North America Compostable Foodservice Packaging Market - Outlook 2024-2034

North America Compostable Foodservice Packaging Market is segmented by Compostable Foodservice Packaging Type (Biodegradable Polymers, Plant-Based Materials, Paper-Based Packaging, Starch-Based Packaging, Bagasse Packaging), Foodservice Application (Fast Food Chains, Cafeterias, Catering Services, Events & Festivals, Retail Foodservice), Distribution Channel (Direct Sales, Eco-Friendly Distributors, Online Retail, Wholesale Suppliers), End User Type (Quick Service Restaurants, Full Service Restaurants, Institutional Foodservice, Food Trucks & Mobile Vendors), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Compostable Foodservice Packaging market is a specialized segment focused on providing environmentally sustainable packaging solutions that decompose naturally, minimizing waste accumulation from the foodservice sector. This market covers a diverse range of compostable materials including biodegradable polymers, plant-based substrates, paper-based products, starch-derived packaging, and bagasse, which are increasingly replacing single-use plastics in restaurants, cafeterias, fast food chains, and catering events. These packaging products are designed to meet stringent regulatory standards for compostability while maintaining performance in protecting food quality and hygiene. The market is driven by growing consumer demand for sustainable alternatives, government regulations promoting eco-friendly packaging, and the foodservice industry's commitment to reducing its carbon footprint. Innovations in material science and composting technologies are expanding the scope and acceptance of compostable packaging, creating opportunities for manufacturers, foodservice providers, and waste management stakeholders. As the market evolves, strategic partnerships and investments are fostering product development and accelerated adoption across North America.

