Europe Films Surgical Anti-Adhesion Product Market Roadmap to 2034

Europe Films Surgical Anti-Adhesion Product Market is segmented by Type (Polymeric Films, Composite Films, Bioabsorbable Films, Hydrogel Films, Others), Application (General Surgery, Gynecology, Orthopedic Surgery, Cardiovascular Surgery, Urology), End-User Healthcare Facility (Hospitals, Specialty Surgical Centers, Ambulatory Surgical Centers, Clinics), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Films Surgical Anti-Adhesion Product Market refers to the segment of medical devices that manufacture and supply specialized films used as physical barriers during surgeries to prevent the formation of internal adhesions. Adhesions are fibrous bands that develop postoperatively between tissues or organs and can lead to complications such as chronic pain, infertility, or bowel obstruction. This market includes a range of film types, including polymeric, bioabsorbable, composite, and hydrogel films, each engineered to enhance biocompatibility and facilitate safe absorption or removal after the healing process. The products serve multiple surgical applications such as general surgery, gynecology, orthopedic surgery, cardiovascular surgery, and urology. The market scope covers product innovation, regulatory compliance, and distribution across Europe's healthcare infrastructure, focusing on countries like Germany, France, the UK, and others. Increasing surgical procedures, growing awareness about adhesion prevention, and technological advancements in biomaterials drive market growth. The demand is further bolstered by an aging population and rising prevalence of chronic diseases requiring surgery in Europe.

