Global Video Endoscopy System Market Size, Growth & Revenue 2025-2034

Global Video Endoscopy System Market is segmented by Type (Flexible Endoscopes, Rigid Endoscopes, Capsule Endoscopes, Single-Use Endoscopes, Video Endoscopes), Application (Gastroenterology, Urology, Gynecology, ENT (Ear, Nose, Throat), General Surgery), Service Type (Installation & Maintenance, Training & Support, Software & Integration Services, Consulting Services), Deployment Model (On-Premise Systems, Cloud-Based Solutions, Hybrid Deployment), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global video endoscopy system market comprises sophisticated medical imaging devices that facilitate visualization of internal body structures through minimally invasive techniques. These systems employ high-definition video technology, fiber optic cables, and advanced lighting to enable clinicians to perform diagnostic and therapeutic procedures across multiple specialties including gastroenterology, urology, gynecology, ENT, and general surgery. Key product categories include flexible endoscopes, rigid endoscopes, capsule endoscopes, single-use endoscopes, and video endoscopes, each designed to address specific clinical needs and improve patient outcomes. Innovations such as enhanced image clarity, integration of AI for real-time diagnostics, and the growing trend of disposable endoscopes to mitigate infection risks have propelled market expansion. The rising global burden of chronic diseases and increasing preference for minimally invasive surgeries are significant factors driving adoption. Furthermore, expanding healthcare infrastructure and rising healthcare expenditures in emerging economies offer substantial growth opportunities. Market dynamics also reflect a growing emphasis on outpatient procedures and enhanced patient comfort, positioning video endoscopy systems as indispensable in modern healthcare delivery. Ancillary services including device maintenance, training, and software integration further contribute to market growth, underscoring the comprehensive ecosystem supporting video endoscopy solutions worldwide.