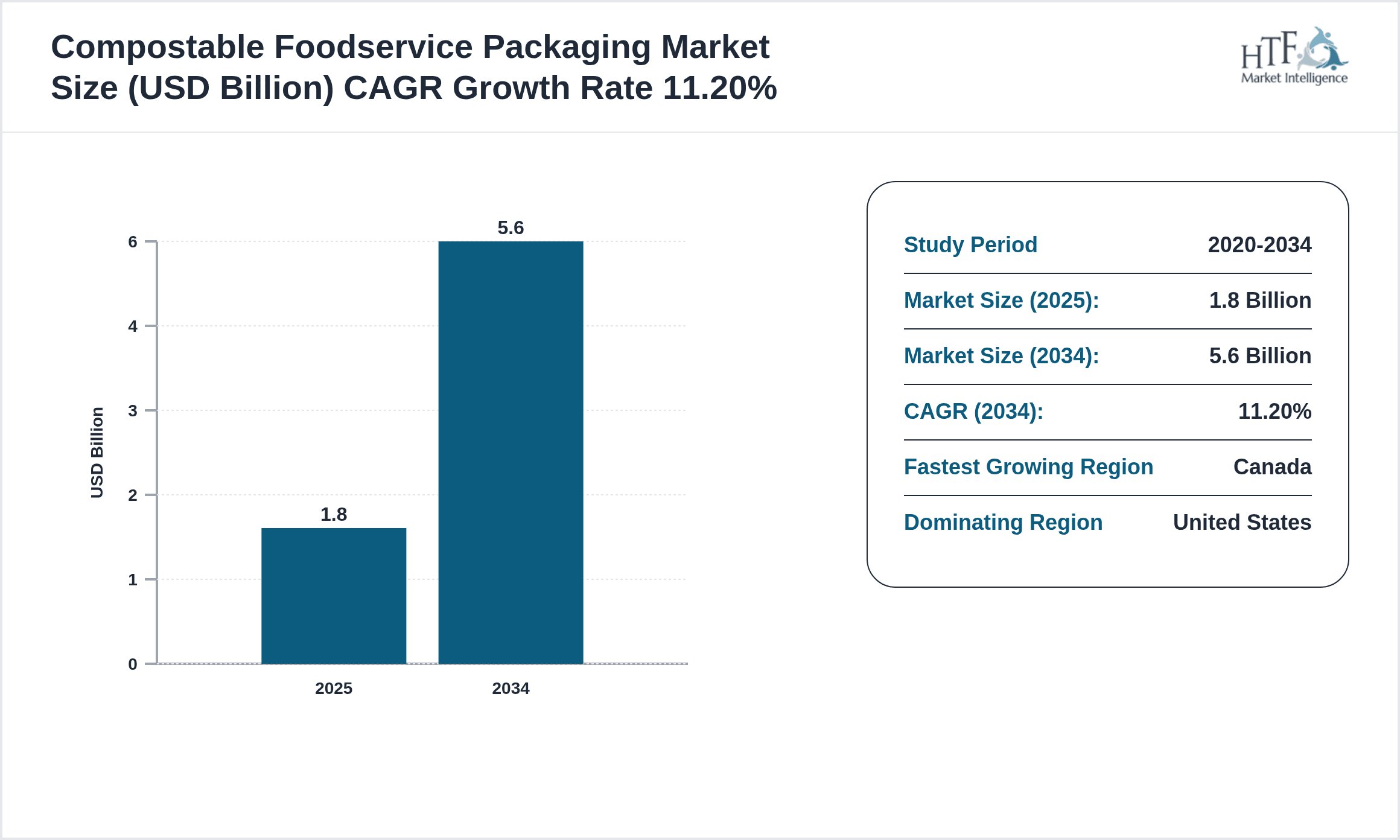

- •Key market highlights include a robust CAGR of 11.2% projected from 2024 to 2034, with the market size expected to grow from USD 1.8 Billion in 2024 to USD 5.6 Billion by 2034. Biodegradable polymers currently dominate the product type segment, while bagasse packaging is experiencing the fastest growth owing to its natural abundance and performance advantages. Fast food chains represent the largest application segment, driven by heightened consumer preference for sustainable packaging in quick-service environments. The United States holds the largest market share within North America, supported by stringent environmental policies and high consumer awareness, whereas Canada is identified as the fastest-growing regional market, propelled by progressive environmental regulations and investments in composting infrastructure.

- •This market offers significant strategic value to environmental sustainability efforts and industry stakeholders by reducing plastic waste, enhancing brand image, and meeting regulatory compliance. Foodservice businesses benefit from improved customer loyalty and alignment with global sustainability goals, while packaging manufacturers gain opportunities to innovate and expand product portfolios. Waste management firms and composting service providers also find value in the expanding volume of compostable materials requiring processing. The market’s growth underpins broader circular economy initiatives and supports the reduction of greenhouse gas emissions associated with plastic waste, positioning compostable foodservice packaging as a critical component in the transition to sustainable packaging ecosystems.

Competitive Landscape

The competitive environment in the North America Compostable Foodservice Packaging market is characterized by a mix of multinational corporations and innovative regional players striving to establish leadership through product innovation, sustainability credentials, and strategic partnerships. Companies are heavily investing in R&D to develop advanced biodegradable materials that meet evolving regulatory standards and consumer expectations. Market rivalry is intensified by the entry of new sustainable material technologies such as bagasse and starch-based alternatives, challenging traditional biodegradable polymers. Pricing strategies vary, with premium pricing justified by superior environmental benefits and certifications. Distribution channels are diversified, including direct sales to large foodservice chains and partnerships with eco-conscious distributors. Companies focus on enhancing their brand positioning by obtaining third-party compostability certifications, engaging in sustainability initiatives, and expanding production capacities. Additionally, mergers and acquisitions are shaping the competitive landscape by consolidating capabilities and expanding geographic reach. The market’s competitive dynamics underscore innovation, sustainability compliance, and customer-centric approaches as key success factors.