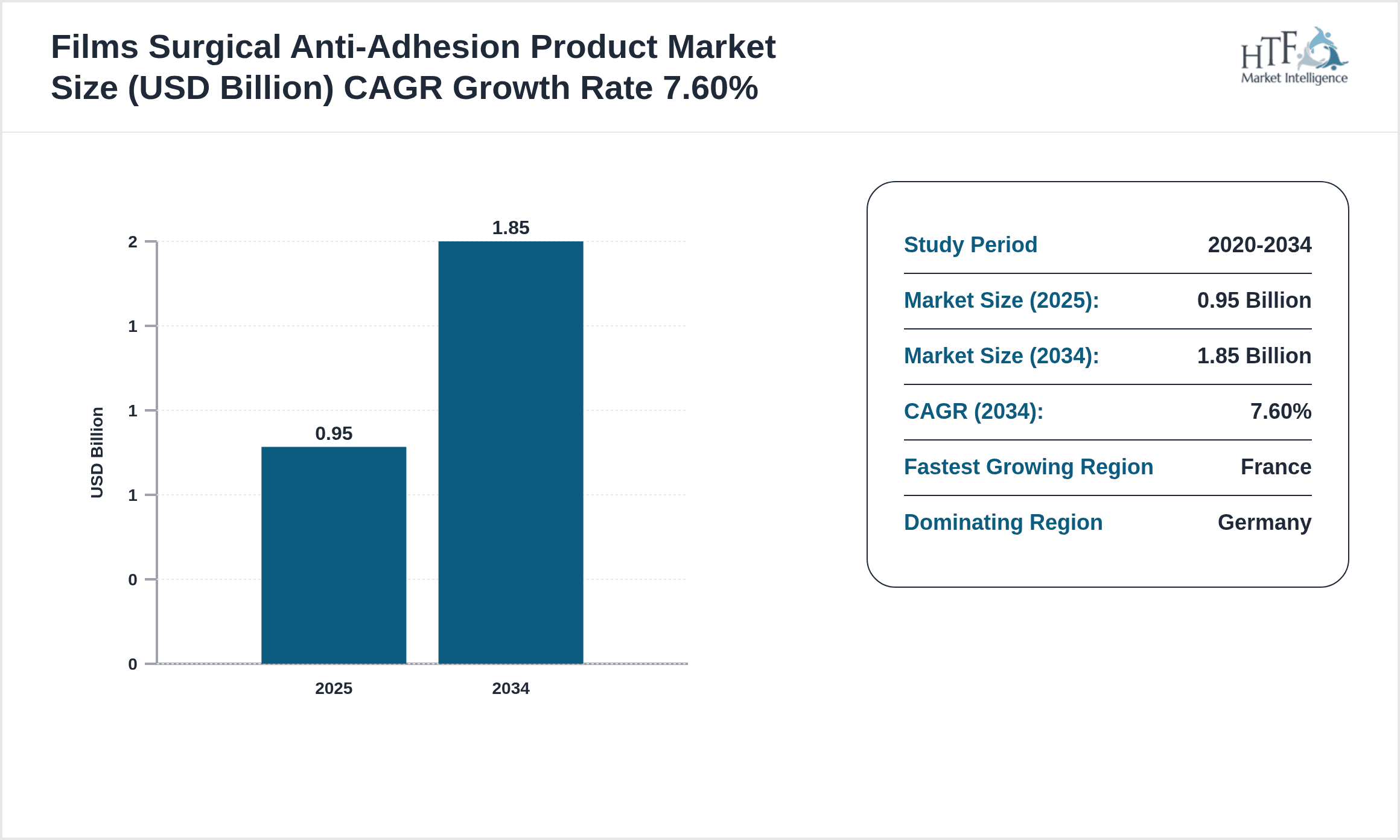

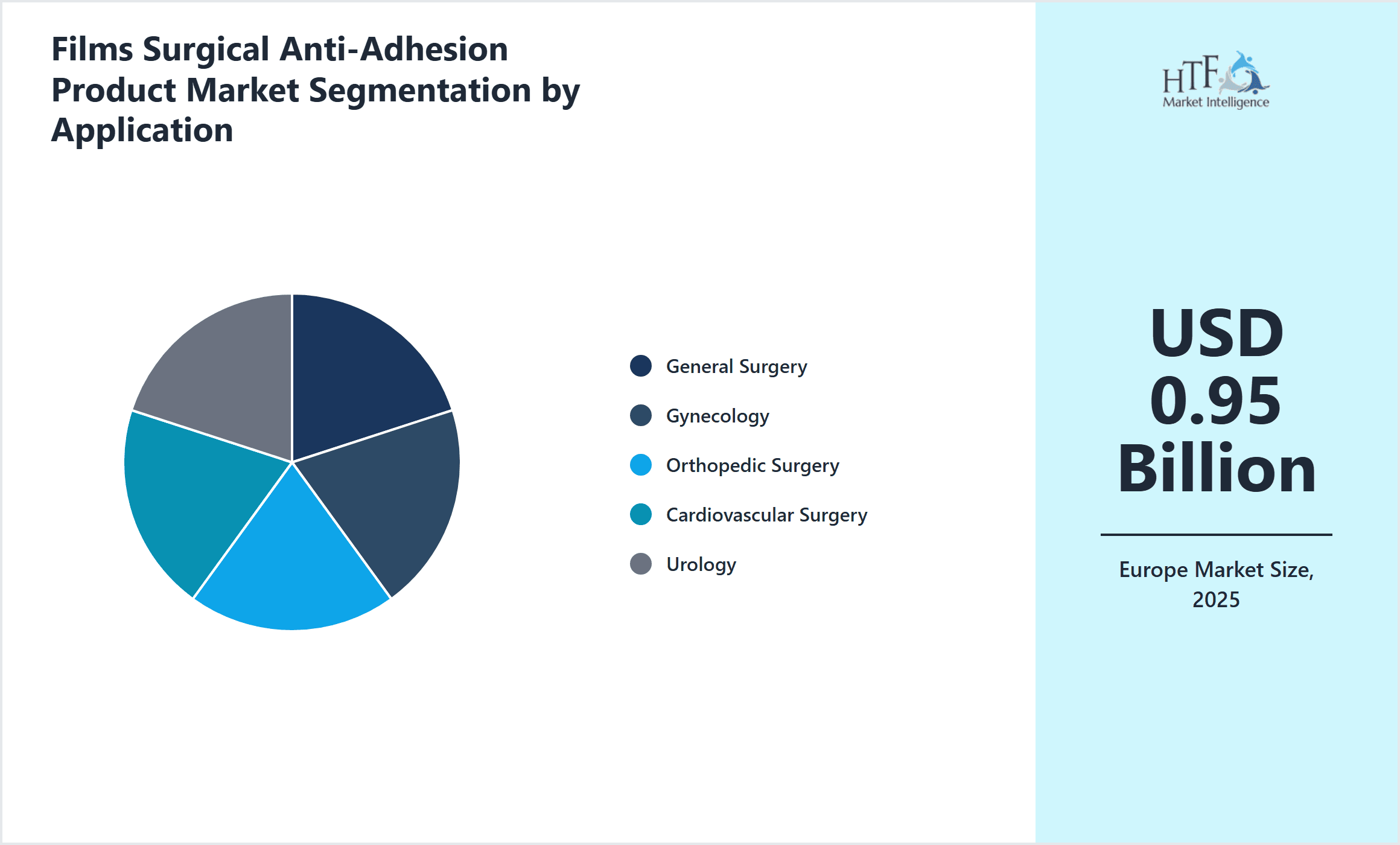

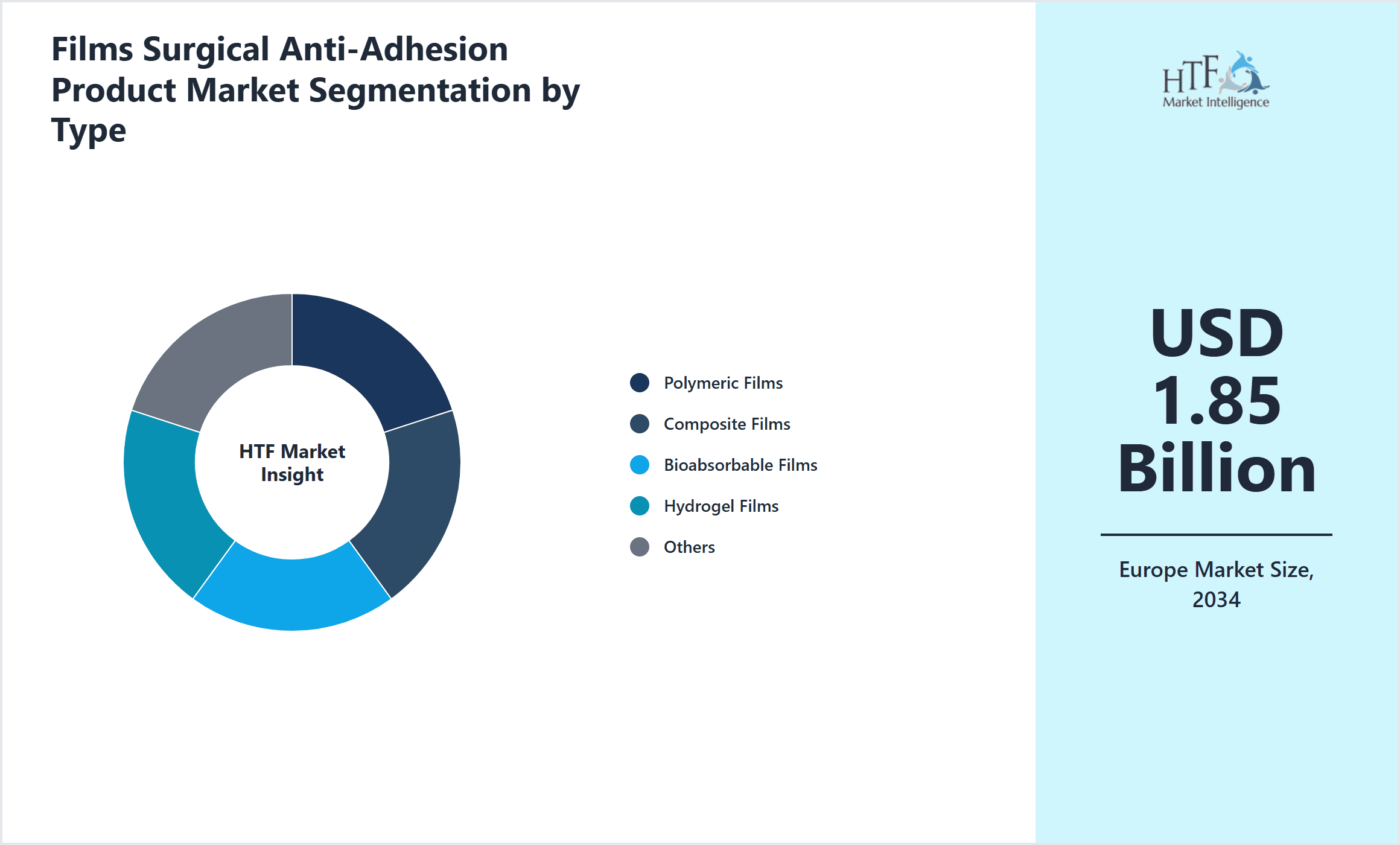

- •Key market highlights include a base market size of USD 0.95 Billion in 2025, projected to reach USD 1.85 Billion by 2034, reflecting a CAGR of 7.6%. Bioabsorbable films dominate the product type segment due to their favorable absorption profile and biocompatibility, while composite films are witnessing the fastest growth fueled by their multifunctional properties. General surgery remains the leading application segment, supported by high procedural volumes, with gynecology following closely. Germany leads the regional market share due to its advanced healthcare infrastructure, and France emerges as the fastest-growing country driven by increasing hospital investments and procedural innovations. Year-over-year growth of approximately 7.2% underscores robust market dynamics amid evolving surgical protocols.

