Global Medical Waste Disposal & Management Market Size, Growth & Revenue 2024-2034

Global Medical Waste Disposal & Management Market is segmented by Medical Waste Type (Infectious Waste, Sharps Waste, Chemical Waste, Pharmaceutical Waste, General Medical Waste), Application (Hospitals, Clinics, Diagnostic Laboratories, Research Institutions, Pharmaceutical Industry), Treatment Technology (Incineration, Autoclaving, Chemical Disinfection, Microwave Treatment, Landfilling), Service Type (Collection & Transportation, Waste Treatment & Disposal, Recycling & Resource Recovery, Consulting & Compliance Management), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Medical Waste Disposal & Management Market is a critical segment of the healthcare ecosystem, focusing on the safe, effective, and environmentally responsible handling of medical waste generated by hospitals, clinics, diagnostic laboratories, research institutions, and pharmaceutical industries. This market covers a broad spectrum of waste types, including infectious waste, sharps, chemical waste, pharmaceutical waste, and general medical refuse. It encompasses numerous technologies and services such as autoclaving, incineration, chemical treatment, and innovative waste minimization techniques designed to mitigate environmental impact and ensure regulatory compliance worldwide. Increasing global healthcare infrastructure, rising disease incidence, and growing awareness of health and environmental risks associated with improper disposal drive demand. The market is further influenced by stringent regulations enforced by health and environmental agencies, encouraging adoption of advanced and sustainable disposal technologies. This sector plays a vital role in protecting public health, preventing contamination, and supporting sustainable healthcare growth globally, positioning it as a strategic priority for governments and private stakeholders alike.

