Global Aluminium Sheathed Cable Market Size, Growth & Revenue 2025-2034

Global Aluminium Sheathed Cable Market is segmented by Cable Type (Low Voltage Aluminium Sheathed Cable, Medium Voltage Aluminium Sheathed Cable, High Voltage Aluminium Sheathed Cable, Control Cables, Specialty Cables), Application Sector (Residential, Commercial, Industrial, Infrastructure, Utilities), Service Type (Installation Services, Maintenance Services, Testing & Certification Services, Repair Services), Deployment Model (Overhead, Underground, Direct Buried), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global aluminium sheathed cable market represents a critical segment within the electrical cable industry, characterized by cables enveloped with aluminium sheathing that offers enhanced mechanical protection, corrosion resistance, and electrical conductivity. These cables find extensive use across residential, commercial, industrial, infrastructure, and utility sectors, facilitating safe and efficient transmission and distribution of electrical power. The market spans a broad spectrum of product types based on voltage classification—ranging from low voltage for domestic wiring to high voltage cables used in heavy industrial and energy sectors. The supply chain integrates raw material suppliers, cable manufacturers, and distributors, culminating in end-users who demand high-performance, durable cabling solutions to meet growing infrastructure needs. Technological advancements including improved sheathing materials and insulation technologies are driving product innovation, while regulatory frameworks ensure safety and quality standards. Increasing urban development, industrialization, and rising investments in infrastructure projects globally are pivotal in propelling market growth. Furthermore, sustainability considerations such as recyclability of aluminium and energy-efficient manufacturing practices are influencing market dynamics and stakeholder strategies. This market is poised for robust expansion driven by demand for reliable electrical infrastructure and the replacement of traditional cabling systems with aluminium sheathed alternatives that offer longevity and safety benefits.

