United Kingdom Automotive Connecting Rod Market - Outlook 2025-2034

United Kingdom Automotive Connecting Rod Market is segmented by Material Type (Forged Steel Connecting Rods, Powder Metallurgy Connecting Rods, Cast Iron Connecting Rods, Aluminum Alloy Connecting Rods, Titanium Alloy Connecting Rods), Vehicle Application (Passenger Cars, Commercial Vehicles, Electric Vehicles, Motorsport Vehicles, Aftermarket Replacement), Manufacturing Technology (Forging, Casting, Powder Metallurgy, Machining), Distribution Channel (OEM Supply, Aftermarket Sales, Direct to Consumer, Tier-1 Supplier Networks), and Geography (England, Scotland, Wales, Northern Ireland)

Pricing

Report Overview

Executive Summary

- •The United Kingdom Automotive Connecting Rod Market is a specialized segment within the automotive components industry, focused on the design, manufacturing, and distribution of connecting rods for various vehicle types including passenger cars, commercial vehicles, electric vehicles, motorsport vehicles, and aftermarket replacements. Connecting rods are fundamental to engine mechanics, facilitating the transfer of piston motion to the crankshaft, thereby enabling engine operation and efficiency. The market is segmented by material types such as forged steel, powder metallurgy, cast iron, aluminum alloy, and titanium alloy, each selected based on performance, cost, and weight considerations. The UK market benefits from a strong automotive manufacturing ecosystem, supported by advanced engineering capabilities and stringent emission regulations that drive innovation towards lightweight and durable components. With growing demand for electric and hybrid vehicles, the market is witnessing a shift towards materials and technologies that support enhanced engine efficiency and reduced environmental impact. Key applications include OEM manufacturing and the aftermarket sector, which together sustain steady growth. The market outlook from 2025 to 2034 projects significant expansion driven by technological advancements, regulatory compliance, and evolving consumer preferences within the UK automotive industry.

