Europe Next Generation Sequencing Market - Size & Outlook 2025-2034

Europe Next Generation Sequencing (NGS) Market is segmented by Sequencing Type (Whole Genome Sequencing, Targeted Sequencing, RNA Sequencing, Exome Sequencing, Epigenetic Sequencing), Application (Clinical Diagnostics, Drug Discovery, Agricultural Genomics, Microbial Genomics, Personalized Medicine), Service Type (Sequencing Services, Data Analysis and Bioinformatics, Sample Preparation, Consulting and Support Services), Deployment Model (Cloud-based, On-premise, Hybrid), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

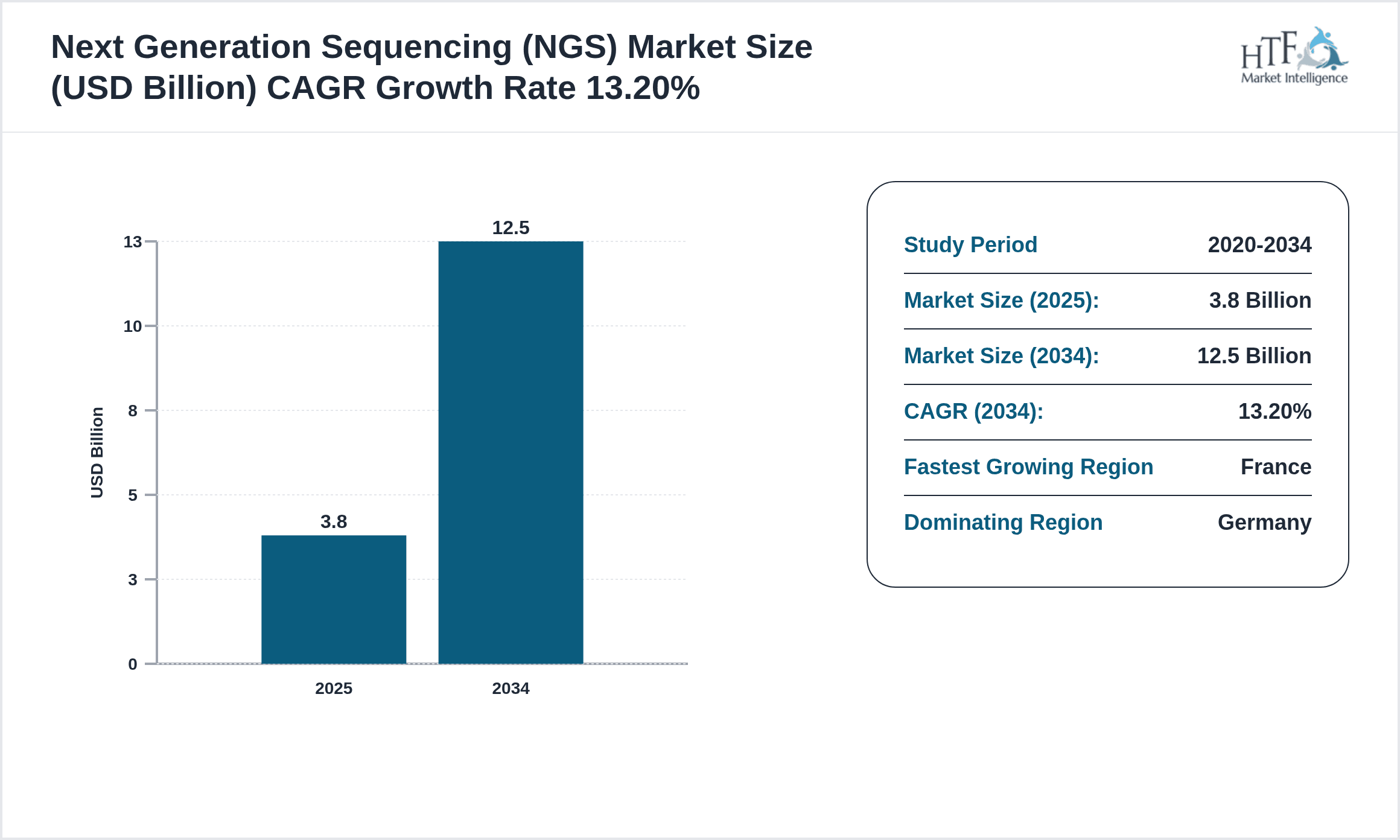

- •The Europe Next Generation Sequencing (NGS) market involves cutting-edge genomic sequencing technologies that facilitate rapid and large-scale analysis of DNA and RNA sequences. It covers a broad spectrum of applications including clinical diagnostics, drug discovery, agricultural genomics, microbial genomics, and personalized medicine. The market serves diverse end users such as hospitals, research centers, pharmaceutical and biotechnology companies, and agricultural research institutes. The value chain comprises sequencing platform manufacturers, consumables and reagent suppliers, bioinformatics software providers, and sequencing service providers. Rapid technological advancements, increasing adoption in clinical and research domains, and the rising demand for precision medicine are key drivers shaping this market. Additionally, the growing focus on agricultural genome analysis and microbial sequencing for environmental and health applications further propels market growth. Europe, led by countries such as Germany, France, and the United Kingdom, remains a critical hub for NGS innovation and deployment with significant investments in genomics infrastructure and regulatory support. The market is expected to witness robust expansion from USD 3.8 billion in 2025 to USD 12.5 billion by 2034 at a CAGR of 13.2%, driven by enhanced sequencing capabilities and expanding application horizons.

- •Key market highlights include the dominance of whole genome sequencing as the leading product type due to its comprehensive genomic insights, while RNA sequencing is the fastest growing segment reflecting increased interest in transcriptomic analysis. Germany stands as the dominating regional market within Europe, credited to its advanced healthcare infrastructure and strong biotech industry. France is identified as the fastest growing country owing to increased government funding and growing clinical adoption of NGS technologies. The market's growth is supported by ongoing innovations in sequencing platforms, reduction in sequencing costs, and the rising prevalence of genetic disorders necessitating advanced diagnostic tools. Furthermore, regulatory frameworks favoring genomic data integration and personalized healthcare adoption enhance market prospects.

