Europe Four Channel Coagulation Analyzer Market - Outlook 2024-2034

Europe Four Channel Coagulation Analyzer Market is segmented by Type (Automated Four Channel Coagulation Analyzer, Semi-Automated Four Channel Coagulation Analyzer, Manual Four Channel Coagulation Analyzer, Portable Four Channel Coagulation Analyzer, Benchtop Four Channel Coagulation Analyzer), Application (Hemostasis Testing, Cardiovascular Disease Monitoring, Surgical Procedures, Research Laboratories, Blood Banks), End-User Facility (Hospitals, Diagnostic Laboratories, Blood Banks, Research Institutes), Deployment Model (Point-of-Care Testing, Central Laboratory Testing), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Four Channel Coagulation Analyzer market is defined by its focus on sophisticated diagnostic equipment that simultaneously evaluates four coagulation parameters to assist clinicians in effective blood clotting assessment. This market spans a range of device types including automated, semi-automated, manual, portable, and benchtop analyzers, utilized across applications such as hemostasis testing, cardiovascular disease monitoring, surgical procedures, research laboratories, and blood banks. The technological scope includes instrumentation, reagents, and software integration, enabling rapid, precise, and reproducible coagulation diagnostics essential for managing bleeding disorders and guiding therapy. The industry is bounded by stringent European regulatory frameworks, high-quality standards, and growing healthcare investments. The market's strategic importance lies in enhancing patient safety, reducing procedural complications, and supporting personalized medicine initiatives. Key drivers include increasing incidence of cardiovascular diseases, expanding geriatric populations, and rising demand for point-of-care testing. This market report comprehensively analyzes segmentation, competitive landscape, growth dynamics, and regulatory environment shaping the Europe Four Channel Coagulation Analyzer industry through 2034.