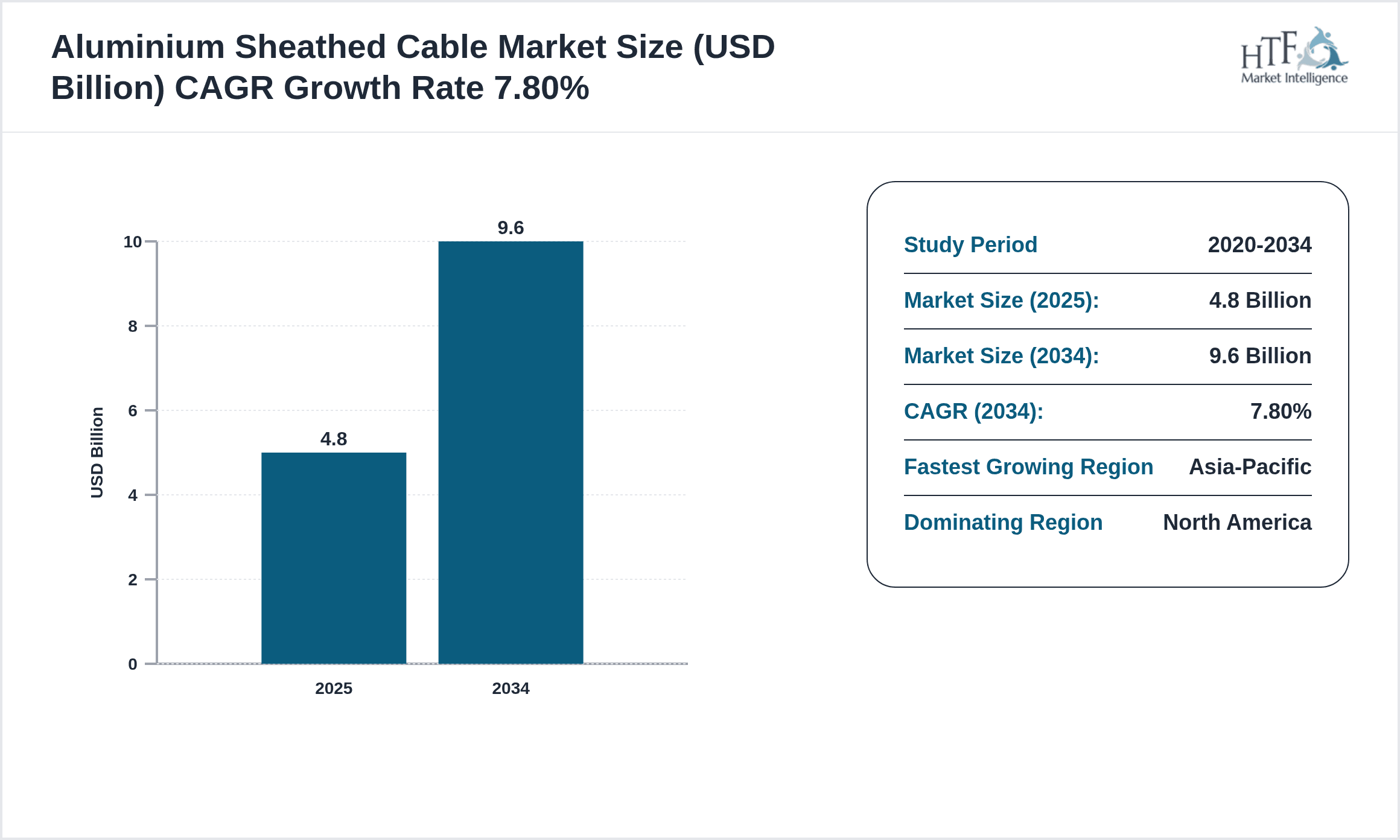

- •Key highlights indicate the market's valuation at USD 4.8 Billion in 2025, with a forecast to reach USD 9.6 Billion by 2034, demonstrating a compound annual growth rate (CAGR) of 7.8%. The year-on-year growth rate stands at approximately 7.4%, reflecting steady demand across major global regions. North America currently dominates the market due to its mature infrastructure and stringent safety regulations, while Asia-Pacific is recognized as the fastest-growing region, stimulated by rapid urbanization and industrial expansion. Low voltage aluminium sheathed cables hold the largest market share, driven by extensive residential and commercial applications, whereas high voltage cables exhibit the fastest growth attributed to new power generation and transmission projects in emerging economies.

- •The global aluminium sheathed cable market holds strategic importance for industries such as construction, energy, transportation, and utilities, offering enhanced safety, reliability, and cost efficiency compared to traditional cabling solutions. Stakeholders including manufacturers, distributors, and end-users benefit from ongoing advancements in cable technology and expanding applications in smart grids, renewable energy integration, and infrastructure modernization. The market’s growth trajectory is supported by favorable regulatory environments and increasing investments in electrification projects worldwide, making aluminium sheathed cables indispensable in the evolving electrical infrastructure landscape.

Competitive Landscape

The global aluminium sheathed cable market is intensely competitive, characterized by the presence of numerous multinational corporations and regional players who continuously innovate to maintain market share and address evolving customer needs. Competitive dynamics focus on product differentiation through advanced sheathing technology, improved insulation materials, and compliance with international safety standards. Market participants adopt varied strategies including strategic partnerships, mergers and acquisitions, and regional expansions to enhance their footprint and operational capabilities. Emphasis is placed on research and development to introduce cables capable of withstanding harsh environmental conditions and meeting stringent electrical performance benchmarks. Pricing strategies vary with product specifications and end-use applications, creating a diverse competitive landscape that balances cost-effectiveness with quality. Distribution channels range from direct sales to partnerships with electrical contractors and infrastructure developers, ensuring wide market reach. Barriers to entry include high capital investments and regulatory compliance, which favor established players with robust manufacturing and supply chain networks. Regional competition is influenced by localized demand patterns and regulatory frameworks, with Asia-Pacific emerging as a hotspot for growth and innovation. Looking forward, the landscape is expected to evolve with the integration of smart cable technologies and sustainability-driven product development, underscoring the importance of agility and innovation for sustained competitive advantage.

