Global High-precision GNSS Receiver Market Size, Growth & Revenue 2025-2034

Global High-precision GNSS Receiver Market is segmented by Product Type (Multi-frequency GNSS Receivers, Single-frequency GNSS Receivers, Network RTK GNSS Receivers, PPP GNSS Receivers, Differential GNSS Receivers), Application (Surveying and Mapping, Precision Agriculture, Construction and Infrastructure, Autonomous Vehicles, Defense and Security), Service Type (Hardware Sales, Software and Firmware Solutions, Positioning as a Service, Maintenance and Support), Deployment Model (Cloud-based Solutions, On-premise Systems, Hybrid Models), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The High-precision GNSS Receiver market globally is defined by devices that achieve exceptional positional accuracy through advanced satellite navigation technologies. These receivers utilize multi-constellation signals from GPS, GLONASS, Galileo, and BeiDou, augmented by correction methods like RTK and PPP to ensure centimeter-level precision critical for applications such as surveying, agriculture, construction, autonomous vehicles, and defense. The market encompasses a broad spectrum of product types including multi-frequency and single-frequency receivers, network RTK systems, and differential GNSS receivers, each tailored to specific use cases and operational environments. The value chain spans component manufacturing, software development for correction algorithms, system integration, distribution, and after-sales support, addressing the needs of a diverse clientele including government agencies, infrastructure developers, automotive OEMs, and precision farming enterprises. The market is driven by the rising demand for enhanced accuracy in location-based services, increasing automation in vehicles, and the expansion of smart infrastructure projects globally. Technological advancements integrating GNSS with IoT and AI further broaden the application landscape, fostering innovation. Moreover, regulatory frameworks mandating precision in navigation and positioning across sectors propel adoption. The High-precision GNSS Receiver market is poised for robust growth, fueled by expanding end-use industries and continuous technological refinement.