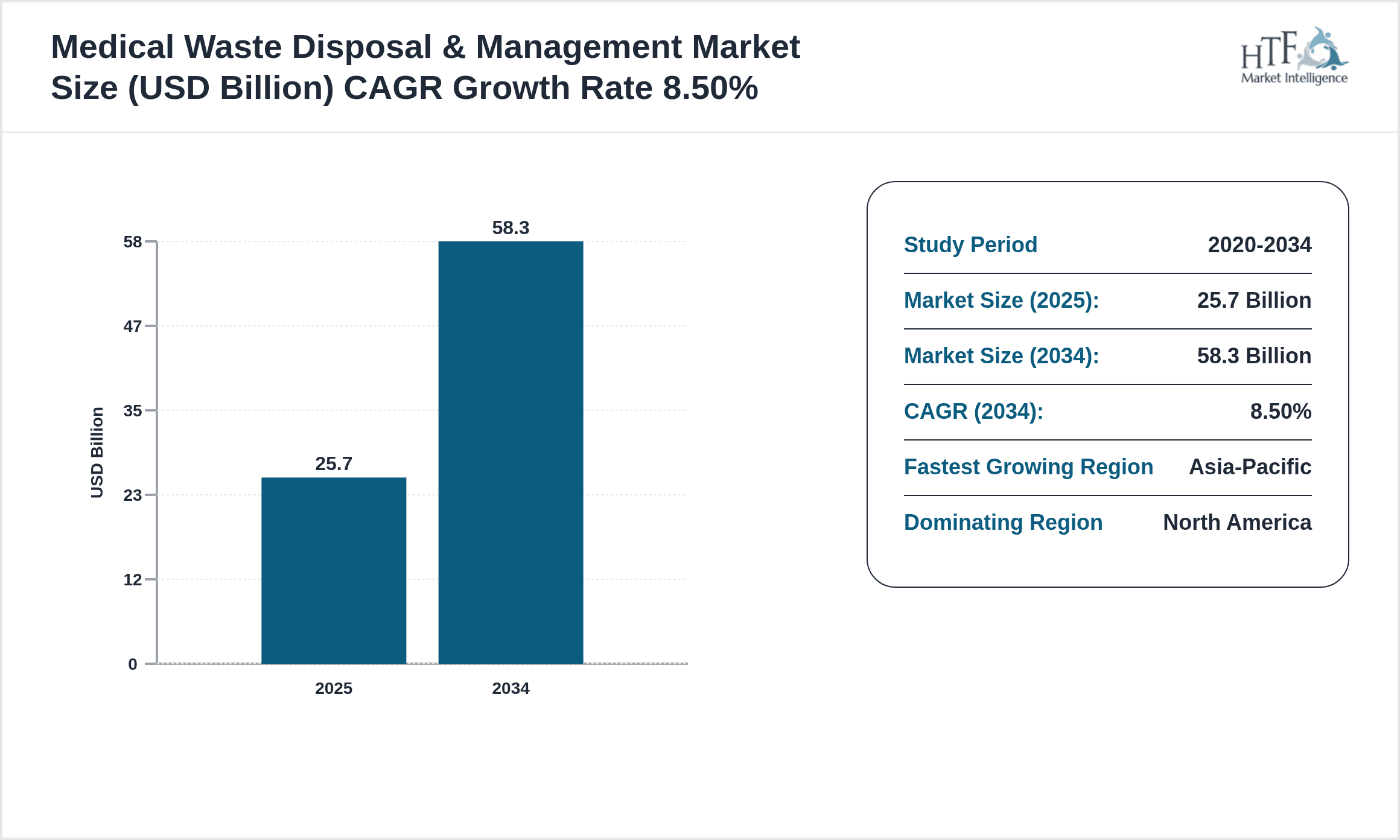

- •Market highlights reveal steady growth with a base market size of USD 25.7 Billion in 2024, anticipated to reach USD 58.3 Billion by 2034, reflecting a robust CAGR of 8.5%. North America dominates the market due to advanced healthcare infrastructure and stringent regulatory frameworks, while Asia-Pacific is the fastest growing region propelled by expanding healthcare facilities and rising awareness. Infectious waste remains the leading product segment, driven by high volumes generated in clinical settings, whereas chemical waste is the fastest growing type due to increasing pharmaceutical and laboratory waste concerns. The hospital application segment holds the largest share, supported by consistent waste generation and regulatory mandates. These growth indicators underscore the increasing prioritization of medical waste management solutions globally, aligning with environmental sustainability goals and public health safety imperatives.

- •The market’s value proposition lies in its ability to furnish safe and compliant medical waste disposal solutions that safeguard healthcare personnel, patients, and the environment. It offers strategic importance to healthcare providers, regulatory bodies, waste management companies, and technology developers by addressing complex waste streams through innovative treatment processes and compliance management. The growing emphasis on sustainability, cost efficiency, and operational safety further enhances market relevance, driving investments and partnerships. This market is integral to achieving global health safety standards and environmental protection objectives, offering stakeholders numerous opportunities to leverage technological advancements and expand service offerings in an evolving regulatory landscape.

Competitive Landscape

The competitive landscape of the global Medical Waste Disposal & Management Market is characterized by intense rivalry among established multinational corporations, regional players, and emerging innovators. Market participants employ diverse strategies including technological innovation, acquisitions, strategic partnerships, and geographic expansion to strengthen their market position. Emphasis on developing eco-friendly and cost-effective waste treatment solutions has intensified competition, with companies investing heavily in R&D to comply with evolving regulatory frameworks and meet customer demands. Pricing strategies are influenced by regulatory compliance costs and the need for differentiated service offerings. Distribution channels and service customization further define competitive advantage, as companies strive to provide end-to-end solutions encompassing collection, transportation, treatment, and disposal. Barriers to entry remain moderate due to regulatory complexities and capital requirements, yet new entrants with niche technologies continue to impact market dynamics. The competitive environment is also shaped by regional market variations, with North America and Europe leading in technological adoption and Asia-Pacific emerging as a hotspot for market growth and competition.

