corporation (United States)

- •SageGlass (United States)

- •Polymer Vision Technologies (United States)

- •Smart Film Technologies LLC (United States)

- •Nippon Sheet Glass Co., Ltd. (Japan)

- •Saint-Gobain S.A. (France)

- •Research Frontiers Europe B.V. (Netherlands)

- •Mitsubishi Electric Corporation (Japan)

- •3M Company (United States)

- •AGC Inc. (Japan)

- •Hanita Coatings Ltd. (Israel)

- •SPD Technologies Asia Ltd. (Singapore)

- •Smart Tint LLC (United States)

- •Polytronix Asia Pacific (Hong Kong)

- •Innovative Smart Films Pvt Ltd. (India)

- •View Smart Technologies GmbH (Germany)

- •Smart Glass International Europe (UK)

- •Kinestral Technologies Inc. (United States)

United States Switchable Smart Film Market Segmentation

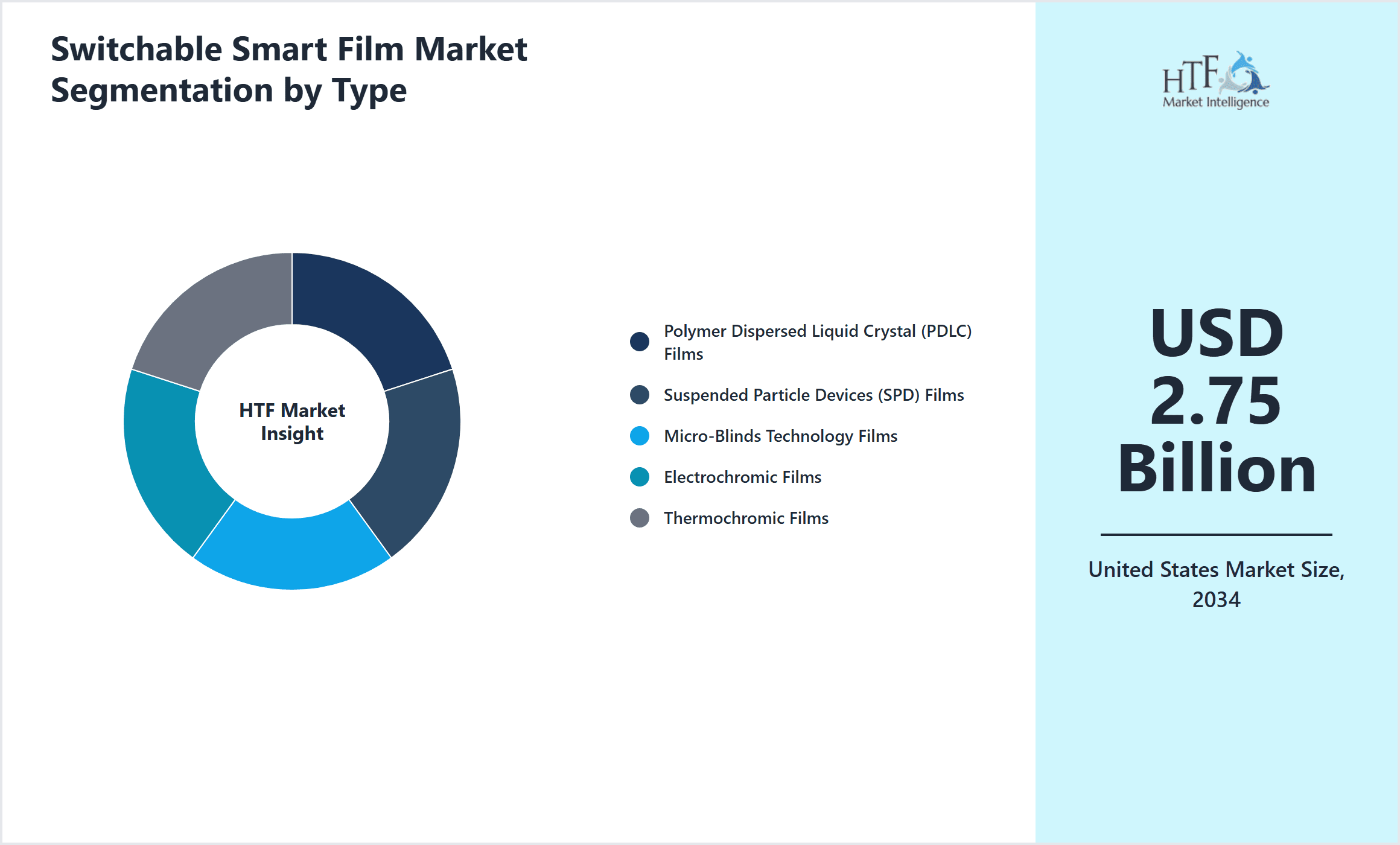

- •By Type

- ◦Polymer Dispersed Liquid Crystal (PDLC) Films

- ◦Suspended Particle Devices (SPD) Films

- ◦Micro-Blinds Technology Films

- ◦Electrochromic Films

- ◦Thermochromic Films

- •By Application

- ◦Privacy Glass

- ◦Sunroofs

- ◦Partition Walls

- ◦Electronic Displays

- ◦Smart Windows

- •By Installation Environment

- ◦Commercial Buildings

- ◦Residential Buildings

- ◦Automotive

- ◦Electronics & Displays

- •By Technology Integration

- ◦Standalone Films

- ◦Integrated IoT-enabled Smart Films

- ◦Hybrid Smart Film Systems

Growth Dynamics

- •The United States Switchable Smart Film Market is propelled by increasing construction of green commercial buildings driven by stringent energy efficiency regulations and incentives. The adoption of smart films helps reduce HVAC loads by modulating solar heat gain, aligning with LEED certification requirements. Additionally, rising consumer demand for privacy solutions in residential and office spaces supports market expansion. Automotive manufacturers integrate switchable films in sunroofs and windows to enhance passenger comfort and vehicle aesthetics, boosting demand. Technological advancements lowering production costs and improving film durability further stimulate market growth, enabling wider acceptance across diverse applications.

- •Growing trends include the integration of smart films with IoT and building automation systems, allowing remote control and real-time energy management. Innovations in electrochromic and SPD technologies improve switching speed and optical clarity, attracting architects and designers. Increasing urbanization and smart city projects in the United States drive demand for smart windows and partitions. Furthermore, collaborations between glass manufacturers and technology providers foster product innovations, expanding application scopes. Consumer preference for sustainable interior design solutions also fuels the adoption of switchable films in residential markets.

- •Restraints impacting the market include the high initial installation cost of switchable smart films compared to conventional glass treatments, limiting penetration in price-sensitive segments. Technical challenges such as limited film lifespan, sensitivity to environmental factors, and power dependency for some technologies constrain wider usage. Additionally, lack of awareness and skepticism regarding performance and durability among end-users hampers adoption. Supply chain disruptions and fluctuations in raw material prices further restrict market growth. Regulatory complexities and certification delays can also pose barriers for new product introductions.

