China Glass Wool or Fiberglass Insulation Market Size, Growth & Revenue 2025-2034

China Glass Wool or Fiberglass Insulation Market is segmented by Product Type (Glass Wool, Fiberglass, Foam Glass, Mineral Wool, Others), Application (Building Insulation, HVAC Systems, Industrial Insulation, Acoustic Insulation, Automotive Insulation), Service Type (Installation Services, Maintenance Services, Consulting Services, After-Sales Support), Regional Deployment (East China, South China, North China, Central China, Northeast China, Northwest China, Southwest China), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Glass Wool or Fiberglass Insulation market is a critical segment within the construction and industrial sectors, focusing on materials designed to provide thermal and acoustic insulation. This market covers various product types including glass wool, fiberglass, foam glass, and mineral wool, which are employed across building insulation, HVAC systems, automotive, industrial, and acoustic applications. The market value chain involves raw material procurement, manufacturing, distribution, and end-use, with players ranging from large-scale manufacturers to regional distributors. The market's growth is driven by rapid urbanization in China, stringent government regulations promoting energy-efficient building codes, and a growing emphasis on sustainable and environmentally friendly construction materials. Additionally, technological innovations in fiber compositions and installation techniques continue to enhance product performance, cost efficiency, and recyclability. The demand for insulation materials is also supported by the increasing need to reduce energy consumption and carbon footprint in residential, commercial, and industrial infrastructures. This report analyzes market size and forecasts from 2020 historical data through 2025 base year to 2034, highlighting key trends, challenges, competitive landscape, and regional dynamics within China.

