Global Semi-Automatic Tension Controller Market Size, Growth & Revenue 2024-2034

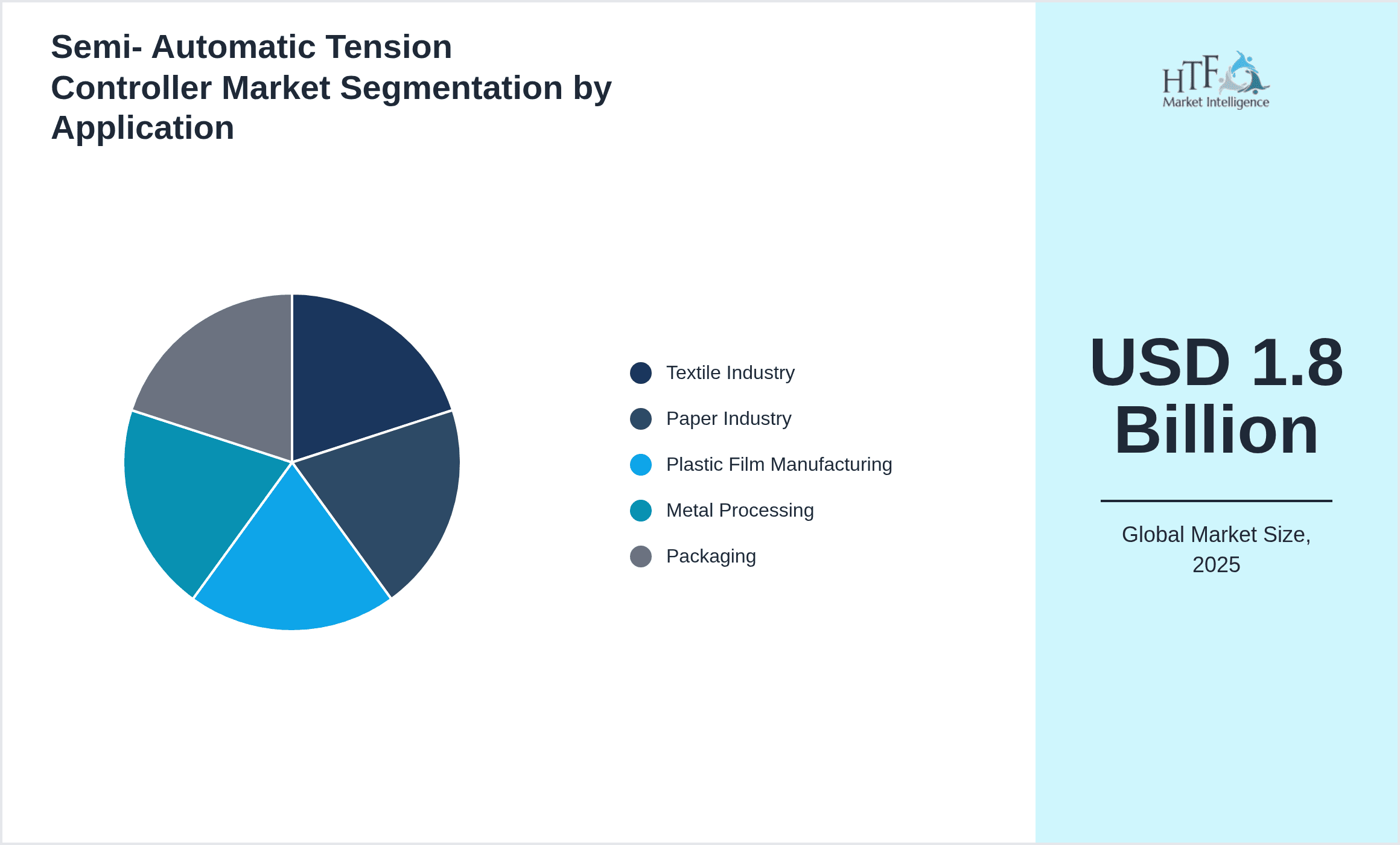

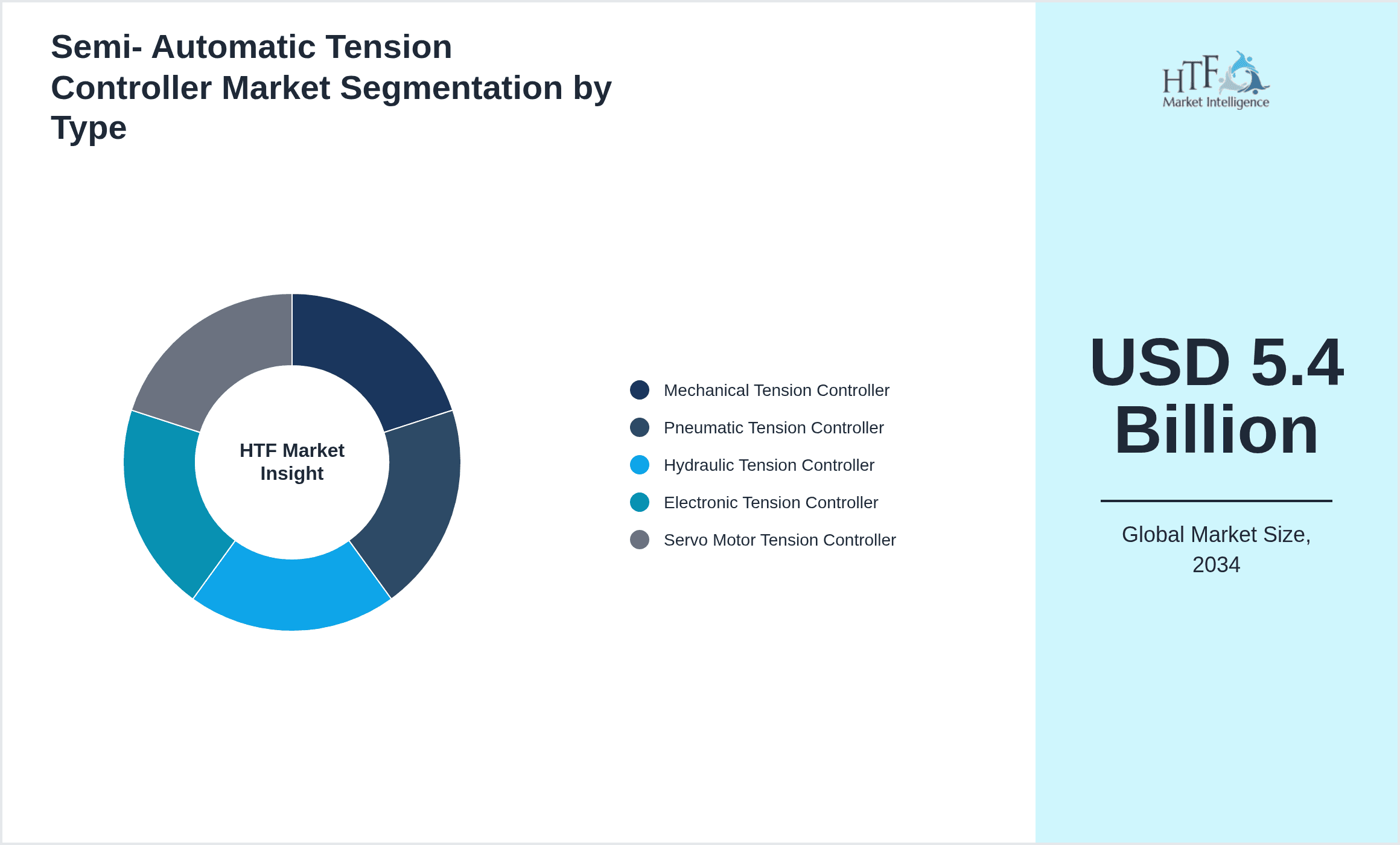

Global Semi-Automatic Tension Controller Market is segmented by Type (Mechanical Tension Controller, Pneumatic Tension Controller, Hydraulic Tension Controller, Electronic Tension Controller, Servo Motor Tension Controller), Application (Textile Industry, Paper Industry, Plastic Film Manufacturing, Metal Processing, Packaging), Industry End-Use (Automotive Manufacturing, Consumer Electronics, Construction Materials, Printing & Publishing), Deployment Model (Standalone Systems, Integrated Production Line Systems, Retrofit Solutions), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Semi-Automatic Tension Controller market is dedicated to devices that provide precise regulation of tension in continuous materials such as textiles, paper, plastic films, and metals during manufacturing. These controllers blend manual and automated tension adjustments to optimize material handling and product quality, covering a variety of technologies including mechanical, pneumatic, hydraulic, electronic, and servo motor systems. The market serves critical applications across textile production, packaging, metal processing, and paper manufacturing industries worldwide. Increasing demand for automation and enhanced process control in manufacturing has driven innovation and adoption of these controllers. The scope covers global manufacturing hubs spanning North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, highlighting regional market dynamics, competitive strategies, and growth drivers shaping the market from 2024 to 2034.