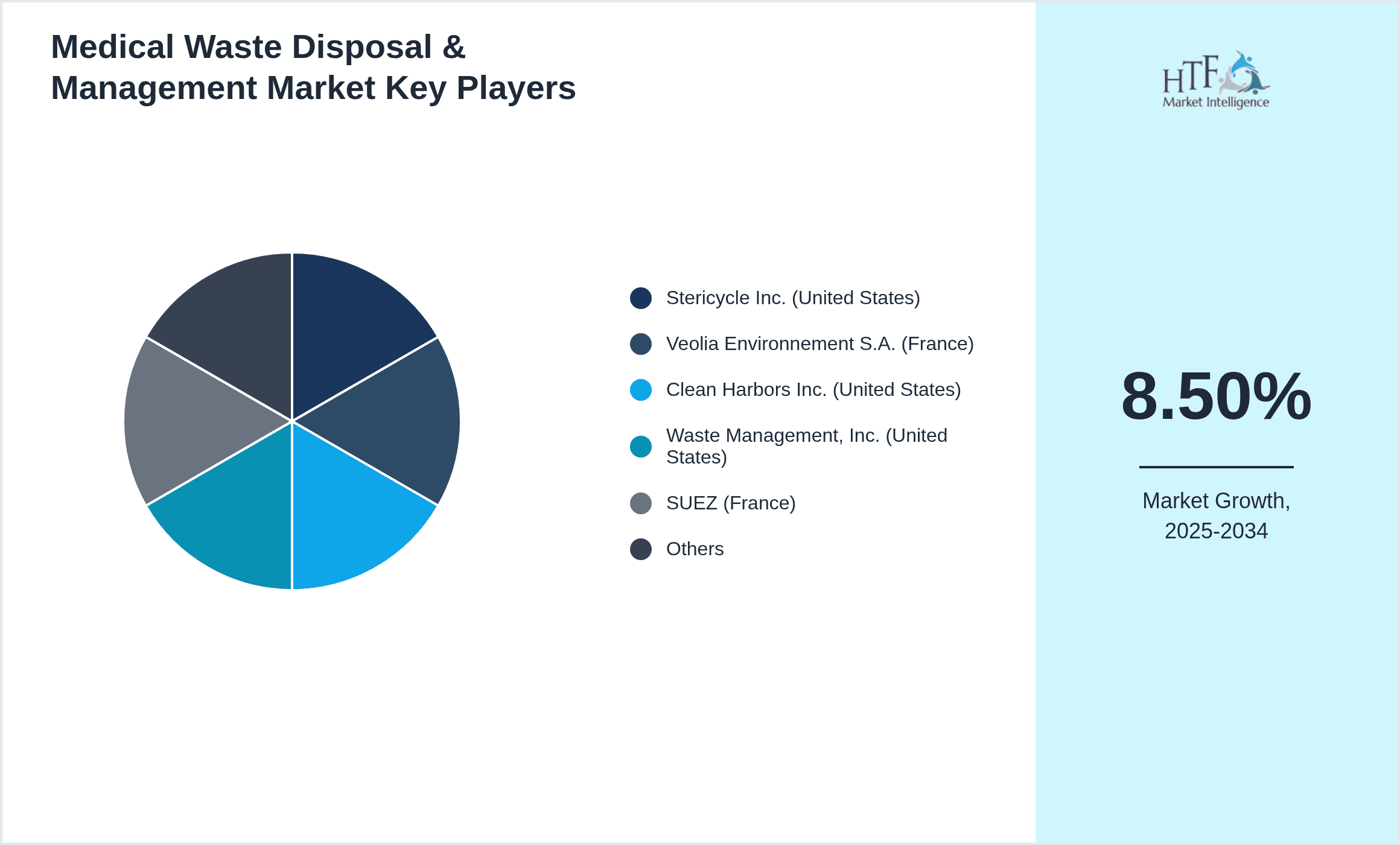

Leading Companies in Medical Waste Disposal & Management Market

- •Stericycle Inc. (United States)

- •Veolia Environnement S.A. (France)

- •Clean Harbors Inc. (United States)

- •Waste Management, Inc. (United States)

- •SUEZ (France)

- •Daniels Health (Australia)

- •MedPro Disposal (United States)

- •Republic Services, Inc. (United States)

- •Sterilex Corporation (United States)

- •Clean Earth, Inc. (United States)

- •Babcock & Wilcox Enterprises, Inc. (United States)