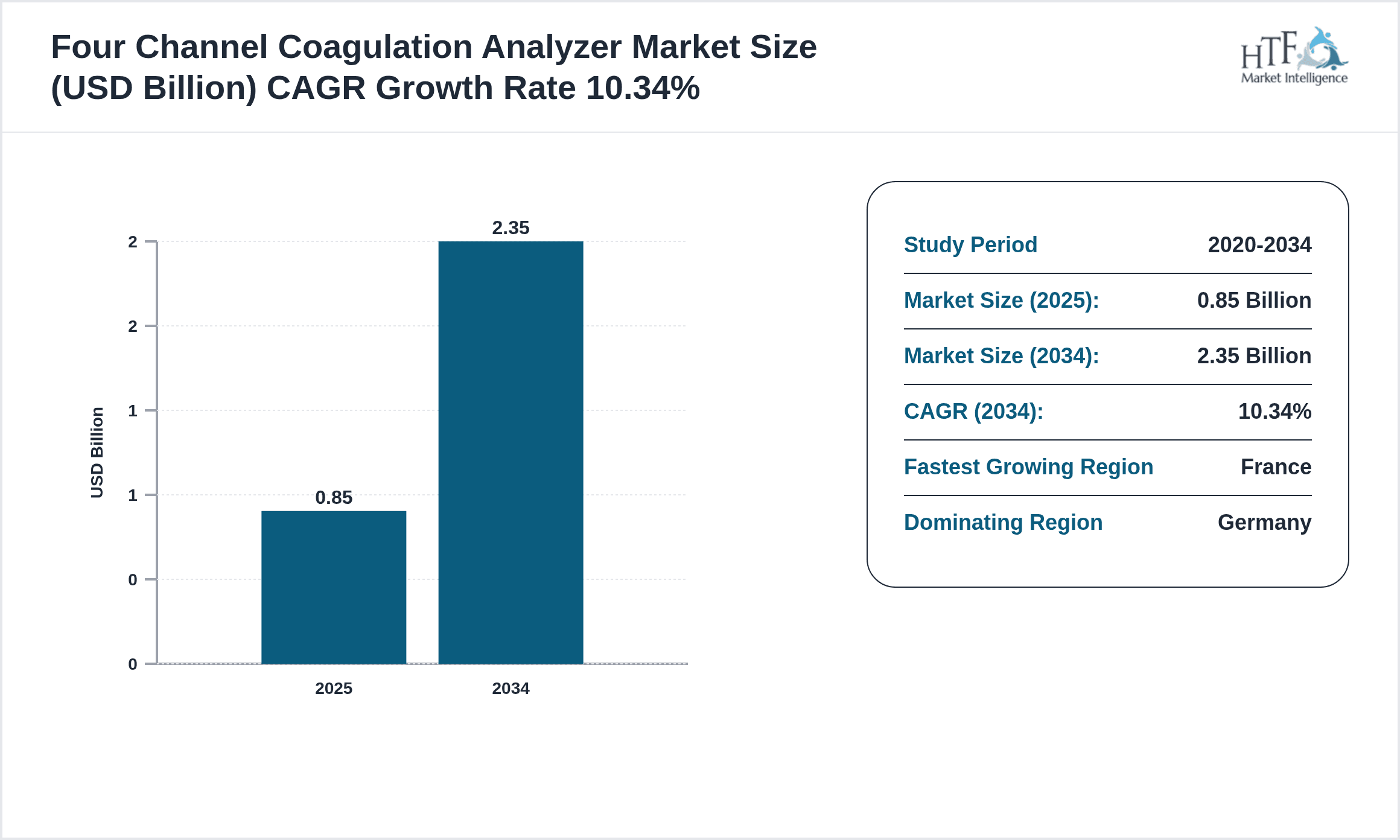

- •The market is projected to grow from USD 0.85 Billion in 2024 to USD 2.35 Billion by 2034, exhibiting a robust CAGR of approximately 10.34%. Dominated by Germany in terms of market share, the region of France is expected to witness the fastest growth rate supported by increasing healthcare infrastructure and rising adoption of portable analyzers. Automated analyzers lead the product category due to their accuracy and efficiency, while portable analyzers are gaining momentum driven by point-of-care testing trends. Key players are investing in R&D to enhance analyzer capabilities and expand regional footprints. The market faces challenges such as stringent regulatory compliance and high device costs, yet opportunities exist through technological advancements and emerging applications in personalized coagulation monitoring.

- •The Europe Four Channel Coagulation Analyzer market offers significant value to healthcare providers, diagnostic laboratories, and patients by enabling timely and accurate coagulation assessment essential for effective treatment management. The market's strategic importance is underscored by its role in improving surgical outcomes, managing anticoagulant therapy, and supporting research innovations. Furthermore, the integration of automated and portable analyzers aligns with the growing demand for efficient workflow and decentralized testing in hospitals and clinics. Stakeholders including manufacturers, distributors, and regulatory bodies benefit from insights into market trends, competitive positioning, and emerging growth opportunities, facilitating informed decision-making and investment strategies within the European healthcare diagnostics landscape.

Competitive Landscape

The Europe Four Channel Coagulation Analyzer market is characterized by intense competition among established multinational corporations and emerging regional players. Market dynamics are driven by continuous innovation in analyzer technology, including automation, miniaturization, and integration with digital health platforms. Companies employ strategies such as product differentiation through enhanced accuracy, faster turnaround times, and user-friendly interfaces to gain competitive advantage. Strategic partnerships, collaborations with research institutes, and acquisitions are common to expand product portfolios and geographic reach. Price competition remains moderate due to high regulatory standards and quality expectations, but affordability remains a consideration for smaller healthcare providers. The competitive environment is also influenced by evolving reimbursement policies and the increasing emphasis on point-of-care testing, fueling investments in portable analyzers. Future trends indicate consolidation and technological convergence, with companies focusing on artificial intelligence and connectivity to differentiate offerings and strengthen market position.