- •Opportunities abound in expanding applications beyond traditional architectural uses, including integration into automotive infotainment displays and adaptive electronics. The rise of smart homes and offices creates demand for films compatible with voice and mobile app controls. Geographic expansion into emerging regional zones within the United States, such as the Southeast, offers untapped potential due to increasing commercial infrastructure. Furthermore, advancements in eco-friendly and recyclable film materials align with sustainability trends, appealing to environmentally conscious consumers. Strategic partnerships and M&A activities present avenues for market consolidation and technological advancement.

- •Challenges include intense competition from alternative shading and privacy solutions like blinds, curtains, and tinted glass, which are often less expensive and better understood by consumers. Ensuring reliability and long-term performance under varying climatic conditions remains a technical hurdle. Additionally, educating architects, builders, and end-users about the benefits and installation processes of smart films requires ongoing marketing efforts. Regulatory uncertainty around electrical safety standards and energy codes may delay approvals. Finally, balancing innovation with cost-effectiveness to achieve mass-market adoption continues to challenge manufacturers and suppliers.

United States Switchable Smart Film Market Trends

- •The market is witnessing a trend towards integration of smart films with IoT-enabled building management systems, enabling remote control and real-time energy optimization. Companies like View, Inc. have introduced smart window solutions with app-based controls enhancing user convenience. This digitization trend aligns with broader smart building initiatives across commercial real estate in the United States.

- •Innovations in electrochromic and SPD technologies have led to faster switching speeds and improved optical quality, attracting adoption in automotive sunroofs and privacy glass. For example, SPD Technologies has developed films capable of instant light modulation, significantly improving passenger comfort and energy savings in vehicles.

- •Collaborations between glass manufacturers and smart film producers have resulted in hybrid products combining laminated safety glass with switchable films, expanding use cases in high-end commercial buildings. These partnerships enhance product durability and compliance with building codes, facilitating wider acceptance.

- •Sustainability is a growing focus, with manufacturers developing eco-friendly films that reduce energy consumption and incorporate recyclable materials. This aligns with increasing regulatory pressure and consumer demand for green building solutions in the United States.

- •Expansion into residential applications is notable, with smart films gaining traction for home automation and privacy control. Enhanced aesthetic appeal and ease of retrofit installation support this trend, broadening the market base.

- •Adoption of micro-blinds technology embedded within glass provides an alternative to switchable films, offering precise light control and added durability, appealing to luxury commercial and residential projects.

- •Future developments indicate a shift towards multifunctional films integrating energy harvesting and self-cleaning properties, positioning smart films as comprehensive smart facade solutions.

United States Switchable Smart Film Market Opportunities

- •The growing demand for retrofit solutions in existing commercial and residential buildings presents a significant opportunity for switchable smart films, allowing energy and privacy upgrades without major structural changes. Targeting this segment can accelerate market penetration.