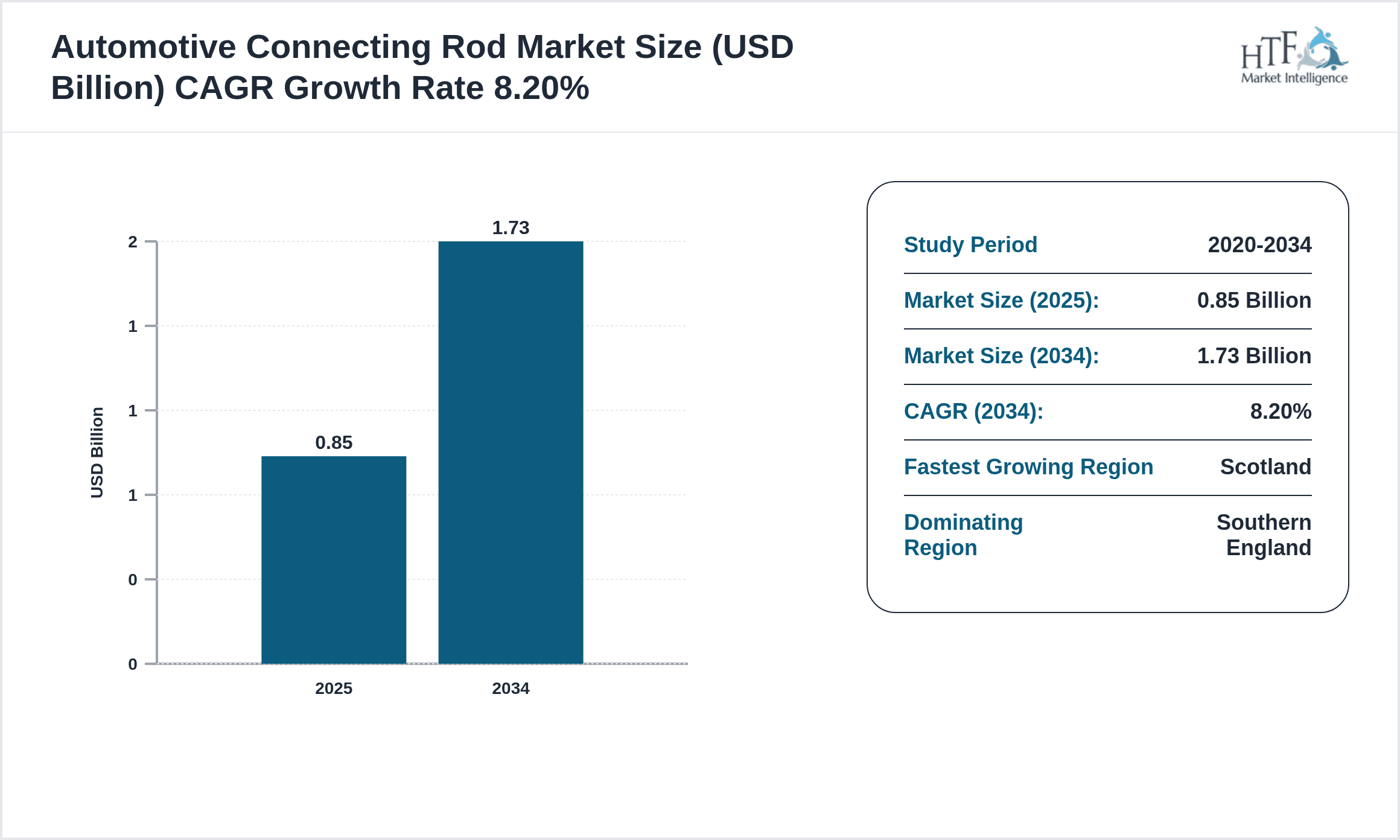

- •Market highlights reveal a base market size of USD 0.85 Billion in 2025, expected to nearly double to USD 1.73 Billion by 2034, representing a CAGR of 8.2%. Forged steel remains the dominant product type due to its superior strength and reliability, while titanium alloy rods are emerging as the fastest-growing segment, capitalizing on the trend towards lightweight, high-performance materials. Passenger cars constitute the primary application segment, followed by commercial vehicles and electric vehicles, reflecting the UK's diversified automotive demand. Regionally, Southern England dominates market share, attributable to its concentration of automotive manufacturing hubs, with Scotland experiencing the fastest growth owing to increased investments in advanced manufacturing and electric vehicle production facilities.

- •The market holds strategic importance across automotive OEMs, aftermarket players, and material technology providers. It supports the UK's ambitions in sustainable mobility and automotive innovation by offering high-quality, technologically advanced connecting rods that improve engine performance and fuel economy. Stakeholders benefit from continuous product development, regulatory support, and expanding electric vehicle adoption, making this market a critical component of the UK's automotive supply chain and industrial growth strategy. The integration of lightweight alloys and precision manufacturing techniques positions the UK as a competitive player in the global connecting rod industry, with opportunities for export and technological leadership.

