Middle East Big Data in Automotive Market - Outlook 2025-2034

Middle East Big Data in Automotive Market is segmented by Product Type (Hardware (Onboard Sensors and Telematics Devices), Software (Vehicle Management and Analytics Software), Services (Consulting, Maintenance, and Support Services), Connectivity Solutions (5G, IoT Network Infrastructure), Data Analytics Platforms (Cloud-Based Big Data Analytics Tools)), Application (Vehicle Telematics, Predictive Maintenance, Fleet Management, Customer Analytics, Supply Chain Optimization), Deployment Model (Cloud-Based, On-Premise, Hybrid), End User (Automotive OEMs, Fleet Operators, Government Agencies, Aftermarket Service Providers), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

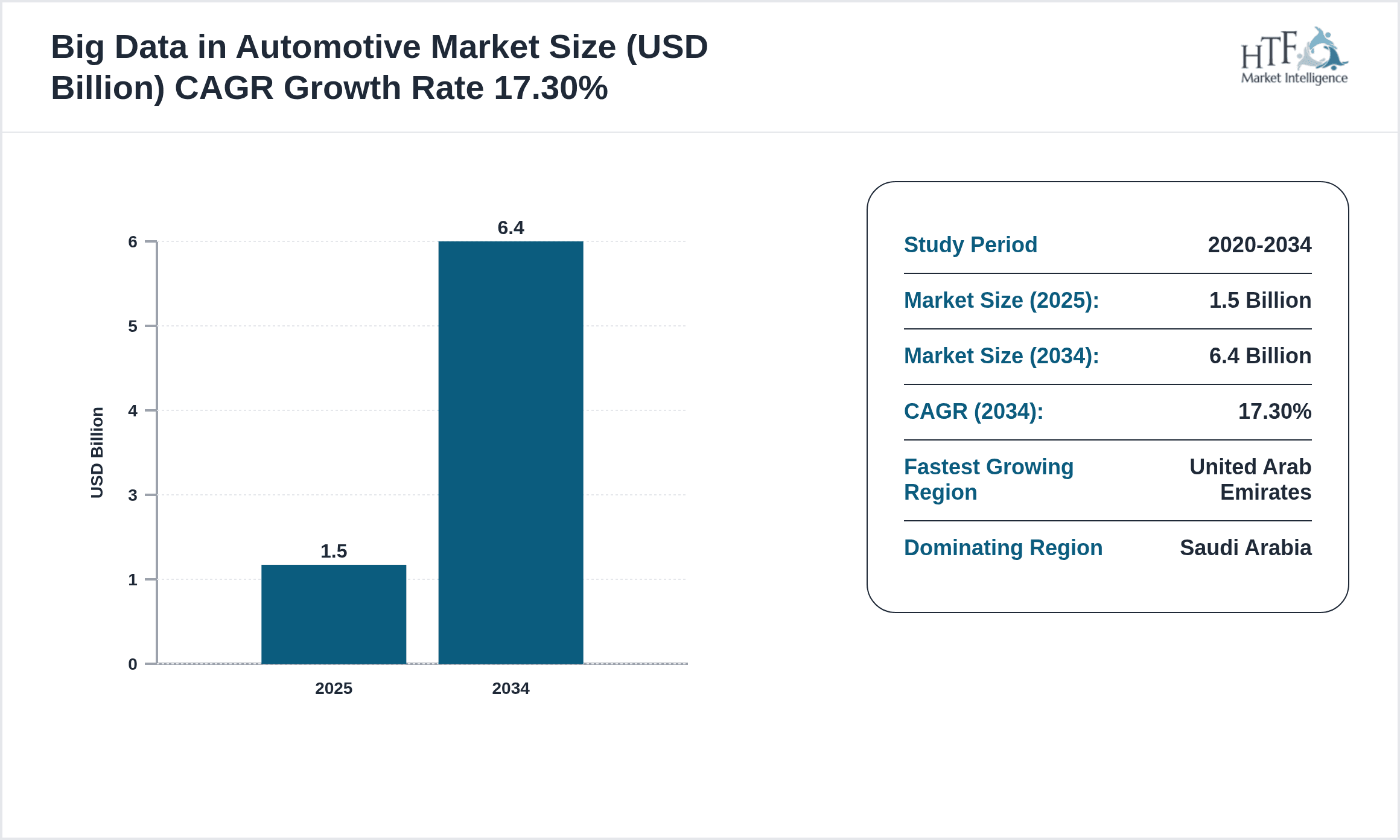

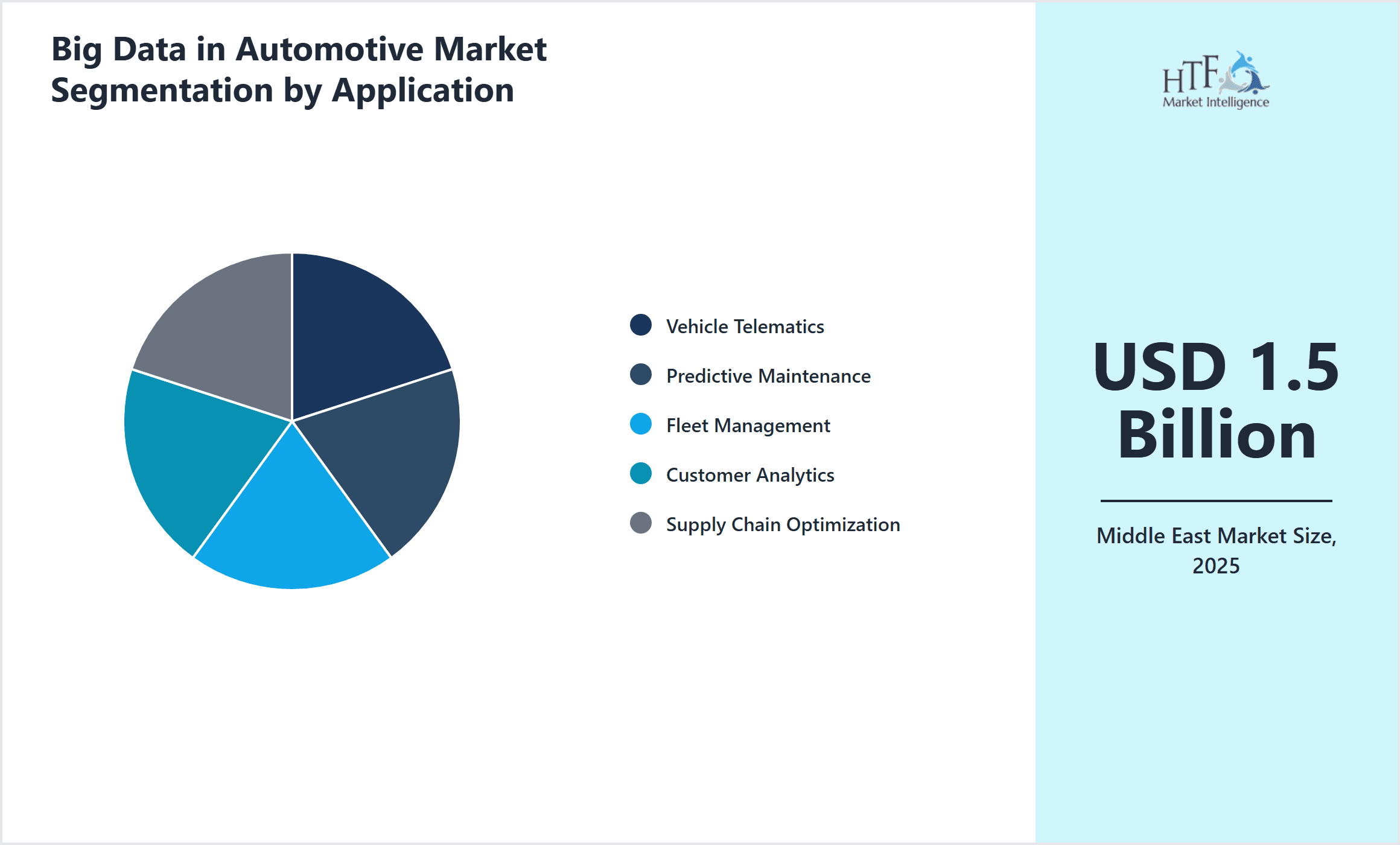

- •The Middle East Big Data in Automotive Market is a dynamic sector that integrates cutting-edge data analytics, software, hardware, and connectivity solutions to transform the automotive landscape across the region. This market focuses on leveraging extensive data generated by connected vehicles, telematics systems, and IoT-enabled infrastructure to improve vehicle safety, enhance predictive maintenance, optimize fleet operations, and deliver personalized customer experiences. Key applications include vehicle telematics, fleet management, customer analytics, and supply chain optimization, supported by a robust ecosystem of hardware devices, software platforms, and service providers. The market is driven by increasing adoption of connected vehicles, government initiatives promoting smart transportation, and growing investments in cloud and AI technologies. The region’s automotive industry is experiencing rapid digital transformation, with Saudi Arabia and the UAE leading adoption due to infrastructural capabilities and regulatory support. The market size is projected to grow from USD 1.5 billion in 2025 to USD 6.4 billion by 2034, at a CAGR of 17.3%, reflecting strong demand for big data-driven automotive solutions that enable greater operational efficiency, safety, and innovation across the Middle East’s automotive ecosystem.

