Global Photovoltaic Transparent Glass Market Size, Growth & Revenue 2024-2034

Global Photovoltaic Transparent Glass Market is segmented by Type (Amorphous Silicon Photovoltaic Glass, Crystalline Silicon Photovoltaic Glass, Thin Film Photovoltaic Glass, Organic Photovoltaic Transparent Glass, Perovskite Photovoltaic Transparent Glass), Application (Building Integrated Photovoltaics (BIPV), Automotive Glazing, Consumer Electronics Displays, Architectural Glass, Others (Agricultural, Marine, etc.)), End-Use Sector (Residential Buildings, Commercial Buildings, Industrial Facilities, Transportation), Deployment Model (New Construction Integration, Retrofit Installations), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global photovoltaic transparent glass market is defined by the production and application of glass products embedded with photovoltaic cells that allow light transmission while generating solar energy. This market embraces a variety of technologies including amorphous silicon, crystalline silicon, and thin-film photovoltaic cells, each catering to distinct performance and application requirements. Its scope extends to sectors such as building-integrated photovoltaics, automotive glazing, consumer electronics, and architectural glass, providing energy-efficient and aesthetically appealing solutions. The industry is driven by increasing demand for renewable energy sources, government incentives, and advancements in material technology that enable seamless integration of solar energy harvesting in everyday surfaces. Key use cases include energy-generating windows, solar facades, and transparent solar panels, which contribute to reducing carbon footprints and enhancing energy independence worldwide. The market’s growth is underpinned by global sustainability goals, urbanization, and technological innovation fostering widespread adoption of photovoltaic transparent glass in multiple industries.