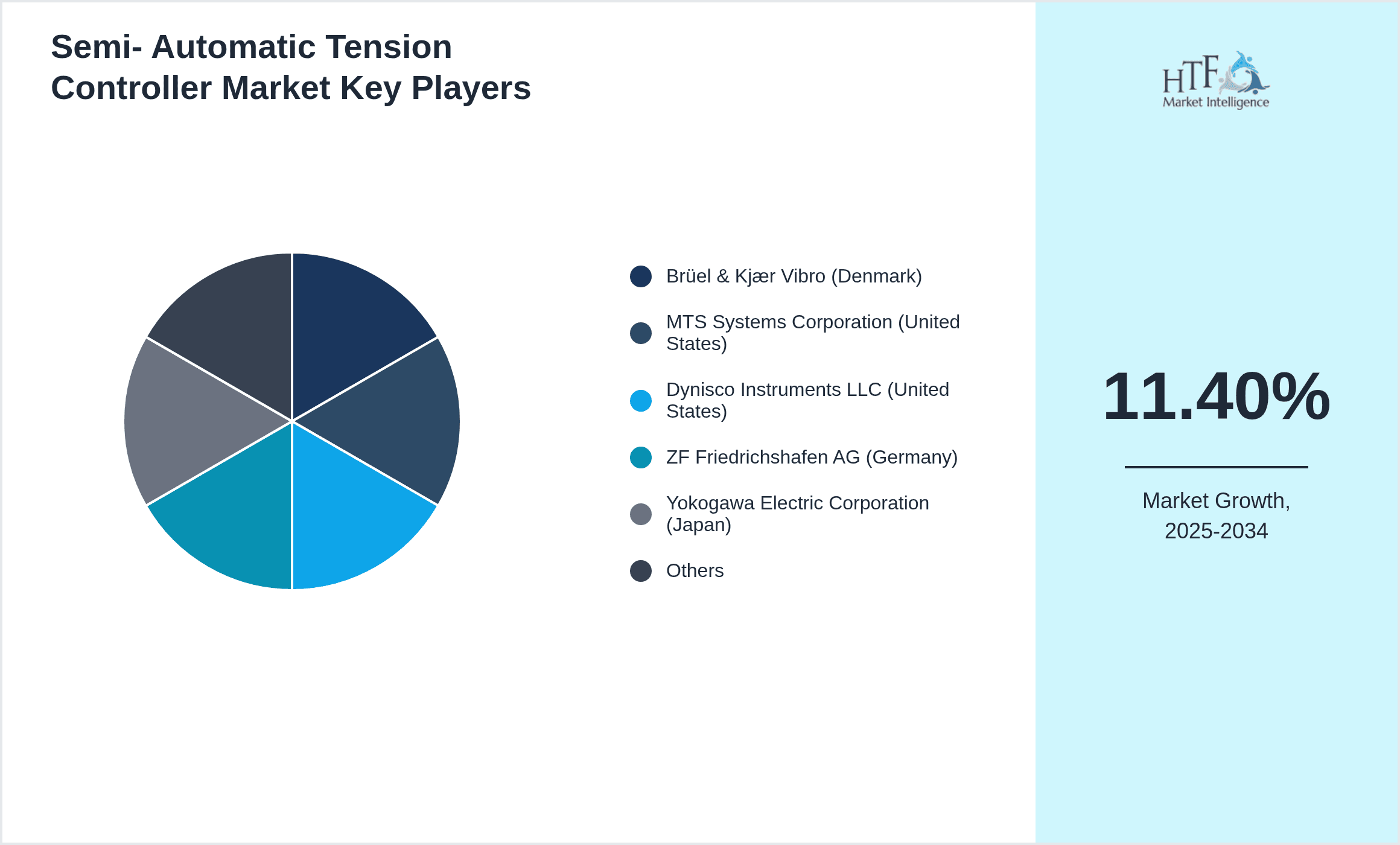

- •Key highlights reveal a robust market expansion with a projected CAGR of 11.4% from USD 1.8 billion in 2024 to USD 5.4 billion by 2034. Mechanical tension controllers currently dominate due to their reliability and cost-effectiveness, while electronic tension controllers are the fastest growing segment driven by technological advancements and increasing automation. North America leads the market share with advanced industrial infrastructure, whereas Asia-Pacific exhibits the highest growth potential fueled by expanding manufacturing sectors. The market dynamics are influenced by rising demand from textile and packaging industries, digital transformation, and increasing regulatory emphasis on product quality and waste reduction.

- •The value proposition of semi-automatic tension controllers lies in their ability to enhance manufacturing efficiency, reduce material waste, and improve product consistency across diverse industries. They offer strategic importance by balancing automation with manual control, allowing flexibility and ease of integration into existing production lines. Stakeholders including manufacturers, suppliers, and end-users benefit from advancements in sensor technology, connectivity, and user interface design. The market's growth trajectory is shaped by continuous innovation, global industrialization trends, and regulatory frameworks promoting quality standards, making it a critical component in the modern manufacturing ecosystem.

Competitive Landscape