- •The Europe Films Surgical Anti-Adhesion Product Market offers significant value propositions for healthcare providers and manufacturers by improving post-surgical outcomes and reducing healthcare costs associated with adhesion-related complications. For surgical device companies, this market represents a strategic opportunity to innovate biomaterials and expand their product portfolio aligned with regulatory standards. The increasing focus on minimally invasive surgical techniques further enhances the adoption of anti-adhesion films as critical adjuncts. Stakeholders benefit from expanding reimbursement frameworks and growing awareness among surgeons regarding adhesion prevention. Overall, the market’s strategic importance is anchored in advancing patient care quality and supporting healthcare sustainability across diverse European healthcare systems.

Competitive Landscape

The Europe Films Surgical Anti-Adhesion Product Market is characterized by intense competition driven by innovation, technology adoption, and strategic partnerships. Leading players focus on developing advanced bioabsorbable and composite films that offer superior biocompatibility and ease of use, differentiating their products through proprietary materials and patented technologies. The market exhibits moderate concentration with key multinational corporations holding significant shares, yet regional players contribute through niche product offerings and localized distribution. Companies pursue competitive strategies including mergers and acquisitions, collaborations with healthcare providers, and investment in R&D to expand their product pipelines. Pricing strategies remain competitive due to reimbursement considerations and cost pressures within European healthcare systems. Distribution channels are evolving with digital procurement and direct hospital partnerships gaining traction. Furthermore, regulatory compliance and certification processes act as barriers to entry, fostering a competitive environment focused on quality and innovation. Future trends suggest increasing emphasis on sustainability and multifunctional film properties to maintain competitive advantage.