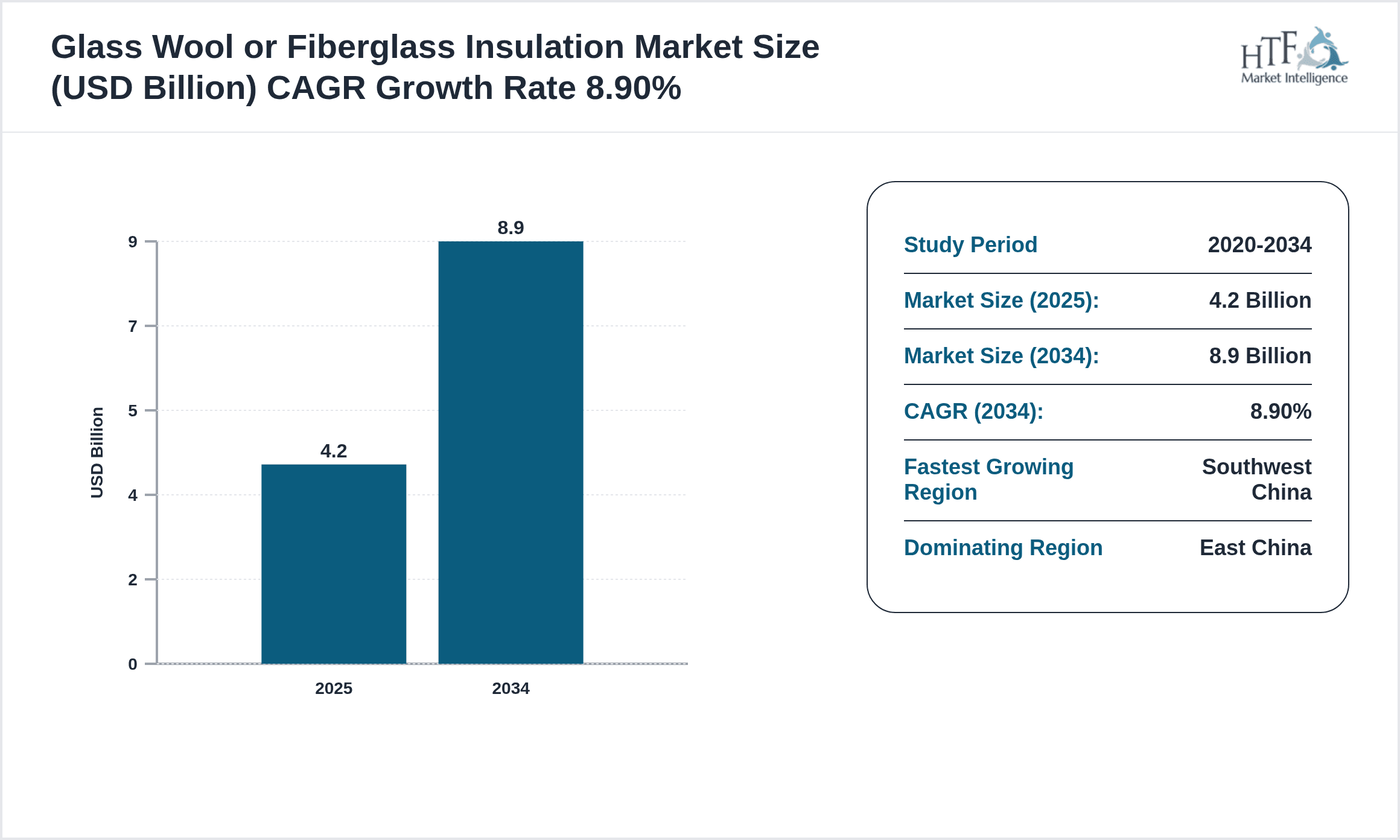

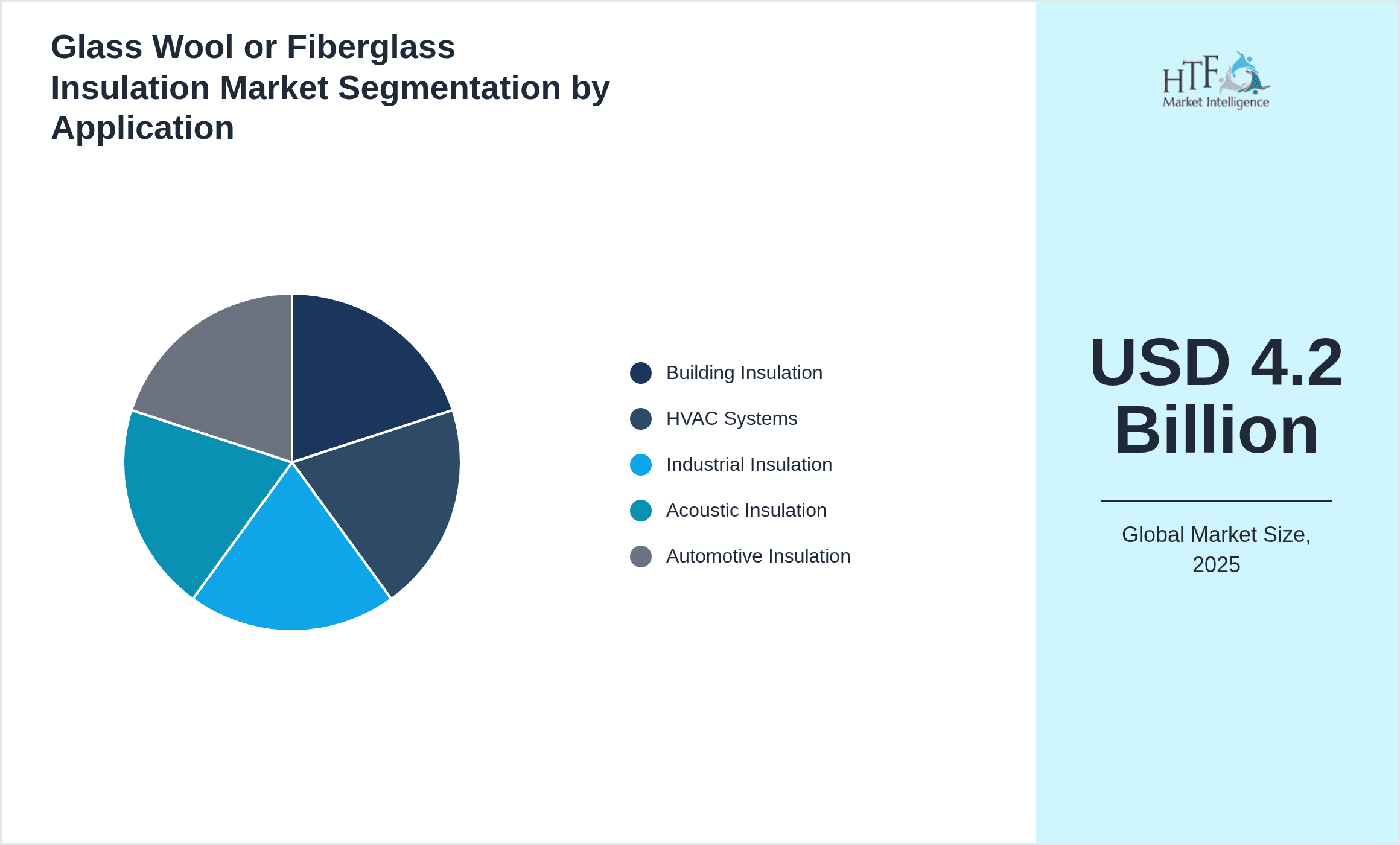

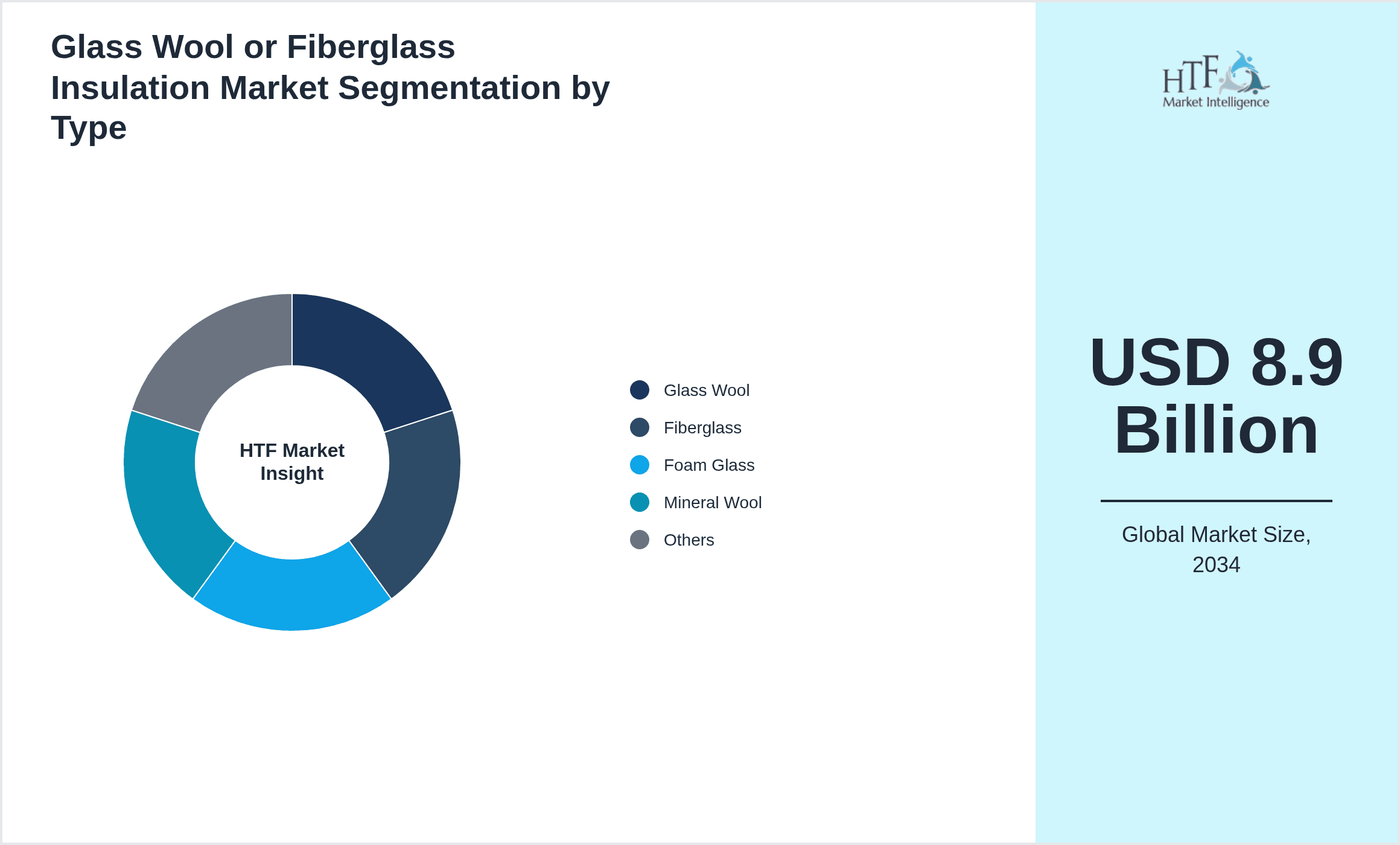

- •Key highlights include a base market size of USD 4.2 Billion in 2025, growing to an estimated USD 8.9 Billion by 2034, reflecting a robust CAGR of 8.9%. East China dominates market share due to its developed industrial base and construction activities, whereas Southwest China is forecasted to exhibit the fastest growth, fueled by infrastructure development and industrial expansion. Glass wool remains the leading product type, favored for its thermal efficiency and cost-effectiveness, while fiberglass is the fastest-growing segment, driven by advanced manufacturing and higher adoption in automotive and industrial insulation. Government policies emphasizing green building certifications and energy conservation further underpin market expansion. The market shows strong year-over-year growth averaging 8.5%, signaling sustained demand and investment opportunities. These insights provide strategic value for manufacturers, investors, and policymakers aiming to capitalize on China’s evolving insulation market.

- •The value proposition of the China Glass Wool or Fiberglass Insulation market lies in its contribution to energy savings, noise reduction, and environmental sustainability, crucial for meeting China’s ambitious carbon neutrality targets. Stakeholders including construction companies, industrial manufacturers, automotive