Competitive Landscape

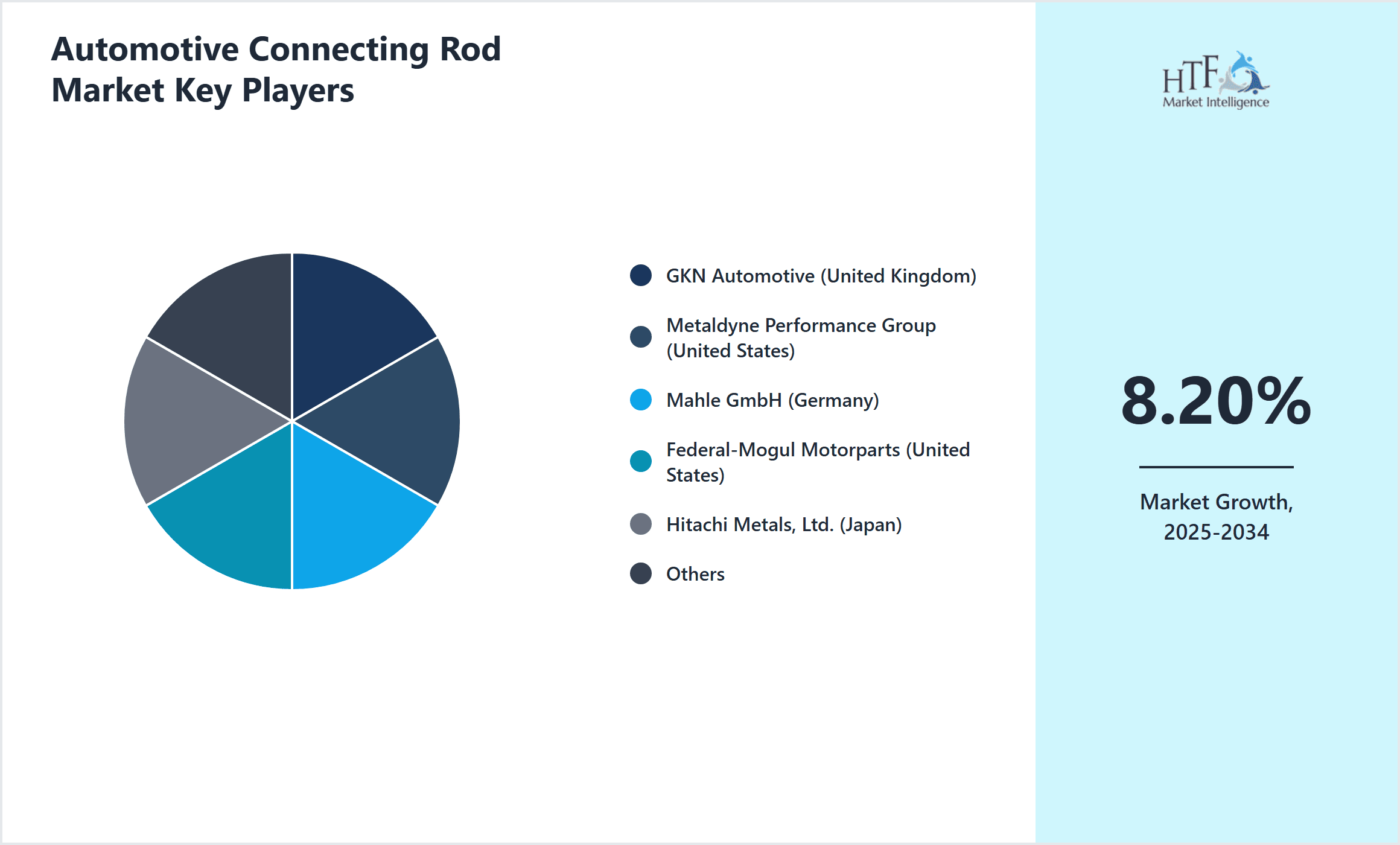

The United Kingdom Automotive Connecting Rod Market exhibits a competitive and dynamic landscape marked by a blend of established multinational corporations and specialized regional manufacturers. Competition is driven by continuous innovation in materials technology, manufacturing precision, and cost optimization. Leading players focus on developing lightweight yet robust connecting rods utilizing advanced alloys such as titanium and aluminum, catering to the growing demand for fuel-efficient and high-performance engines. Market rivalry is intensified by the presence of OEMs and aftermarket suppliers focusing on quality, reliability, and customization capabilities. Strategic partnerships, technology licensing, and process optimization are key competitive strategies to enhance market positioning. Additionally, firms invest in R&D to meet increasingly stringent UK and EU emissions regulations, which necessitate advanced engine components. The competitive environment also features mergers and acquisitions aimed at expanding product portfolios and geographic reach. Distribution channels span direct OEM contracts and aftermarket networks, with digitalization and Industry 4.0 practices influencing manufacturing efficiency and supply chain responsiveness. Overall, the market is characterized by high entry barriers due to technical expertise requirements and regulatory compliance, fostering a stable yet innovation-driven competitive setting.