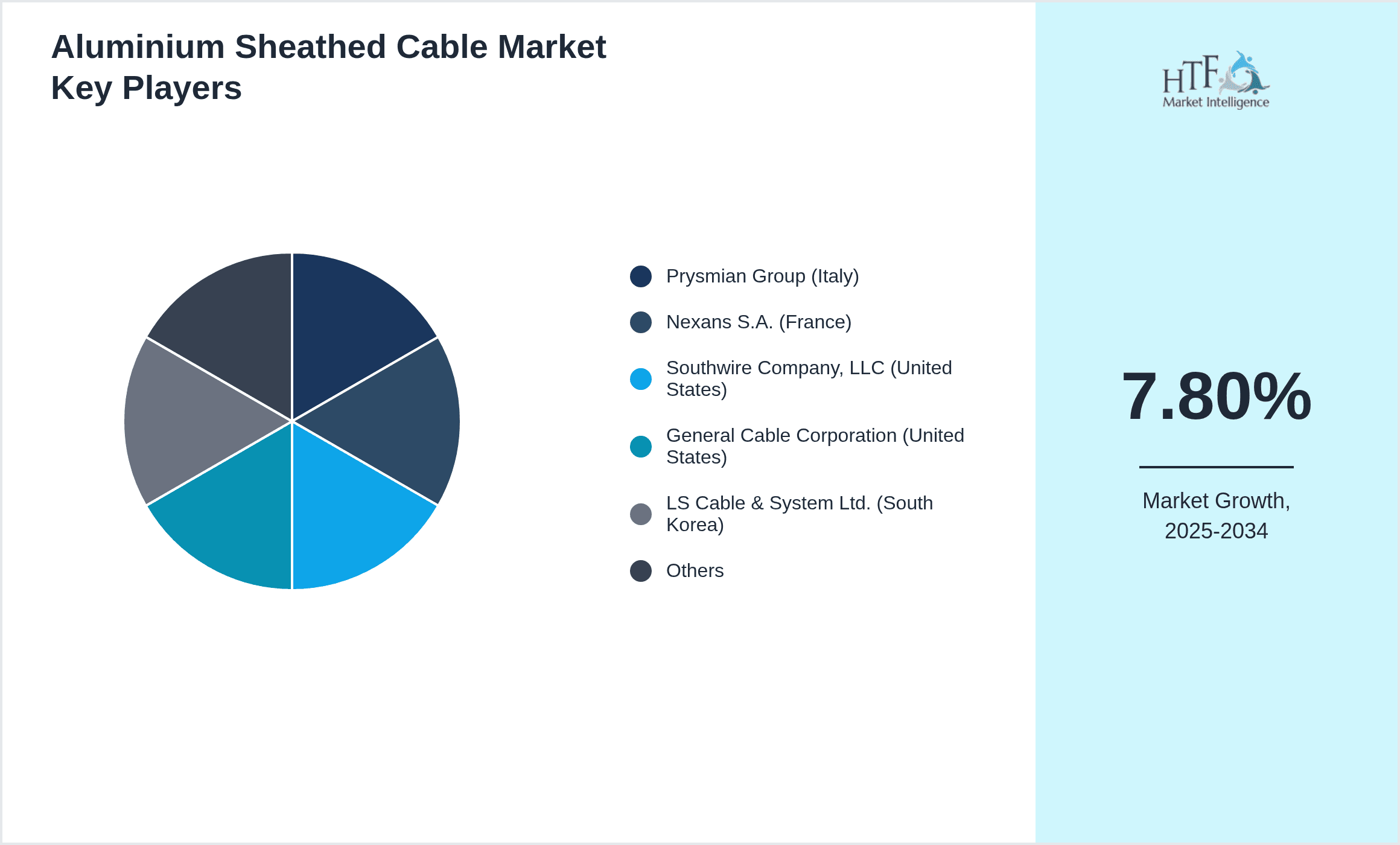

Leading Companies in Aluminium Sheathed Cable Market

- •Prysmian Group (Italy)

- •Nexans S.A. (France)

- •Southwire Company, LLC (United States)

- •General Cable Corporation (United States)

- •LS Cable & System Ltd. (South Korea)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Hengtong Group (China)

- •KEI Industries Limited (India)

- •Furukawa Electric Co., Ltd. (Japan)

- •NKT A/S (Denmark)

- •Encore Wire Corporation (United States)

- •Belden Inc. (United States)

- •Polycab India Limited (India)

- •Top Cable Corporation (China)

- •Sumitomo Wiring Systems, Ltd. (Japan)

- •South East Cable Manufacturers Ltd. (India)

- •Universal Cables Limited (India)

- •Havells India Limited (India)

- •Chint Group (China)

- •FLEX (United States)

- •ABB Ltd. (Switzerland)

- •Molex LLC (United States)

- •Leoni AG (Germany)

- •Prysmian Cavi e Sistemi Energia S.r.l (Italy)

- •Sumitomo Corporation (Japan)

Market Breakdown

- •By Cable Type

- ◦Low Voltage Aluminium Sheathed Cable

- ◦Medium Voltage Aluminium Sheathed Cable

- ◦High Voltage Aluminium Sheathed Cable

- ◦Control Cables

- ◦Specialty Cables

- •By Application Sector

- ◦Residential

- ◦Commercial

- ◦Industrial

- ◦Infrastructure

- ◦Utilities

- •By Service Type

- ◦Installation Services

- ◦Maintenance Services

- ◦Testing & Certification Services

- ◦Repair Services

- •By Deployment Model

- ◦Overhead

- ◦Underground

- ◦Direct Buried

Growth Dynamics

- •The surge in global infrastructure development, especially in emerging economies, is a key growth driver, with aluminium sheathed cables preferred for their lightweight and corrosion-resistant properties, enhancing installation efficiency and longevity in power distribution networks.