producers, and government bodies benefit from high-performance insulation solutions that reduce operational costs and improve indoor environmental quality. The strategic importance of this market is underscored by increasing urbanization, government incentives for green building practices, and rising consumer awareness of energy-efficient materials. Continuous innovation and supply chain optimization also offer competitive advantages. As China transitions towards sustainable infrastructure development, the glass wool and fiberglass insulation market stands as a vital enabler for achieving energy efficiency and environmental compliance objectives across multiple end-use sectors.

Competitive Landscape

The China Glass Wool or Fiberglass Insulation market is characterized by a mix of domestic and international players competing through innovation, capacity expansion, and strategic partnerships. The competitive environment is shaped by continuous product development aimed at enhancing thermal performance, fire resistance, and environmental sustainability. Market leaders adopt multi-channel distribution strategies and invest heavily in R&D to introduce next-generation insulation materials that comply with evolving government regulations and green building standards. Pricing strategies are influenced by raw material costs, primarily silica sand and recycled glass, with manufacturers balancing cost competitiveness and quality assurance. Strategic mergers and acquisitions have been observed to consolidate market positions and expand geographic reach within China’s diverse regional markets. The adoption of digital supply chain management and localized manufacturing hubs enables faster delivery and customized solutions, enhancing customer satisfaction. The market entry barriers include high capital investment requirements, technical expertise, and regulatory compliance, which favor established players but also encourage innovation-driven new entrants. Regional competition is intense, with East China being the most developed market and Southwest China offering growth opportunities due to infrastructural development. Future trends indicate increasing focus on eco-friendly insulation materials and integration with smart building systems, positioning market participants to capitalize on sustainability and digitalization trends.

Prominent Players in Glass Wool or Fiberglass Insulation Market

- •Saint-Gobain (France)

- •Owens Corning (United States)

- •Jushi Group (China)

- •Nippon Sheet Glass Co., Ltd. (Japan)

- •Kaiser Fiber Glass Group (China)

- •China National Building Material Company (China)

- •PPG Industries (United States)

- •AGY Holding Corp. (United States)

- •Knauf Insulation (Germany)

- •Mingyang Group (China)

- •Beijing New Building Materials Public Limited Company (China)

- •Xinyi Glass Holdings Limited (China)

- •Asahi Glass Co., Ltd. (Japan)

- •BASF SE (Germany)

- •Saint-Gobain Weber (China)