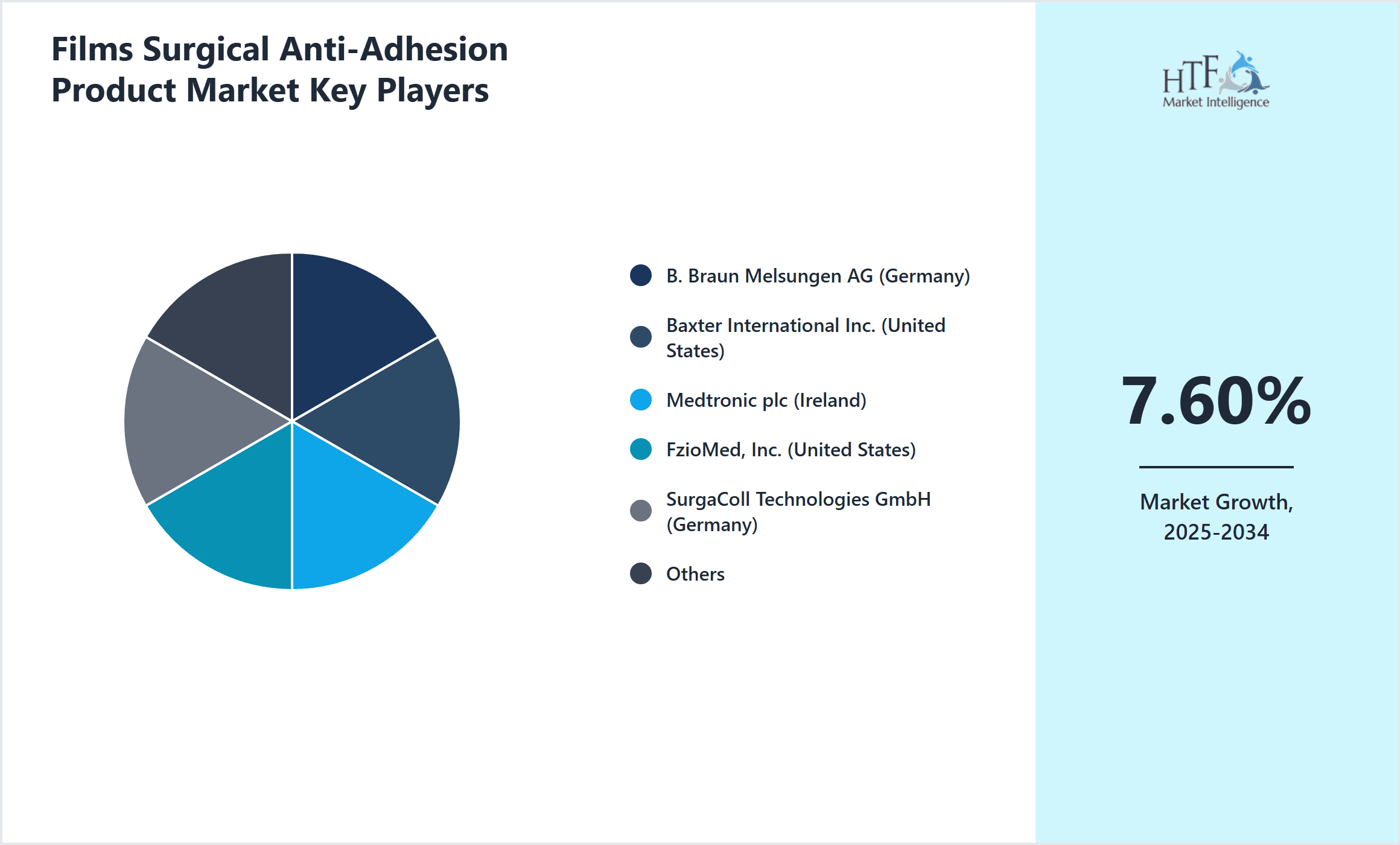

Prominent Players in Europe Films Surgical Anti-Adhesion Product Market

- •B. Braun Melsungen AG (Germany)

- •Baxter International Inc. (United States)

- •Medtronic plc (Ireland)

- •FzioMed, Inc. (United States)

- •SurgaColl Technologies GmbH (Germany)

- •Kensey Nash Corporation (United States)

- •United States Surgical Corporation (United States)

- •Axogen, Inc. (United States)

- •Cygnus Medical (United States)

- •SurgiMend (United Kingdom)

- •Integra LifeSciences Holdings Corporation (United States)

- •Tissue Science Laboratories (United Kingdom)

- •Ethicon Inc. (United States)

- •Sekisui Chemical Co., Ltd. (Japan)

- •Hollister Incorporated (United States)

- •Baxano Surgical Inc. (United States)

- •Genzyme Corporation (United States)

- •Aesculap AG (Germany)

- •Polyganics BV (Netherlands)

- •SurgiTel (United States)

- •Biocomposites Ltd. (United Kingdom)

- •Cytograft Tissue Engineering, Inc. (United States)

- •Microtek Medical, Inc. (United States)