- •Emerging applications in automotive interiors, including sunroofs and privacy windows, offer growth potential as manufacturers seek to enhance passenger experience and meet regulatory standards for energy efficiency and safety.

- •Advancements in low-power and self-powered film technologies enable expansion into off-grid and energy-sensitive environments, opening new markets in remote and sustainable construction projects.

- •Collaborating with smart home technology providers to integrate films with voice and app controls can enhance product appeal and market reach, leveraging the smart home adoption trend in the United States.

- •Developing region-specific products tailored to climatic and regulatory conditions of fast-growing zones such as the Southeast can capture localized demand effectively.

- •Investment in eco-friendly manufacturing and recyclable film materials can differentiate product offerings and align with increasing environmental regulations and consumer preferences.

- •Strategic mergers and acquisitions can consolidate technological capabilities and expand distribution networks, accelerating innovation and market coverage in the United States.

United States Switchable Smart Film Market Challenges

- •High upfront costs of switchable smart films compared to traditional glass treatments restrict adoption among cost-sensitive commercial and residential customers, requiring manufacturers to innovate on cost reduction.

- •Durability concerns under harsh environmental conditions, including UV exposure and temperature fluctuations, pose technical challenges impacting product lifespan and customer confidence.

- •Limited consumer awareness and misconceptions about smart film performance necessitate ongoing education and marketing efforts by industry stakeholders.

- •Complexities in ensuring compliance with electrical safety standards and energy codes across different states can delay product approvals and market entry.

- •Competition from established shading solutions such as blinds, curtains, and tinted glass, which are often perceived as more cost-effective and simpler to install, limits market penetration.

- •Supply chain disruptions and fluctuations in raw material costs, particularly for liquid crystals and specialty polymers, can lead to pricing volatility and production delays.

- •Balancing innovation with scalability remains a challenge, as manufacturers must optimize production processes to meet growing demand while maintaining quality and cost competitiveness.

Regulatory Framework

- •Between 2020 and 2025, the United States saw the implementation of the Energy Conservation and Building Codes Act updates, which mandated increased energy efficiency standards for commercial and residential buildings, encouraging the adoption of switchable smart films as part of compliant glazing solutions.

- •The National Electrical Code (NEC) revisions in 2023 introduced stricter electrical safety requirements for switchable film installations, impacting product certification processes and installation practices across states.

- •Environmental Protection Agency (EPA) initiatives launched in 2022 incentivize green building materials, including smart films that contribute to energy savings and reduced carbon footprints, through tax credits and grants.

- •California’s Title 24 Building Energy Efficiency Standards updated in 2024 require dynamic glazing solutions in new commercial buildings, significantly driving demand within the state and influencing broader market trends in the West Coast region.

- •The Occupational Safety and Health Administration (OSHA) released guidelines in 2021 for safe handling and disposal of smart film materials containing liquid crystals and polymers, fostering safer manufacturing and installation environments.

Market Intelligence

- •15th February 2025, SmartGlass International Inc. launched an advanced polymer dispersed liquid crystal film featuring enhanced durability and faster switching speeds tailored for commercial office buildings. This product incorporates IoT compatibility allowing integration with existing building automation systems for energy optimization. The launch aims to capture the growing demand for smart windows in the United States, particularly in West Coast high-rise developments. Strategic marketing efforts target architects and facility managers seeking sustainable, high-performance glazing solutions. Source: Official Company Website

- •10th May 2025, View, Inc. introduced a new line of electrochromic smart films with improved optical clarity and reduced power consumption, designed for large-scale retrofit projects in educational and healthcare facilities. The innovation provides seamless dimming functionality controlled via mobile applications, enhancing occupant comfort and energy management. This launch strengthens View’s market position in the United States, especially in the Northeast and Midwest regions where energy codes are becoming more stringent. The product also supports LEED certification goals, appealing to environmentally conscious clients. Source: Industry Publication

- •20th August 2024, SPD Technologies, Inc. announced a strategic partnership with a leading automotive manufacturer to supply suspended particle device films for sunroofs and privacy windows in electric vehicles. This collaboration aims to enhance passenger comfort and vehicle energy efficiency, aligning with increasing consumer demand for advanced automotive interiors. The partnership is expected to accelerate adoption of SPD films in the United States automotive sector, particularly in the Southeast region experiencing rapid EV market growth. Source: Official Press Release

- •5th November 2024, Polymer Vision Technologies secured a significant contract with a major commercial real estate developer to provide micro-blinds technology films for a new office complex in the Southwest. The films offer precise light control and durability, addressing tenant demands for privacy and aesthetic customization. This deal underscores the expanding role of smart films in commercial architecture across emerging growth zones within the United States. Source: Industry News

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 2.75 Billion |

| CAGR | 12.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | SmartGlass International Inc. (United States), Polytronix, Inc. (United States), Research Frontiers Inc. (United States), View, Inc. (United States), SPD Technologies, Inc. (United States) |

United States Switchable Smart Film Market - United States Size & Outlook 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.