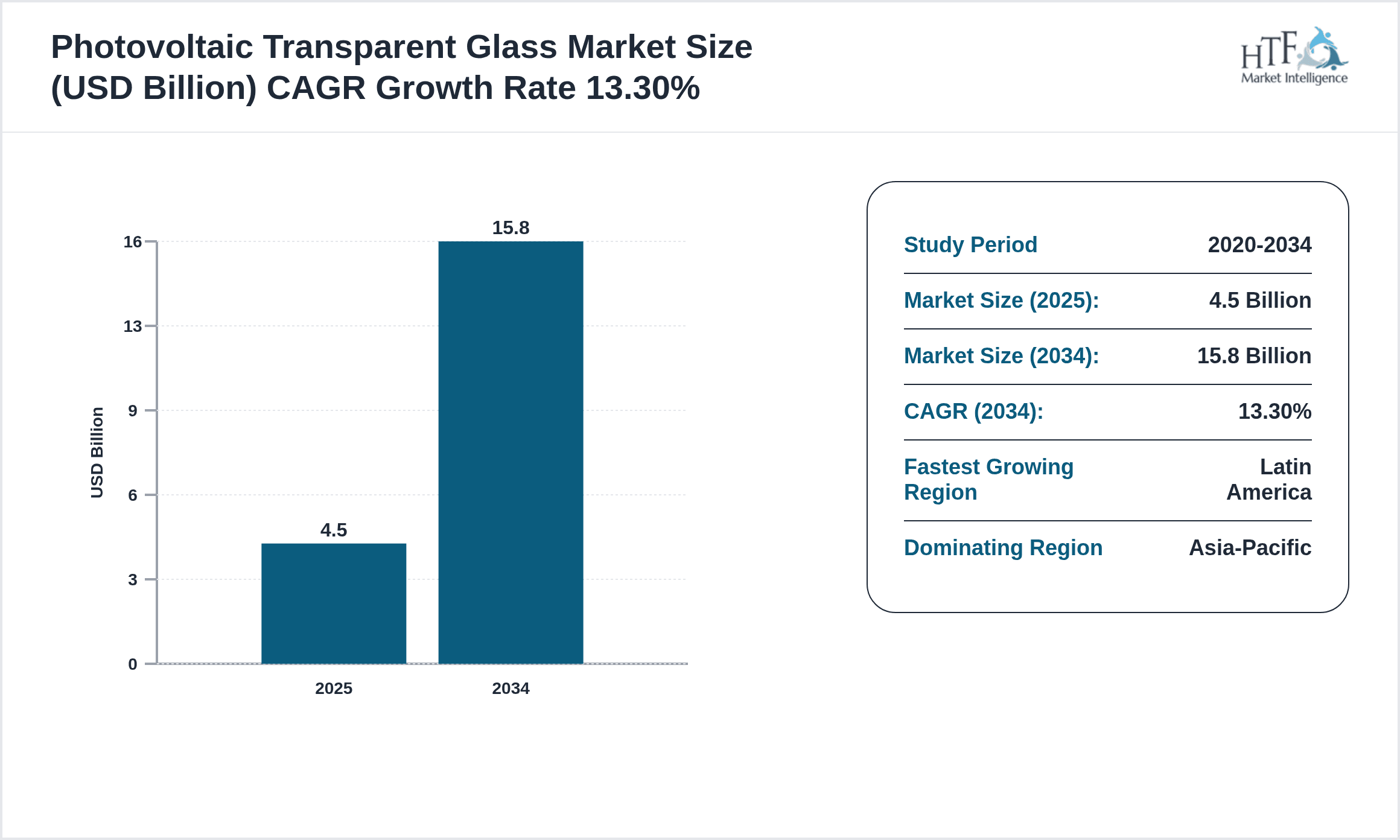

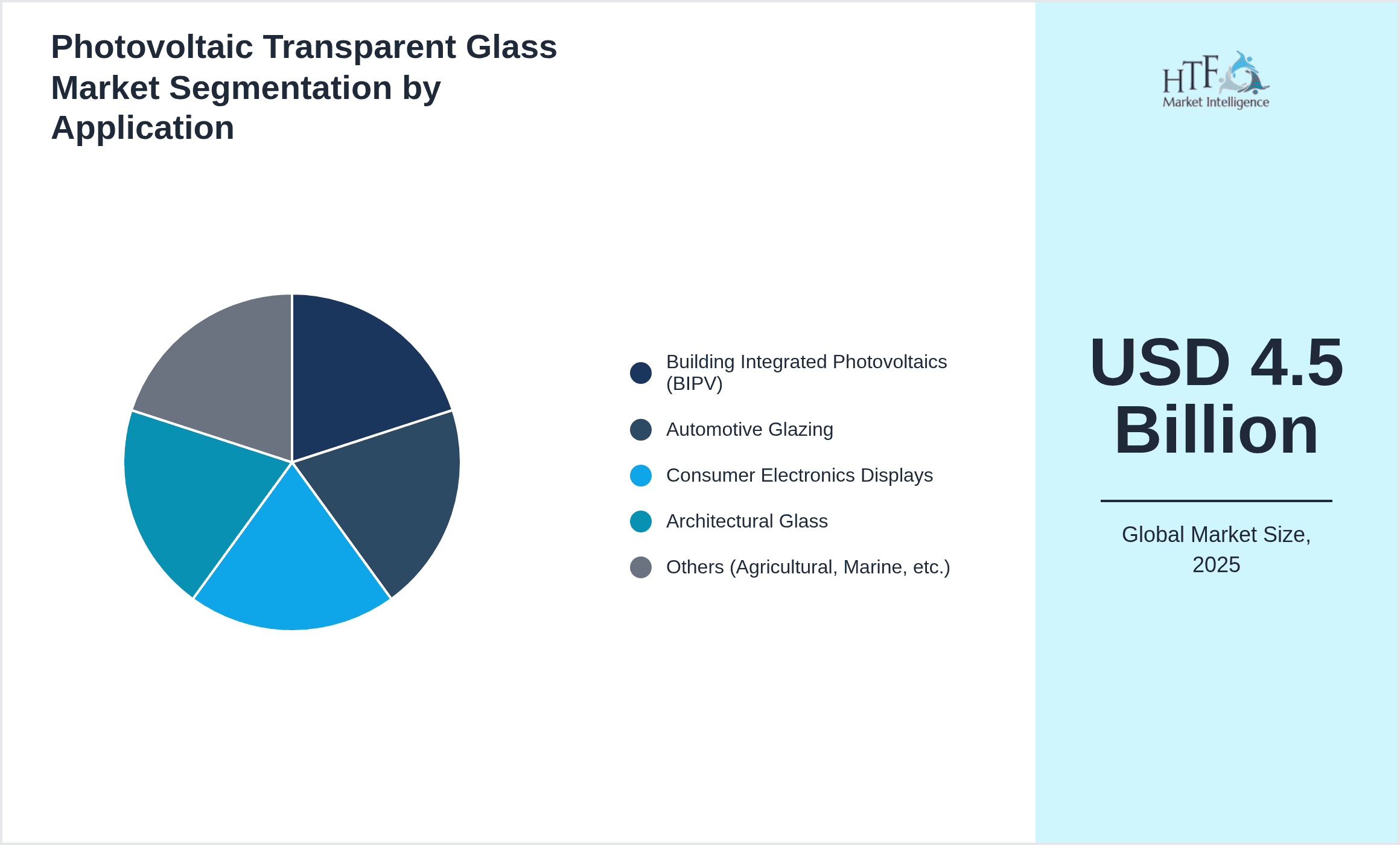

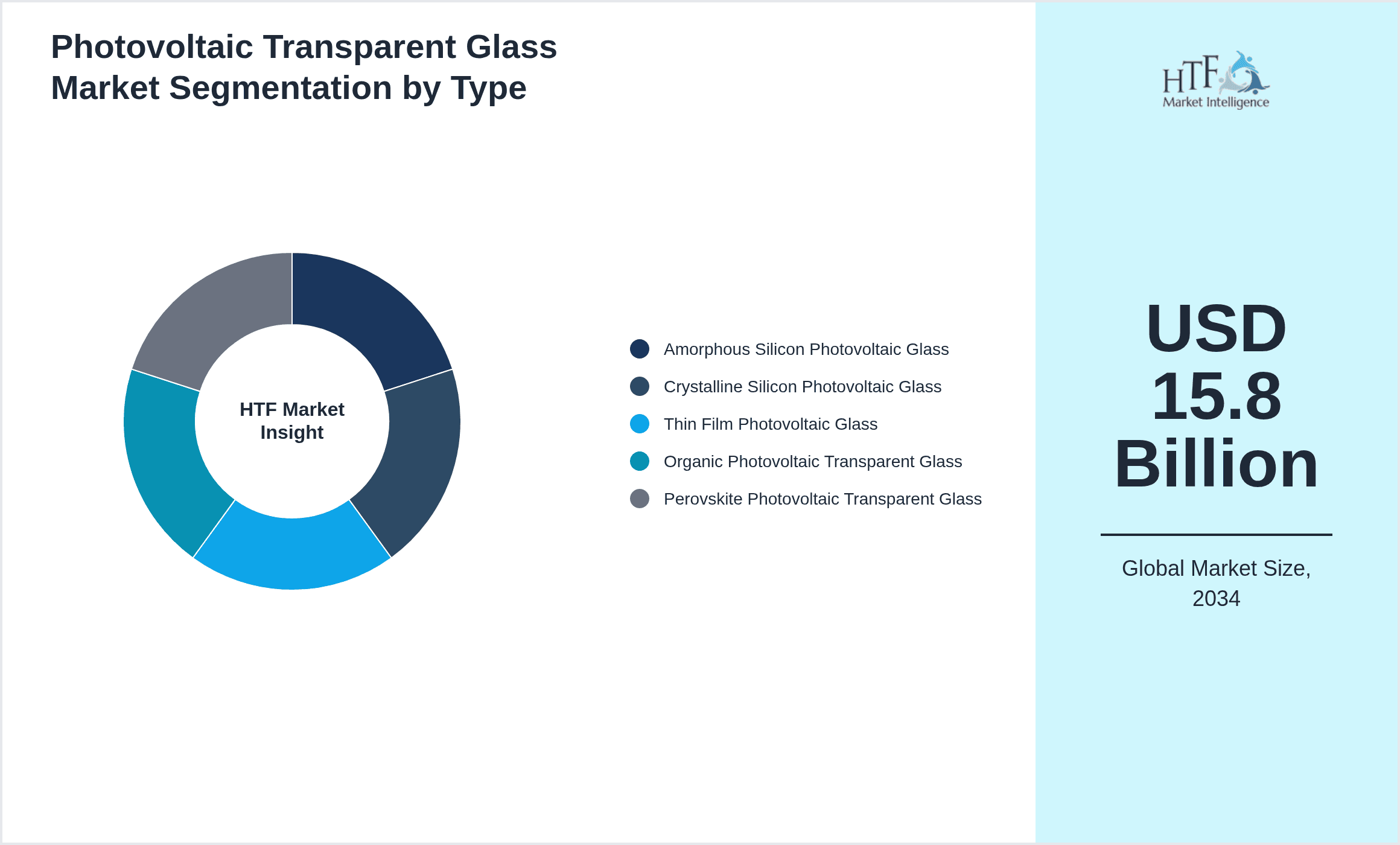

- •Significant market highlights include a robust CAGR of approximately 13.3% expected between 2024 and 2034, driven by escalating investments in green building projects and automotive electrification. The Asia-Pacific region dominates the market share due to large-scale construction and manufacturing activities, while Latin America emerges as the fastest-growing region owing to expanding renewable energy initiatives. Amorphous silicon remains the leading product type by market penetration, benefiting from cost-effectiveness and flexibility, whereas thin-film technology exhibits the highest growth rate due to superior design adaptability and efficiency improvements. Applications in building-integrated photovoltaics continue to lead revenue generation, followed closely by automotive glazing, reflecting the industry's strategic focus on sustainable infrastructure and eco-friendly transportation solutions. These dynamics collectively underscore the market’s promising trajectory and its critical role in global renewable energy deployment.