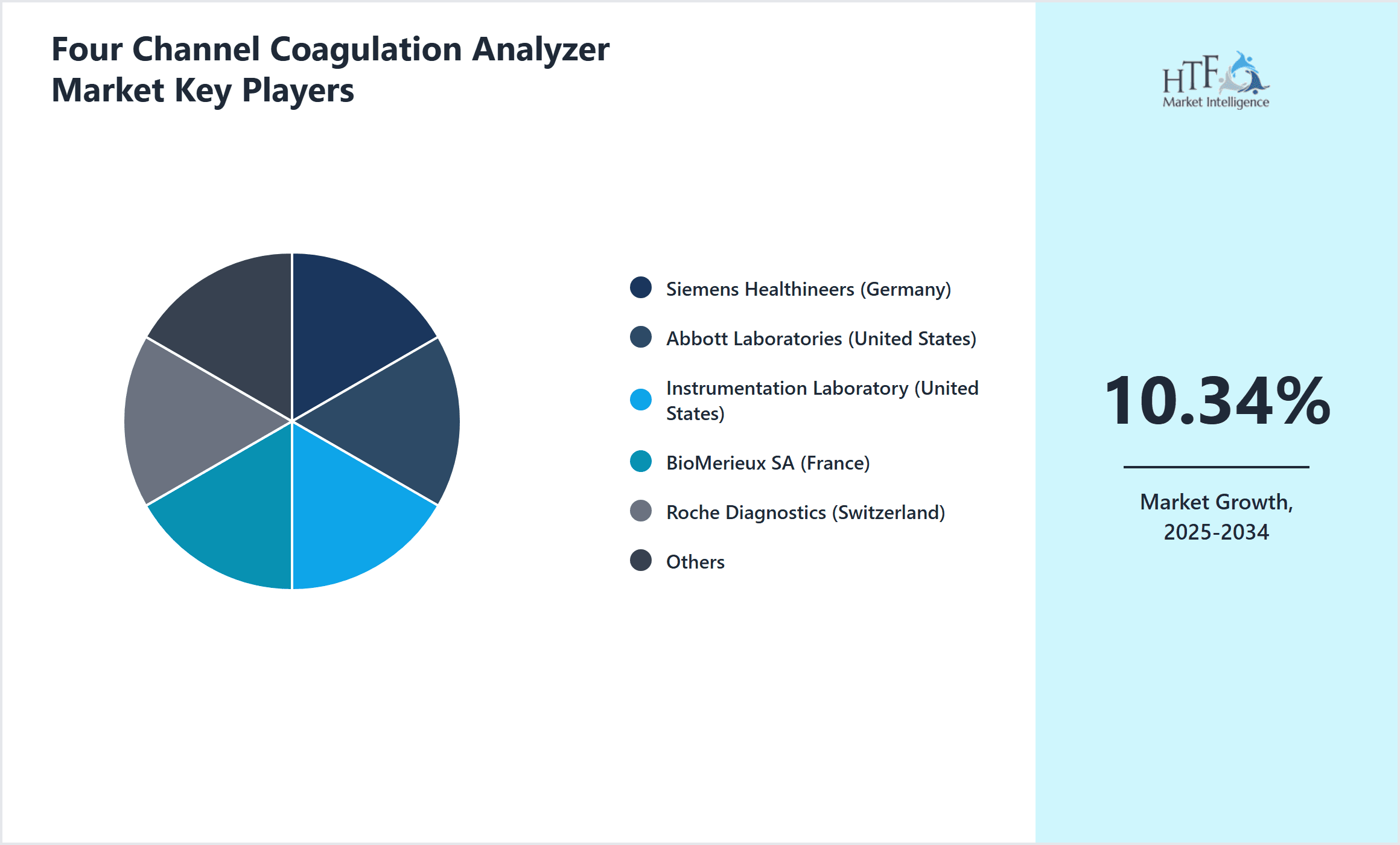

Leading Companies in Four Channel Coagulation Analyzer Market

- •Siemens Healthineers (Germany)

- •Abbott Laboratories (United States)

- •Instrumentation Laboratory (United States)

- •BioMerieux SA (France)

- •Roche Diagnostics (Switzerland)

- •Werfen (Spain)

- •Stago Group (France)

- •Sysmex Corporation (Japan)

- •Thermo Fisher Scientific (United States)