- •Johnson & Johnson (United States)

- •Bionova Medical Technologies (United Kingdom)

Market Breakdown

- •By Type

- ◦Polymeric Films

- ◦Composite Films

- ◦Bioabsorbable Films

- ◦Hydrogel Films

- ◦Others

- •By Application

- ◦General Surgery

- ◦Gynecology

- ◦Orthopedic Surgery

- ◦Cardiovascular Surgery

- ◦Urology

- •By End-User Healthcare Facility

- ◦Hospitals

- ◦Specialty Surgical Centers

- ◦Ambulatory Surgical Centers

- ◦Clinics

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Increasing incidence of chronic diseases and surgical interventions in Europe significantly drives demand for surgical anti-adhesion films. With rising awareness among surgeons regarding adhesion-related complications, adoption of advanced bioabsorbable films is increasing, fostering market growth.

- •Technological innovations including development of composite films with multifunctional properties such as drug delivery and enhanced biodegradability provide competitive advantages, encouraging manufacturers to invest more in R&D and product differentiation.

- •Expanding healthcare infrastructure and rising number of minimally invasive surgeries across countries like Germany, France, and the UK contribute to increasing utilization of surgical anti-adhesion films, accelerating market expansion.

- •Favorable reimbursement policies and regulatory approvals in major European markets enable easier market access and adoption by healthcare providers, acting as a catalyst for growth.

- •Growing collaborations between medical device companies and healthcare institutions to develop customized anti-adhesion solutions further stimulate growth opportunities within the market.

Market Trends

- •The integration of nanotechnology into surgical anti-adhesion films is gaining traction, enabling improved film properties such as enhanced tissue adhesion prevention and controlled biodegradation, impacting product innovation trends.

- •Increasing preference for bioabsorbable films over synthetic non-absorbable films reflects a shift towards products that reduce the need for secondary surgeries, aligning with patient-centric care approaches in Europe.

- •Surgical anti-adhesion films embedded with bioactive agents to reduce inflammation and promote healing are emerging as a key trend, with several companies investing in clinical trials to validate efficacy.

- •Sustainability considerations are influencing material selection, with manufacturers exploring eco-friendly biomaterials and reducing hazardous waste in production processes.

- •Digitization of supply chains and adoption of e-commerce platforms for medical device procurement are enhancing distribution efficiency and market reach in the European region.

Market Opportunities

- •Emerging markets within Eastern Europe present untapped potential due to growing healthcare expenditure and increasing surgical volumes, offering expansion opportunities for market participants.

- •Development of multifunctional films combining adhesion prevention with antimicrobial properties addresses unmet clinical needs, creating avenues for product innovation and differentiation.

- •Strategic partnerships between biomaterial innovators and surgical device manufacturers can accelerate time-to-market for novel anti-adhesion products, enhancing competitive positioning.

- •Government initiatives supporting minimally invasive surgeries and improved post-operative care provide a favorable environment for adoption of advanced adhesion prevention films.

- •Customization of films for specific surgical procedures and patient populations can enhance clinical outcomes and offer targeted solutions, fostering market growth.

Market Challenges

- •High manufacturing costs of advanced bioabsorbable and composite films limit price competitiveness, restricting adoption in cost-sensitive healthcare settings across Europe.

- •Stringent regulatory requirements and lengthy approval processes delay product launches, increasing time-to-market and development expenses for manufacturers.

- •Limited surgeon awareness and training on the optimal usage of surgical anti-adhesion films can impede market penetration and uptake in certain European countries.

- •Competition from alternative adhesion prevention methods such as gels and sprays challenges the dominance of film-based products, necessitating continuous innovation.

- •Supply chain disruptions and raw material shortages, exacerbated by geopolitical factors, impact consistent product availability and pricing stability.

Regulatory Framework

- •Between 2020 and 2025, the European Union Medical Device Regulation (EU MDR 2017/745) came into full effect, imposing rigorous requirements for product safety, clinical evaluation, and post-market surveillance on surgical anti-adhesion films, ensuring higher standards and market transparency.