- •Market highlights include the dominance of software solutions as the leading product type, accounting for the largest market share due to the increasing integration of AI and machine learning in automotive analytics. Data analytics platforms are identified as the fastest-growing segment, driven by rising demand for real-time insights and advanced predictive capabilities. Regionally, Saudi Arabia holds the largest market share, attributed to robust infrastructure development and government smart city initiatives, while the United Arab Emirates is the fastest-growing market owing to its high digital penetration and investment in autonomous vehicle technologies. The market growth is supported by advancements in connectivity solutions and increasing fleet digitization across commercial and public transport sectors. These factors collectively contribute to the expanding scope and scale of big data applications in the Middle East automotive industry through 2034.

- •The strategic importance of the Middle East Big Data in Automotive Market lies in its ability to revolutionize vehicle management, enhance safety protocols, and enable predictive maintenance, thereby reducing downtime and operational costs for stakeholders. For automakers and fleet operators, big data analytics provide actionable intelligence to optimize vehicle performance and customer satisfaction. Governments benefit through improved traffic management and compliance with environmental standards. Investors and technology providers find significant opportunities to innovate and capture emerging market segments, fueled by regulatory support and infrastructural advancements. As the region embraces smart mobility and digital transformation, the big data automotive market is positioned as a key enabler of sustainable, efficient, and intelligent transportation systems, making it an essential focus for industry participants and policymakers alike.