- •Rising demand for safer and fire-resistant electrical wiring in residential and commercial buildings is propelling market expansion, as aluminium sheathed cables meet stringent safety standards and reduce fire hazards compared to conventional cables.

- •Government initiatives promoting electrification and smart grid deployments across multiple regions are accelerating adoption, with investments channeled towards upgrading existing power infrastructure using advanced aluminium sheathed cabling solutions.

- •Technological advancements in sheathing materials and insulation technology are enabling the development of cables with superior mechanical strength and thermal stability, broadening application possibilities and improving market competitiveness.

- •Increasing urbanization and industrialization worldwide intensify the need for reliable electrical infrastructure, driving demand for aluminium sheathed cables in sectors such as manufacturing, transportation, and utilities.

- •Growing environmental awareness and regulatory push for sustainable materials are encouraging manufacturers to adopt aluminium, which is recyclable and offers lower environmental impact compared to copper-sheathed alternatives.

- •Expansion of renewable energy projects such as solar and wind farms requires specialized high voltage aluminium sheathed cables for efficient power transmission, contributing to the fastest growth segment in the market.

Market Trends

- •The trend toward integrating smart cable technologies with sensors for real-time condition monitoring is gaining traction, enabling predictive maintenance and reducing downtime in power distribution systems.

- •Manufacturers are increasingly adopting eco-friendly materials and green manufacturing processes to align with global sustainability goals, enhancing brand reputation and compliance with environmental regulations.

- •Customization and modular cable solutions tailored to specific customer requirements are becoming prevalent, allowing for enhanced flexibility and efficiency in installation and operation.

- •Collaborations between cable manufacturers and infrastructure developers are on the rise, facilitating co-development of cables optimized for specialized applications such as offshore wind farms and urban transit networks.

- •Digitalization of supply chains and adoption of Industry 4.0 technologies in cable manufacturing are improving production efficiency, quality control, and inventory management across the value chain.

- •Rising adoption of aluminium sheathed cables in replacement projects of aging copper infrastructure is reshaping market dynamics, driven by cost-effectiveness and performance advantages.

- •Increasing regulatory emphasis on fire safety and electrical standards globally is reinforcing market demand for aluminium sheathed cables that comply with enhanced safety certifications.

Market Opportunities

- •Expanding electrification in remote and rural areas presents significant opportunities for aluminium sheathed cables due to their durability and ease of installation in challenging environments.

- •The rising deployment of renewable energy infrastructure globally offers promising avenues for high voltage aluminium sheathed cables tailored to specialized power transmission needs.

- •Growth in smart city initiatives worldwide drives demand for advanced cabling solutions integrating sensor technologies for enhanced grid management and energy efficiency.

- •Emerging markets in Latin America and Middle East & Africa exhibit underpenetrated potential with increasing investments in infrastructure and energy sectors requiring robust cabling systems.

- •Technological innovation in lightweight, flexible, and fire-resistant materials can unlock new application areas, including transportation and data centers, expanding market reach.

- •Strategic partnerships between cable manufacturers and construction firms can facilitate integrated project delivery, improving installation timelines and reducing costs.

- •Digital transformation in cable manufacturing and supply chain management offers opportunities for operational efficiencies and enhanced customer responsiveness.

Market Challenges

- •Volatility in raw material prices, particularly aluminium and insulating polymers, poses cost challenges affecting pricing stability and profit margins for manufacturers.

- •Intense competition from copper sheathed cables and alternative materials limits market penetration in regions with established copper infrastructure and cost preferences.

- •Stringent and varying regulatory requirements across different countries complicate compliance and increase time-to-market for new cable products.

- •Technical challenges in ensuring long-term performance and reliability of aluminium sheathed cables under extreme environmental conditions require ongoing R&D investment.

- •Limited awareness and preference for aluminium cables in some end-user segments hinder market adoption despite technical advantages.

- •Supply chain disruptions due to geopolitical tensions or global events can affect raw material availability and delivery schedules, impacting market growth.

- •High initial installation costs and infrastructure adaptation requirements can deter adoption in cost-sensitive markets despite lifecycle benefits.

Regulatory Framework

- •Between 2020 and 2025, the National Electrical Code (NEC) updates in the United States introduced stricter requirements for fire resistance and safety in cable installations, mandating enhanced testing and certification for aluminium sheathed cables to ensure compliance and market acceptance.