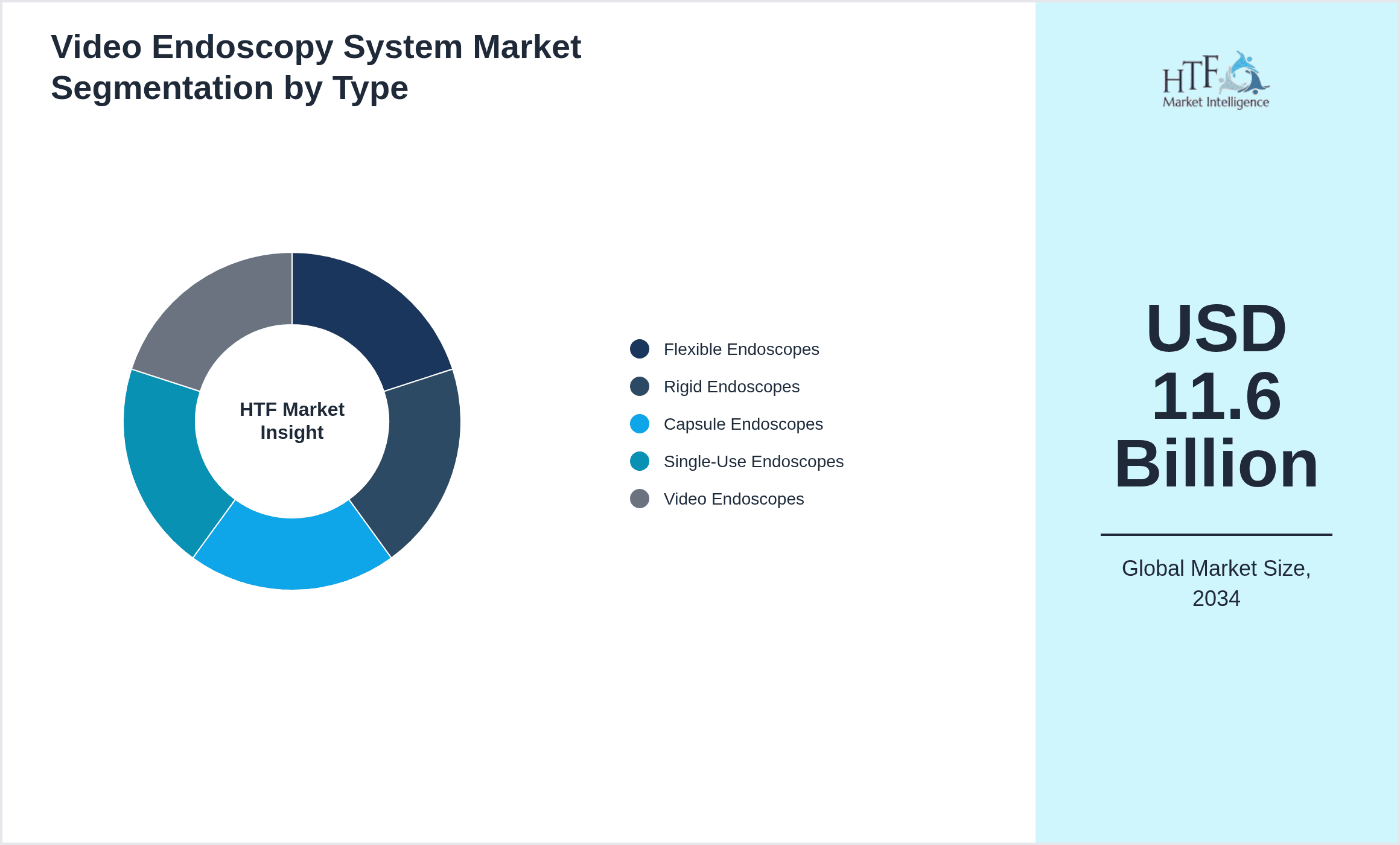

- •The market recorded a base size of USD 4.8 billion in 2025 and is projected to reach USD 11.6 billion by 2034, reflecting a robust CAGR of approximately 10.1% during the forecast period. This growth is fueled by technological advancements, increasing prevalence of gastrointestinal and urological disorders, and growing demand for single-use endoscopes to address infection control concerns. North America dominates the market, accounting for the largest share due to advanced healthcare infrastructure and high adoption rates, while Asia-Pacific is the fastest growing region driven by expanding healthcare access and government initiatives. Key product segments leading growth include flexible endoscopes and single-use endoscopes, the latter rapidly gaining traction for their infection prevention benefits. Market trends emphasize digital integration, AI-enabled diagnostics, and portable endoscopy systems enhancing clinical efficiency. Meanwhile, challenges such as high device costs and regulatory complexities persist, requiring manufacturers to innovate and streamline compliance. Strategic partnerships, mergers, and acquisitions continue to shape competitive dynamics, fostering innovation and geographic expansion.

- •Video endoscopy systems offer substantial value to healthcare providers, improving diagnostic precision and enabling minimally invasive interventions that reduce patient recovery times and hospital stays. These systems support a broad range of clinical applications, from routine diagnostics to complex surgeries, making them essential tools for specialists. The integration of AI and enhanced imaging technologies further empowers clinicians with real-time decision support, improving clinical outcomes and operational workflows. For medical device manufacturers and investors, the market promises sustained growth driven by technological innovation and expanding healthcare demands globally. Strategic investments in emerging markets and product diversification toward single-use and portable devices present lucrative opportunities. Additionally, the growing focus on infection control and patient safety reinforces the importance of video endoscopy systems in contemporary healthcare paradigms, enhancing their strategic relevance across hospital settings, ambulatory care centers, and specialized clinics worldwide.

Competitive Landscape

The global video endoscopy system market exhibits a highly competitive environment characterized by rapid technological innovation, strategic collaborations, and extensive product portfolios. Leading companies compete through continuous R&D investments to enhance imaging quality, device miniaturization, and integration with AI-enabled diagnostic platforms. Market players adopt diverse strategies including mergers and acquisitions, partnerships, and geographic expansion to strengthen market presence and access emerging markets. Pricing strategies are influenced by device sophistication and regulatory compliance costs, with players balancing affordability and innovation to capture diverse customer segments. Distribution channels encompass direct sales, distributors, and e-commerce platforms, ensuring broad accessibility. Barriers to entry include stringent regulatory requirements and high capital investment for technology development. Regional competition intensifies as emerging market players introduce cost-effective solutions tailored to local needs. Future competitive trends indicate a shift toward personalized endoscopy solutions, cloud-based image management, and enhanced interoperability with hospital IT systems, driving differentiation and sustained market growth.

