Europe Processed Chicken Market - Europe Size & Outlook 2025-2034

Europe Processed Chicken Market is segmented by Type (Frozen Processed Chicken, Fresh Processed Chicken, Marinated Processed Chicken, Cooked Processed Chicken, Breaded Processed Chicken), Application (Retail, Foodservice, Institutional Catering, Ready-to-Eat Meals, Food Processing), Packaging Type (Vacuum Packaging, Modified Atmosphere Packaging, Skin Packaging, Tray Packaging), Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Foodservice Distributors), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Processed Chicken market comprises a diverse range of chicken products subjected to various processing techniques including freezing, marination, cooking, and breading. These products cater to multiple applications such as retail distribution, foodservice outlets, institutional catering, ready-to-eat meal production, and further food processing industries. The market addresses consumer demand for convenient, safe, and flavorful protein sources, emphasizing enhanced shelf life and ease of preparation. It plays a pivotal role in Europe’s food ecosystem by integrating advanced processing technologies compliant with rigorous food safety regulations and sustainability mandates. The market scope extends across multiple European countries with a focus on product innovation, supply chain optimization, and adaptation to evolving dietary trends. This market is of strategic importance due to its contribution to nutritional security, economic value generation, and its capacity to meet the lifestyle needs of a diverse consumer base across urban and rural areas with increasing preference for processed poultry products.

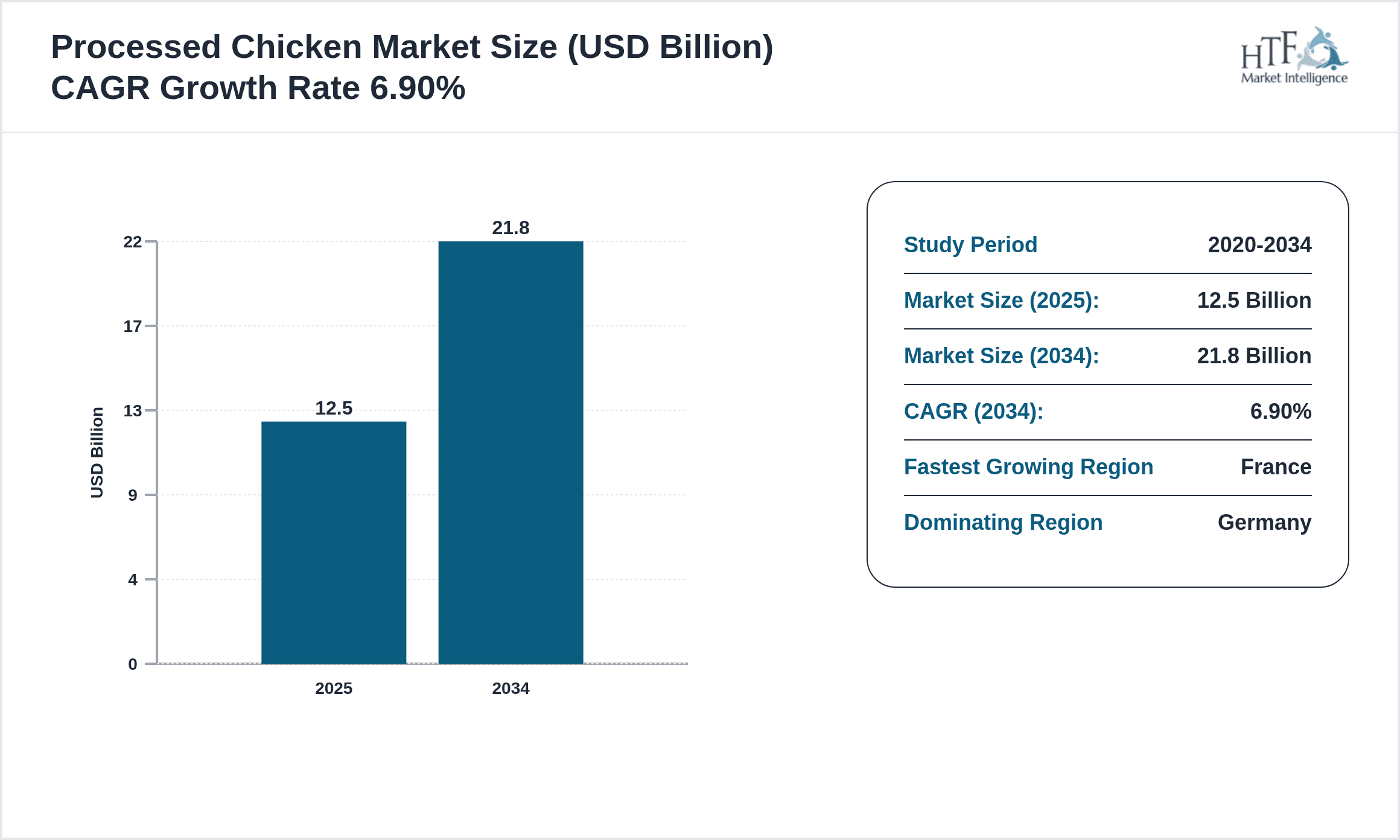

- •The Europe Processed Chicken market was valued at USD 12.5 Billion in 2025 and is forecast to reach USD 21.8 Billion by 2034, exhibiting a robust CAGR of 6.9%. Germany leads the market in terms of size and consumption, with France emerging as the fastest growing country driven by increasing demand for marinated and convenience chicken products. Frozen Processed Chicken dominates the product segment with the largest market share, while Marinated Processed Chicken registers the highest growth rate fueled by consumer preference for ready-to-cook options. Retail and Foodservice applications constitute the major demand centers, supported by expanding modern retail channels and growing foodservice industry in Europe.