- •The European Union implemented the Construction Products Regulation (CPR) in 2017 with ongoing enforcement through 2025, requiring cables to meet harmonized fire performance standards, thus influencing product development and certification in the aluminium sheathed cable segment.

- •China's GB/T standards for electrical cables were revised between 2020 and 2025 to incorporate higher durability and environmental resistance criteria, impacting manufacturing processes and quality control for aluminium cable producers targeting the domestic market.

- •India's Bureau of Indian Standards (BIS) updated the IS 1554 series standards during 2023-2025, emphasizing enhanced mechanical protection and corrosion resistance for sheathed cables, which has prompted industry-wide product upgrades and certification drives.

- •Government incentives in various regions promote the use of recyclable and sustainable materials in electrical infrastructure, indirectly supporting aluminium sheathed cables due to aluminium's recyclability and favorable environmental profile, shaping regulatory and market trends.

Market Intelligence

- •15th February 2025, Prysmian Group announced the launch of its new range of high voltage aluminium sheathed cables designed for renewable energy projects, featuring enhanced thermal stability and corrosion resistance. This product line targets offshore wind farms and solar power plants, aiming to support the growing global shift towards sustainable energy infrastructure. The launch includes advanced manufacturing techniques that reduce production emissions and improve cable lifespan. Prysmian’s strategic objective is to capture emerging market segments by providing reliable and eco-friendly cabling solutions, enhancing its competitive positioning. Source: Prysmian Group Official Press Release.

- •10th April 2025, Nexans S.A. introduced an innovative smart cable system integrating sensor technology within aluminium sheathed cables for real-time monitoring of electrical load and cable health. This innovation is expected to transform maintenance practices by enabling predictive analytics and reducing operational downtime in utility networks. Nexans has positioned this product to cater to smart grid deployments globally, leveraging IoT capabilities for enhanced grid resilience and efficiency. The company anticipates this launch will accelerate adoption of aluminium sheathed cables in technologically advanced infrastructure projects. Source: Nexans Corporate News.

- •20th June 2025, Southwire Company completed the acquisition of a regional cable manufacturer specializing in aluminium sheathed cables for industrial applications in Latin America. This strategic move aims to expand Southwire’s footprint in high-growth emerging markets and diversify its product portfolio. The acquisition is expected to generate synergies through combined manufacturing capabilities and broaden distribution channels. Southwire’s focus on strengthening regional presence aligns with global growth trends and increasing demand for durable electrical cabling solutions in industrial sectors. Source: Southwire Company Official Announcement.

- •5th August 2025, LS Cable & System Ltd. announced a partnership with a leading infrastructure developer in Asia-Pacific to supply medium voltage aluminium sheathed cables for a major urban transit project. This collaboration underscores LS Cable’s commitment to supporting large-scale infrastructure developments with customized cabling solutions designed for high safety and performance standards. The partnership also incorporates joint R&D efforts to innovate cable design tailored to the unique requirements of mass transit systems. This initiative demonstrates the growing integration of aluminium sheathed cables in public infrastructure expansion. Source: LS Cable & System Ltd. Press Release.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 9.6 Billion |

| CAGR | 7.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.4% |

| Scope of Report | Market is segmented by Cable Type (Low Voltage Aluminium Sheathed Cable, Medium Voltage Aluminium Sheathed Cable, High Voltage Aluminium Sheathed Cable, Control Cables, Specialty Cables), Application Sector (Residential, Commercial, Industrial, Infrastructure, Utilities), Service Type (Installation Services, Maintenance Services, Testing & Certification Services, Repair Services), Deployment Model (Overhead, Underground, Direct Buried) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Prysmian Group (Italy), Nexans S.A. (France), Southwire Company, LLC (United States), General Cable Corporation (United States), LS Cable & System Ltd. (South Korea), Sumitomo Electric Industries, Ltd. (Japan), Hengtong Group (China), KEI Industries Limited (India), Furukawa Electric Co., Ltd. (Japan), NKT A/S (Denmark), Encore Wire Corporation (United States), Belden Inc. (United States), Polycab India Limited (India), Top Cable Corporation (China), Sumitomo Wiring Systems, Ltd. (Japan), South East Cable Manufacturers Ltd. (India), Universal Cables Limited (India), Havells India Limited (India), Chint Group (China), FLEX (United States), ABB Ltd. (Switzerland), Molex LLC (United States), Leoni AG (Germany), Prysmian Cavi e Sistemi Energia S.r.l (Italy), Sumitomo Corporation (Japan) |

Global Aluminium Sheathed Cable Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.