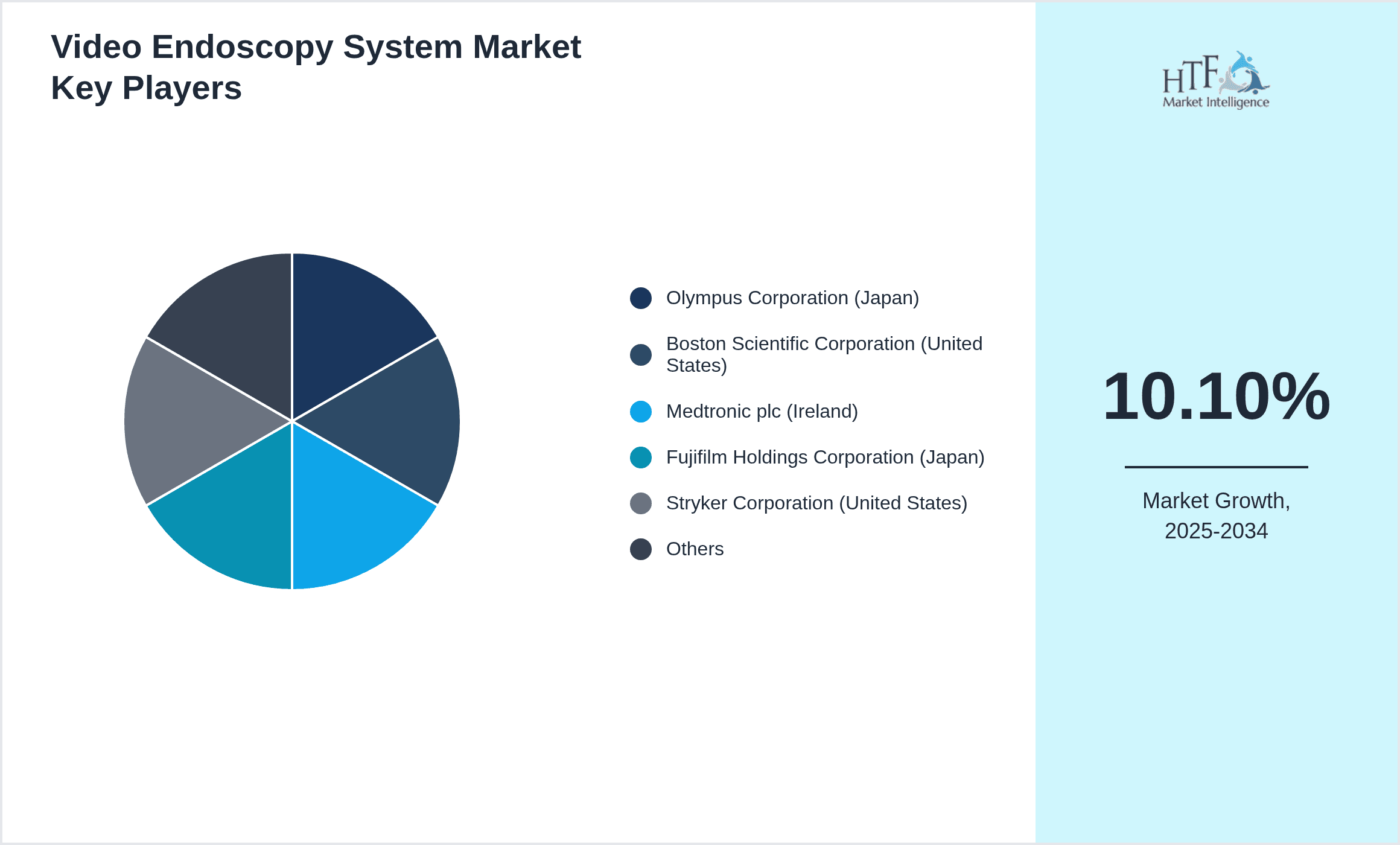

Leading Companies in Video Endoscopy System Market

- •Olympus Corporation (Japan)

- •Boston Scientific Corporation (United States)

- •Medtronic plc (Ireland)

- •Fujifilm Holdings Corporation (Japan)

- •Stryker Corporation (United States)

- •Karl Storz SE & Co. KG (Germany)

