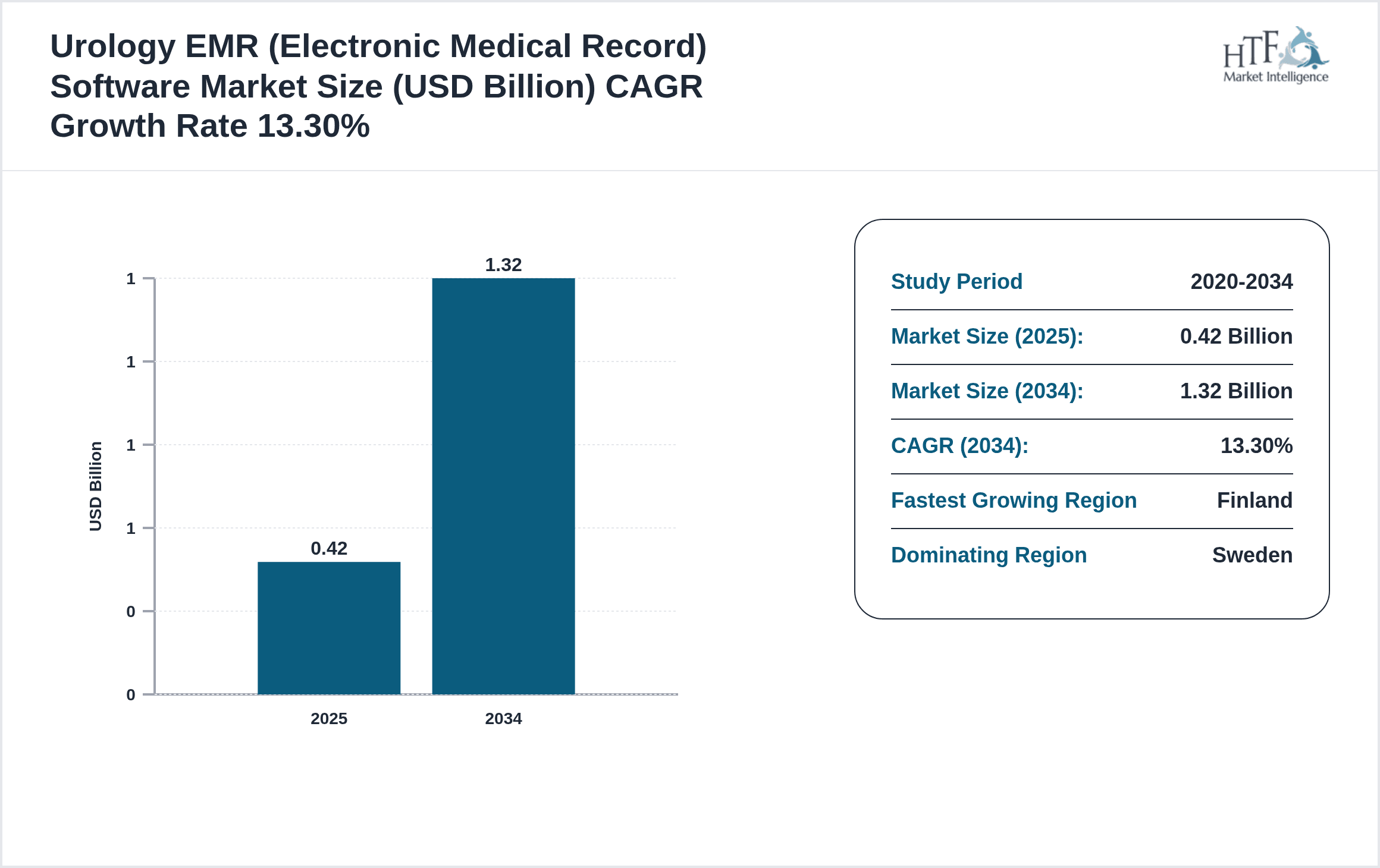

Nordic Urology EMR Software Market Size, Growth & Revenue 2025-2034

Nordic Urology EMR Software Market is segmented by Urology EMR Software Type (Cloud-based Urology EMR Software, On-premise Urology EMR Software, Hybrid Urology EMR Software, Mobile EMR Solutions, AI-Integrated Urology EMR Software), Application in Urology Healthcare (Outpatient Clinics, Hospitals, Academic & Research Institutes, Telemedicine Services, Diagnostic Centers), Service Model (Software-as-a-Service (SaaS), Implementation & Training Services, Maintenance & Support Services, Consulting Services), Deployment Model (Cloud-based Deployment, On-premise Deployment, Hybrid Deployment), and Geography (Finland, Sweden, Denmark, Norway, Iceland)