Companies Shaping the Automotive Connecting Rod Market

- •GKN Automotive (United Kingdom)

- •Metaldyne Performance Group (United States)

- •Mahle GmbH (Germany)

- •Federal-Mogul Motorparts (United States)

- •Hitachi Metals, Ltd. (Japan)

- •SinterCast AB (Sweden)

- •Alcoa Corporation (United States)

- •Tupy S.A. (Brazil)

- •Nippon Piston Ring Co., Ltd. (Japan)

- •Schaeffler AG (Germany)

- •Forged Components Ltd. (United Kingdom)

- •ElringKlinger AG (Germany)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •RS Technologies, Inc. (United States)

- •Metals Industry Research & Development Center (Taiwan)

- •Timken Company (United States)

- •SGL Carbon SE (Germany)

- •Aluminum Corporation of China Limited (China)

- •NACHI-FUJIKOSHI Corp. (Japan)

- •Bharat Forge Ltd. (India)

- •Precision Castparts Corp. (United States)

- •Magna International Inc. (Canada)

- •Hitachi Automotive Systems, Ltd. (Japan)

- •Schaeffler Technologies AG & Co. KG (Germany)

- •BASF SE (Germany)

Market Breakdown

- •By Material Type

- ◦Forged Steel Connecting Rods

- ◦Powder Metallurgy Connecting Rods

- ◦Cast Iron Connecting Rods

- ◦Aluminum Alloy Connecting Rods

- ◦Titanium Alloy Connecting Rods

- •By Vehicle Application

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Motorsport Vehicles

- ◦Aftermarket Replacement

- •By Manufacturing Technology

- ◦Forging

- ◦Casting

- ◦Powder Metallurgy

- ◦Machining

- •By Distribution Channel

- ◦OEM Supply

- ◦Aftermarket Sales

- ◦Direct to Consumer

- ◦Tier-1 Supplier Networks

Growth Dynamics

- •The United Kingdom Automotive Connecting Rod Market growth is primarily driven by the increasing demand for lightweight and high-strength engine components in passenger and commercial vehicles. Manufacturers are adopting advanced materials such as titanium alloys to reduce vehicle weight and enhance fuel efficiency, responding to stricter emissions regulations. The growth of electric vehicles, while reducing dependence on traditional combustion engines, also fuels demand for specialized connecting rods in hybrid powertrains and motorsport applications. Government incentives for clean mobility and increasing automotive production capacities in regions like Southern England further stimulate market expansion. Additionally, rising aftermarket replacement demand due to vehicle aging and enhanced performance expectations contributes to sustained growth.

- •Technological innovation is a key growth driver, with manufacturers investing in advanced forging and powder metallurgy techniques to produce connecting rods with superior mechanical properties and reduced manufacturing costs. Integration of Industry 4.0 and automation in production lines improves quality control and scalability, enabling faster response to market needs. The UK’s strong automotive R&D ecosystem fosters collaborations between OEMs and material specialists to develop next-generation connecting rods tailored to evolving vehicle architectures. Moreover, the motorsport sector continues to propel innovation, creating a trickle-down effect that benefits mainstream automotive applications.

- •Consumer demand for high-performance and durable vehicles drives adoption of premium connecting rod materials like forged steel and titanium alloys. Enhanced engine designs necessitate components that withstand higher stresses and temperatures, encouraging upgrades from traditional cast iron rods. The aftermarket segment benefits from increasing vehicle parc and maintenance activities, providing steady revenue streams for connecting rod suppliers. Furthermore, environmental awareness and regulatory compliance compel automakers to optimize engine efficiency, directly impacting connecting rod design and material selection. This demand landscape contributes positively to market growth.