- •The Europe NGS market presents a compelling value proposition to stakeholders including healthcare providers, pharmaceutical companies, and agricultural researchers. The technology's ability to deliver precise genomic information accelerates drug development, improves diagnostic accuracy, and enables tailored therapeutic interventions. For investors and industry participants, the market offers substantial growth opportunities driven by continuous R&D investments, strategic collaborations, and expanding applications in emerging fields such as microbiome analysis and epigenetics. The integration of bioinformatics and data analytics further strengthens the ecosystem, enabling actionable insights from complex genomic data. Overall, the Europe NGS market is strategically positioned to transform healthcare, agriculture, and life sciences, fostering innovation and economic growth across the region.

Competitive Landscape

The competitive environment in the Europe Next Generation Sequencing market is characterized by rapid technological innovation, strategic collaborations, and aggressive market expansion efforts by key players. Companies are focusing on developing next-gen sequencing platforms with enhanced speed, accuracy, and throughput to meet growing clinical and research demands. Market participants employ diverse competitive strategies including product differentiation through proprietary chemistries and bioinformatics solutions, mergers and acquisitions to consolidate technological capabilities, and regional partnerships to strengthen distribution networks. Pricing strategies vary across segments, with competitive pricing of consumables and instruments fostering broader adoption. Distribution channels include direct sales, partnerships with healthcare providers, and online platforms, facilitating widespread market penetration. Technology adoption trends emphasize integration of AI and machine learning for data interpretation, improving diagnostic utility. Barriers to entry include high R&D costs, regulatory compliance complexities, and the need for robust data security frameworks. Regional competition is intense with Western European countries leading innovation, while emerging markets within Europe are rapidly adopting NGS technologies. Future competitive trends point towards personalized medicine integration, expansion into novel application areas, and enhanced data management solutions.