Pricing

Report Overview

Executive Summary

- •The Nordic Urology EMR Software market is a specialized segment of healthcare IT focusing on electronic medical record systems tailored for urology practices and institutions within Denmark, Finland, Iceland, Norway, and Sweden. These solutions streamline patient data management, facilitate clinical workflows, and enhance communication among urologists, nurses, and administrative staff. The market scope includes cloud-based, on-premise, hybrid, mobile, and AI-integrated EMR platforms designed to support outpatient clinics, hospitals, academic and research institutes, telemedicine providers, and diagnostic centers. Key functionalities involve patient history tracking, diagnostic imaging integration, treatment planning, and compliance with stringent Nordic healthcare data regulations. The market value chain extends from software development and customization to deployment, training, and ongoing support services. Growing healthcare digitization, telehealth adoption, and AI-driven analytics underpin the demand for advanced urology EMR systems in the Nordic region. These technologies improve clinical decision-making, operational efficiency, and patient outcomes, positioning them as essential tools for modern urology care delivery. The market is expected to witness robust growth driven by increasing investments in healthcare IT infrastructure and evolving regulatory frameworks that emphasize data security and interoperability.

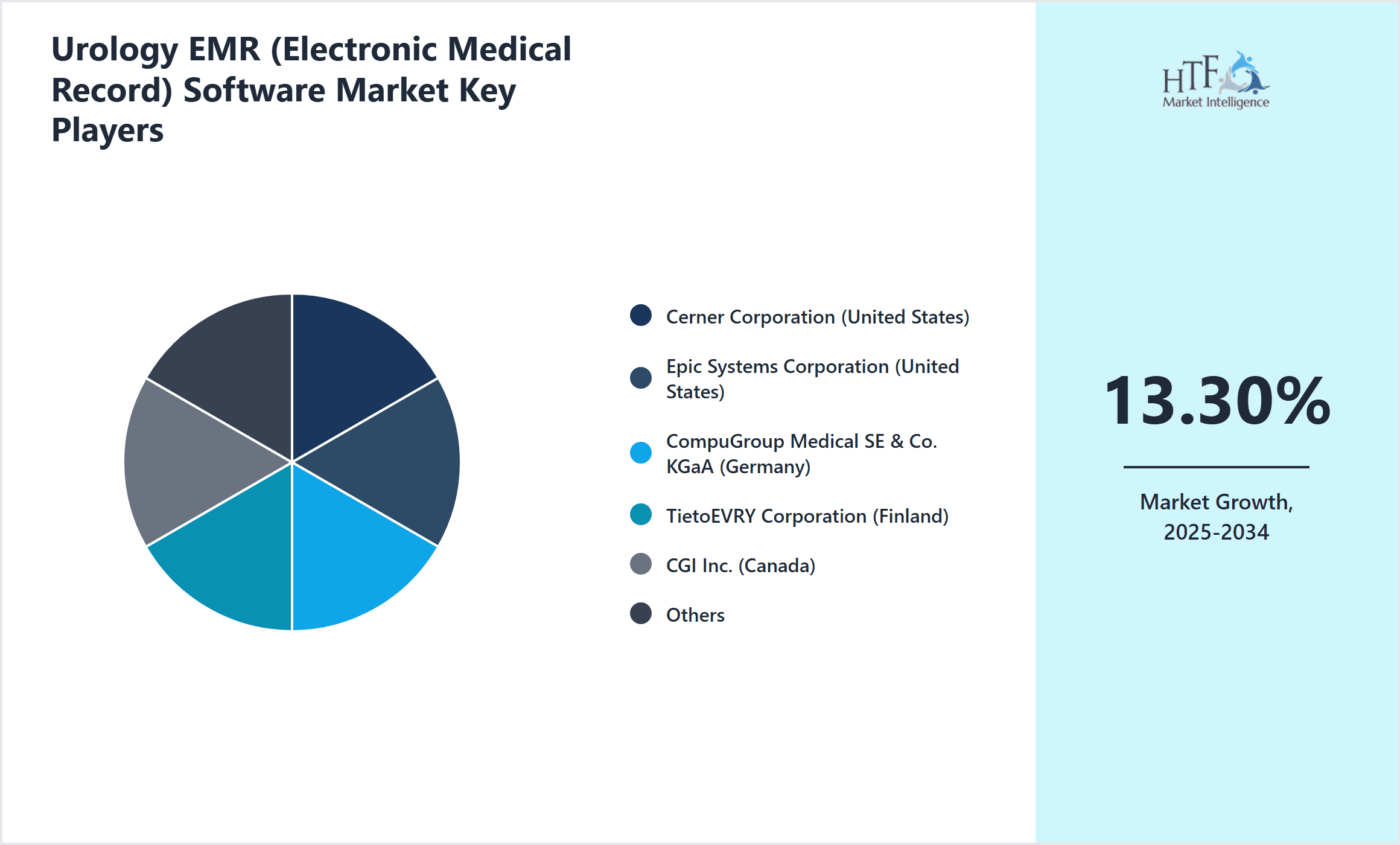

- •Key market highlights demonstrate that the Nordic Urology EMR Software market was valued at USD 0.42 Billion in 2025 and is forecasted to reach USD 1.32 Billion by 2034, registering a CAGR of 13.3%. Sweden currently dominates the market, supported by its advanced healthcare system and high technology adoption rate. Finland is identified as the fastest-growing country due to increasing investments in AI integration and telemedicine capabilities. Cloud-based EMR solutions lead the product segment, driven by scalability and cost-effectiveness, while AI-integrated EMRs are the fastest-growing type, offering enhanced clinical decision support and predictive analytics. Market growth is propelled by rising chronic urology disease prevalence, governmental digital health initiatives, and expanding telehealth services across the region.