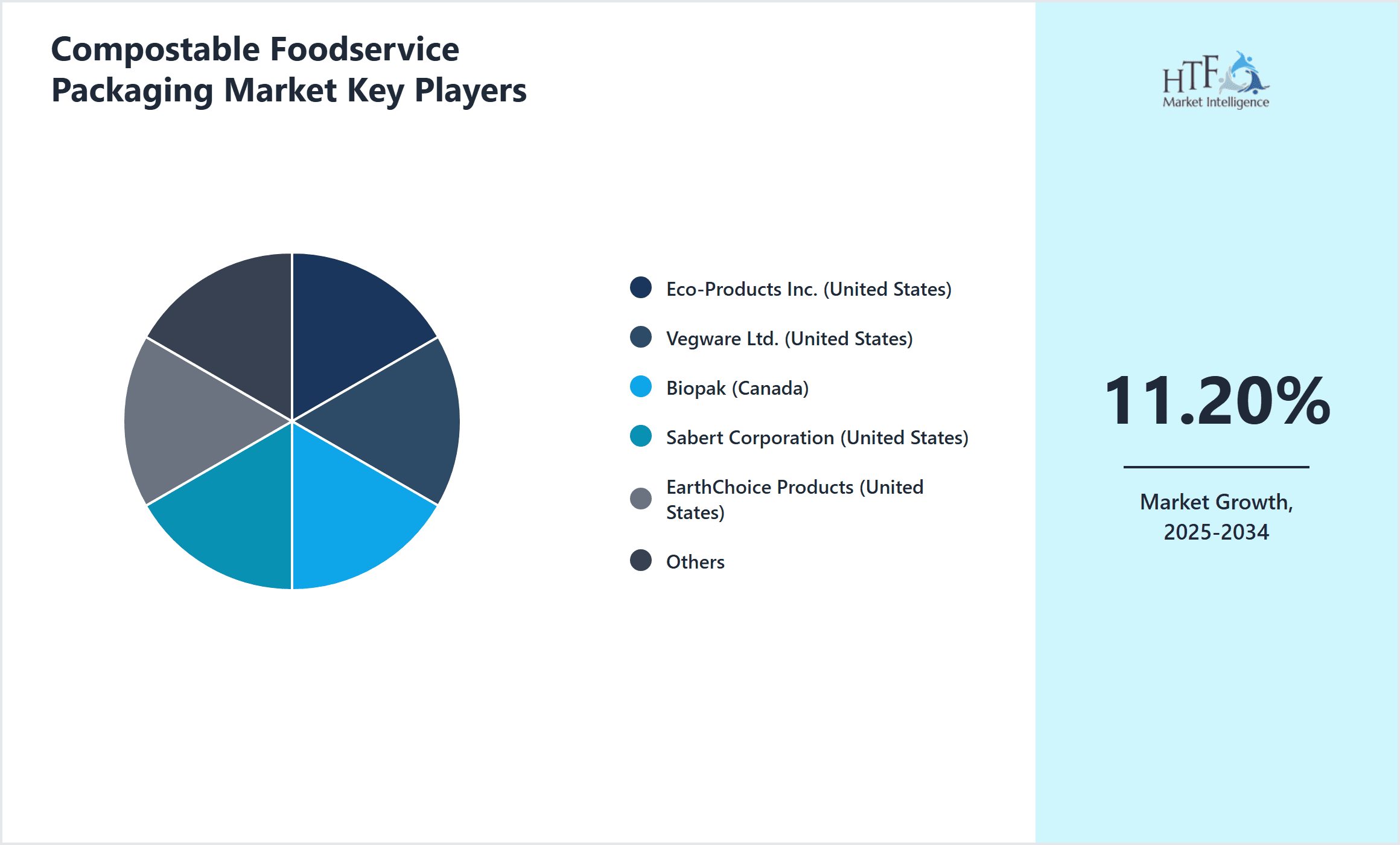

Leading Companies in Compostable Foodservice Packaging Market

- •Eco-Products Inc. (United States)

- •Vegware Ltd. (United States)

- •Biopak (Canada)

- •Sabert Corporation (United States)

- •EarthChoice Products (United States)

- •Dart Container Corporation (United States)

- •Green Paper Products (United States)

- •Genpak LLC (United States)

- •Biofase (Mexico)

- •NatureWorks LLC (United States)

- •Biopac (United States)

- •Tetra Pak (United States)

- •StalkMarket (Canada)

- •VegTrug (United States)

- •Green Paper Products (Canada)

- •Earth Friendly Products (United States)

- •Eco-Products Canada (Canada)

- •BioGreen Packaging (Mexico)

- •Greenware (United States)

- •Repurpose Compostable Products (United States)

- •BioPak USA (United States)

- •Clearpack (United States)

- •Green Packaging Group (Canada)

- •Earth Pack (United States)

- •Sustainable Packaging Industries (United States)