The competitive environment in the global semi-automatic tension controller market is characterized by a mix of established multinational corporations and emerging regional players focusing on innovation, quality, and customization. Market leaders adopt strategies including technological advancement, strategic partnerships, and extensive distribution networks to maintain and expand their market positions. Innovation efforts focus on integrating IoT capabilities, enhancing user interface, and improving accuracy and responsiveness of tension control mechanisms. Competition is also fueled by pricing strategies and product differentiation through features like energy efficiency and ease of maintenance. Regional competition varies, with North America and Europe emphasizing high-end technological solutions, while Asia-Pacific focuses on cost-effective and scalable products. Mergers and acquisitions are increasingly used as strategic tools to consolidate market share and expand geographic presence, while companies continuously invest in R&D to meet evolving industry standards and customer expectations.

Prominent Players in Semi-Automatic Tension Controller Market

- •Brüel & Kjær Vibro (Denmark)

- •MTS Systems Corporation (United States)

- •Dynisco Instruments LLC (United States)

- •ZF Friedrichshafen AG (Germany)

- •Yokogawa Electric Corporation (Japan)

- •Nordson Corporation (United States)

- •Saueressig GmbH (Germany)

- •Kobayashi Pressure Gauge Mfg. Co., Ltd. (Japan)

- •Sika AG (Switzerland)

- •GAM Enterprises LLC (United States)

- •Lenzkes GmbH & Co. KG (Germany)

- •FMS Corporation (United States)

- •Meggitt PLC (United Kingdom)

- •Emerson Electric Co. (United States)

- •Omron Corporation (Japan)

- •Parker Hannifin Corporation (United States)

- •Sensotech GmbH (Germany)

- •Honeywell International Inc. (United States)

- •Schneider Electric SE (France)

- •Siemens AG (Germany)

- •Fuji Electric Co., Ltd. (Japan)

- •ABB Ltd (Switzerland)

- •Rockwell Automation, Inc. (United States)