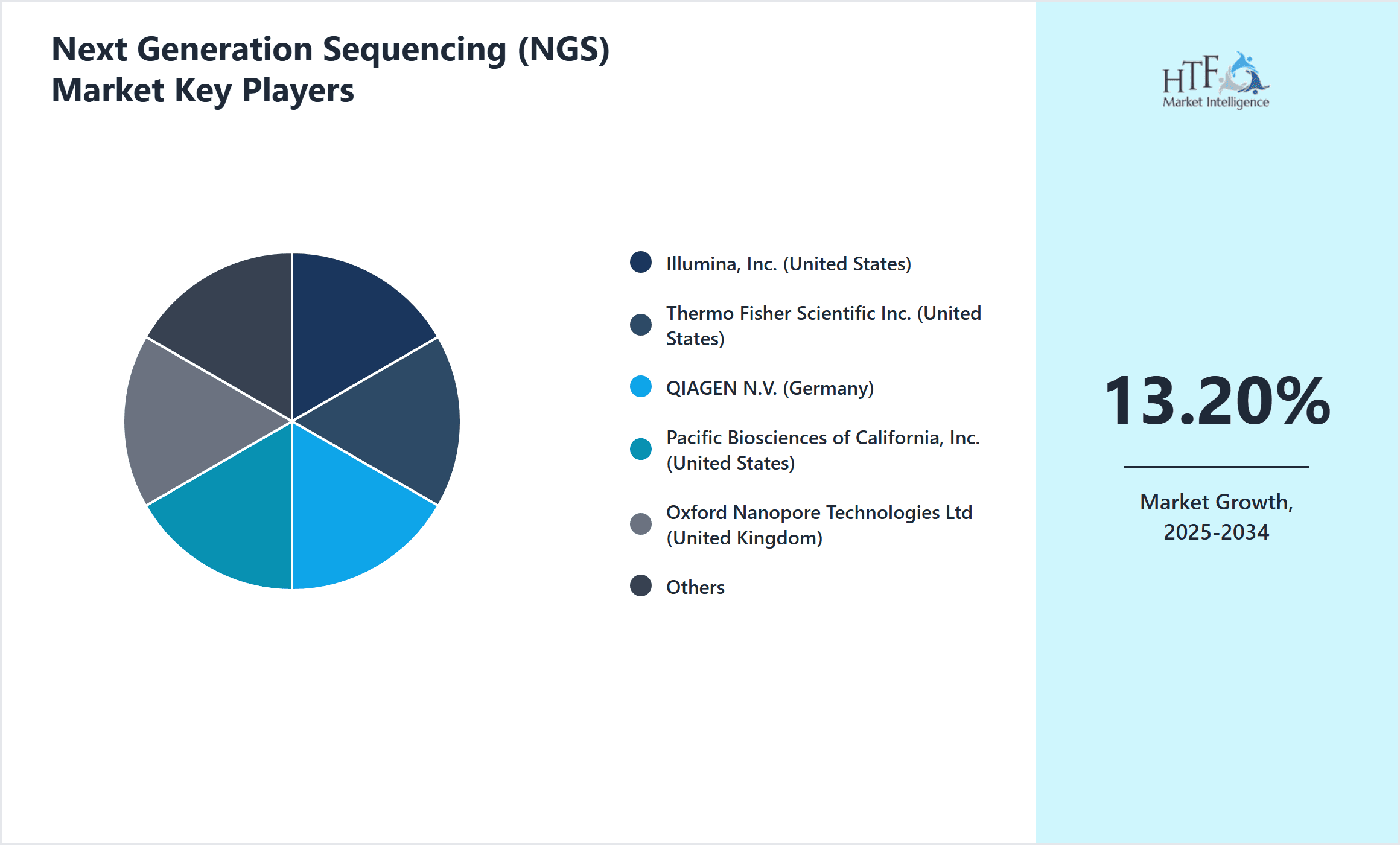

Prominent Players in Next Generation Sequencing Market

- •Illumina, Inc. (United States)