Competitive Landscape

The competitive environment in the Middle East Big Data in Automotive Market is characterized by intense rivalry among global technology providers, automotive OEMs, and emerging regional startups focused on big data analytics and IoT integration. Market leaders employ a mix of innovation-centric strategies, including continuous R&D investments in AI-driven analytics, strategic partnerships with telecom operators for enhanced connectivity, and collaborations with local governments to align with smart city initiatives. Competitive positioning often hinges on the ability to offer scalable, cloud-based platforms that support real-time vehicle data processing and predictive maintenance services. Pricing strategies vary with service bundling and customization to meet diverse client requirements across passenger and commercial vehicle segments. Distribution channels leverage digital platforms and regional offices to enhance customer engagement. Market entry barriers include high capital investment, stringent regulatory compliance, and the need for advanced technological capabilities. Future competition is expected to intensify with increased regional digital infrastructure and growing demand for autonomous vehicle data solutions, driving innovation and consolidation trends.

Key Participants in Big Data in Automotive Market

- •IBM Corporation (United States)

- •Microsoft Corporation (United States)

- •SAP SE (Germany)

- •Oracle Corporation (United States)

- •Bosch Automotive Service Solutions (Germany)

- •Siemens AG (Germany)

- •Cisco Systems, Inc. (United States)

- •PTC Inc. (United States)

- •Teradata Corporation (United States)

- •Hitachi Vantara Corporation (Japan)

- •Tata Consultancy Services (India)

- •HARMAN International (United States)

- •NVIDIA Corporation (United States)

- •Honeywell International Inc. (United States)

- •Infosys Limited (India)

- •Accenture plc (Ireland)

- •Dell Technologies Inc. (United States)

- •Capgemini SE (France)