Market Breakdown

- •By Compostable Foodservice Packaging Type

- ◦Biodegradable Polymers

- ◦Plant-Based Materials

- ◦Paper-Based Packaging

- ◦Starch-Based Packaging

- ◦Bagasse Packaging

- •By Foodservice Application

- ◦Fast Food Chains

- ◦Cafeterias

- ◦Catering Services

- ◦Events & Festivals

- ◦Retail Foodservice

- •By Distribution Channel

- ◦Direct Sales

- ◦Eco-Friendly Distributors

- ◦Online Retail

- ◦Wholesale Suppliers

- •By End User Type

- ◦Quick Service Restaurants

- ◦Full Service Restaurants

- ◦Institutional Foodservice

- ◦Food Trucks & Mobile Vendors

Growth Dynamics

- •The North America compostable foodservice packaging market is propelled by increasing regulatory mandates aimed at reducing plastic waste and promoting sustainable alternatives. Governments across the United States, Canada, and Mexico have introduced bans and restrictions on single-use plastics, compelling foodservice providers to adopt compostable packaging solutions. Consumer awareness of environmental issues, particularly plastic pollution and carbon footprint, has surged, significantly influencing purchase decisions and encouraging brand loyalty toward eco-conscious businesses. Technological advancements in biodegradable materials have enhanced product performance, making compostable packaging more competitive with traditional plastics. Additionally, corporate sustainability initiatives and the rising popularity of green certifications are accelerating adoption among foodservice operators. Investment in composting infrastructure and waste management systems further supports market growth by improving end-of-life processing for compostable materials. Together, these factors create a favorable environment fostering rapid expansion and innovation in the compostable foodservice packaging segment.

- •Rising demand for environmentally responsible packaging in fast food chains and large-scale catering operations is a key driver for market expansion. These sectors prioritize packaging solutions that align with sustainability goals while maintaining functionality and cost-effectiveness. Increasing partnerships between packaging manufacturers and foodservice providers facilitate customized, compliant packaging offerings. The trend of zero-waste and circular economy models adopted by major foodservice chains encourages the incorporation of compostable packaging to reduce landfill waste. Furthermore, consumer preference shifts towards plant-based diets contribute indirectly by increasing demand for packaging that reflects overall sustainability values. The growing investment in research and development enhances the quality and variety of compostable products, enabling penetration into diverse foodservice applications. These growth drivers collectively underpin a positive outlook for the North America compostable foodservice packaging market.

- •The market faces challenges such as higher production costs compared to conventional plastic packaging, which may deter price-sensitive foodservice operators. Limited availability and inconsistent quality of compostable raw materials can impact product performance and scalability. Inadequate composting infrastructure in certain regions restricts effective end-of-life processing, leading to potential contamination of recycling streams and consumer confusion. Regulatory discrepancies between states and provinces create compliance complexities for manufacturers and distributors operating across North America. Additionally, consumer skepticism about the actual environmental benefits of compostable packaging, often due to lack of awareness or misinformation, poses a restraint. These factors necessitate concerted efforts in education, infrastructure development, and cost optimization to sustain market growth.

- •Emerging opportunities include the expansion of compostable packaging into niche applications such as food delivery, meal kits, and on-the-go snacks, driven by evolving consumer lifestyles. Technological innovations in raw materials, including the use of agricultural waste and novel biopolymers, present significant potential to reduce costs and improve product performance. The increasing adoption of eco-labeling and certification programs offers avenues for differentiation and enhanced consumer trust. Geographic expansion into underpenetrated areas within North America, supported by government incentives and public awareness campaigns, can accelerate market growth. Strategic collaborations between packaging companies, foodservice operators, and waste management firms facilitate closed-loop systems, enhancing sustainability impact. These opportunities position the compostable foodservice packaging market for robust future growth.

- •Competitive pressures and technological challenges remain significant hurdles, including the need to balance biodegradability with durability and food safety requirements. Market fragmentation with numerous small players complicates standardization and scalability efforts. The volatility of raw material prices, especially for plant-based and biopolymer inputs, affects profitability. Navigating complex and evolving regulatory landscapes demands continuous compliance monitoring and adaptation. Furthermore, the COVID-19 pandemic disrupted supply chains and altered foodservice consumption patterns, creating uncertainty. Overcoming consumer misconceptions and improving waste collection systems are critical challenges to maximize compostable packaging benefits. Addressing these issues requires innovation, stakeholder collaboration, and policy alignment to ensure sustainable market progression.

Market Trends

- •The North America market is witnessing a surge in the use of bagasse-based packaging, leveraging its excellent compostability and renewable nature. Leading foodservice companies are incorporating bagasse products to meet sustainability commitments while maintaining cost-effectiveness. This trend reflects a broader shift towards natural fiber-based materials as alternatives to bioplastics. Additionally, the integration of digital tracking and certifications on packaging enhances transparency and consumer confidence in compostability claims, aligning with rising demand for verified eco-friendly products.