- •Processed chicken products offer significant value propositions through ease of use, extended freshness, and flavor enhancement, making them indispensable to retailers, foodservice operators, and institutional caterers. Strategic importance of this market is underscored by its alignment with consumer trends towards protein-rich diets, convenience foods, and sustainable sourcing. Stakeholders leverage technological advancements in processing and packaging to enhance product differentiation and meet stringent regulatory standards. The market’s growth is further propelled by investments in cold-chain infrastructure, digital retail platforms, and innovation in value-added chicken products, positioning it as a key segment for future growth in Europe’s poultry sector.

Competitive Landscape

The Europe Processed Chicken market is characterized by intense competition among key players adopting strategies such as product innovation, strategic partnerships, and geographic expansion to consolidate market share. Companies invest heavily in advanced processing technologies including marination techniques and automated packaging systems to improve product quality and shelf life. Emphasis on sustainability and animal welfare practices has led to adoption of eco-friendly processing and sourcing methods. Market players actively pursue mergers and acquisitions to broaden product portfolios and access new distribution networks across Europe. Digital transformation initiatives in supply chain management and e-commerce platforms enhance operational efficiency and consumer reach. Businesses focus on catering to evolving consumer preferences by introducing organic, antibiotic-free, and ready-to-cook chicken products. The competitive environment also involves pricing strategies tailored to diverse consumer segments and collaboration with retail chains for exclusive product launches, ensuring sustained growth and differentiation in a mature market.

Leading Companies in Processed Chicken Market

- •2 Sisters Food Group (United Kingdom)

- •LDC Group (France)

- •PHW Group (Germany)

- •Vion Food Group (Netherlands)

- •Kavli Holding (Norway)

- •Doux Group (France)

- •Sadia (Brazil - operations in Europe)

- •Pilgrim’s Pride Corporation (United States - European operations)

- •AIA Group (Italy)

- •Hain Celestial Group (United States - European operations)

- •BRF S.A. (Brazil - European operations)

- •MHP SE (Ukraine)

- •Al Islami Foods (United Arab Emirates - European operations)

- •Plukon Food Group (Netherlands)

- •Gold&Green Foods (Finland)

- •Cargill Incorporated (United States - European operations)

- •Hans Knauthe GmbH & Co KG (Germany)

- •Atria Plc (Finland)

- •Faccenda Group (United Kingdom)

- •Norac Foods (United Kingdom)

Market Segments

- •By Type

- ◦Frozen Processed Chicken

- ◦Fresh Processed Chicken

- ◦Marinated Processed Chicken

- ◦Cooked Processed Chicken

- ◦Breaded Processed Chicken

- •By Application

- ◦Retail

- ◦Foodservice

- ◦Institutional Catering

- ◦Ready-to-Eat Meals

- ◦Food Processing

- •By Packaging Type

- ◦Vacuum Packaging

- ◦Modified Atmosphere Packaging

- ◦Skin Packaging

- ◦Tray Packaging

- •By Distribution Channel

- ◦Supermarkets & Hypermarkets

- ◦Specialty Stores

- ◦Online Retail

- ◦Foodservice Distributors

Market Drivers

Rising consumer demand for convenient and ready-to-cook protein sources drives the processed chicken market in Europe. Changing lifestyles with increasing working population and urbanization lead consumers to opt for processed chicken products that reduce preparation time. Recent innovations, such as marinated and flavored chicken varieties introduced by key players, cater to diverse taste preferences, enhancing market appeal. For instance, in early 2025, 2 Sisters Food Group launched a new range of pre-seasoned frozen chicken portions targeting millennials seeking quick meal solutions. Additionally, growing awareness of protein-rich diets and health-conscious eating habits promote processed chicken as a lean meat option. Expansion of modern retail and foodservice channels facilitates wider accessibility to processed chicken products. Regulatory emphasis on food safety and quality assurance further boosts consumer confidence, encouraging market growth. Investments in cold chain infrastructure across Eastern and Southern Europe improve product availability and shelf life, reinforcing demand. The integration of sustainable sourcing and ethical production practices resonates with environmentally aware consumers, adding impetus to market development.