- •The value proposition of Nordic Urology EMR Software lies in its ability to deliver seamless patient data management, improve clinical workflow efficiencies, and ensure regulatory compliance with Nordic data protection laws. These systems enable healthcare providers to enhance patient care quality, reduce administrative burdens, and foster data-driven treatment strategies. For technology vendors and healthcare stakeholders, the market presents strategic growth opportunities through innovation in AI, interoperability, and cloud technologies. Additionally, the market supports healthcare digitization goals and aligns with broader European Union healthcare policy frameworks, reinforcing its strategic importance to public and private health sectors.

Competitive Landscape

The Nordic Urology EMR Software market is characterized by a competitive environment where established global healthcare IT companies and regional specialized vendors coexist. Market players adopt diverse strategies such as technological innovation, strategic partnerships, and tailored service offerings to address the unique requirements of Nordic healthcare institutions. Key competitive factors include product customization capabilities, compliance with stringent regional and EU data privacy regulations, integration with existing healthcare IT ecosystems, and scalability of cloud-based solutions. Players actively invest in AI and machine learning to enhance clinical decision support features and predictive analytics within their EMR platforms. Mergers and acquisitions play a critical role in consolidating market presence and expanding geographic reach. Pricing strategies balance value-based offerings with cost containment pressures faced by public healthcare providers. Distribution channels leverage direct sales, partnerships with healthcare IT integrators, and collaborations with government health agencies. The competitive landscape is also influenced by the rapid evolution of telemedicine services, necessitating agile product development and robust cybersecurity measures. Future trends indicate increased focus on interoperability standards, patient-centric features, and expansion of AI applications, which will further intensify competition among market participants.

Leading Companies in Nordic Urology EMR Software Market

- •Cerner Corporation (United States)

- •Epic Systems Corporation (United States)

- •CompuGroup Medical SE & Co. KGaA (Germany)

- •TietoEVRY Corporation (Finland)

- •CGI Inc. (Canada)

- •Philips Healthcare (Netherlands)

- •Cambio Healthcare Systems AB (Sweden)

- •Systematic A/S (Denmark)

- •Sectra AB (Sweden)

- •Visma AS (Norway)

- •Nexer Group (Sweden)

- •Orion Health Group (New Zealand)

- •CGM Clinical (Germany)

- •MedApp Ltd. (Finland)

- •KRY International AB (Sweden)

- •Siemens Healthineers (Germany)

- •EVRY Healthcare (Norway)

- •InterSystems Corporation (United States)

- •Visma Enterprise (Norway)

- •Cerner Nordic (Sweden)

- •Tunstall Nordic AB (Sweden)