- •Keurig Dr Pepper Inc. (United States)

- •EnviroSolutions LLC (United States)

- •MedWaste Disposal Services (Canada)

- •HealthLink, Inc. (United States)

- •Onyx Environmental Services (United States)

- •Pacific Waste Management (Australia)

- •CleanMed Waste Services (India)

- •BPM Medical Waste Services (South Africa)

- •BioMedical Waste Solutions (United Kingdom)

Market Breakdown

- •By Medical Waste Type

- ◦Infectious Waste

- ◦Sharps Waste

- ◦Chemical Waste

- ◦Pharmaceutical Waste

- ◦General Medical Waste

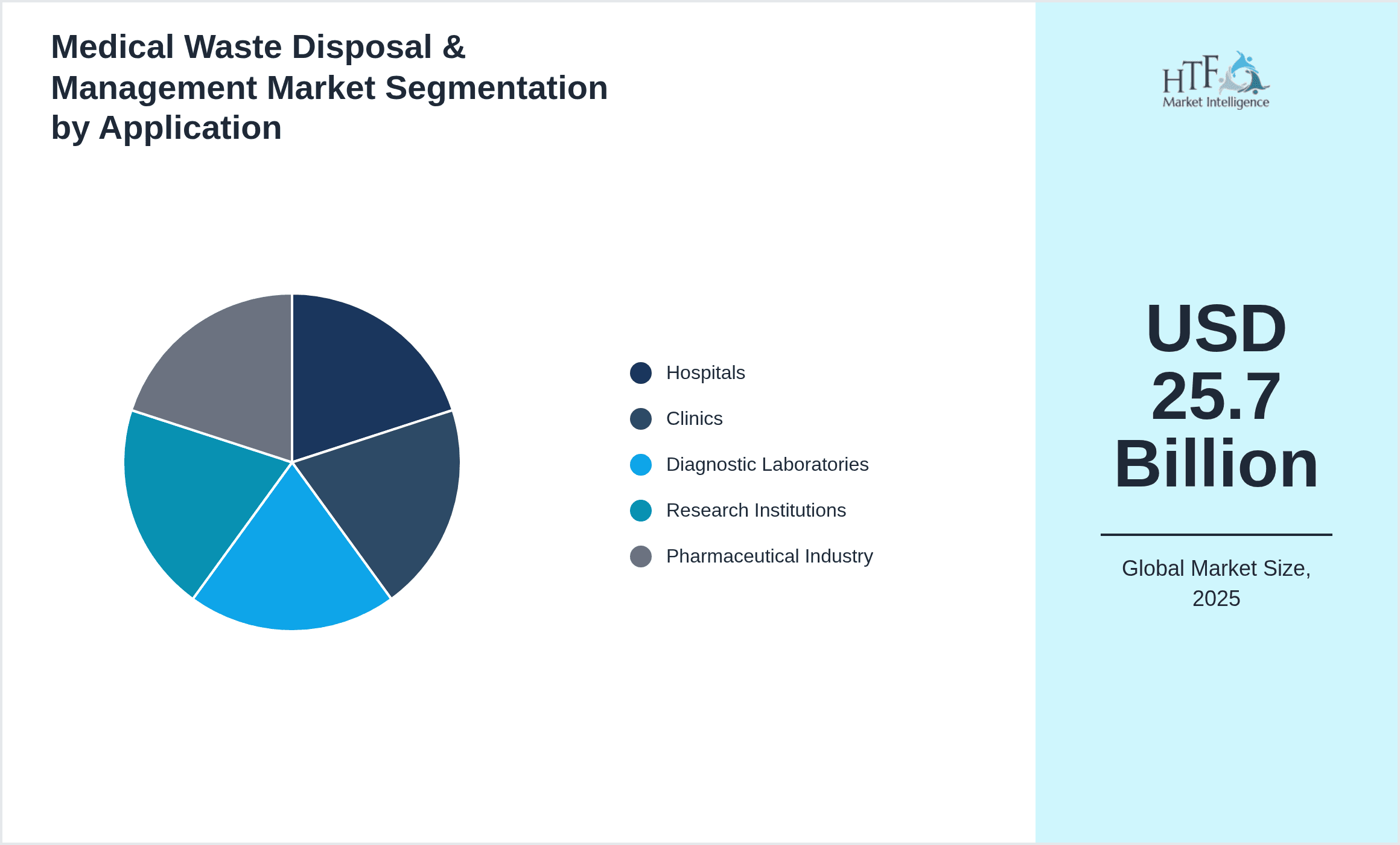

- •By Application

- ◦Hospitals

- ◦Clinics

- ◦Diagnostic Laboratories

- ◦Research Institutions

- ◦Pharmaceutical Industry

- •By Treatment Technology

- ◦Incineration

- ◦Autoclaving

- ◦Chemical Disinfection

- ◦Microwave Treatment

- ◦Landfilling

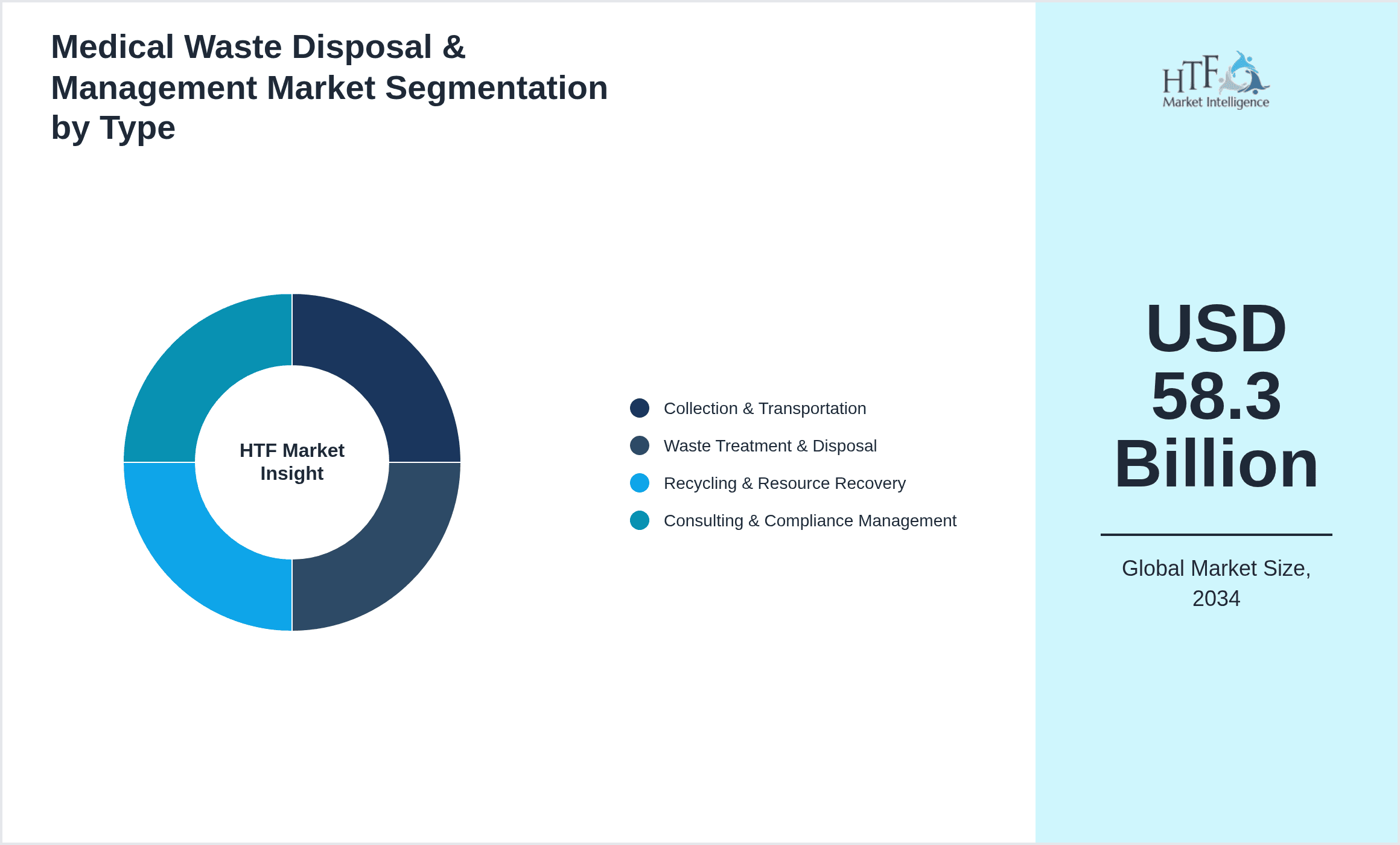

- •By Service Type

- ◦Collection & Transportation

- ◦Waste Treatment & Disposal

- ◦Recycling & Resource Recovery

- ◦Consulting & Compliance Management

Growth Dynamics

- •The global Medical Waste Disposal & Management Market is primarily driven by the expansion of healthcare infrastructure worldwide, which results in increased generation of medical waste. Rising incidences of chronic diseases and pandemics have further accentuated the demand for efficient waste management solutions. Government regulations enforcing stringent disposal norms and environmental protection laws compel healthcare providers to adopt advanced treatment technologies. Additionally, increasing awareness about the health hazards related to improper waste handling among healthcare workers and the public fuels market growth. Investments in sustainable and eco-friendly waste disposal methods by private and public sectors also contribute significantly to expanding market opportunities.