Market Trend

Growing consumer preference for clean-label and organic processed chicken products shapes future trends in the European market. Manufacturers are increasingly adopting natural ingredients, reducing additives, and promoting antibiotic-free chicken offerings to align with evolving health consciousness. The rise of e-commerce and online grocery platforms accelerates market penetration, providing convenient access to processed chicken products across Europe, especially in countries like France and the UK. Companies such as LDC Group have recently expanded their digital sales channels in 2025 to capitalize on this shift. Additionally, innovation in sustainable packaging solutions, including biodegradable films and recyclable materials, is gaining traction to meet stringent environmental regulations and consumer expectations. The trend of ready-to-eat and ready-to-cook meal kits incorporating processed chicken is expanding, supported by busy lifestyles and demand for diverse culinary experiences. Collaborative efforts between poultry processors and foodservice providers to launch value-added products tailored for institutional catering signify another important trend. These developments collectively position the processed chicken market for sustained growth with a focus on health, convenience, and sustainability.

Market Opportunities

Expansion into emerging Eastern European markets presents significant growth opportunities for processed chicken producers, given rising disposable incomes and changing dietary patterns in countries such as Poland, Romania, and Hungary. Investments in cold chain logistics and modern retail infrastructure in these regions enable penetration of high-quality processed chicken products. The increasing demand for ethnic and flavored chicken products offers scope for product diversification and innovation. Strategic partnerships between European poultry processors and local foodservice chains facilitate market entry and brand recognition. Additionally, the growing demand for sustainable and ethically sourced chicken products opens avenues for premium product lines with certifications such as organic, free-range, and animal welfare labels. Integration of technology-driven traceability systems assures consumers about product origin and quality, enhancing trust and repeat purchases. The rise of plant-based and hybrid protein products incorporating processed chicken as a complementary ingredient also creates novel market segments. These opportunities, combined with digital marketing and e-commerce expansion, position the processed chicken market for accelerated growth across Europe.

Market Challenges

Stringent food safety regulations and compliance requirements pose significant challenges to processed chicken producers in Europe, increasing operational costs and complexity. Recent outbreaks linked to poultry-borne pathogens have heightened scrutiny and necessitated rigorous quality control measures, impacting smaller processors disproportionately. Supply chain disruptions caused by geopolitical tensions and fluctuating feed ingredient prices lead to cost volatility and supply uncertainties. For example, the Russia-Ukraine conflict in 2024 disrupted grain supplies, affecting feed costs and chicken production across several European countries. Consumer concerns regarding the use of antibiotics and additives create pressure for reformulation and transparency, requiring substantial investment in R&D. Additionally, rising labor costs and workforce shortages in processing plants challenge operational efficiency. Competitive pressure from alternative proteins, including plant-based substitutes, demands continuous innovation and differentiation. Environmental sustainability regulations related to emissions and waste management impose further compliance burdens. These challenges necessitate strategic investments in technology, process optimization, and supply chain resilience to maintain profitability and market position.

Regulation

Over the past five years, the European Union has implemented stringent regulations to enhance food safety and animal welfare in the processed chicken market. The EU Food Hygiene Package, updated in 2021, mandates comprehensive hazard analysis and critical control points (HACCP) protocols across processing facilities, ensuring safer chicken products. The Farm to Fork Strategy introduced new sustainability targets in 2023, emphasizing reduced antibiotic use in poultry farming and promoting organic certification. Additionally, Regulation (EU) 2019/6 on veterinary medicinal products enforces stricter controls on antibiotic residues, directly impacting processed chicken producers’ sourcing and production methods. Countries such as Germany and France have adopted national legislation aligning with these EU directives, imposing rigorous inspection and labeling requirements. These regulatory frameworks aim to boost consumer confidence, minimize health risks, and support environmentally sustainable poultry production. Compliance with these evolving standards drives innovation in processing technologies and supply chain transparency, shaping the competitive landscape of the European processed chicken market.

Recent Industry Insights

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Recent Merger and Acquisition

Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 21.8 Billion |

| CAGR | 6.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.7% |

| Scope of Report | Market is segmented by Type (Frozen Processed Chicken, Fresh Processed Chicken, Marinated Processed Chicken, Cooked Processed Chicken, Breaded Processed Chicken), Application (Retail, Foodservice, Institutional Catering, Ready-to-Eat Meals, Food Processing), Packaging Type (Vacuum Packaging, Modified Atmosphere Packaging, Skin Packaging, Tray Packaging), Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Foodservice Distributors) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | 2 Sisters Food Group (United Kingdom), LDC Group (France), PHW Group (Germany), Vion Food Group (Netherlands), Kavli Holding (Norway), Doux Group (France), Sadia (Brazil - operations in Europe), Pilgrim’s Pride Corporation (United States - European operations), AIA Group (Italy), Hain Celestial Group (United States - European operations), BRF S.A. (Brazil - European operations), MHP SE (Ukraine), Al Islami Foods (United Arab Emirates - European operations), Plukon Food Group (Netherlands), Gold&Green Foods (Finland), Cargill Incorporated (United States - European operations), Hans Knauthe GmbH & Co KG (Germany), Atria Plc (Finland), Faccenda Group (United Kingdom), Norac Foods (United Kingdom) |

Europe Processed Chicken Market - Europe Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.