- •The value proposition of photovoltaic transparent glass lies in its dual functionality of energy generation and transparency, enabling architects, automotive designers, and electronics manufacturers to integrate solar power without compromising aesthetics or usability. This innovation supports environmental sustainability by reducing reliance on fossil fuels and lowering greenhouse gas emissions. Stakeholders including glass manufacturers, technology innovators, construction firms, and government bodies benefit from the expanding market through enhanced energy efficiency standards, cost savings, and compliance with regulatory frameworks. Strategic importance is further highlighted by growing consumer awareness and demand for green buildings and smart technologies, positioning photovoltaic transparent glass as a cornerstone in the transition to a low-carbon economy and resilient urban environments worldwide.

Competitive Landscape

The photovoltaic transparent glass market is characterized by intense competition among multinational corporations and regional manufacturers striving for technological leadership and market share. Companies invest heavily in research and development to enhance photovoltaic efficiency, transparency, and durability while reducing production costs. Innovation strategies include developing novel thin-film materials, integrating nanotechnology, and improving manufacturing scalability. Rivalry is also influenced by strategic partnerships, joint ventures, and acquisitions aimed at expanding product portfolios and geographic reach. Market positioning often hinges on product differentiation through customization and compliance with environmental standards. Distribution channels are optimized to cater to construction, automotive, and consumer electronics sectors, emphasizing prompt delivery and technical support. Competitive advantages are increasingly gained through sustainable production methods and digitalization of manufacturing, which also serve as barriers to new entrants. The evolving landscape foresees consolidation and collaborative innovation as key trends shaping future competition.