- •Strategic partnerships and joint ventures between UK-based manufacturers and global suppliers expand technological capabilities and product portfolios. These collaborations facilitate access to advanced materials, manufacturing technologies, and new market segments such as electric and hybrid vehicles. Investment in local manufacturing infrastructure, particularly in Northern and Scotland regions, drives regional market growth. The government’s focus on innovation funding and clean automotive technologies further catalyzes market development. Export opportunities to European and global markets also present growth potential for UK-based connecting rod producers.

- •The rise in motorsport activities within the UK contributes significantly to demand for high-performance connecting rods. Motorsport applications require lightweight, high-strength rods capable of enduring extreme operating conditions, fostering material innovation and precision manufacturing. The technology advancements and quality standards pioneered in this segment often extend to commercial automotive sectors, enhancing overall market growth. Additionally, increasing vehicle electrification encourages development of hybrid powertrain-compatible connecting rods, opening new avenues for product differentiation and revenue generation.

Market Trends

- •A prominent trend in the UK automotive connecting rod market is the shift towards lightweight materials such as titanium and aluminum alloys, driven by the need for improved fuel efficiency and lower emissions. This trend is supported by advancements in forging and powder metallurgy technologies that enable cost-effective mass production of these materials.

- •The increasing integration of electric and hybrid vehicles in the UK market is influencing connecting rod demand patterns, with a growing focus on components compatible with hybrid internal combustion engines. Manufacturers are innovating designs to cater to these evolving powertrain architectures.

- •Digitalization in manufacturing, including the adoption of Industry 4.0 technologies such as IoT sensors and AI-driven quality control, is enhancing production efficiency and product consistency. UK manufacturers are leveraging these technologies to maintain competitive advantage.

- •Sustainability initiatives are shaping raw material sourcing and production processes, with greater emphasis on recycling and environmentally friendly manufacturing methods. This trend aligns with the UK government’s broader environmental policies and consumer preferences.

- •Collaborative innovation between automotive OEMs, material suppliers, and research institutions is becoming increasingly common. Such partnerships accelerate development cycles and enable rapid commercialization of advanced connecting rod technologies tailored to market needs.

Market Opportunities

- •Rising demand for electric and hybrid vehicles in the UK presents significant opportunities for manufacturers to develop specialized connecting rods suited for these powertrains, including lightweight and high-strength alloys that meet unique performance requirements.

- •Expansion of the UK aftermarket segment driven by the aging vehicle population offers growth potential for replacement connecting rods, particularly those designed for performance enhancement and durability improvements.

- •Investment in advanced manufacturing capabilities such as additive manufacturing and precision forging opens avenues to produce customized connecting rods, enabling penetration into niche markets including motorsport and luxury vehicles.

- •Government incentives and funding for green technologies encourage R&D in sustainable materials and production processes, allowing companies to innovate and gain competitive advantage in the UK automotive components market.

- •Export potential to European and global markets remains a key opportunity, especially for UK firms with strong technological expertise and quality certifications, facilitating international market expansion.

Market Challenges

- •Stringent regulatory requirements regarding emissions and safety impose high compliance costs on manufacturers, necessitating continuous innovation and investment in material science and production technology.

- •Raw material price volatility, especially for specialty alloys like titanium, creates cost pressures that can impact profitability and pricing strategies for connecting rod producers.

- •The transition towards electric vehicles reduces demand for traditional internal combustion engine components, leading to potential market contraction and the need for product portfolio diversification.

- •Intense competition from low-cost manufacturers in Asia and Eastern Europe challenges UK-based companies to maintain quality leadership while managing cost competitiveness.

- •Supply chain disruptions due to geopolitical factors or logistical constraints can delay production schedules and increase operational costs, affecting market responsiveness.

Regulatory Framework

- •Between 2020 and 2025, the UK government implemented the Vehicle Emissions Standards (2021) mandating stricter limits on NOx and CO2 emissions for new vehicles, directly influencing connecting rod design towards lightweight and low-friction materials to improve engine efficiency.