- •Ortho Clinical Diagnostics (United States)

- •HORIBA Medical (France)

- •Mindray Medical International (China)

- •Beckman Coulter (United States)

- •DiaSys Diagnostic Systems (Germany)

- •HemosIL (United States)

- •Becton Dickinson (United States)

- •Instrumentation Laboratory (Italy)

- •Agilent Technologies (United States)

- •Bio-Rad Laboratories (United States)

- •Horiba Ltd. (Japan)

- •Mindray Bio-Medical Electronics (China)

- •DiaMed GmbH (Switzerland)

- •Sysmex Europe GmbH (Germany)

- •Quidel Corporation (United States)

- •Sekisui Diagnostics (Japan)

Market Breakdown

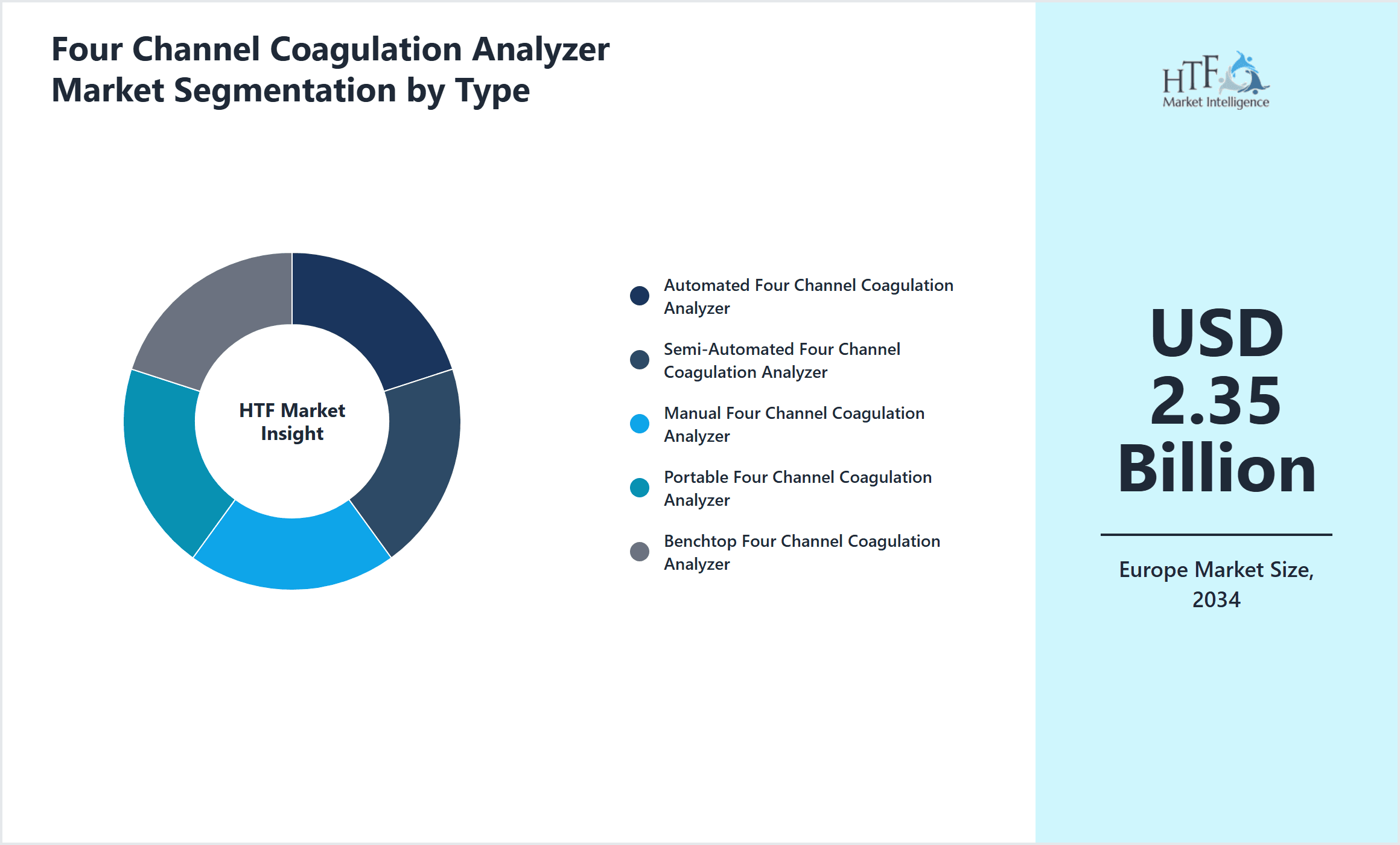

- •By Type

- ◦Automated Four Channel Coagulation Analyzer

- ◦Semi-Automated Four Channel Coagulation Analyzer

- ◦Manual Four Channel Coagulation Analyzer

- ◦Portable Four Channel Coagulation Analyzer

- ◦Benchtop Four Channel Coagulation Analyzer

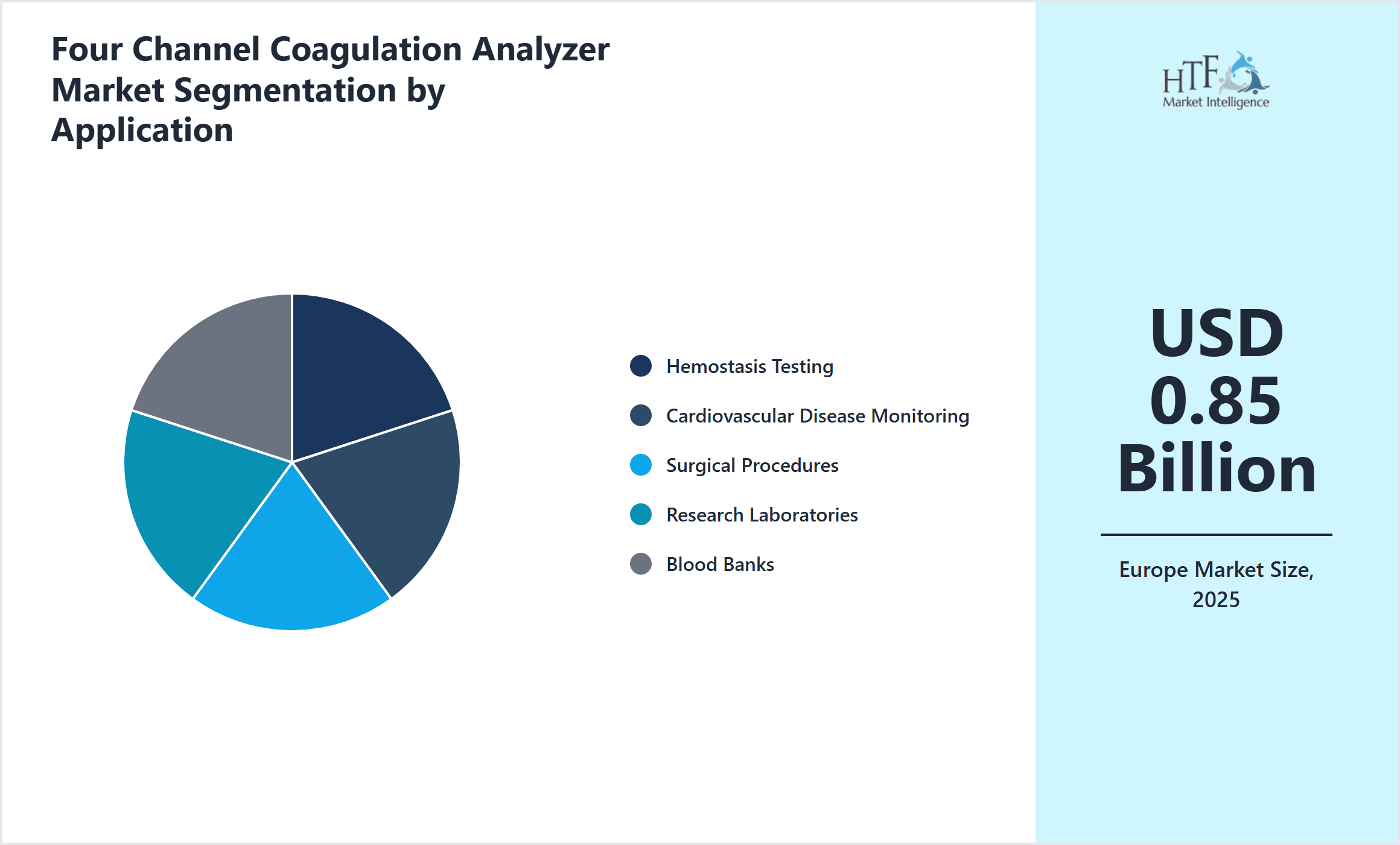

- •By Application

- ◦Hemostasis Testing

- ◦Cardiovascular Disease Monitoring

- ◦Surgical Procedures

- ◦Research Laboratories

- ◦Blood Banks

- •By End-User Facility

- ◦Hospitals

- ◦Diagnostic Laboratories

- ◦Blood Banks

- ◦Research Institutes

- •By Deployment Model

- ◦Point-of-Care Testing

- ◦Central Laboratory Testing

Growth Dynamics

- •The Europe Four Channel Coagulation Analyzer market is propelled by increasing prevalence of cardiovascular diseases and bleeding disorders across the region, necessitating precise coagulation monitoring for effective treatment. Rising geriatric population elevates demand for