- •Vitec Software Group AB (Sweden)

- •Mediware Information Systems (United States)

- •Hogia Group AB (Sweden)

- •Sectra Nordic (Sweden)

Market Breakdown

- •By Urology EMR Software Type

- ◦Cloud-based Urology EMR Software

- ◦On-premise Urology EMR Software

- ◦Hybrid Urology EMR Software

- ◦Mobile EMR Solutions

- ◦AI-Integrated Urology EMR Software

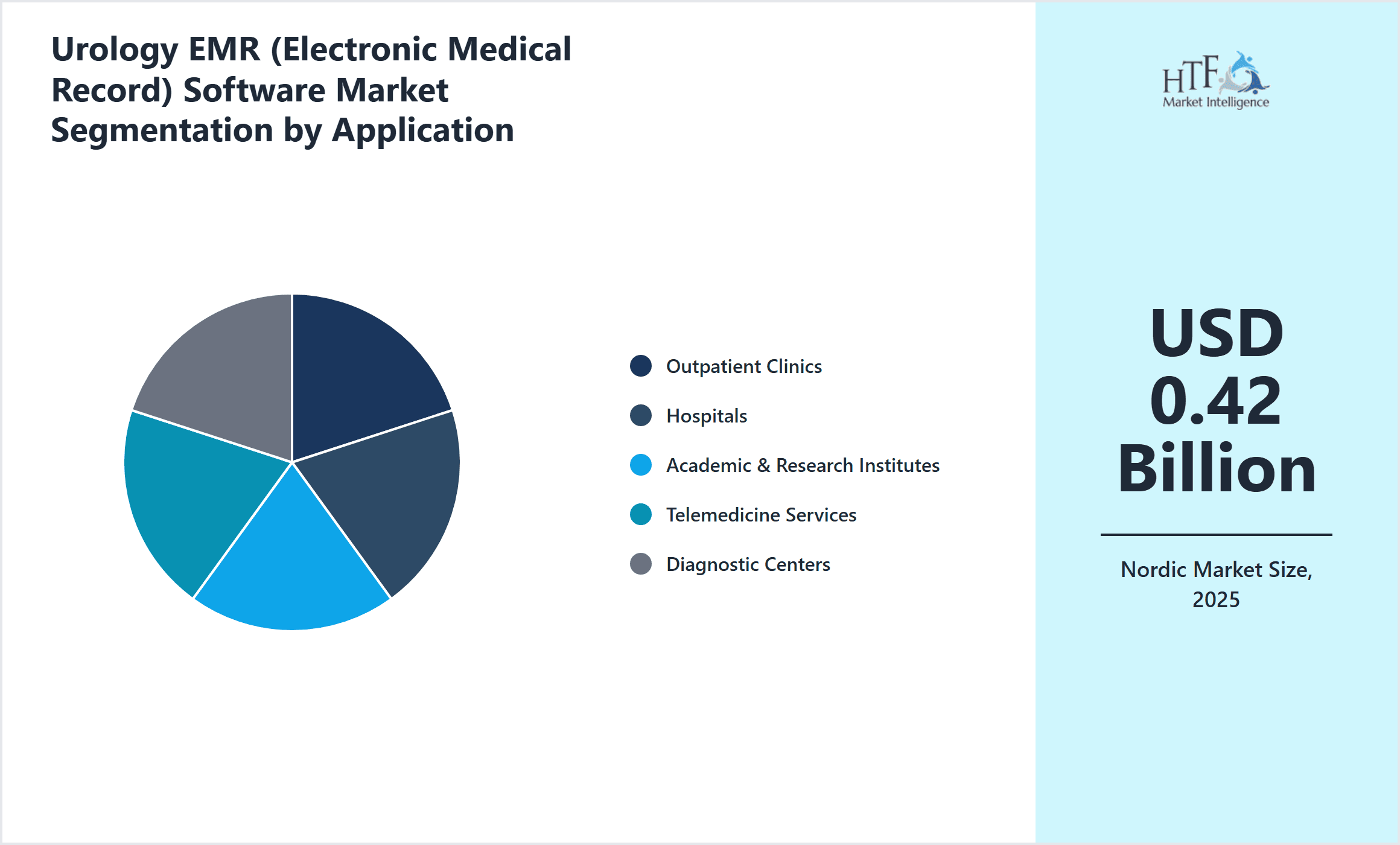

- •By Application in Urology Healthcare

- ◦Outpatient Clinics

- ◦Hospitals

- ◦Academic & Research Institutes

- ◦Telemedicine Services

- ◦Diagnostic Centers

- •By Service Model

- ◦Software-as-a-Service (SaaS)