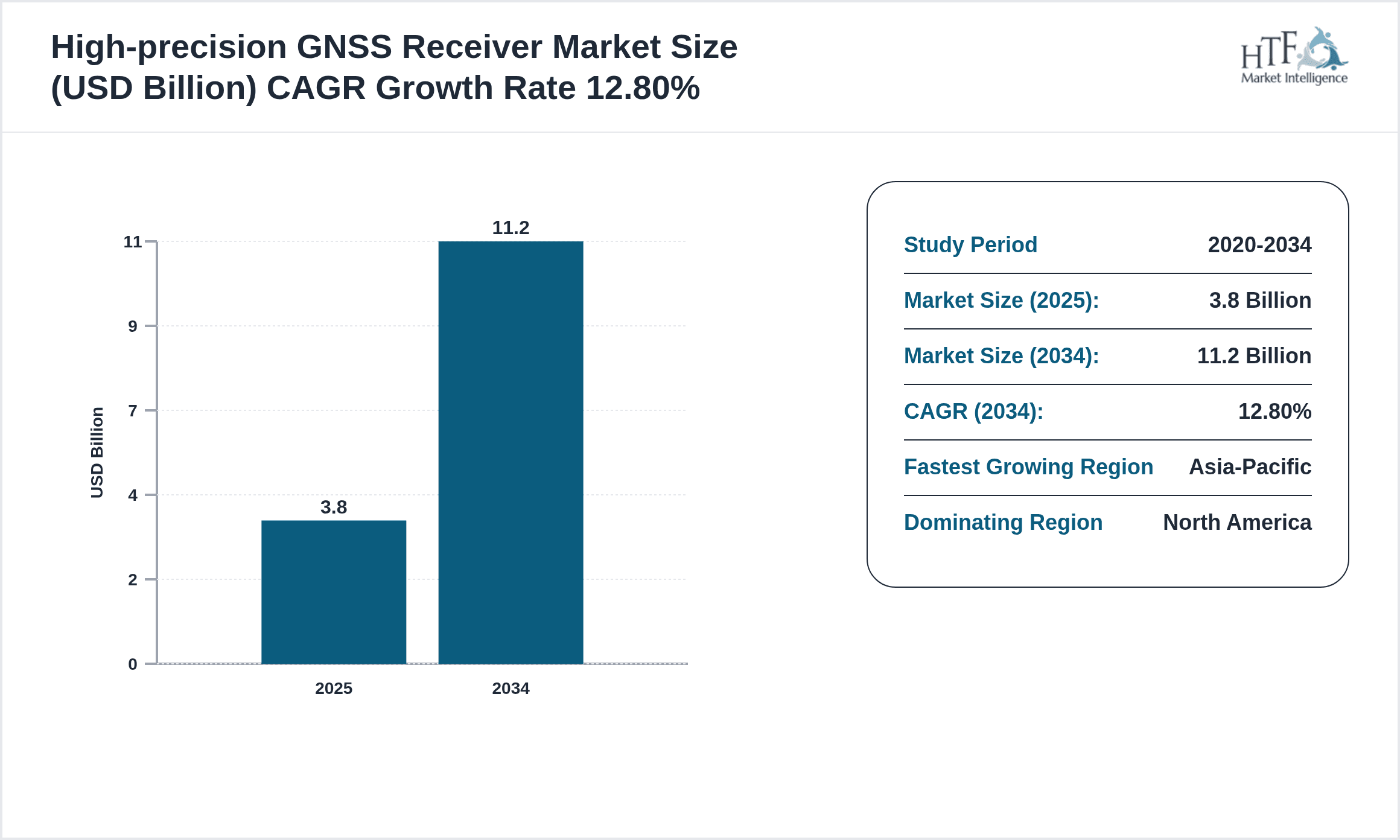

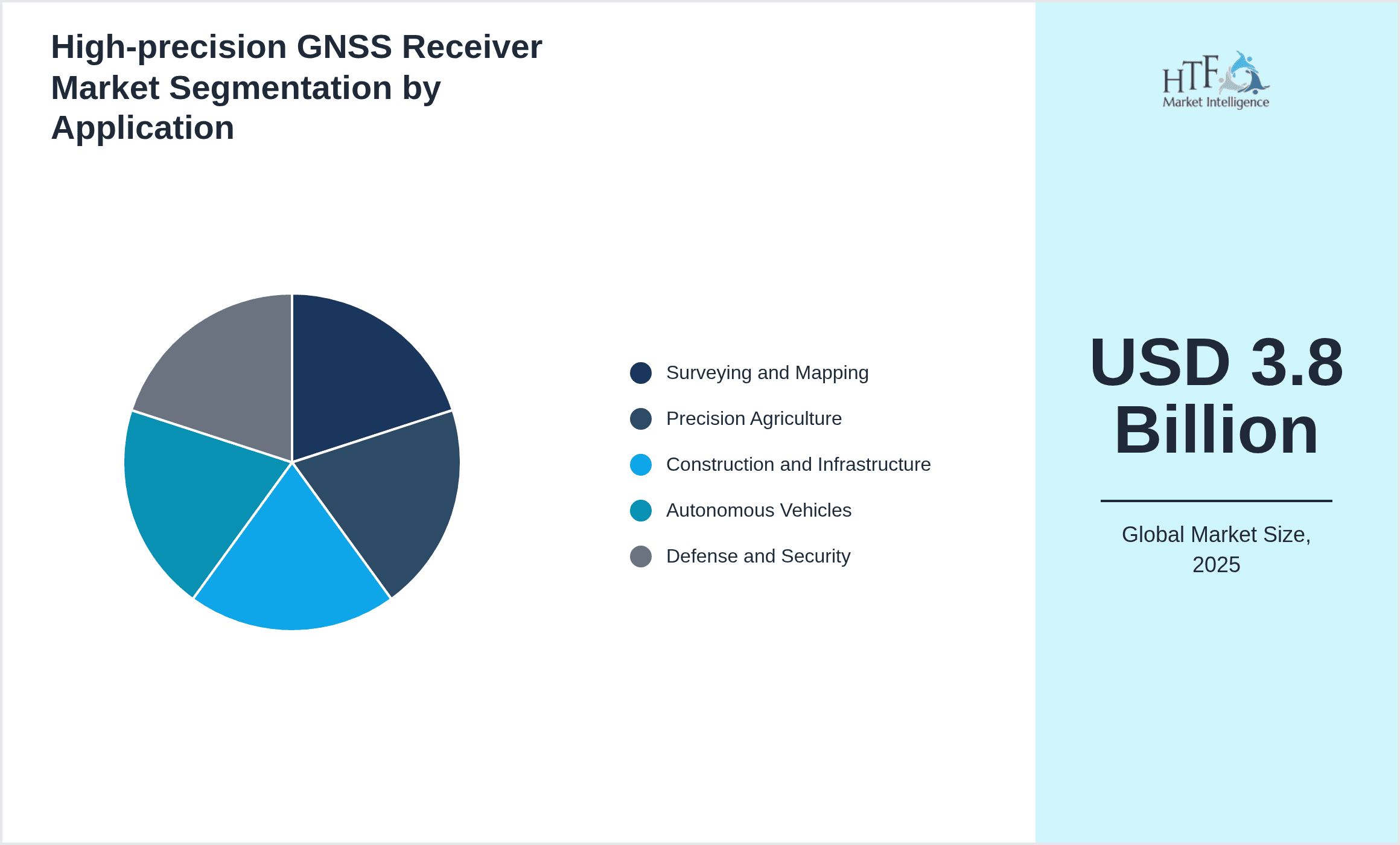

- •Market highlights include a base market size of USD 3.8 Billion in 2025, projected to reach USD 11.2 Billion by 2034, reflecting a CAGR of 12.8%. The Asia-Pacific region is expected to register the highest growth rate due to rapid industrialization, smart city initiatives, and increasing adoption in agriculture and autonomous vehicle sectors. North America maintains market dominance owing to early technology adoption, strong defense spending, and established infrastructure.

- •The value proposition of High-precision GNSS Receivers lies in their ability to deliver unparalleled positional accuracy, enabling enhanced operational efficiency, safety, and productivity across industries. For stakeholders including manufacturers, service providers, and end users, these technologies offer strategic advantages in precision agriculture, infrastructure development, autonomous navigation, and defense applications. The integration of GNSS with emerging technologies fosters innovation and opens new market avenues, making the sector a critical component of the global smart technology ecosystem.

Competitive Landscape

The global High-precision GNSS Receiver market is characterized by intense competition among leading technology providers and emerging innovators focusing on product differentiation, technological advancement, and strategic partnerships. Companies emphasize enhancing receiver sensitivity, multi-constellation compatibility, and integration with complementary technologies such as IoT and AI to maintain competitive advantage. Market players adopt various strategies including mergers and acquisitions to consolidate market share and expand geographic presence, while investing significantly in R&D to introduce next-generation GNSS receivers with improved accuracy and robustness. Pricing strategies vary with product sophistication and application-specific customization, influencing distribution channel dynamics. Regional competition is influenced by technology adoption rates, regulatory environments, and infrastructure development, with North America and Europe showcasing mature markets and Asia-Pacific emerging as a highly dynamic growth region. Future trends indicate increasing convergence of GNSS with cloud computing and edge analytics, amplifying competitive pressures and innovation pace.