diagnostic solutions, as elderly patients are more prone to coagulation abnormalities. Technological advancements in analyzer automation and integration with hospital information systems enhance workflow efficiency, attracting healthcare providers. Government initiatives promoting early diagnosis and improved healthcare infrastructure investment further stimulate market growth. Additionally, the growing adoption of point-of-care testing devices in outpatient and emergency settings supports market expansion by enabling rapid clinical decisions and improving patient outcomes.

- •Medical device manufacturers continuously innovate to improve analyzer functionality, accuracy, and usability, driving market growth. Portable analyzers are gaining traction due to their convenience and suitability for decentralized testing. Increasing awareness among clinicians about the benefits of multi-parameter coagulation testing leads to higher adoption rates. Furthermore, reimbursement policies favoring advanced diagnostics enhance market attractiveness. Collaborations between reagent suppliers and instrument manufacturers facilitate integrated solutions, providing end-users with streamlined workflows. The trend towards personalized medicine and precision healthcare encourages the development of analyzers capable of customized coagulation profiling, broadening application scope and market potential.

- •Despite robust growth drivers, the market faces challenges such as stringent European regulatory requirements that prolong product approvals and increase compliance costs. High acquisition and maintenance costs of automated analyzers limit accessibility for smaller healthcare facilities, restraining market penetration. Additionally, the need for skilled personnel to operate complex instruments poses operational barriers. Market growth is also affected by competition from alternative diagnostic technologies and point-of-care devices that offer simplified testing. Variability in reimbursement frameworks across European countries creates uncertainty and impacts purchasing decisions. These challenges necessitate strategic approaches by manufacturers to offer cost-effective, easy-to-use solutions compliant with regulatory standards.

- •Opportunities abound in expanding the portable and point-of-care analyzer segments, leveraging technological miniaturization and wireless connectivity to serve remote and ambulatory care settings. Emerging markets within Eastern and Southern Europe present untapped demand due to improving healthcare infrastructure and rising disease burden. Integration of artificial intelligence and data analytics in coagulation analyzers offers potential for enhanced diagnostic accuracy and predictive capabilities. Strategic partnerships with hospitals and diagnostic chains can facilitate wider adoption. Additionally, development of multiplex testing reagents and consumables tailored for four-channel analyzers provides revenue growth avenues. The growing emphasis on personalized coagulation monitoring and tailored therapies opens new application domains, further expanding market scope.