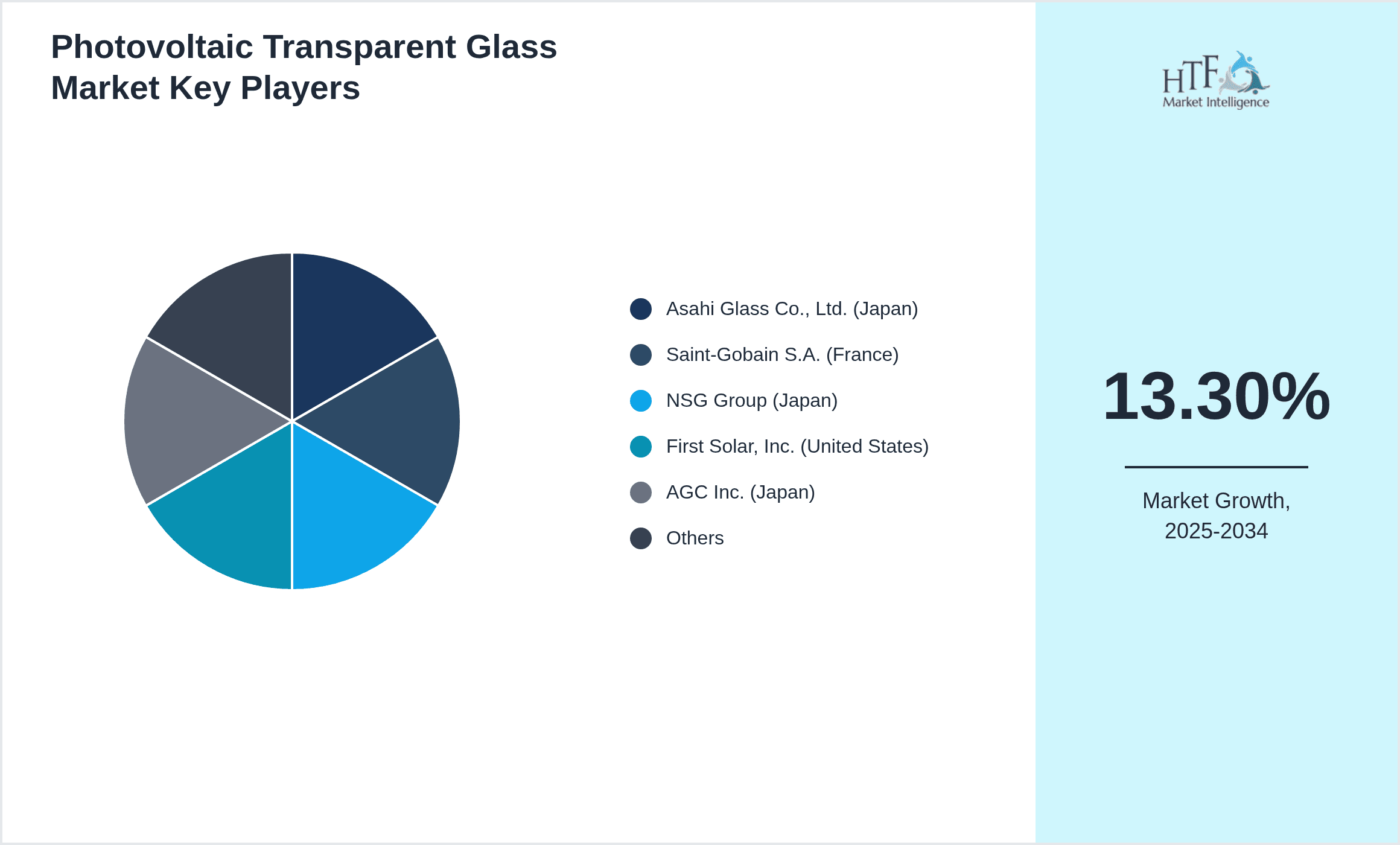

Prominent Players in Photovoltaic Transparent Glass Market

- •Asahi Glass Co., Ltd. (Japan)

- •Saint-Gobain S.A. (France)

- •NSG Group (Japan)

- •First Solar, Inc. (United States)

- •AGC Inc. (Japan)

- •SolarWindow Technologies, Inc. (United States)

- •Ubiquitous Energy, Inc. (United States)

- •Heliatek GmbH (Germany)

- •Onyx Solar Energy S.L. (Spain)

- •Pythagoras Solar (Turkey)

- •SageGlass (United States)

- •GlassX (South Korea)

- •Sunpartner Technologies (France)

- •Polysolar Ltd. (United Kingdom)

- •Heliospectra AB (Sweden)

- •BayWa r.e. renewable energy GmbH (Germany)

- •Heraeus Holding GmbH (Germany)

- •Saint-Gobain Solar (France)

- •Nippon Sheet Glass Co., Ltd. (Japan)

- •SolarWindow Technologies (United States)

- •ClearVue Technologies Limited (Australia)

- •Phononic Vitrification (United States)

- •SunPower Corporation (United States)

- •Heliatek GmbH (Germany)

- •Ubiquitous Energy, Inc. (United States)

Market Breakdown

- •By Type

- ◦Amorphous Silicon Photovoltaic Glass

- ◦Crystalline Silicon Photovoltaic Glass

- ◦Thin Film Photovoltaic Glass

- ◦Organic Photovoltaic Transparent Glass

- ◦Perovskite Photovoltaic Transparent Glass

- •By Application

- ◦Building Integrated Photovoltaics (BIPV)

- ◦Automotive Glazing

- ◦Consumer Electronics Displays

- ◦Architectural Glass

- ◦Others (Agricultural, Marine, etc.)