- •Thermo Fisher Scientific Inc. (United States)

- •QIAGEN N.V. (Germany)

- •Pacific Biosciences of California, Inc. (United States)

- •Oxford Nanopore Technologies Ltd (United Kingdom)

- •Roche Holding AG (Switzerland)

- •BGI Genomics Co., Ltd. (China)

- •Agilent Technologies, Inc. (United States)

- •PerkinElmer, Inc. (United States)

- •Genewiz, Inc. (United States)

- •Eurofins Scientific SE (Luxembourg)

- •SOPHiA GENETICS SA (Switzerland)

- •Novogene Corporation (China)

- •Takara Bio Inc. (Japan)

- •Eppendorf AG (Germany)

- •Qiagen GmbH (Germany)

- •Genomic Vision (France)

- •ArcherDX, Inc. (United States)

- •10x Genomics, Inc. (United States)

- •Novartis AG (Switzerland)

- •Bio-Rad Laboratories, Inc. (United States)

- •Illumina Cambridge Ltd. (United Kingdom)

- •CeGaT GmbH (Germany)

- •GenapSys, Inc. (United States)

- •F. Hoffmann-La Roche AG (Switzerland)

Market Breakdown

- •By Sequencing Type

- ◦Whole Genome Sequencing

- ◦Targeted Sequencing

- ◦RNA Sequencing

- ◦Exome Sequencing

- ◦Epigenetic Sequencing

- •By Application

- ◦Clinical Diagnostics

- ◦Drug Discovery

- ◦Agricultural Genomics

- ◦Microbial Genomics

- ◦Personalized Medicine

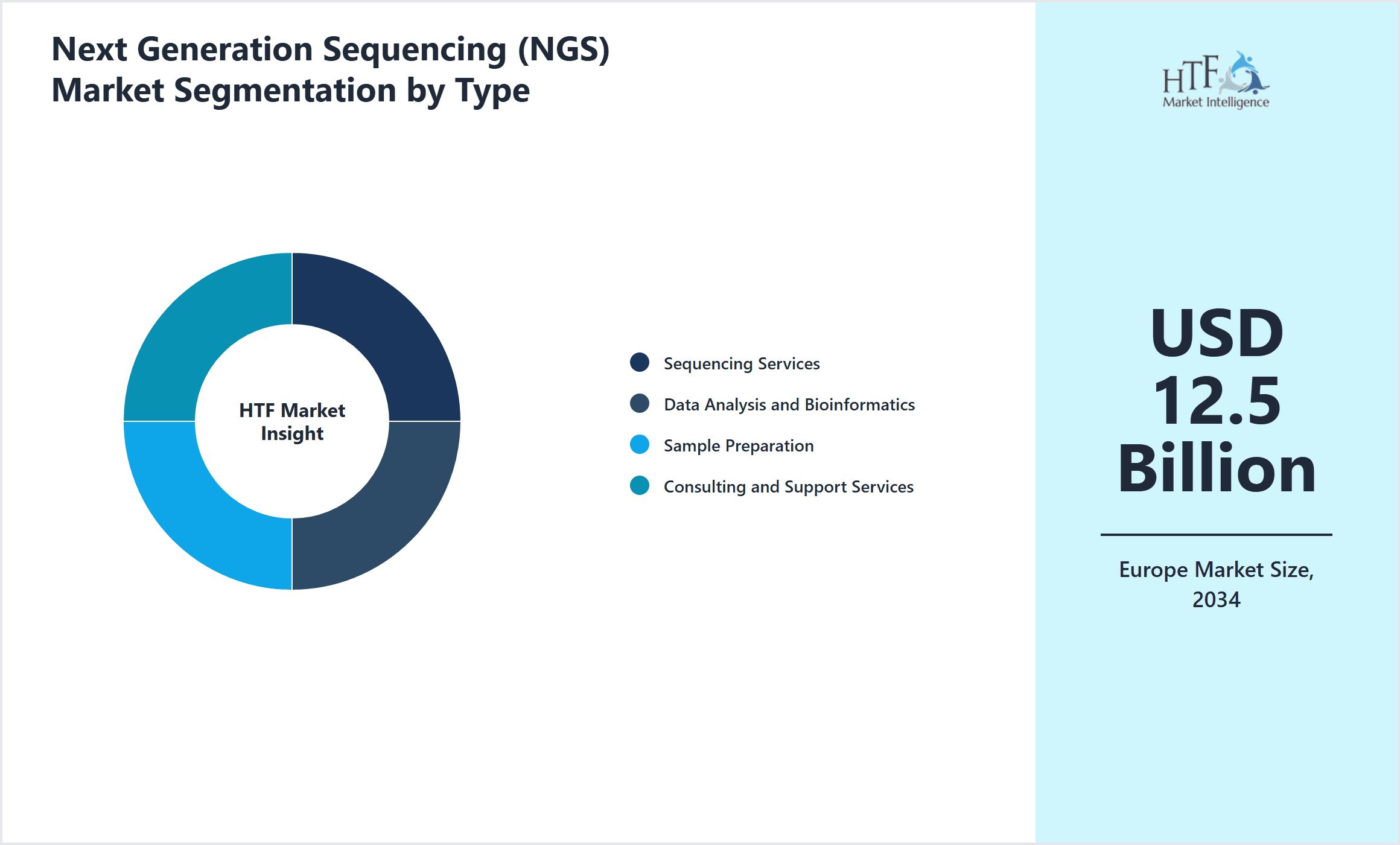

- •By Service Type

- ◦Sequencing Services

- ◦Data Analysis and Bioinformatics

- ◦Sample Preparation

- ◦Consulting and Support Services

- •By Deployment Model

- ◦Cloud-based

- ◦On-premise

- ◦Hybrid

Growth Dynamics

- •The rapid advancement of sequencing technologies has significantly reduced costs and increased throughput, enabling broader clinical and research adoption across Europe. For instance, the decreasing cost per genome has facilitated its integration into routine diagnostics and personalized medicine, driving market expansion.