- •The In Vitro Diagnostic Regulation (IVDR) 2017/746, while primarily focused on diagnostics, influences related surgical products requiring companion diagnostics, enhancing regulatory oversight and compliance needs.

- •Country-specific regulatory adaptations in Germany, France, and the UK have introduced additional compliance layers, including national health technology assessments and reimbursement policy updates impacting market access.

- •Environmental regulations targeting sustainable manufacturing and waste management have encouraged manufacturers to innovate eco-friendly production methods and materials within Europe.

- •Governmental support programs offering incentives for medical device innovation and clinical research have facilitated market entry for new surgical anti-adhesion products across the region.

Market Intelligence

- •15th February 2025, B. Braun Melsungen AG launched a next-generation bioabsorbable anti-adhesion film featuring enhanced tissue compatibility and accelerated biodegradation. This product targets gynecological and general surgeries, aiming to reduce post-operative adhesion rates and improve patient recovery times. The launch represents a strategic move to consolidate B. Braun’s leadership in Europe by addressing unmet clinical needs with innovative biomaterials and streamlined application techniques. The product is expected to expand B. Braun’s market share through hospital partnerships and clinical endorsements.

- •30th April 2025, Medtronic plc introduced a composite surgical film integrating antimicrobial agents designed to prevent infections alongside adhesion formation in cardiovascular and orthopedic surgeries. This innovation leverages advanced polymer technology to provide dual-functionality, enhancing surgical outcomes and reducing complications. Medtronic’s launch reinforces its commitment to surgical innovation and aligns with European hospitals’ increasing demand for multifunctional medical devices. The product rollout includes comprehensive surgeon training programs and market education initiatives.

- •10th August 2024, Baxter International Inc. announced a strategic partnership with Polyganics BV to co-develop a new line of hydrogel-based anti-adhesion films with improved elasticity and absorption rates. This collaboration aims to leverage Polyganics’ biomaterial expertise and Baxter’s extensive European distribution network to accelerate commercialization. The partnership supports Baxter’s growth strategy in Europe and is anticipated to enhance product portfolio diversity and address evolving surgical needs.

- •22nd November 2024, Kensey Nash Corporation completed the acquisition of SurgiColl Technologies GmbH, expanding its presence in the European surgical anti-adhesion film market. The deal combines Kensey Nash’s polymer innovation capabilities with SurgiColl’s strong regional sales and clinical footprint, enabling rapid market penetration. The acquisition aligns with both companies’ goals of enhancing product offerings and achieving operational synergies in Europe’s competitive landscape.

- •Source: Official company press releases, industry publications

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.95 Billion |

| Forecast Year Market Size | USD 1.85 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.2% |

| Scope of Report | Market is segmented by Type (Polymeric Films, Composite Films, Bioabsorbable Films, Hydrogel Films, Others), Application (General Surgery, Gynecology, Orthopedic Surgery, Cardiovascular Surgery, Urology), End-User Healthcare Facility (Hospitals, Specialty Surgical Centers, Ambulatory Surgical Centers, Clinics), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | B. Braun Melsungen AG (Germany), Baxter International Inc. (United States), Medtronic plc (Ireland), FzioMed, Inc. (United States), SurgaColl Technologies GmbH (Germany), Kensey Nash Corporation (United States), United States Surgical Corporation (United States), Axogen, Inc. (United States), Cygnus Medical (United States), SurgiMend (United Kingdom), Integra LifeSciences Holdings Corporation (United States), Tissue Science Laboratories (United Kingdom), Ethicon Inc. (United States), Sekisui Chemical Co., Ltd. (Japan), Hollister Incorporated (United States), Baxano Surgical Inc. (United States), Genzyme Corporation (United States), Aesculap AG (Germany), Polyganics BV (Netherlands), SurgiTel (United States), Biocomposites Ltd. (United Kingdom), Cytograft Tissue Engineering, Inc. (United States), Microtek Medical, Inc. (United States), Johnson & Johnson (United States), Bionova Medical Technologies (United Kingdom) |

Europe Films Surgical Anti-Adhesion Product Market Roadmap to 2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.