- •E+E Elektronik GmbH (Austria)

- •Kistler Group (Switzerland)

Market Breakdown

- •By Type

- ◦Mechanical Tension Controller

- ◦Pneumatic Tension Controller

- ◦Hydraulic Tension Controller

- ◦Electronic Tension Controller

- ◦Servo Motor Tension Controller

- •By Application

- ◦Textile Industry

- ◦Paper Industry

- ◦Plastic Film Manufacturing

- ◦Metal Processing

- ◦Packaging

- •By Industry End-Use

- ◦Automotive Manufacturing

- ◦Consumer Electronics

- ◦Construction Materials

- ◦Printing & Publishing

- •By Deployment Model

- ◦Standalone Systems

- ◦Integrated Production Line Systems

- ◦Retrofit Solutions

Growth Dynamics

- •Rising demand for automation and precision control in manufacturing processes is a primary growth driver, enabling manufacturers to reduce material waste and improve product quality. For example, textile manufacturers increasingly adopt semi-automatic tension controllers to ensure consistent fabric tension, directly impacting fabric texture and durability.

- •Integration of advanced sensor technologies and IoT connectivity in tension controllers is facilitating real-time monitoring and remote control capabilities, enhancing operational efficiency across industries such as packaging and metal processing.

- •Expansion of end-use industries, particularly in Asia-Pacific, driven by rapid industrialization and rising demand for consumer goods, is stimulating higher adoption rates of semi-automatic tension controllers.

- •Regulatory emphasis on reducing production waste and improving energy efficiency is encouraging manufacturers to invest in sophisticated tension control systems that optimize resource utilization and comply with environmental standards.

- •Growing replacement demand for legacy manual tension control systems with semi-automatic and electronic variants supports market expansion, especially in developed regions with a focus on Industry 4.0 adoption.

Market Trends

- •The trend towards smart manufacturing is driving development of tension controllers with enhanced automation and machine learning capabilities, allowing predictive maintenance and adaptive tension adjustments based on material behavior.

- •Manufacturers are focusing on miniaturization and modular designs of tension controllers to facilitate easier integration into compact production lines and reduce installation costs.

- •Sustainability initiatives have led to increased demand for energy-efficient and environmentally friendly tension control systems that minimize power consumption and extend equipment lifespan.

- •Collaborations between tension controller manufacturers and industrial automation companies are becoming more prevalent to provide comprehensive solutions combining hardware and software for process optimization.

- •The rise in demand for customized tension controllers tailored to specific manufacturing requirements is fostering innovation in product design and functionality.

Market Opportunities

- •Emerging markets in Latin America and the Middle East & Africa offer significant opportunities due to increasing industrial base and investments in manufacturing infrastructure requiring modern tension control solutions.

- •Integration of AI and machine learning algorithms in tension controllers presents avenues for product differentiation and enhanced performance, catering to advanced manufacturing needs.

- •Growing focus on retrofit solutions for existing production lines creates potential for market penetration by offering cost-effective semi-automatic tension controllers that improve efficiency without full system overhaul.

- •Expansion into adjacent industries such as renewable energy manufacturing and electronics assembly can open new application segments for tension controllers.

- •Strategic partnerships with system integrators and automation suppliers can enhance market reach and accelerate adoption of advanced tension control technologies globally.

Market Challenges

- •High initial investment costs for advanced electronic tension controllers can deter adoption among small and medium-sized enterprises, limiting market penetration in some regions.

- •Technical complexities in integrating semi-automatic tension controllers with legacy manufacturing systems pose challenges related to compatibility and require specialized expertise.

- •Fluctuations in raw material prices and supply chain disruptions can impact production costs and availability of components necessary for manufacturing tension controllers.

- •Lack of standardized global regulations and certification processes for tension control equipment may result in varied quality and performance, affecting customer confidence.

- •Limited awareness and technical knowledge regarding benefits of semi-automatic tension controllers in emerging markets can slow adoption rates.

Regulatory Framework

- •Between 2019 and 2024, the implementation of international standards such as ISO 9001:2015 for quality management has mandated stricter control over manufacturing processes, directly influencing the adoption of precise tension control systems.