- •Key challenges include managing the cost pressures from healthcare providers seeking budget-friendly diagnostic solutions while maintaining high accuracy and compliance. Supply chain disruptions and raw material shortages affect production timelines and costs. Rapid technological obsolescence requires continuous investment in R&D to keep pace with innovation. Data security and interoperability issues arise with increasing digitization and connectivity of analyzers. Moreover, competitive intensity from generic and low-cost analyzer suppliers may erode market shares of established players. Navigating diverse regulatory frameworks across European countries and ensuring adherence to evolving standards remain complex. Addressing these challenges is critical for sustained growth and market leadership.

Market Trends

- •A significant trend in the Europe Four Channel Coagulation Analyzer market is the increasing adoption of automated systems with enhanced throughput and connectivity features, allowing seamless integration with laboratory information management systems to improve diagnostic workflows and data management.

- •Portable and point-of-care coagulation analyzers are gaining prominence in ambulatory care and emergency settings, driven by the demand for rapid, on-site testing that facilitates timely clinical decision-making and improves patient outcomes.

- •Manufacturers are focusing on reagent kits compatible with multiple analyzer platforms, increasing flexibility and reducing operational costs for healthcare providers while expanding the analyzers' application range.

- •Integration of digital health technologies, including cloud-based data storage and artificial intelligence algorithms, is transforming coagulation diagnostics by enabling predictive analytics and personalized patient monitoring.

- •Collaborations between diagnostic companies and healthcare institutions are facilitating clinical trials and validation studies to improve device accuracy and expand indications, fostering innovation and market acceptance.

- •Sustainability initiatives are influencing product design with manufacturers adopting eco-friendly materials and energy-efficient technologies to comply with European environmental regulations and reduce carbon footprint.

- •The development of multiplex testing capabilities within four channel analyzers allows simultaneous measurement of multiple coagulation parameters, enhancing diagnostic efficiency and clinical relevance.

Market Opportunities

- •Expanding point-of-care testing capabilities to underserved regions in Europe presents a strategic opportunity to increase market penetration and improve patient care by enabling decentralized coagulation diagnostics.

- •Developing cost-effective analyzer models tailored for small clinics and diagnostic centers can address affordability barriers and widen the user base across the region.

- •Integrating artificial intelligence and machine learning into coagulation analyzers offers potential for advanced predictive diagnostics, enabling early detection of coagulation abnormalities and personalized treatment planning.

- •Collaborating with pharmaceutical companies to co-develop diagnostic solutions for anticoagulant therapies can create synergistic value and open new revenue streams.

- •Leveraging digital connectivity and remote monitoring features can facilitate telemedicine applications, enhancing chronic disease management and patient engagement.

- •Introducing reagent kits compatible with multiple analyzer platforms can increase customer retention and provide cross-selling opportunities within the coagulation diagnostics portfolio.

- •Targeting emerging markets within Europe with customized marketing and distribution strategies can unlock latent demand driven by improving healthcare infrastructures and rising disease incidence.

Market Challenges

- •Navigating the complex regulatory landscape in Europe, including compliance with the In Vitro Diagnostic Regulation (IVDR), imposes significant time and financial burdens on manufacturers seeking market approval for new coagulation analyzers.

- •High costs associated with advanced automated analyzers limit adoption among smaller healthcare providers and diagnostic laboratories, constraining market growth in certain segments.

- •The requirement for skilled laboratory personnel to operate and maintain sophisticated coagulation analyzers poses training and operational challenges, particularly in decentralized healthcare settings.

- •Competition from alternative diagnostic technologies and simpler point-of-care devices may reduce market share for four channel analyzers, necessitating continuous innovation to maintain relevance.

- •Supply chain disruptions and raw material shortages impact production schedules and costs, creating uncertainties for manufacturers and healthcare providers alike.

- •Data security and interoperability concerns arise as coagulation analyzers increasingly adopt digital connectivity, requiring robust cybersecurity measures and compliance with data protection regulations.

- •Variability in healthcare reimbursement policies across European countries creates market entry and expansion challenges, affecting purchasing decisions and revenue predictability.