- •Increased government funding and supportive policies in European countries such as Germany and France stimulate R&D investments in genomics and precision medicine, fostering robust market growth. These initiatives also accelerate infrastructure development for NGS applications in healthcare and agriculture.

- •Rising prevalence of genetic disorders and cancers in Europe has heightened demand for advanced diagnostic tools, positioning NGS as a critical technology for early detection, prognosis, and treatment monitoring. This clinical necessity is a key growth driver.

- •Expanding applications of NGS in emerging fields such as microbiome research, epigenetics, and agricultural genomics diversify the market and unlock new revenue streams, attracting investments from multiple industries including pharma and agri-biotech.

- •Strategic collaborations between sequencing platform providers, bioinformatics companies, and healthcare institutions enhance technological integration and service offerings, thereby strengthening market presence and customer reach throughout Europe.

- •The growing adoption of cloud-based bioinformatics and data analysis platforms facilitates efficient handling of large genomic datasets, improving accessibility and turnaround times for sequencing results which further supports market scalability.

- •Increasing awareness among clinicians and patients regarding the benefits of personalized medicine encourages the adoption of NGS, stimulating demand for customized therapies and targeted drug development in the European healthcare sector.

Market Trends

- •The integration of artificial intelligence and machine learning algorithms in NGS data analysis is transforming genomic interpretation by enhancing accuracy and predictive power, as demonstrated by leading European bioinformatics firms.