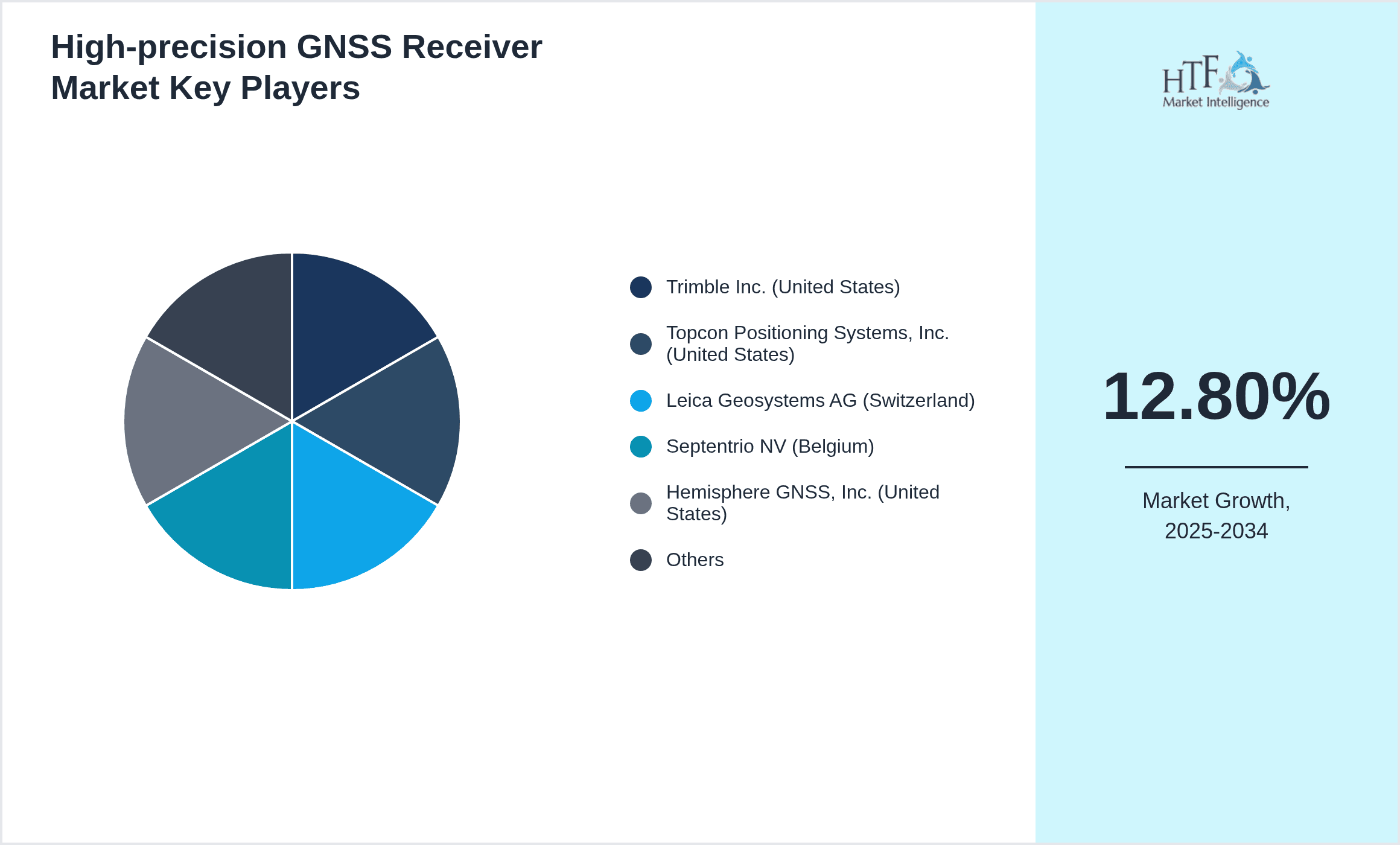

Leading Companies in High-precision GNSS Receiver Market

- •Trimble Inc. (United States)

- •Topcon Positioning Systems, Inc. (United States)

- •Leica Geosystems AG (Switzerland)

- •Septentrio NV (Belgium)

- •Hemisphere GNSS, Inc. (United States)

- •NovAtel Inc. (Canada)

- •CHC Navigation (China)

- •Javad GNSS (United States)

- •ComNav Technology Ltd. (China)

- •Unicore Communications Inc. (United States)

- •Garmin Ltd. (Switzerland)

- •Tersus GNSS (United States)

- •Sokkia Co., Ltd. (Japan)

- •NavCom Technology, Inc. (United States)

- •Racelogic Ltd. (United Kingdom)

- •Stonex Srl (Italy)

- •Furuno Electric Co., Ltd. (Japan)

- •South Survey Instruments Co., Ltd. (China)

- •Geodetics Inc. (United States)

- •Ashtech (United States)

- •GeoMax AG (Switzerland)

- •Sokkia Co., Ltd. (Japan)

- •CHC Navigation (China)

- •Piksi Multi GNSS Receiver (United States)

- •NovAtel Inc. (Canada)