- •Technological advancements such as the adoption of microwave treatment, chemical disinfection, and autoclaving are revolutionizing waste management practices, offering safer and environmentally sustainable alternatives to traditional incineration. The integration of IoT and data analytics in waste tracking and compliance monitoring enhances operational efficiency and transparency. Rising collaborations between waste management companies and healthcare institutions foster innovation and service expansion. Furthermore, growing demand in emerging economies driven by increasing healthcare access and infrastructure development is a powerful growth catalyst. These trends reflect a shift towards more efficient, compliant, and sustainable medical waste management systems globally.

- •Despite growth prospects, the market faces restraints including high operational costs associated with advanced treatment technologies and infrastructure development. Regulatory compliance complexities across different regions require significant investment in training and system upgrades. The lack of awareness and infrastructure in underdeveloped regions limits market penetration. Additionally, the risk of pathogen spread and environmental contamination due to improper handling poses ongoing challenges. These factors can hinder rapid adoption of modern waste management solutions, especially in cost-sensitive and resource-constrained settings, thereby restraining market expansion.

- •Opportunities abound in the development of innovative, cost-effective, and eco-friendly waste treatment technologies that minimize environmental impact and enhance safety. Emerging markets in Asia-Pacific, Latin America, and the Middle East & Africa present significant growth potential due to expanding healthcare sectors and increasing regulatory enforcement. Digitalization and smart waste management solutions offer avenues for operational optimization and compliance assurance. There is also growing scope in service diversification such as consulting, training, and compliance management to enable healthcare providers to meet regulatory standards efficiently. Strategic partnerships and mergers can further unlock market expansion and technology transfer opportunities.

- •Challenges in the market revolve around inconsistent regulatory frameworks across countries, leading to compliance difficulties for global operators. Limited infrastructure and logistical challenges in remote or underdeveloped areas impede comprehensive waste collection and treatment. The threat of infectious disease outbreaks necessitates rapid and safe disposal, pressuring existing systems. Additionally, high capital expenditure for state-of-the-art facilities restricts market entry and expansion for smaller players. Ensuring workforce safety and mitigating environmental pollution remain ongoing concerns requiring continual innovation and investment, which may slow market adoption in cost-sensitive regions.

Market Trends

- •Increasing adoption of sustainable and environmentally friendly medical waste disposal technologies such as autoclaving and microwave treatment is reshaping the market. Companies are focusing on reducing carbon footprints and emissions associated with waste processing by integrating renewable energy sources and advanced filtration systems. The trend towards circular economy principles encourages recycling and resource recovery from non-hazardous medical waste streams, supporting sustainability goals and regulatory compliance.