- •Innovations in compostable coatings and barrier technologies are enabling packaging to better preserve food freshness and prevent leakage, expanding their applicability to diverse food types. These technical improvements address previous limitations that hindered wide-scale adoption in fast food and catering segments. Companies are increasingly investing in research partnerships to develop multifunctional packaging solutions that combine sustainability with superior performance.

- •The rise of zero-waste and circular economy initiatives at municipal and corporate levels is influencing procurement policies, driving foodservice operators to prioritize compostable packaging. This strategic alignment is fostering collaborations across supply chains to establish effective collection and composting systems, thus closing the loop on packaging waste. The trend is supported by growing consumer activism and regulatory pressures, making sustainable packaging a key competitive differentiator.

- •Sustainability certifications such as BPI and Compost Manufacturing Alliance are gaining prominence, with manufacturers prominently displaying these labels to validate compostability claims. This shift enhances market trust and encourages adoption among environmentally conscious consumers and businesses. The certification trend is complemented by increased regulatory scrutiny on greenwashing, promoting authentic sustainability practices.

- •E-commerce and food delivery segments are experiencing rising demand for compostable foodservice packaging due to increased online food ordering. This shift requires packaging that is not only sustainable but also durable and tamper-evident, fostering innovation in design and materials. Market players are responding with tailored solutions for delivery-friendly compostable containers and utensils.

Market Opportunities

- •The expansion of compostable packaging into institutional foodservice, including schools and hospitals, represents a significant growth opportunity. These sectors are increasingly adopting sustainability programs and require compliant packaging solutions that meet health and safety standards. Tailored product development and partnerships with institutional buyers can unlock new revenue streams.

- •Advancements in composting infrastructure, particularly in urban areas of Canada and the United States, create opportunities for higher adoption rates and reduced contamination of compostable waste streams. Public-private partnerships to enhance waste collection and processing will support market expansion and consumer confidence.

- •Integration of smart packaging technologies, such as QR codes and NFC tags, offers opportunities for engagement and education, enabling consumers to verify compostability and learn disposal instructions. This innovation can improve end-user compliance and brand differentiation.

- •Growing consumer preference for plant-based diets and sustainable lifestyles aligns with demand for eco-friendly packaging, providing opportunities for co-branding and marketing eco-conscious foodservice offerings. This synergy can drive higher sales and loyalty.

- •Geographic expansion into smaller cities and rural areas in North America, where compostable packaging penetration remains low, offers untapped potential. Educational campaigns and localized distribution partnerships can facilitate market entry and growth.

Market Challenges

- •Cost competitiveness remains a pressing challenge, as compostable foodservice packaging typically incurs higher manufacturing and raw material expenses compared to conventional plastics. This price differential can limit adoption among smaller foodservice operators and price-sensitive segments, impacting overall market penetration.

- •The lack of standardized composting infrastructure across North America creates logistical challenges, resulting in inconsistent waste processing and reduced environmental benefits. This fragmentation also confuses consumers regarding proper disposal, potentially leading to contamination of recycling and compost streams.

- •Regulatory complexity with varied guidelines and enforcement across states and provinces complicates compliance for manufacturers and distributors, increasing operational risks and costs. Navigating these discrepancies requires dedicated resources and continuous monitoring.

- •Material performance limitations, such as lower moisture resistance and durability compared to plastics, restrict the applicability of compostable packaging for certain food types and service models. Addressing these technical constraints is critical for broader acceptance.

- •Consumer misconceptions about the environmental impact of compostable packaging, often fueled by unclear labeling and misinformation, hinder market growth by reducing willingness to pay a premium or properly dispose of products. Education and transparent communication are essential to overcome this barrier.

Regulatory Framework

- •Between 2020 and 2024, several key regulations have shaped the North America compostable foodservice packaging market. The U.S. Environmental Protection Agency (EPA) and state-level agencies introduced bans on single-use plastics in multiple states, requiring foodservice providers to transition to compostable alternatives. Canada implemented the Single-Use Plastics Prohibition Regulations in 2022, mandating phase-outs of specific plastic products and encouraging compostable substitutes. Mexico has followed suit with national guidelines promoting sustainable packaging and waste reduction. These regulations emphasize compliance with ASTM D6400 and EN 13432 compostability standards, requiring manufacturers to obtain third-party certifications. The regulatory environment has accelerated product innovation and adoption while imposing challenges related to certification, labeling, and waste management infrastructure. Additionally, municipalities have introduced local ordinances supporting composting programs, further influencing market dynamics and encouraging industry-wide collaboration.