Regulatory Framework

- •Between 2019 and 2024, the European Union implemented the In Vitro Diagnostic Regulation (IVDR) to replace the previous Directive, imposing stricter requirements on safety, performance, and clinical evidence for coagulation analyzers, significantly impacting product approval timelines and compliance costs.

- •The IVDR mandates enhanced post-market surveillance and vigilance reporting, requiring manufacturers to establish robust quality management systems and continuous performance monitoring of coagulation analyzers in Europe.

- •Country-specific mandates, such as Germany's Medical Devices Act (MPG) amendments, harmonize with the IVDR to ensure consistent regulatory oversight, affecting market entry strategies for coagulation analyzer manufacturers.

- •Environmental regulations in Europe promote sustainable manufacturing practices, influencing the design and disposal of analyzer components and reagents to minimize ecological impact.

- •Government initiatives supporting digital health integration encourage manufacturers to develop coagulation analyzers compatible with electronic health records and telemedicine applications, fostering innovation under the regulatory umbrella.

Market Intelligence

- •15th March 2024, Siemens Healthineers launched the Atellica COAG 360, an automated four channel coagulation analyzer designed for high-throughput clinical laboratories. The device features advanced multiplex testing capabilities, seamless integration with laboratory information systems, and AI-driven data analytics for enhanced diagnostic accuracy. Targeting European hospitals and diagnostic centers, this launch aims to streamline workflow and reduce turnaround times, addressing the growing demand for efficient hemostasis testing. Siemens Healthineers emphasized the analyzer's compliance with IVDR requirements and its role in supporting personalized anticoagulant therapy management. The product is expected to strengthen Siemens' market leadership in Europe’s coagulation diagnostics sector. Source: Siemens Healthineers Official Press Release

- •22nd November 2023, Stago Group introduced the STA Compact Max, a portable four channel coagulation analyzer optimized for point-of-care settings including emergency departments and outpatient clinics. The device offers rapid results within 10 minutes and is compatible with a wide range of reagent kits, increasing flexibility for European healthcare providers. Stago’s innovation supports the trend toward decentralized testing and is designed to meet stringent European regulatory standards, including IVDR compliance. The product launch reflects growing demand for portable coagulation diagnostics driven by the COVID-19 pandemic’s impact on healthcare delivery models. This strategic move is anticipated to expand Stago’s presence in the European point-of-care market. Source: Stago Group Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 2.35 Billion |

| CAGR | 10.34% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.34% |

| Scope of Report | Market is segmented by Type (Automated Four Channel Coagulation Analyzer, Semi-Automated Four Channel Coagulation Analyzer, Manual Four Channel Coagulation Analyzer, Portable Four Channel Coagulation Analyzer, Benchtop Four Channel Coagulation Analyzer), Application (Hemostasis Testing, Cardiovascular Disease Monitoring, Surgical Procedures, Research Laboratories, Blood Banks), End-User Facility (Hospitals, Diagnostic Laboratories, Blood Banks, Research Institutes), Deployment Model (Point-of-Care Testing, Central Laboratory Testing) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Siemens Healthineers (Germany), Abbott Laboratories (United States), Instrumentation Laboratory (United States), BioMerieux SA (France), Roche Diagnostics (Switzerland), Werfen (Spain), Stago Group (France), Sysmex Corporation (Japan), Thermo Fisher Scientific (United States), Ortho Clinical Diagnostics (United States), HORIBA Medical (France), Mindray Medical International (China), Beckman Coulter (United States), DiaSys Diagnostic Systems (Germany), HemosIL (United States), Becton Dickinson (United States), Instrumentation Laboratory (Italy), Agilent Technologies (United States), Bio-Rad Laboratories (United States), Horiba Ltd. (Japan), Mindray Bio-Medical Electronics (China), DiaMed GmbH (Switzerland), Sysmex Europe GmbH (Germany), Quidel Corporation (United States), Sekisui Diagnostics (Japan) |

Europe Four Channel Coagulation Analyzer Market - Outlook 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Market market is projected to grow at a steady CAGR from 2025 to 2030, driven by increasing demand and expansion in various applications.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.