- •There is a growing trend towards decentralized and point-of-care sequencing solutions, enabling faster diagnostics and personalized treatment decisions particularly in oncology and infectious diseases.

- •Collaborative consortia between public and private sectors are increasing, pooling resources for large-scale genomics projects that advance research and clinical applications across Europe.

- •Sustainability initiatives are influencing NGS platform development, with manufacturers focusing on reducing reagent waste and energy consumption to align with European environmental regulations.

- •The shift from traditional sequencing towards single-cell and spatial transcriptomics technologies is gaining momentum, enabling deeper insights into cellular heterogeneity and disease mechanisms.

- •Cloud computing adoption for genomic data storage and analysis is rising steadily, driven by the need for scalable, secure, and collaborative research environments in Europe’s genomics landscape.

- •Increasing patient-centric approaches and real-world evidence integration into NGS workflows are reshaping clinical trial designs and personalized therapy development.

Market Opportunities

- •Expanding NGS applications in rare genetic disease diagnostics in Europe offers significant growth potential due to unmet clinical needs and advances in genetic counseling services.

- •Emerging agricultural genomics markets present opportunities for NGS technologies to enhance crop yield, disease resistance, and food security across European farming sectors.

- •Investment in cloud-based bioinformatics platforms and AI-driven analytics can unlock new service models and improve accessibility to complex genomic data interpretation for smaller laboratories and clinics.

- •Collaborations with pharmaceutical companies to develop companion diagnostics and biomarker discovery platforms enable co-development of targeted therapies, enhancing market penetration.

- •Government incentives promoting precision medicine adoption facilitate market entry for innovative sequencing solutions tailored to public healthcare systems.

- •Expanding the scope of microbial genomics for infectious disease surveillance and antibiotic resistance monitoring creates new avenues for NGS applications in public health.

- •Development of portable and rapid sequencing devices for clinical and field use offers opportunities to address unmet needs in point-of-care diagnostics and environmental genomics.

Market Challenges

- •High initial capital expenditure and operational costs associated with advanced NGS platforms limit adoption especially among smaller healthcare providers and research institutions.

- •Complex regulatory frameworks across European countries pose challenges for uniform market entry and compliance, affecting commercialization timelines of new sequencing technologies.

- •Data privacy concerns and stringent GDPR regulations complicate the management, sharing, and storage of sensitive genomic data, necessitating robust cybersecurity measures.

- •Shortage of skilled bioinformatics professionals and genomic data analysts restricts the effective utilization of NGS technologies and interpretation of complex datasets.

- •Integration of NGS data into existing clinical workflows requires significant training and infrastructure upgrades, delaying widespread clinical adoption.

- •Variability in reimbursement policies across European healthcare systems limits consistent access to NGS-based diagnostics for patients.

- •Rapid technological advancements may lead to product obsolescence and require continuous capital investment to keep pace with evolving market standards.

Regulatory Framework

- •The EU In Vitro Diagnostic Regulation (IVDR) implemented between 2022 and 2025 mandates stringent compliance for NGS-based diagnostic devices, including performance evaluation and post-market surveillance, enhancing patient safety and market transparency.

- •GDPR regulations enacted before 2020 impose strict data protection requirements for genomic data, influencing how NGS data is collected, processed, and shared across European countries, with significant impact on bioinformatics service providers.

- •Country-specific guidelines such as Germany’s Medical Devices Act and France’s ANSM regulations provide frameworks for clinical validation and approval of NGS technologies, affecting market entry strategies.

- •The European Medicines Agency (EMA) supports genomic data incorporation in drug development and companion diagnostics, fostering innovation while ensuring regulatory compliance for novel therapeutics.

- •Government initiatives promoting precision medicine, including funding programs and reimbursement policies, vary across Europe but collectively aim to enhance availability and affordability of NGS diagnostics within public healthcare systems.