Market Breakdown

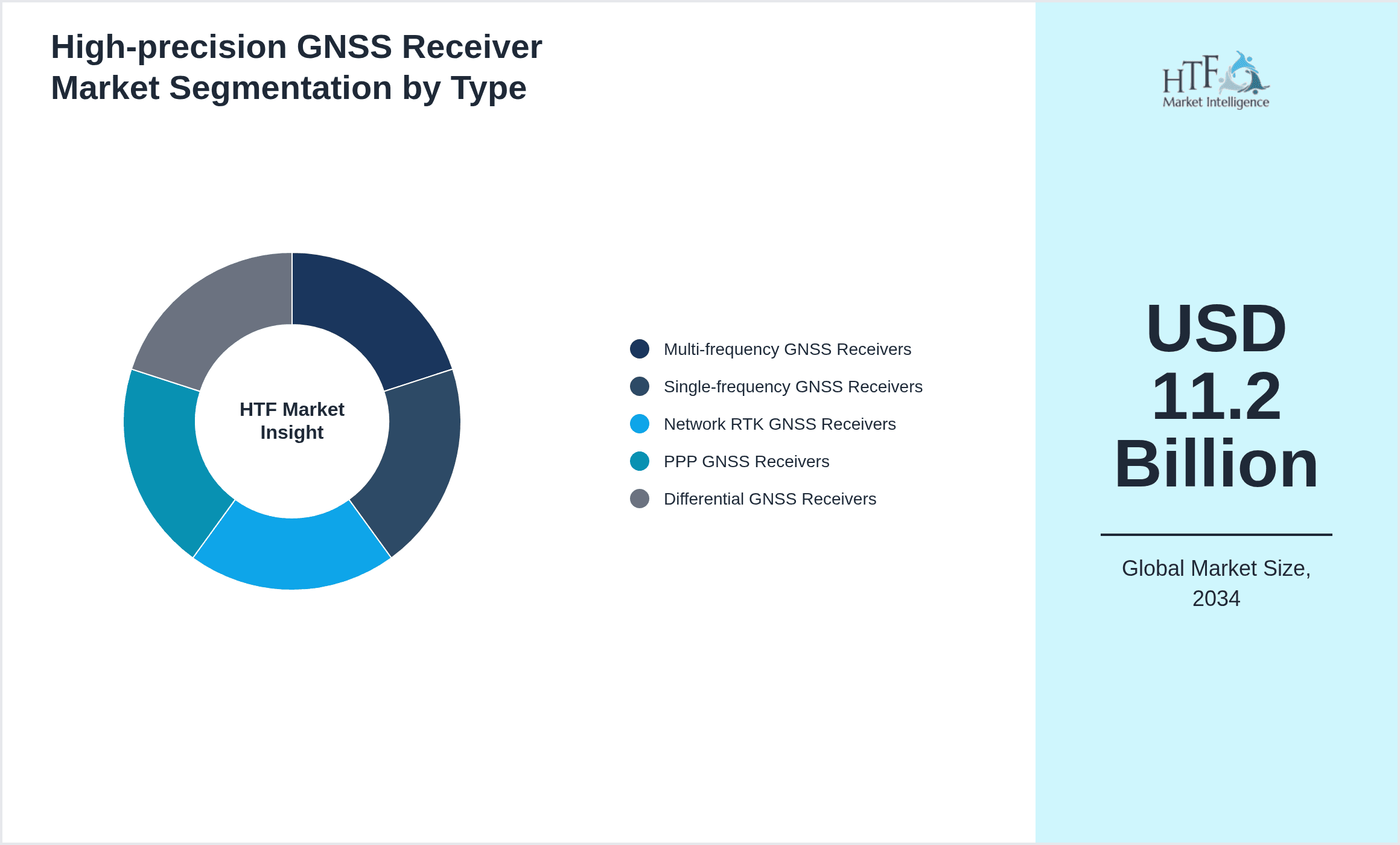

- •By Product Type

- ◦Multi-frequency GNSS Receivers

- ◦Single-frequency GNSS Receivers

- ◦Network RTK GNSS Receivers

- ◦PPP GNSS Receivers

- ◦Differential GNSS Receivers

- •By Application

- ◦Surveying and Mapping

- ◦Precision Agriculture

- ◦Construction and Infrastructure

- ◦Autonomous Vehicles

- ◦Defense and Security

- •By Service Type

- ◦Hardware Sales

- ◦Software and Firmware Solutions

- ◦Positioning as a Service

- ◦Maintenance and Support

- •By Deployment Model

- ◦Cloud-based Solutions

- ◦On-premise Systems

- ◦Hybrid Models

Growth Dynamics

- •The rising adoption of precision agriculture techniques is a primary growth driver, enabling farmers to optimize resource use and increase crop yields through accurate field mapping and real-time positioning. This adoption is supported by government subsidies and increasing awareness of sustainable farming practices globally.

- •Expansion in autonomous vehicle development necessitates high-precision GNSS receivers for accurate navigation and safety systems. Partnerships between GNSS technology providers and automotive OEMs accelerate market growth by addressing stringent accuracy and reliability requirements.