- •New environmental regulations introduced in North America and Europe require manufacturers to reduce waste and energy consumption, pushing the market toward energy-efficient and automated tension controllers.

- •Safety standards for industrial machinery, including ISO 12100, have been updated to ensure equipment reliability and operator safety, encouraging the integration of semi-automatic tension controllers with advanced safety features.

- •Regional mandates in Asia-Pacific countries have promoted adoption of Industry 4.0 technologies, including smart tension control solutions, to modernize manufacturing capabilities and increase global competitiveness.

- •Government incentives and subsidy programs in several regions support investments in automation and process optimization technologies, indirectly benefiting the semi-automatic tension controller market.

Market Intelligence

- •15th January 2025, Nordson Corporation launched an advanced electronic tension controller featuring IoT-enabled real-time monitoring and adaptive tension adjustment, aimed at the packaging and textile industries. This product incorporates AI algorithms to predict tension variations and optimize control, reducing material waste by up to 15%. The launch strengthens Nordson’s position in high-precision tension control solutions and responds to growing demand for smart manufacturing devices across global markets. Source: Official Nordson Corporation Press Release

- •22nd March 2025, Siemens AG introduced a modular semi-automatic tension controller system designed for seamless integration into existing production lines in the metal processing sector. The system offers enhanced user interface capabilities and energy-efficient operation, facilitating reduced downtime and maintenance costs. This innovation supports Siemens's strategic focus on Industry 4.0 solutions, enabling manufacturers to improve process accuracy and operational flexibility. Source: Siemens Corporate Announcements

- •10th February 2025, Parker Hannifin Corporation announced a strategic partnership with a leading textile machinery manufacturer to co-develop customized tension control solutions tailored to high-speed fabric production lines. This collaboration aims to combine Parker’s tension control expertise with the partner’s machinery technology to deliver enhanced product quality and operational efficiency, targeting expansion in Asia-Pacific and Latin America regions. Source: Parker Hannifin Corporate News

- •28th April 2025, Honeywell International Inc. completed the acquisition of a niche tension controller startup specializing in servo motor technology. This acquisition enables Honeywell to broaden its semi-automatic tension controller portfolio with advanced servo-driven products, supporting its growth strategy in smart automation technologies for the packaging and electronics industries. The deal is expected to accelerate product development and global market penetration. Source: Honeywell Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.4 Billion |

| CAGR | 11.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.3% |

| Scope of Report | Market is segmented by Type (Mechanical Tension Controller, Pneumatic Tension Controller, Hydraulic Tension Controller, Electronic Tension Controller, Servo Motor Tension Controller), Application (Textile Industry, Paper Industry, Plastic Film Manufacturing, Metal Processing, Packaging), Industry End-Use (Automotive Manufacturing, Consumer Electronics, Construction Materials, Printing & Publishing), Deployment Model (Standalone Systems, Integrated Production Line Systems, Retrofit Solutions) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Brüel & Kjær Vibro (Denmark), MTS Systems Corporation (United States), Dynisco Instruments LLC (United States), ZF Friedrichshafen AG (Germany), Yokogawa Electric Corporation (Japan), Nordson Corporation (United States), Saueressig GmbH (Germany), Kobayashi Pressure Gauge Mfg. Co., Ltd. (Japan), Sika AG (Switzerland), GAM Enterprises LLC (United States), Lenzkes GmbH & Co. KG (Germany), FMS Corporation (United States), Meggitt PLC (United Kingdom), Emerson Electric Co. (United States), Omron Corporation (Japan), Parker Hannifin Corporation (United States), Sensotech GmbH (Germany), Honeywell International Inc. (United States), Schneider Electric SE (France), Siemens AG (Germany), Fuji Electric Co., Ltd. (Japan), ABB Ltd (Switzerland), Rockwell Automation, Inc. (United States), E+E Elektronik GmbH (Austria), Kistler Group (Switzerland) |

Global Semi-Automatic Tension Controller Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.