Market Intelligence

- •15th January 2025, Illumina, Inc. announced the launch of its NovaSeq X Plus sequencing system in Europe, featuring enhanced throughput and reduced sequencing costs to accelerate clinical and research applications. The platform integrates advanced AI-driven data analysis tools designed to streamline genomic workflows and improve diagnostic accuracy. This launch aims to strengthen Illumina’s market leadership in the European NGS sector by catering to growing demand across clinical diagnostics and pharmaceutical research. The system also offers enhanced scalability for laboratories of varying sizes, supporting precision medicine initiatives across the region. Source: Illumina Official Press Release

- •3rd March 2025, QIAGEN N.V. introduced an updated QIAseq targeted sequencing panel optimized for oncology applications in European markets. The new panel provides higher sensitivity for rare mutation detection and improved compatibility with formalin-fixed paraffin-embedded (FFPE) samples, addressing key clinical challenges. QIAGEN’s bioinformatics suite accompanying the panel delivers comprehensive variant interpretation and reporting, enabling streamlined integration into clinical workflows. This development reflects the company’s commitment to advancing precision oncology and expanding its presence in European clinical laboratories. Source: QIAGEN Corporate Announcement

- •20th May 2025, Oxford Nanopore Technologies Ltd expanded its European operations by opening a new sequencing center in Germany, aimed at enhancing service capabilities and customer support. The facility focuses on delivering ultra-long-read sequencing services and real-time data analysis for applications in microbial genomics and infectious disease surveillance. This strategic expansion is intended to meet increasing demand from research institutions and healthcare providers across Europe, facilitating faster turnaround times and localized technical assistance. The move also underscores Oxford Nanopore’s commitment to innovation and market penetration in the region. Source: Oxford Nanopore Technologies Press Release

- •10th October 2024, Thermo Fisher Scientific Inc. completed the acquisition of a European bioinformatics startup specializing in AI-driven genomic data interpretation. The acquisition enhances Thermo Fisher’s portfolio with advanced analytics capabilities, enabling more precise and scalable genomic insights for clinical and research customers. This strategic move supports Thermo Fisher’s goal to integrate sequencing hardware and software solutions, creating end-to-end platforms for European markets. It also positions the company to leverage growing investments in precision medicine and personalized healthcare across the continent. Source: Thermo Fisher Official News

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 12.5 Billion |

| CAGR | 13.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.5% |

| Scope of Report | Market is segmented by Sequencing Type (Whole Genome Sequencing, Targeted Sequencing, RNA Sequencing, Exome Sequencing, Epigenetic Sequencing), Application (Clinical Diagnostics, Drug Discovery, Agricultural Genomics, Microbial Genomics, Personalized Medicine), Service Type (Sequencing Services, Data Analysis and Bioinformatics, Sample Preparation, Consulting and Support Services), Deployment Model (Cloud-based, On-premise, Hybrid) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Illumina, Inc. (United States), Thermo Fisher Scientific Inc. (United States), QIAGEN N.V. (Germany), Pacific Biosciences of California, Inc. (United States), Oxford Nanopore Technologies Ltd (United Kingdom), Roche Holding AG (Switzerland), BGI Genomics Co., Ltd. (China), Agilent Technologies, Inc. (United States), PerkinElmer, Inc. (United States), Genewiz, Inc. (United States), Eurofins Scientific SE (Luxembourg), SOPHiA GENETICS SA (Switzerland), Novogene Corporation (China), Takara Bio Inc. (Japan), Eppendorf AG (Germany), Qiagen GmbH (Germany), Genomic Vision (France), ArcherDX, Inc. (United States), 10x Genomics, Inc. (United States), Novartis AG (Switzerland), Bio-Rad Laboratories, Inc. (United States), Illumina Cambridge Ltd. (United Kingdom), CeGaT GmbH (Germany), GenapSys, Inc. (United States), F. Hoffmann-La Roche AG (Switzerland) |

Europe Next Generation Sequencing Market - Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.