- •Digital transformation is gaining traction, with the deployment of IoT-enabled waste tracking and monitoring systems that enhance transparency, traceability, and compliance reporting. These technologies enable real-time data collection, facilitate regulatory audits, and improve operational efficiencies, helping healthcare providers manage waste more effectively and comply with evolving legislation.

- •Strategic collaborations and mergers between waste management firms and healthcare organizations are becoming more prevalent to expand service portfolios and geographic reach. These alliances enable sharing of technology, expertise, and infrastructure, leading to improved service delivery and cost optimization. For example, partnerships focused on developing decentralized waste treatment facilities cater to regional needs efficiently.

- •Increasing regulatory focus on hazardous waste segregation and safe disposal is driving healthcare providers to invest in comprehensive waste management training and compliance programs. This trend encourages better waste segregation at source, reducing risks and enhancing treatment efficiency while ensuring adherence to international standards and local regulations.

- •Rising demand for mobile and on-site waste treatment solutions is emerging, particularly in remote and disaster-affected areas. Compact, portable technologies enable immediate waste neutralization, reducing transportation risks and costs. This trend supports rapid response capabilities and enhances environmental safety in diverse healthcare settings.

Market Opportunities

- •The rapid expansion of healthcare infrastructure in developing regions such as Asia-Pacific and Latin America offers substantial opportunities for market players to introduce advanced medical waste disposal solutions. Increasing government funding and international aid programs aimed at improving healthcare sanitation create favorable conditions for market entry and growth.

- •Innovations in waste treatment technologies that reduce environmental impact and operational costs present promising avenues for product development and differentiation. In particular, eco-friendly alternatives to incineration such as plasma gasification and enzymatic treatments are gaining attention and investment.

- •Digital waste management platforms that provide end-to-end solutions, including waste tracking, compliance reporting, and analytics, represent a growing market segment. These platforms help healthcare providers optimize processes and meet stringent regulatory demands, enhancing customer value and retention.

- •Collaborations with governments and NGOs to implement community-level medical waste management programs can expand market reach and create social impact. These initiatives foster public-private partnerships that facilitate technology deployment and capacity building in underserved areas.

- •Diversifying service offerings to include consulting, training, and regulatory compliance management enables companies to build long-term client relationships and generate recurring revenue streams. This strategic approach addresses evolving industry needs and positions players as trusted partners.

Market Challenges

- •The heterogeneity of regulatory standards across different countries complicates compliance for global medical waste management providers, requiring tailored solutions and significant resource allocation. This inconsistency slows market expansion and increases operational complexity.

- •Limited awareness and inadequate infrastructure in many low-income regions hinder effective medical waste collection and treatment, resulting in environmental contamination and health risks. Addressing these gaps is both a challenge and a necessity for market development.

- •High capital and operational expenditures associated with advanced treatment technologies such as autoclaving and plasma gasification constrain adoption, particularly among smaller healthcare facilities and in resource-limited settings.

- •Managing infectious waste safely during pandemics and outbreaks places immense pressure on existing disposal systems, exposing weaknesses and necessitating rapid scaling and innovation. Ensuring workforce safety and preventing cross-contamination remain critical challenges.

- •The risk of illegal dumping and improper disposal due to lack of enforcement or corruption undermines market integrity and environmental safety, requiring stronger governance and monitoring mechanisms.

Regulatory Framework

- •Between 2019 and 2024, global regulatory bodies strengthened medical waste management standards, mandating comprehensive waste segregation, tracking, and treatment protocols. The WHO updated guidelines emphasizing environmentally sound disposal methods and minimizing incineration emissions. National regulations increasingly require licensing for waste handlers and impose strict penalties for non-compliance, thereby elevating industry standards and operational transparency.

- •The United States Environmental Protection Agency (EPA) enhanced hazardous waste rule enforcement, introducing more rigorous reporting requirements and promoting sustainable disposal technologies. The European Union implemented the Waste Framework Directive revisions focusing on circular economy principles, encouraging recycling and recovery of medical waste components.