- ◦Implementation & Training Services

- ◦Maintenance & Support Services

- ◦Consulting Services

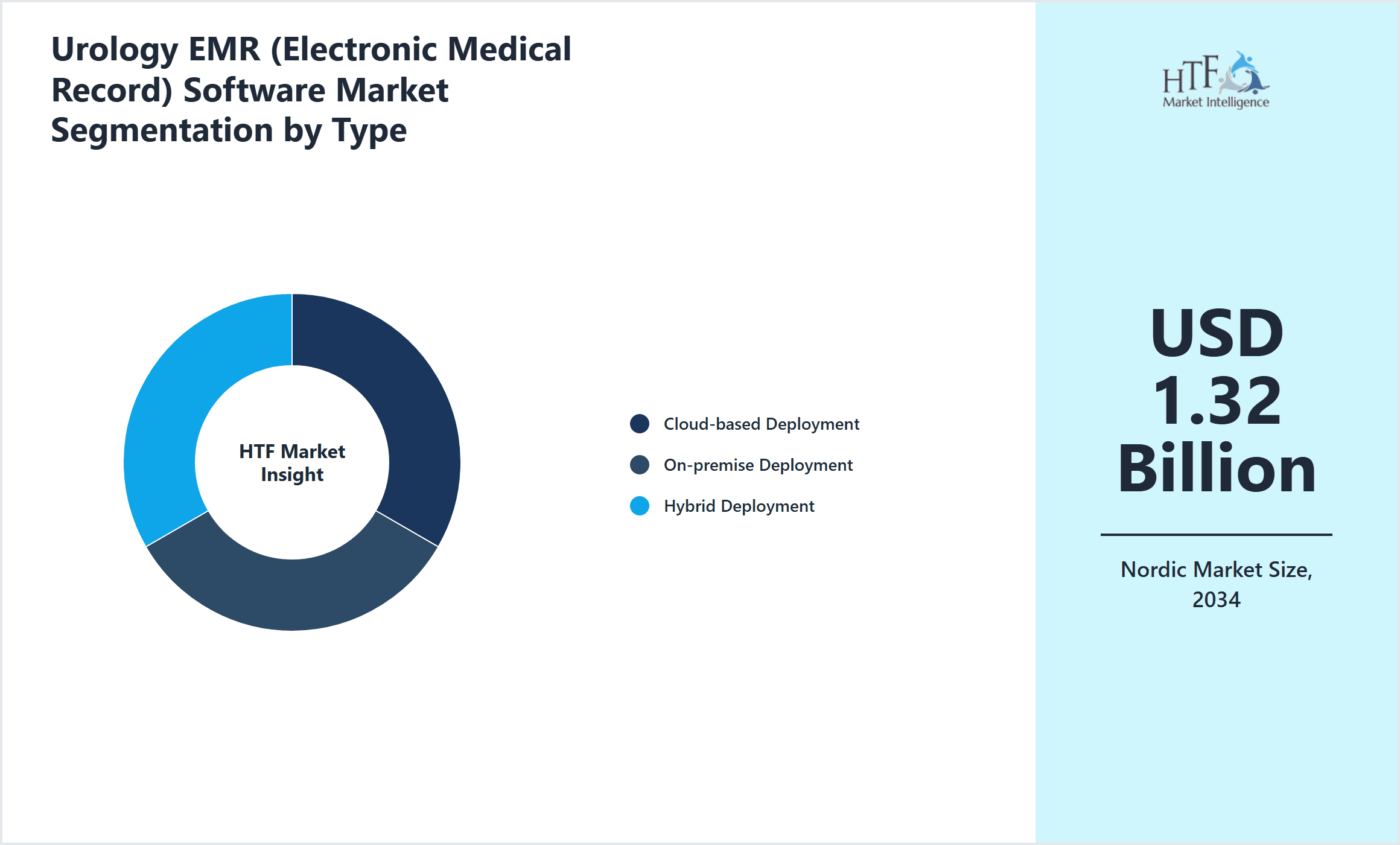

- •By Deployment Model

- ◦Cloud-based Deployment

- ◦On-premise Deployment

- ◦Hybrid Deployment

Growth Dynamics

- •Increasing prevalence of urological disorders in the Nordic population drives demand for specialized EMR software, enabling better chronic disease management and clinical outcomes.