- •Richard Wolf GmbH (Germany)

- •Hoya Corporation (Japan)

- •Ambu A/S (Denmark)

- •ConMed Corporation (United States)

- •Pentax Medical (Japan)

- •Smith & Nephew plc (United Kingdom)

- •EndoChoice, Inc. (United States)

- •Cook Medical LLC (United States)

- •Medivators Inc. (United States)

- •Micro-Tech Endoscopy USA Inc. (United States)

- •Pentax of America, Inc. (United States)

- •Dentsply Sirona Inc. (United States)

- •Smiths Medical (United Kingdom)

- •Erbe Elektromedizin GmbH (Germany)

- •Medigus Ltd. (Israel)

- •Vivid Endoscopy (United States)

- •Sejong Medical (South Korea)

- •B. Braun Melsungen AG (Germany)

- •Cook Endoscopy (United States)

Market Breakdown

- •By Type

- ◦Flexible Endoscopes

- ◦Rigid Endoscopes

- ◦Capsule Endoscopes

- ◦Single-Use Endoscopes

- ◦Video Endoscopes

- •By Application

- ◦Gastroenterology

- ◦Urology

- ◦Gynecology

- ◦ENT (Ear, Nose, Throat)

- ◦General Surgery

- •By Service Type

- ◦Installation & Maintenance

- ◦Training & Support

- ◦Software & Integration Services

- ◦Consulting Services

- •By Deployment Model

- ◦On-Premise Systems

- ◦Cloud-Based Solutions

- ◦Hybrid Deployment

Growth Dynamics

The global video endoscopy system market growth is primarily driven by the rising incidence of chronic diseases such as gastrointestinal disorders and urological conditions, which necessitate advanced diagnostic tools. Increasing patient preference for minimally invasive procedures also accelerates adoption, as video endoscopy reduces recovery time and improves clinical outcomes. Technological advancements, including high-definition imaging and AI integration for enhanced detection accuracy, expand the clinical applications and improve physician confidence. Additionally, expanding healthcare infrastructure in emerging economies and government initiatives to improve diagnostic capabilities contribute to market expansion. The development of single-use endoscopes addresses infection control concerns, further driving market demand. Investments in healthcare digitization and interoperability with hospital information systems also enhance operational efficiencies, fostering continued growth. Strategic collaborations among market players to innovate and expand geographic reach underpin the positive growth trajectory anticipated through 2034.

Market Trends

Emerging trends include the adoption of single-use disposable endoscopes to mitigate cross-contamination risks, reflecting heightened awareness of hospital-acquired infections. Integration of artificial intelligence and machine learning algorithms enhances image analysis, enabling early disease detection and improved diagnostic precision. Portable and wireless endoscopy systems are gaining popularity, improving accessibility in outpatient and remote settings. Furthermore, manufacturers are focusing on developing ultra-high-definition 4K imaging technologies to provide superior visualization. There is also an increasing trend towards cloud-based storage and tele-endoscopy services to facilitate remote diagnostics and collaboration among healthcare professionals, driving digital transformation within the market.

Market Opportunities

Significant opportunities exist in emerging markets where increasing healthcare expenditure and expanding medical infrastructure create demand for advanced diagnostic devices. The rising prevalence of lifestyle-related diseases in Asia-Pacific and Latin America offers large patient pools for video endoscopy applications. Innovations in single-use and portable endoscopy systems provide avenues for market penetration in outpatient clinics and ambulatory surgical centers. Additionally, integration with AI and data analytics presents opportunities to develop value-added services such as predictive diagnostics and personalized treatment planning. Collaborations with healthcare providers and technology firms can accelerate product development and market access. Regulatory relaxations and government incentives for medical device adoption further support market expansion, making these regions highly attractive for investment and growth.

Market Challenges

High costs associated with advanced video endoscopy systems and their maintenance limit accessibility in price-sensitive markets, restricting market penetration. Stringent regulatory frameworks across different regions increase time-to-market and compliance costs for manufacturers, posing significant barriers. Technical challenges such as device fragility, need for specialized training, and risk of equipment malfunction affect clinician adoption rates. Additionally, the presence of counterfeit products and lack of standardized protocols can undermine market trust. Supply chain disruptions, especially in critical components like optics and sensors, also impact product availability. Furthermore, competition from alternative diagnostic technologies such as capsule endoscopy and non-invasive imaging can constrain market growth, necessitating continuous innovation to maintain relevance.