- •The Sustainability in Automotive Manufacturing Act (2023) requires manufacturers to adopt environmentally friendly processes and promote recyclable materials in component production, impacting connecting rod material selection and manufacturing methods.

- •Safety Compliance Regulations (2022) introduced enhanced testing protocols for engine components to ensure durability and reliability under extreme conditions, compelling suppliers to uphold higher quality standards.

- •The UK Industrial Strategy (2024) includes incentives for innovation in electric and hybrid vehicle components, encouraging investment in R&D for advanced connecting rods compatible with alternative powertrains.

- •Trade and Tariff Policies post-Brexit (2021-2024) have led to new import-export requirements affecting supply chains, necessitating adaptation by connecting rod manufacturers to minimize disruption and maintain market access.

Market Intelligence

- •15th January 2025, GKN Automotive announced the launch of a new series of titanium alloy connecting rods designed specifically for hybrid and electric vehicle applications in the UK market. These rods offer a 30% weight reduction compared to conventional forged steel rods, enhancing vehicle efficiency and performance. The product leverages advanced forging technology and is targeted at premium OEMs aiming to meet stringent emissions targets while maintaining engine durability. This innovation is expected to strengthen GKN Automotive’s position in the UK connecting rod market and support the transition to electrified powertrains. Source: Official GKN Automotive Press Release

- •22nd March 2025, Mahle GmbH opened a new R&D center in Birmingham, UK, focused on developing next-generation connecting rods using powder metallurgy and additive manufacturing techniques. This facility aims to accelerate product development cycles and improve material efficiency, catering to both combustion and hybrid engine markets. The center is a strategic investment to capitalize on the UK’s growing electric vehicle industry and regulatory push for greener automotive components. Mahle expects enhanced collaboration with local automotive OEMs and suppliers. Source: Mahle Corporate Website

- •10th June 2025, Forged Components Ltd. announced its expansion of manufacturing capacity in Northern England with the installation of state-of-the-art forging presses and robotic machining lines. This investment aims to meet rising demand for forged steel connecting rods in passenger and commercial vehicles across the UK. The enhanced production capabilities will reduce lead times and increase output by 40%, supporting both OEM and aftermarket segments. The company highlighted its commitment to sustainable manufacturing practices aligned with UK environmental policies. Source: Forged Components Ltd. Official Announcement

- •5th September 2025, SinterCast AB signed a strategic partnership with a major UK automotive OEM to supply advanced powder metallurgy connecting rods tailored for high-performance electric hybrid powertrains. The collaboration focuses on joint development of lightweight, high-strength components optimized for efficiency and durability. This partnership underscores the growing importance of innovative materials in the UK automotive market and positions SinterCast as a key technology provider. The initiative is expected to accelerate adoption of powder metallurgy solutions in mainstream vehicle production. Source: Industry Publication

Regional Outlook

The Southern England currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Scotland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- England

- Scotland

- Wales

- Northern Ireland

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 1.73 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Material Type (Forged Steel Connecting Rods, Powder Metallurgy Connecting Rods, Cast Iron Connecting Rods, Aluminum Alloy Connecting Rods, Titanium Alloy Connecting Rods), Vehicle Application (Passenger Cars, Commercial Vehicles, Electric Vehicles, Motorsport Vehicles, Aftermarket Replacement), Manufacturing Technology (Forging, Casting, Powder Metallurgy, Machining), Distribution Channel (OEM Supply, Aftermarket Sales, Direct to Consumer, Tier-1 Supplier Networks) |

| Regions Covered | England, Scotland, Wales, Northern Ireland |

| Key Companies | GKN Automotive (United Kingdom), Metaldyne Performance Group (United States), Mahle GmbH (Germany), Federal-Mogul Motorparts (United States), Hitachi Metals, Ltd. (Japan) |

United Kingdom Automotive Connecting Rod Market - Outlook 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Market market is expected to see significant growth and value in 2025.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.