- •Government initiatives promoting healthcare digitization and data interoperability standards in Nordic countries are accelerating adoption of advanced urology EMR platforms.

- •Integration of artificial intelligence and machine learning enhances diagnostic accuracy and predictive analytics, attracting healthcare providers to invest in AI-enabled EMR solutions.

- •The growing telemedicine trend, especially post-COVID-19, is increasing demand for mobile and cloud-based EMR systems that facilitate remote patient monitoring and virtual consultations.

- •Healthcare providers seek cost-effective, scalable EMR solutions, boosting popularity of cloud-based deployment models across Nordic hospitals and clinics.

- •Rising patient data security concerns and stringent Nordic data privacy laws are prompting vendors to enhance cybersecurity features within their EMR offerings.

- •Collaborations between software vendors and healthcare institutions foster customized EMR solutions that address local clinical workflows and regulatory requirements.

Market Trends

- •Adoption of cloud-native urology EMR platforms is increasing, driven by benefits such as cost efficiency, accessibility, and ease of updates.

- •AI and predictive analytics capabilities are being embedded into EMR systems, enabling early detection of urological conditions and personalized treatment plans.

- •Integration with telemedicine platforms supports remote diagnostics and patient follow-up, which is gaining traction in rural and underserved Nordic regions.

- •Focus on user-friendly interfaces and mobile accessibility improves clinician engagement and reduces training time for urology EMR software.

- •Interoperability initiatives are fostering seamless data exchange across hospitals, laboratories, and pharmacies, enhancing care coordination.

- •Sustainability and green IT practices are influencing vendor product development, with energy-efficient cloud data centers becoming a priority.

- •Increased patient involvement through portals and apps integrated with EMR systems is improving transparency and adherence to treatment.

Market Opportunities

- •Expansion into tele-urology services offers significant growth potential by enabling remote consultations and continuous patient monitoring.

- •Development of AI-powered diagnostic tools and clinical decision support integrated with EMR systems can enhance market differentiation and adoption.

- •Customization of EMR platforms for smaller outpatient clinics and private urology practices presents untapped market segments in the Nordic region.

- •Collaborative partnerships with government healthcare bodies can facilitate large-scale EMR deployments aligned with national digital health strategies.

- •Increasing demand for interoperability solutions creates opportunities for vendors specializing in seamless integration with diverse healthcare IT systems.

- •Emerging markets within Nordic countries, such as telemedicine and mobile health, offer avenues for innovative EMR service offerings.

- •Investment in cybersecurity features tailored for healthcare data protection can provide a competitive edge in a highly regulated environment.

Market Challenges

- •Stringent data privacy and security regulations in Nordic countries increase compliance complexity and implementation costs for EMR vendors.

- •High integration complexity with legacy hospital IT systems limits rapid deployment and seamless interoperability of new EMR solutions.

- •Resistance to change among healthcare professionals and need for extensive training can slow adoption of advanced urology EMR software.

- •Limited IT infrastructure in smaller clinics and remote areas restricts deployment of cloud-based and mobile EMR solutions.

- •Cost pressures in public healthcare budgets challenge pricing strategies and may delay procurement decisions for new software systems.

- •Rapid technological advancements require continuous product updates, posing resource challenges for smaller EMR vendors.

- •Ensuring data accuracy and minimizing clinical errors in automated AI-driven tools remains a critical concern for regulatory approval.

Regulatory Framework

- •The General Data Protection Regulation (GDPR), implemented between 2018 and 2025, mandates strict data privacy and security standards for all healthcare software operating in the Nordic region, significantly impacting EMR system design and vendor compliance strategies.

- •The Nordic Council of Ministers has introduced the Nordic eHealth Strategy, promoting interoperability and standardized electronic health records across member countries, with phased implementation from 2020 through 2025 to enhance cross-border healthcare delivery.

- •National regulations in Sweden and Finland require certification and periodic audits of healthcare IT systems, ensuring compliance with patient safety and data integrity standards, which influence EMR software validation and deployment processes.

- •The EU Medical Device Regulation (MDR) enacted in 2021 encompasses certain software functionalities within EMR platforms, necessitating conformity assessments and post-market surveillance to guarantee clinical safety and efficacy.