- •Fujitsu Limited (Japan)

- •General Electric Company (United States)

- •Alphabet Inc. (United States)

- •SAP Ariba (Germany)

- •Cognizant Technology Solutions (United States)

- •Wipro Limited (India)

- •Ericsson AB (Sweden)

Market Breakdown

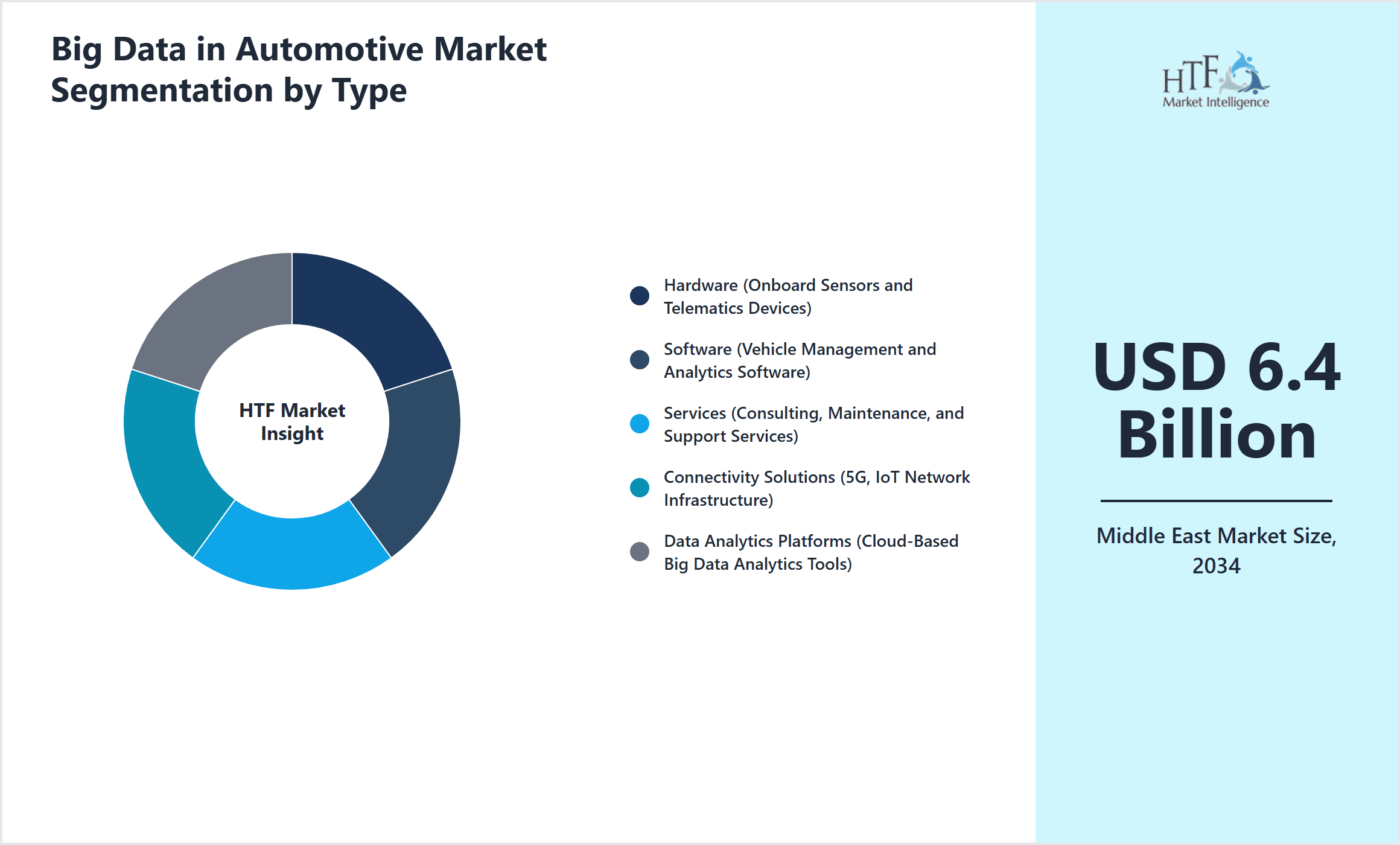

- •By Product Type

- ◦Hardware (Onboard Sensors and Telematics Devices)