- •In Asia-Pacific, countries like India and China enacted stricter biomedical waste management rules, emphasizing decentralized treatment and encouraging private sector participation. These regulations promote adoption of advanced technologies and foster public awareness campaigns to improve compliance.

- •Environmental protection agencies worldwide mandated the adoption of real-time waste tracking systems and electronic manifest systems to enhance regulatory oversight and reduce illegal dumping. These measures improve traceability and accountability across the waste management supply chain.

- •Government incentives and subsidies were introduced to support infrastructure development and technology adoption in medical waste management, particularly favoring eco-friendly and energy-efficient solutions. These policies aim to align healthcare waste management with broader environmental sustainability goals.

Market Intelligence

- •15th January 2025, Stericycle Inc. launched a next-generation autoclave system featuring enhanced energy efficiency and automated waste tracking capabilities designed for large hospital networks. This innovation aims to reduce operational costs while ensuring compliance with stringent environmental regulations, positioning Stericycle as a leader in sustainable medical waste treatment. The system integrates IoT sensors for real-time monitoring, enhancing transparency and safety. This launch underscores the company’s commitment to innovation and environmental stewardship in the medical waste disposal sector. Source: Stericycle Official Press Release

- •10th March 2025, Veolia Environnement S.A. introduced a comprehensive digital platform for medical waste management that offers end-to-end tracking, compliance reporting, and analytics for healthcare providers globally. The platform leverages AI-driven insights to optimize collection routes and treatment scheduling, significantly improving efficiency and reducing carbon emissions. This strategic initiative reflects Veolia’s focus on digital transformation and sustainability, catering to increasing regulatory demands. The platform is expected to enhance client engagement and operational transparency across multiple regions. Source: Veolia Corporate Announcement

- •22nd October 2024, Clean Harbors Inc. announced a strategic partnership with a leading pharmaceutical company to develop specialized hazardous waste treatment facilities across Asia-Pacific. The collaboration aims to address the growing challenge of pharmaceutical waste disposal with advanced plasma gasification technology that minimizes environmental impact. This joint venture is expected to expand Clean Harbors’ footprint in emerging markets and promote sustainable waste management practices within the pharmaceutical sector, supporting regional regulatory compliance and environmental goals. Source: Clean Harbors News Release

- •5th August 2024, Waste Management, Inc. completed the acquisition of a regional medical waste disposal company in Europe, enhancing its service capacity and geographic reach. This acquisition enables Waste Management to offer integrated waste solutions with advanced treatment technologies and strengthen its competitive position in the European market. The move aligns with the company’s growth strategy focusing on sustainable waste management and compliance with evolving European Union regulations, providing clients with comprehensive disposal and recycling services. Source: Waste Management Official Statement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 25.7 Billion |

| Forecast Year Market Size | USD 58.3 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Medical Waste Type (Infectious Waste, Sharps Waste, Chemical Waste, Pharmaceutical Waste, General Medical Waste), Application (Hospitals, Clinics, Diagnostic Laboratories, Research Institutions, Pharmaceutical Industry), Treatment Technology (Incineration, Autoclaving, Chemical Disinfection, Microwave Treatment, Landfilling), Service Type (Collection & Transportation, Waste Treatment & Disposal, Recycling & Resource Recovery, Consulting & Compliance Management) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Stericycle Inc. (United States), Veolia Environnement S.A. (France), Clean Harbors Inc. (United States), Waste Management, Inc. (United States), SUEZ (France), Daniels Health (Australia), MedPro Disposal (United States), Republic Services, Inc. (United States), Sterilex Corporation (United States), Clean Earth, Inc. (United States), Babcock & Wilcox Enterprises, Inc. (United States), Keurig Dr Pepper Inc. (United States), EnviroSolutions LLC (United States), MedWaste Disposal Services (Canada), HealthLink, Inc. (United States), Onyx Environmental Services (United States), Pacific Waste Management (Australia), CleanMed Waste Services (India), BPM Medical Waste Services (South Africa), BioMedical Waste Solutions (United Kingdom) |

Global Medical Waste Disposal & Management Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.