- •Infrastructure modernization projects in urban and rural areas drive demand for GNSS receivers in surveying and construction, improving project efficiency and reducing costs through precise spatial data collection and monitoring.

- •Technological advancements, such as integration of GNSS with IoT and AI, enhance real-time data processing capabilities, fostering new applications and expanding market opportunities across sectors like logistics and defense.

- •Increasing government regulations mandating high accuracy in navigation for safety and operational efficiency stimulate investments in GNSS technologies, further propelling market expansion.

- •Growing investments in satellite constellations and augmentation systems improve GNSS signal availability and integrity, boosting confidence among end users and stimulating market demand.

- •Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to rapid industrialization, urbanization, and adoption of advanced positioning technologies in various industries.

Market Trends

- •Increasing adoption of multi-constellation and multi-frequency GNSS receivers enhances positioning accuracy and robustness, a trend driven by the need for reliable navigation in complex environments such as urban canyons and dense forests.

- •Integration of GNSS receivers with cloud computing platforms enables advanced data analytics and real-time monitoring, improving operational decision-making across applications including fleet management and precision agriculture.

- •Growing focus on miniaturization and power efficiency in GNSS receiver design supports expanding use in portable and wearable devices, opening new consumer and industrial application segments.

- •Collaborations between GNSS manufacturers and software providers are facilitating the development of customized solutions tailored to specific industry needs, enhancing user experience and market penetration.

- •Rising demand for autonomous drones in surveying, agriculture, and logistics sectors drives innovation in GNSS receiver technologies optimized for UAV applications.

- •Sustainability trends are influencing the market, with GNSS technology enabling efficient resource management and reduced environmental impact in agriculture and construction industries.

- •Emerging use of GNSS in augmented reality (AR) and virtual reality (VR) applications fosters development of receivers capable of delivering ultra-precise positional information for immersive experiences.

Market Opportunities

- •Expansion of network RTK services in developing regions presents significant market opportunities by providing affordable and high-accuracy positioning solutions to new user bases.

- •Development of integrated GNSS and sensor fusion systems offers growth potential in autonomous navigation and robotics, enhancing accuracy and reliability under challenging conditions.

- •Increasing investments in smart city initiatives globally create demand for GNSS-enabled infrastructure monitoring and asset management solutions, supporting sustainable urban development.

- •Untapped markets in Latin America and Middle East & Africa provide opportunities for market players to establish presence through localized solutions and partnerships with regional stakeholders.

- •Advancements in PPP GNSS technology enable broader applications in maritime and aviation navigation, expanding the market scope beyond terrestrial use cases.

- •Collaborations with telecommunication providers to offer GNSS-based positioning as a service could unlock recurring revenue streams and enhance product offerings.

- •Innovation in low-power GNSS receivers supports growth in wearable technology and IoT devices, creating new consumer and industrial market segments.

Market Challenges

- •High costs associated with advanced GNSS receiver technology limit adoption among small and medium enterprises, especially in developing economies, constraining market penetration.

- •Signal interference and multipath effects in urban and indoor environments pose technical challenges that affect the accuracy and reliability of GNSS receivers.

- •Regulatory complexities and varying standards across regions create barriers for global product deployment and increase compliance costs for manufacturers.

- •Intense competition and price sensitivity in the market pressure profit margins, necessitating continuous innovation and cost optimization by market players.

- •Lack of skilled workforce and technical expertise in emerging markets hampers effective utilization and maintenance of high-precision GNSS systems.

- •Cybersecurity risks associated with GNSS spoofing and jamming require robust countermeasures, increasing complexity and costs for end users and providers.

- •Supply chain disruptions for critical components impact production schedules and market availability, affecting overall market growth trajectories.

Regulatory Framework

- •From 2020 to 2025, multiple regions have implemented regulations mandating high accuracy and reliability standards for GNSS-based navigation in safety-critical sectors such as aviation and maritime. For instance, the International Civil Aviation Organization (ICAO) introduced performance requirements for GNSS augmentation systems to enhance flight safety, impacting receiver specifications globally.

- •The European Union enacted the Galileo GNSS program policies promoting interoperability and data security standards between GNSS systems, fostering market harmonization and encouraging adoption of multi-constellation receivers.

- •North America’s Federal Communications Commission (FCC) updated spectrum management regulations to minimize GNSS interference, supporting market growth by ensuring signal integrity for receivers used in critical infrastructure and defense applications.