- ◦Software (Vehicle Management and Analytics Software)

- ◦Services (Consulting, Maintenance, and Support Services)

- ◦Connectivity Solutions (5G, IoT Network Infrastructure)

- ◦Data Analytics Platforms (Cloud-Based Big Data Analytics Tools)

- •By Application

- ◦Vehicle Telematics

- ◦Predictive Maintenance

- ◦Fleet Management

- ◦Customer Analytics

- ◦Supply Chain Optimization

- •By Deployment Model

- ◦Cloud-Based

- ◦On-Premise

- ◦Hybrid

- •By End User

- ◦Automotive OEMs

- ◦Fleet Operators

- ◦Government Agencies

- ◦Aftermarket Service Providers

Growth Dynamics

- •The Middle East Big Data in Automotive Market growth is primarily driven by increasing vehicle connectivity and digital transformation initiatives across the region’s automotive sector. Governments in Saudi Arabia and UAE are actively promoting smart city projects integrating intelligent transportation systems, which heavily rely on big data analytics for efficient traffic management and safety enhancement. Additionally, rising investments in IoT infrastructure and 5G network deployments provide the backbone for real-time data exchange, enabling advanced vehicle telematics and predictive maintenance. The growing commercial fleet sector, especially logistics and ride-sharing services, demands sophisticated fleet management solutions to optimize operations and reduce costs. The proliferation of data-driven customer analytics also fuels adoption, helping automakers and service providers tailor offerings to regional consumer preferences. These factors collectively propel the market forward, fostering innovation and expanding application areas within the Middle East automotive ecosystem.

- •Emerging trends include the integration of artificial intelligence and machine learning algorithms with big data platforms to enhance predictive analytics accuracy and automate decision-making processes in vehicle maintenance and fleet operations. Increasing adoption of cloud-based big data platforms allows for scalable storage and processing of massive automotive datasets, facilitating advanced analytics and remote monitoring. The rise of connected and autonomous vehicles is accelerating demand for sophisticated data analytics solutions capable of processing sensor and telematics data in real-time. Furthermore, regional players are investing in cybersecurity frameworks to safeguard automotive data, reflecting growing awareness about data privacy and protection. Collaborative partnerships between automotive OEMs, telecom providers, and technology firms are becoming prevalent, driving innovation and expanding big data capabilities across the Middle East market.

- •Market restraints include challenges related to data privacy regulations and lack of standardized frameworks for data sharing among stakeholders, which can hinder seamless big data integration. The high initial costs associated with deploying advanced hardware and software platforms, combined with limited IT infrastructure in certain Middle East countries, act as barriers to widespread adoption. Additionally, concerns over cybersecurity threats targeting connected vehicles and networks create hesitancy among fleet operators and consumers. Limited availability of skilled data scientists and analytics professionals in the region further restricts the development and deployment of sophisticated big data solutions. The fragmented automotive market with diverse regulatory environments across Middle Eastern countries complicates cross-border implementation of unified data strategies, impacting market scalability.

- •Market opportunities arise from expanding smart transportation initiatives and infrastructure developments across the Middle East, especially within Saudi Arabia’s Vision 2030 and UAE’s smart city frameworks, which prioritize digital mobility solutions. The increasing penetration of electric and autonomous vehicles creates demand for real-time data analytics to monitor vehicle health and optimize energy consumption. Growing adoption of predictive maintenance solutions offers opportunities for reducing downtime and operational expenditure for fleet operators and OEMs. Additionally, development of localized data centers and cloud infrastructure enhances data sovereignty, attracting investments in big data platforms. Strategic collaborations between local governments, automotive manufacturers, and technology providers to develop region-specific solutions present avenues for innovation and market expansion.

- •Key challenges include navigating complex regulatory environments with varying data protection laws across Middle Eastern countries, which complicate data collection and sharing practices. Integration of legacy automotive systems with modern big data platforms poses technical difficulties, requiring significant customization and resources. The fragmented nature of automotive fleets, including varied vehicle types and manufacturers, leads to challenges in standardizing data formats and protocols. Limited consumer awareness about the benefits of big data analytics in vehicle safety and maintenance slows adoption rates. Furthermore, geopolitical tensions in the region may impact cross-border collaborations and technology transfer, potentially delaying market development. Addressing these challenges requires coordinated policy efforts, industry collaboration, and investment in technology standardization.