- •Government incentives and funding programs support digital health innovation, including EMR adoption, under frameworks like the Danish Digital Health Strategy and Norway's National Health ICT Plan, fostering vendor participation and market growth.

Market Intelligence

- •15th January 2025, TietoEVRY Corporation launched its latest AI-Integrated Urology EMR solution designed to enhance diagnostic accuracy and streamline clinical workflows specifically for Nordic healthcare providers. This cloud-based platform incorporates predictive analytics and real-time data visualization, enabling urologists to make more informed treatment decisions. The solution aims to improve patient outcomes while ensuring compliance with regional data protection regulations. TietoEVRY’s strategic focus on AI-driven healthcare IT reflects growing market demand for intelligent EMR systems across the Nordic region. The company plans to collaborate with hospitals and research institutes for pilot implementations throughout 2025. Source: TietoEVRY Official Press Release

- •22nd March 2025, Cambio Healthcare Systems AB announced a partnership with leading telemedicine provider KRY International AB to integrate its cloud-based Urology EMR software with KRY’s virtual consultation platform. This initiative aims to expand tele-urology services in Sweden and neighboring Nordic countries, facilitating remote patient monitoring and virtual care delivery. The integrated solution will enable seamless data sharing and improve accessibility for patients in rural areas. This collaboration positions both companies at the forefront of digital health innovation within the region. Source: Cambio Healthcare Systems Press Statement

- •10th May 2025, Sectra AB completed the acquisition of a smaller healthcare IT firm specializing in cybersecurity solutions tailored for EMR systems. This strategic move enhances Sectra’s cybersecurity capabilities within its Urology EMR software suite, addressing rising concerns over patient data protection in the Nordic healthcare market. The acquisition enables Sectra to offer more robust security features, including advanced encryption and threat detection, reinforcing customer confidence and compliance adherence. This consolidation reflects increasing market emphasis on data privacy and secure digital health infrastructures. Source: Sectra AB Corporate Announcement

- •8th September 2025, Visma AS introduced a new mobile EMR application targeting outpatient urology clinics across Norway. The app offers user-friendly interfaces, offline accessibility, and seamless integration with existing hospital EMR systems, supporting clinicians in both urban and remote settings. This product launch addresses growing demand for mobile health solutions and telemedicine-enabled care in the region. Visma AS aims to strengthen its position in the Nordic healthcare IT market through continuous innovation and customer-centric development. Source: Visma AS Official Website

Regional Outlook

The Sweden currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Finland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Finland

- Sweden

- Denmark

- Norway

- Iceland

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.42 Billion |

| Forecast Year Market Size | USD 1.32 Billion |

| CAGR | 13.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.6% |

| Scope of Report | Market is segmented by Urology EMR Software Type (Cloud-based Urology EMR Software, On-premise Urology EMR Software, Hybrid Urology EMR Software, Mobile EMR Solutions, AI-Integrated Urology EMR Software), Application in Urology Healthcare (Outpatient Clinics, Hospitals, Academic & Research Institutes, Telemedicine Services, Diagnostic Centers), Service Model (Software-as-a-Service (SaaS), Implementation & Training Services, Maintenance & Support Services, Consulting Services), Deployment Model (Cloud-based Deployment, On-premise Deployment, Hybrid Deployment) |

| Regions Covered | Finland, Sweden, Denmark, Norway, Iceland |

| Key Companies | Cerner Corporation (United States), Epic Systems Corporation (United States), CompuGroup Medical SE & Co. KGaA (Germany), TietoEVRY Corporation (Finland), CGI Inc. (Canada), Philips Healthcare (Netherlands), Cambio Healthcare Systems AB (Sweden), Systematic A/S (Denmark), Sectra AB (Sweden), Visma AS (Norway), Nexer Group (Sweden), Orion Health Group (New Zealand), CGM Clinical (Germany), MedApp Ltd. (Finland), KRY International AB (Sweden), Siemens Healthineers (Germany), EVRY Healthcare (Norway), InterSystems Corporation (United States), Visma Enterprise (Norway), Cerner Nordic (Sweden), Tunstall Nordic AB (Sweden), Vitec Software Group AB (Sweden), Mediware Information Systems (United States), Hogia Group AB (Sweden), Sectra Nordic (Sweden) |

Nordic Urology EMR Software Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.