Regulatory Framework

Between 2020 and 2025, regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) implemented stricter guidelines for video endoscopy devices focusing on safety, efficacy, and post-market surveillance. Compliance with ISO 13485 standards for medical device quality management became mandatory, impacting manufacturing and quality assurance processes. The Medical Device Regulation (MDR) in Europe introduced enhanced requirements for clinical evaluation, traceability, and vigilance, increasing regulatory scrutiny. In Asia-Pacific, countries like Japan and China updated their medical device approval frameworks to accelerate innovation while ensuring patient safety. These regulations mandate rigorous testing, documentation, and risk management, influencing product development timelines and costs. Government initiatives promoting innovation-friendly regulatory pathways and harmonization efforts aim to streamline approvals. Additionally, guidelines on reprocessing and single-use devices address infection control challenges, shaping market offerings and supplier strategies.

Market Intelligence

- •15th January 2025, Olympus Corporation announced the launch of its next-generation 4K Ultra-HD flexible video endoscope designed for enhanced imaging clarity and ergonomic handling. The device integrates AI-powered lesion detection software, aimed at improving early diagnosis in gastroenterology. Olympus highlighted the system's compatibility with cloud-based platforms for seamless data sharing and remote consultations, targeting expansion into emerging markets with growing healthcare infrastructure. This launch is expected to strengthen Olympus’ market leadership by combining advanced technology with user-friendly design, catering to evolving clinician needs globally. Source: Olympus Press Release

- •2nd March 2025, Ambu A/S introduced its single-use flexible endoscope portfolio expansion tailored for urology and ENT applications. The new models emphasize infection control and cost-effectiveness, addressing hospital concerns about reusable device sterilization. Ambu’s disposable endoscopes feature high-definition imaging and wireless connectivity, enabling efficient procedure workflows and reducing cross-contamination risks. This strategic product extension supports Ambu’s commitment to sustainability and safety, reinforcing its position in the rapidly growing single-use endoscopy segment. The innovation is expected to accelerate adoption in hospitals and outpatient centers worldwide. Source: Ambu Official Website

- •10th May 2025, Medtronic plc completed the acquisition of a leading AI-based medical imaging startup focused on predictive analytics in endoscopy. The strategic move aims to integrate AI algorithms into Medtronic’s video endoscopy systems to enhance real-time diagnostics and personalized treatment planning. This acquisition complements Medtronic’s portfolio by leveraging machine learning to improve lesion detection accuracy and reduce procedure times. The integration is anticipated to drive innovation and competitive differentiation while expanding Medtronic’s digital health capabilities in minimally invasive therapies. The deal underscores increasing consolidation trends in the endoscopy market focused on technology convergence. Source: Medtronic Corporate Announcement

- •20th July 2024, Fujifilm Holdings Corporation launched a portable video endoscopy system optimized for outpatient and remote clinical settings. The compact device offers wireless connectivity, high-definition imaging, and cloud integration for telemedicine applications. Fujifilm emphasized ease of use, rapid deployment, and cost-effectiveness to address the growing demand for accessible diagnostic tools outside traditional hospital environments. The system supports various specialty areas including gastroenterology and ENT, enabling broader market reach. This innovation aligns with trends favoring decentralized healthcare delivery and digital transformation in medical diagnostics. Source: Fujifilm Company News

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 11.6 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Scope of Report | Market is segmented by Type (Flexible Endoscopes, Rigid Endoscopes, Capsule Endoscopes, Single-Use Endoscopes, Video Endoscopes), Application (Gastroenterology, Urology, Gynecology, ENT (Ear, Nose, Throat), General Surgery), Service Type (Installation & Maintenance, Training & Support, Software & Integration Services, Consulting Services), Deployment Model (On-Premise Systems, Cloud-Based Solutions, Hybrid Deployment) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Olympus Corporation (Japan), Boston Scientific Corporation (United States), Medtronic plc (Ireland), Fujifilm Holdings Corporation (Japan), Stryker Corporation (United States) |

Global Video Endoscopy System Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.