Market Trends

- •A significant trend in the Middle East Big Data in Automotive Market is the growing adoption of AI-powered analytics integrated with big data platforms, enabling more accurate vehicle condition monitoring and predictive maintenance. This technological convergence enhances operational efficiency and reduces unplanned downtime, gaining traction among fleet operators and OEMs.

- •Cloud migration of automotive data analytics platforms is gaining momentum, driven by the need for scalable, flexible solutions capable of processing large volumes of vehicle-generated data from connected and autonomous vehicles across the region’s expanding smart mobility initiatives.

- •Strategic partnerships between automotive manufacturers and telecom providers are shaping the market by enhancing connectivity infrastructure, facilitating real-time data transmission, and supporting advanced telematics applications in the Middle East.

- •The rise of electric vehicles (EVs) in the Middle East is prompting the development of specialized big data solutions to monitor battery health, charging patterns, and energy usage, contributing to sustainable automotive practices and regulatory compliance.

- •Increased focus on cybersecurity within automotive big data systems is emerging as a critical trend due to rising threats targeting connected vehicle networks, prompting investments in secure data transmission, storage, and access control mechanisms.

- •Government-led smart city projects incorporating intelligent transport systems are driving big data adoption, integrating traffic management, vehicle monitoring, and environmental analytics to optimize urban mobility and reduce congestion.

- •The market is witnessing a shift toward hybrid deployment models combining cloud and on-premise solutions, offering flexibility and enhanced data control to automotive stakeholders in the Middle East.

Market Opportunities

- •The Middle East market presents strategic opportunities in expanding big data applications for autonomous vehicle development, where real-time data analytics are essential for navigation, safety, and system optimization. Investment in this segment can position companies as early movers in a rapidly evolving automotive landscape.

- •Untapped potential exists in developing predictive maintenance solutions tailored to harsh regional climates, enabling fleet operators to minimize vehicle breakdowns and extend asset lifecycles through localized data insights and analytics.

- •Investments in local cloud infrastructure and data centers offer opportunities to address data sovereignty concerns, enhancing trust and compliance for automotive big data services within the Middle East.

- •Geographical expansion into emerging markets within the Middle East, such as Oman and Kuwait, provides growth avenues as these countries increase investment in smart transportation and connected vehicle initiatives.

- •Product development focusing on cybersecurity-enhanced big data platforms can meet rising demand for secure automotive data management, creating differentiation and competitive advantage.

- •Collaborations and strategic alliances between technology providers, automotive OEMs, and government bodies can accelerate innovation, streamline regulatory compliance, and expand market reach across the region.

- •Future market needs indicate growth in customer analytics solutions that leverage big data to improve personalized vehicle services, marketing strategies, and customer retention in the Middle East automotive sector.

Market Challenges

- •A major challenge in the Middle East Big Data in Automotive Market is the lack of unified regulations governing data privacy and protection across different countries, which complicates cross-border data exchange and integration critical for regional automotive analytics platforms.

- •Technical limitations in integrating legacy automotive systems with modern big data infrastructure result in increased complexity and costs, hindering seamless adoption especially among smaller fleet operators.

- •Companies face resource constraints due to a shortage of skilled data scientists and automotive analytics experts in the region, limiting the development and deployment of advanced big data solutions tailored to local needs.

- •Cost pressures and pricing sensitivity among fleet operators and automotive service providers restrict investments in comprehensive big data platforms, slowing market penetration.

- •Regulatory uncertainties and evolving compliance requirements create challenges for technology providers in maintaining up-to-date solutions that meet all regional legal standards.

- •Intense competition from global technology giants and local startups alike increases market saturation risk, necessitating continuous innovation and differentiation to retain market share.

- •Supply chain disruptions and infrastructural gaps in certain Middle East countries pose operational challenges in hardware deployment and maintenance services for big data automotive solutions.

Regulatory Framework

- •Between 2020 and 2025, the Middle East region has seen the implementation of data protection laws such as the UAE’s Data Protection Law (2021), which mandates stringent requirements for personal data handling and cybersecurity, impacting how automotive big data is collected and processed.