- •Asia-Pacific countries such as Japan and South Korea introduced mandates for GNSS-enabled autonomous vehicle navigation systems, accelerating demand for high-precision receivers compliant with safety and operational standards.

- •Government incentives and funding programs have been established across major regions to support research and development in GNSS technology, facilitating innovation and market expansion through collaborative initiatives between public and private sectors.

Market Intelligence

- •15th February 2025, Trimble Inc. launched the Trimble R12i GNSS receiver featuring advanced multi-frequency technology with enhanced RTK capabilities designed for precision agriculture and construction markets. The product incorporates inertial measurement unit (IMU) technology for improved performance in challenging environments, targeting increased operational efficiency and reliability. This launch strengthens Trimble’s portfolio by addressing market demand for rugged, high-accuracy receivers with seamless integration into cloud platforms. The initiative aligns with global trends towards digital transformation in geospatial data acquisition and autonomous navigation applications. Source: Official Trimble Press Release

- •3rd June 2025, NovAtel Inc. introduced the SMART6-L GNSS receiver, a compact, low-power, multi-constellation device optimized for unmanned aerial vehicles (UAVs) and autonomous robotic systems. The receiver offers enhanced signal tracking and anti-jamming features, supporting demanding applications in surveying and defense. NovAtel’s innovation aims to capture growing UAV market segments by delivering precise navigation solutions with reduced weight and power consumption. This product launch reflects the company’s strategic focus on expanding into emerging markets and leveraging IoT connectivity. Source: NovAtel Corporate Website

- •20th September 2024, Leica Geosystems AG announced a strategic partnership with a leading cloud analytics provider to develop integrated GNSS data processing solutions. The collaboration targets enhanced real-time positioning accuracy through cloud-based correction services and AI-powered analytics, aimed at infrastructure and autonomous vehicle applications. This initiative is expected to accelerate the adoption of cloud-enabled GNSS technologies, improve user experience, and expand Leica’s market reach. The partnership demonstrates a trend toward ecosystem development and service-based revenue models in the GNSS industry. Source: Industry Publication – Geospatial Today

- •12th January 2025, Hemisphere GNSS, Inc. completed the acquisition of a software startup specializing in GNSS signal integrity and spoofing detection technologies. The acquisition aims to enhance Hemisphere’s product portfolio with advanced cybersecurity features, addressing increasing concerns over GNSS vulnerabilities in defense and critical infrastructure sectors. This move consolidates Hemisphere’s position as a technology leader and reflects broader industry trends prioritizing security and resilience in navigation systems. The integration is expected to accelerate innovation and market differentiation. Source: Hemisphere GNSS Official Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 11.2 Billion |

| CAGR | 12.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.1% |

| Scope of Report | Market is segmented by Product Type (Multi-frequency GNSS Receivers, Single-frequency GNSS Receivers, Network RTK GNSS Receivers, PPP GNSS Receivers, Differential GNSS Receivers), Application (Surveying and Mapping, Precision Agriculture, Construction and Infrastructure, Autonomous Vehicles, Defense and Security), Service Type (Hardware Sales, Software and Firmware Solutions, Positioning as a Service, Maintenance and Support), Deployment Model (Cloud-based Solutions, On-premise Systems, Hybrid Models) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Trimble Inc. (United States), Topcon Positioning Systems, Inc. (United States), Leica Geosystems AG (Switzerland), Septentrio NV (Belgium), Hemisphere GNSS, Inc. (United States), NovAtel Inc. (Canada), CHC Navigation (China), Javad GNSS (United States), ComNav Technology Ltd. (China), Unicore Communications Inc. (United States), Garmin Ltd. (Switzerland), Tersus GNSS (United States), Sokkia Co., Ltd. (Japan), NavCom Technology, Inc. (United States), Racelogic Ltd. (United Kingdom), Stonex Srl (Italy), Furuno Electric Co., Ltd. (Japan), South Survey Instruments Co., Ltd. (China), Geodetics Inc. (United States), Ashtech (United States), GeoMax AG (Switzerland), Sokkia Co., Ltd. (Japan), CHC Navigation (China), Piksi Multi GNSS Receiver (United States), NovAtel Inc. (Canada) |

Global High-precision GNSS Receiver Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.