- •By End-Use Sector

- ◦Residential Buildings

- ◦Commercial Buildings

- ◦Industrial Facilities

- ◦Transportation

- •By Deployment Model

- ◦New Construction Integration

- ◦Retrofit Installations

Growth Dynamics

- •Rising demand for sustainable construction materials and the increasing adoption of green building codes worldwide are propelling the growth of photovoltaic transparent glass, enabling architects and developers to integrate energy harvesting within building envelopes effectively.

- •Technological advancements in thin-film and organic photovoltaic materials improve the transparency and efficiency of solar glass, encouraging wider application in automotive and consumer electronics sectors, thereby expanding market reach.

- •Government incentives and regulatory frameworks promoting renewable energy adoption and carbon emission reductions create a favorable environment for photovoltaic transparent glass market expansion, especially in regions focusing on climate goals.

- •Increasing urbanization and demand for smart cities stimulate investments in energy-efficient infrastructure, positioning photovoltaic transparent glass as a vital component for integrating renewable energy in urban environments.

- •Growing environmental awareness and consumer preference for eco-friendly products drive manufacturers and end-users to adopt photovoltaic transparent glass across multiple applications, fostering sustainable industry growth.

Market Trends

- •Integration of photovoltaic transparent glass with smart window technologies featuring adjustable tinting and energy management systems is gaining traction, enhancing user comfort and energy savings in commercial and residential buildings.

- •Collaborations between glass manufacturers and solar technology firms are accelerating innovation pipelines, resulting in novel product offerings with improved efficiency and durability tailored for specific market segments.

- •The advent of perovskite-based transparent photovoltaic glass promises higher power conversion efficiencies and flexibility, marking a disruptive innovation set to reshape market dynamics over the next decade.

- •Sustainability-focused certifications and green building rating systems increasingly recognize photovoltaic transparent glass installations, boosting market adoption through enhanced project valuation and compliance incentives.

- •Regional market players are expanding manufacturing capacities in Asia-Pacific and Latin America to capitalize on growing demand and favorable manufacturing ecosystems, influencing global supply chain configurations.

Market Opportunities

- •Emerging markets in Latin America and the Middle East & Africa present significant growth opportunities due to rising investments in renewable infrastructure and favorable government policies targeting energy security and sustainability.

- •Innovations in flexible and ultra-thin photovoltaic transparent glass open new application avenues in automotive sunroofs, wearable electronics, and portable devices, expanding the market scope beyond traditional construction uses.

- •Strategic partnerships between technology developers and glass manufacturers can accelerate commercialization of advanced photovoltaic glass products, reducing time-to-market and enhancing competitive positioning.

- •Increasing retrofit projects in developed regions aiming to improve energy efficiency in existing buildings provide lucrative opportunities for photovoltaic transparent glass providers offering customized solutions.

- •Government subsidies and green financing initiatives for sustainable construction and energy projects worldwide incentivize investments and adoption of photovoltaic transparent glass solutions across multiple sectors.

Market Challenges

- •High initial investment costs and longer payback periods associated with photovoltaic transparent glass installations hinder widespread adoption, especially among price-sensitive segments and developing economies.

- •Technical challenges related to balancing transparency with photovoltaic efficiency limit product performance and design options, necessitating ongoing research and development efforts.

- •Fragmented regulatory frameworks and varying standards across regions complicate market entry and compliance for manufacturers aiming for global expansion.

- •Limited consumer awareness about photovoltaic transparent glass benefits restricts market penetration, particularly in residential and small commercial sectors.

- •Supply chain disruptions and raw material price volatility pose risks to production continuity and cost management, impacting market stability.

Regulatory Framework

- •Between 2020 and 2024, multiple regions have introduced stringent building codes mandating energy efficiency standards that include the use of photovoltaic transparent glass, encouraging its integration in new constructions and renovations.