- •Saudi Arabia’s National Cybersecurity Authority established regulations in 2021 requiring compliance with cybersecurity frameworks to protect connected vehicle networks and related data systems, enhancing market trust and security standards.

- •The introduction of smart transportation policies promoting IoT and big data utilization in countries like Qatar and Kuwait between 2022 and 2024 has encouraged investments and innovation in automotive data analytics platforms.

- •Regional collaboration initiatives launched in 2023 aim to harmonize data sharing protocols across the Middle East to facilitate seamless integration of big data services in the automotive sector while safeguarding data privacy.

- •Government incentives and funding programs supporting digital transformation in transportation have been established since 2021, providing financial support and regulatory guidance to automotive big data service providers and technology developers.

Market Intelligence

- •15th February 2025, IBM Corporation launched an AI-enhanced big data analytics platform tailored for the Middle East automotive industry, integrating real-time vehicle telematics with predictive maintenance capabilities. The solution leverages cloud computing and IoT connectivity optimized for regional network infrastructure, aiming to reduce downtime for fleet operators and enhance vehicle safety. This launch positions IBM as a key innovator addressing the unique operational challenges of Middle Eastern automotive ecosystems. Source: IBM Official Press Release

- •10th April 2025, Microsoft Corporation introduced Azure-based automotive big data services with enhanced cybersecurity features specifically designed for Middle East markets. The platform supports hybrid deployment models and advanced data analytics for connected and autonomous vehicles, facilitating compliance with regional data privacy regulations. This initiative strengthens Microsoft's footprint in the automotive sector and accelerates digital transformation efforts across the Gulf Cooperation Council countries. Source: Microsoft News Center

- •5th January 2025, SAP SE announced a strategic partnership with a leading Middle Eastern telecom operator to co-develop cloud-based data analytics platforms for automotive fleet management. The collaboration focuses on leveraging 5G connectivity to enable real-time data processing and improve logistics efficiency for regional transportation companies, enhancing supply chain visibility and reducing operational costs. Source: SAP Corporate News

- •20th March 2025, Oracle Corporation completed the acquisition of a regional big data startup specializing in automotive predictive maintenance solutions. The deal is expected to expand Oracle’s product portfolio with localized analytics capabilities, addressing specific environmental and operational conditions prevalent in the Middle East automotive market. This acquisition strengthens Oracle’s competitive position and accelerates innovation in the region. Source: Oracle Investor Relations

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.5 Billion |

| Forecast Year Market Size | USD 6.4 Billion |

| CAGR | 17.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 17.3% |

| Scope of Report | Market is segmented by Product Type (Hardware (Onboard Sensors and Telematics Devices), Software (Vehicle Management and Analytics Software), Services (Consulting, Maintenance, and Support Services), Connectivity Solutions (5G, IoT Network Infrastructure), Data Analytics Platforms (Cloud-Based Big Data Analytics Tools)), Application (Vehicle Telematics, Predictive Maintenance, Fleet Management, Customer Analytics, Supply Chain Optimization), Deployment Model (Cloud-Based, On-Premise, Hybrid), End User (Automotive OEMs, Fleet Operators, Government Agencies, Aftermarket Service Providers) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | The Middle East market presents strategic opportunities in expanding big data applications for autonomous vehicle development, where real-time data analytics are essential for navigation, safety, and system optimization. Investment in this segment can position companies as early movers in a rapidly evolving automotive landscape., Untapped potential exists in developing predictive maintenance solutions tailored to harsh regional climates, enabling fleet operators to minimize vehicle breakdowns and extend asset lifecycles through localized data insights and analytics., Investments in local cloud infrastructure and data centers offer opportunities to address data sovereignty concerns, enhancing trust and compliance for automotive big data services within the Middle East., Geographical expansion into emerging markets within the Middle East, such as Oman and Kuwait, provides growth avenues as these countries increase investment in smart transportation and connected vehicle initiatives., Product development focusing on cybersecurity-enhanced big data platforms can meet rising demand for secure automotive data management, creating differentiation and competitive advantage. |

Middle East Big Data in Automotive Market - Outlook 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.