- •The enforcement mechanisms include penalties for non-compliance and incentives for businesses adopting eco-friendly packaging. Regulatory bodies actively monitor claims to prevent greenwashing, ensuring that compostable packaging meets required biodegradability and disintegration criteria. Government grants and subsidies support R&D and infrastructure development, fostering market growth. The evolving policy landscape necessitates ongoing adaptation by market participants to maintain compliance and capitalize on emerging opportunities.

- •Safety standards related to food contact materials must be adhered to, with regulations from the FDA and Health Canada governing the use of compostable packaging in direct food applications. These standards ensure consumer health while facilitating innovation in material formulations.

- •State-specific mandates, such as California’s compostable packaging requirements and New York’s single-use plastic ban, set regional benchmarks influencing national market trends. These regional policies often act as catalysts for broader regulatory adoption across North America.

- •Government initiatives promoting circular economy principles and zero-waste goals provide a supportive policy framework, aligning with global sustainability commitments. These initiatives offer strategic direction and funding opportunities that benefit the compostable foodservice packaging market.

Market Intelligence

- •15th March 2024, Eco-Products Inc. launched a new line of compostable food containers made from 100% plant-based bagasse material designed for fast food chains and catering services. These containers offer enhanced durability and moisture resistance, meeting ASTM D6400 standards. The product introduction aims to support foodservice companies in meeting stricter environmental regulations while providing consumers with sustainable packaging options. This launch strengthens Eco-Products’ position as a leader in the North American compostable packaging sector and aligns with rising demand for natural fiber-based solutions. Source: Official company press release.

- •10th November 2023, Sabert Corporation introduced innovative biodegradable polymer utensils incorporating renewable raw materials and compostable coatings. The new utensils target quick service restaurants and event caterers seeking to reduce plastic waste without compromising performance. The development involved collaboration with material scientists and environmental organizations to ensure compliance with North American composting facilities. By expanding its sustainable product portfolio, Sabert aims to capture growing market share and support industry sustainability goals. Source: Industry publication.

- •7th July 2024, Vegware Ltd. announced a strategic partnership with a leading waste management company to establish closed-loop composting programs across major U.S. cities. This initiative facilitates collection and processing of compostable foodservice packaging, addressing key infrastructure challenges and improving diversion rates. The collaboration is expected to enhance consumer confidence and accelerate market adoption by demonstrating end-to-end sustainability. Vegware’s commitment to environmental stewardship is reinforced by this move, positioning the company as a sustainability pioneer. Source: Official press release.

- •22nd January 2025, NatureWorks LLC expanded its production capacity for polylactic acid (PLA) biopolymers at its North American facility to meet increasing demand from the compostable packaging sector. The investment includes advanced manufacturing technologies to improve product consistency and reduce carbon footprint. NatureWorks’ expansion supports the growing appetite for biodegradable polymers in foodservice packaging and underpins industry-wide efforts to replace conventional plastics. This strategic move is expected to bolster supply chain resilience and foster innovation in sustainable packaging solutions. Source: Industry news.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.6 Billion |

| CAGR | 11.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.2% |

| Scope of Report | Market is segmented by Compostable Foodservice Packaging Type (Biodegradable Polymers, Plant-Based Materials, Paper-Based Packaging, Starch-Based Packaging, Bagasse Packaging), Foodservice Application (Fast Food Chains, Cafeterias, Catering Services, Events & Festivals, Retail Foodservice), Distribution Channel (Direct Sales, Eco-Friendly Distributors, Online Retail, Wholesale Suppliers), End User Type (Quick Service Restaurants, Full Service Restaurants, Institutional Foodservice, Food Trucks & Mobile Vendors) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Eco-Products Inc. (United States), Vegware Ltd. (United States), Biopak (Canada), Sabert Corporation (United States), EarthChoice Products (United States), Dart Container Corporation (United States), Green Paper Products (United States), Genpak LLC (United States), Biofase (Mexico), NatureWorks LLC (United States), Biopac (United States), Tetra Pak (United States), StalkMarket (Canada), VegTrug (United States), Green Paper Products (Canada), Earth Friendly Products (United States), Eco-Products Canada (Canada), BioGreen Packaging (Mexico), Greenware (United States), Repurpose Compostable Products (United States), BioPak USA (United States), Clearpack (United States), Green Packaging Group (Canada), Earth Pack (United States), Sustainable Packaging Industries (United States) |

North America Compostable Foodservice Packaging Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.