- •The European Union’s Renewable Energy Directive and the U.S. Energy Policy Act have established compliance requirements and incentives that directly impact the photovoltaic transparent glass market by promoting solar energy utilization.

- •Safety and environmental standards for glass manufacturing, such as the ISO 14001 environmental management system, have been enforced globally, affecting production processes and product certification.

- •Countries in Asia-Pacific have implemented subsidies and tax benefits specifically targeting the adoption of building-integrated photovoltaics, bolstering demand for photovoltaic transparent glass products.

- •Recent updates in fire safety regulations and glazing standards necessitate rigorous testing and certification of photovoltaic transparent glass, ensuring market compliance and consumer safety.

Market Intelligence

- •15th January 2025, Asahi Glass Co., Ltd. unveiled its latest photovoltaic transparent glass product featuring enhanced thin-film solar cells with 20% improved efficiency and increased transparency, designed for integration in high-rise buildings. The innovation aims to meet growing demand for energy-efficient construction materials in urban centers, providing architects with versatile design options without compromising on aesthetic appeal. This launch positions Asahi Glass as a technological leader, reinforcing its market presence in Asia-Pacific and Europe. Source: Company Press Release

- •28th March 2025, Saint-Gobain S.A. announced a strategic partnership with SolarWindow Technologies to co-develop organic photovoltaic transparent glass tailored for automotive applications. This collaboration combines Saint-Gobain's expertise in glass manufacturing with SolarWindow's cutting-edge solar technology, targeting the expanding electric vehicle market. The joint initiative focuses on producing lightweight, flexible solar glass that enhances energy efficiency and vehicle range, aiming for commercial availability by late 2026. Source: Industry Publication

- •12th July 2025, Ubiquitous Energy, Inc. revealed a breakthrough in transparent photovoltaic coating technology that increases power conversion efficiency by 15% while maintaining color neutrality. This advancement is expected to accelerate market adoption in consumer electronics and architectural sectors by enabling seamless integration of solar energy harvesting surfaces. The company plans to license the technology to global glass manufacturers by 2026, expanding its commercial footprint. Source: Official Company Announcement

- •3rd October 2025, First Solar, Inc. completed the acquisition of Pythagoras Solar to strengthen its portfolio in building-integrated photovoltaic solutions. The acquisition enhances First Solar’s capabilities in transparent solar glass manufacturing and expands its market reach into Europe and Asia. This strategic move is aligned with the company’s growth plan focused on sustainable urban infrastructure projects and renewable energy integration. Source: Corporate News Release

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 15.8 Billion |

| CAGR | 13.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.7% |

| Scope of Report | Market is segmented by Type (Amorphous Silicon Photovoltaic Glass, Crystalline Silicon Photovoltaic Glass, Thin Film Photovoltaic Glass, Organic Photovoltaic Transparent Glass, Perovskite Photovoltaic Transparent Glass), Application (Building Integrated Photovoltaics (BIPV), Automotive Glazing, Consumer Electronics Displays, Architectural Glass, Others (Agricultural, Marine, etc.)), End-Use Sector (Residential Buildings, Commercial Buildings, Industrial Facilities, Transportation), Deployment Model (New Construction Integration, Retrofit Installations) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Asahi Glass Co., Ltd. (Japan), Saint-Gobain S.A. (France), NSG Group (Japan), First Solar, Inc. (United States), AGC Inc. (Japan), SolarWindow Technologies, Inc. (United States), Ubiquitous Energy, Inc. (United States), Heliatek GmbH (Germany), Onyx Solar Energy S.L. (Spain), Pythagoras Solar (Turkey), SageGlass (United States), GlassX (South Korea), Sunpartner Technologies (France), Polysolar Ltd. (United Kingdom), Heliospectra AB (Sweden), BayWa r.e. renewable energy GmbH (Germany), Heraeus Holding GmbH (Germany), Saint-Gobain Solar (France), Nippon Sheet Glass Co., Ltd. (Japan), SolarWindow Technologies (United States), ClearVue Technologies Limited (Australia), Phononic Vitrification (United States), SunPower Corporation (United States), Heliatek GmbH (Germany), Ubiquitous Energy, Inc. (United States) |

Global Photovoltaic Transparent Glass Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.