- •Shanghai Fiberglass Plant (China)

- •China Fiberglass Holdings Co., Ltd. (China)

- •Knauf Group (China)

- •Jiangsu Yingming New Material Technology Co., Ltd. (China)

- •Yantai Wanhua Chemical Group Co., Ltd. (China)

- •Jiangsu Zhongwei New Materials Co., Ltd. (China)

- •Foshan Nanhai Huafeng Insulation Materials Co., Ltd. (China)

- •Shandong Huatai New Materials Co., Ltd. (China)

- •Zhejiang Jushi Co., Ltd. (China)

- •China National Chemical Corporation Ltd (China)

Market Breakdown

- •By Product Type

- ◦Glass Wool

- ◦Fiberglass

- ◦Foam Glass

- ◦Mineral Wool

- ◦Others

- •By Application

- ◦Building Insulation

- ◦HVAC Systems

- ◦Industrial Insulation

- ◦Acoustic Insulation

- ◦Automotive Insulation

- •By Service Type

- ◦Installation Services

- ◦Maintenance Services

- ◦Consulting Services

- ◦After-Sales Support

- •By Regional Deployment

- ◦East China

- ◦South China

- ◦North China

- ◦Central China

- ◦Northeast China

- ◦Northwest China

- ◦Southwest China

Growth Dynamics

- •Rapid urbanization in China has led to increased construction activities, significantly driving demand for glass wool and fiberglass insulation materials that provide energy-efficient building solutions. Government initiatives promoting green buildings and energy conservation have further accelerated market adoption. The rising preference for sustainable construction materials aligns with China's carbon neutrality objectives, boosting market growth.

- •Technological advancements in insulation material formulations, such as improved fire resistance, thermal conductivity, and recyclable components, have enhanced product performance and broadened application scope. These innovations enable manufacturers to meet stringent building codes and environmental standards, expanding market penetration in commercial and industrial sectors.

- •Growing industrialization, particularly in manufacturing and automotive sectors, is driving demand for specialized insulation products to improve energy efficiency and reduce operational costs. Fiberglass insulation is increasingly adopted for HVAC systems and industrial facilities, highlighting a shift towards advanced insulation technologies in these industries.

- •Increasing consumer awareness regarding indoor air quality and noise pollution mitigation is propelling demand for acoustic insulation applications. This trend supports the growth of glass wool and fiberglass products in both residential and commercial construction, aligning with evolving lifestyle preferences and regulatory guidelines.

- •Government subsidies and financing schemes for energy-efficient retrofitting and new construction projects incentivize the adoption of efficient insulation materials, creating a favorable investment environment. These policies stimulate market demand, especially in urban redevelopment and infrastructure projects across various Chinese regions.

- •Emerging construction technologies and prefabricated building components are integrating advanced insulation materials, enabling faster installation and reduced labor costs. This trend supports market expansion by enhancing the value proposition of glass wool and fiberglass insulation in modern construction methodologies.

- •The expansion of cold chain logistics and refrigerated transport sectors in China is increasing demand for high-performance insulation materials, particularly fiberglass, to maintain temperature-sensitive supply chains, representing a niche but rapidly growing market segment.

Market Trends

- •The market is witnessing a shift towards eco-friendly and sustainable insulation materials with increased use of recycled glass and low-VOC binders, addressing environmental concerns and regulatory compliance. Leading manufacturers are investing in green product lines to meet growing demand for sustainable construction materials.

- •Integration of smart insulation technologies that incorporate sensors for real-time monitoring of thermal performance and structural integrity is an emerging trend, enhancing building management systems and energy optimization.

- •Collaborations between insulation manufacturers and construction companies are increasing to develop customized solutions tailored to specific project requirements, improving installation efficiency and reducing waste during construction.

- •The rise of prefabricated and modular construction methods is driving demand for insulation products that are lightweight, easy to install, and compatible with off-site manufacturing processes, reshaping market supply chains and distribution models.

- •Digitalization in supply chain management and e-commerce platforms is expanding market reach and improving customer engagement, enabling faster delivery and enhanced after-sales support services in the insulation sector.

- •Increasing focus on acoustic insulation driven by urban noise pollution concerns is boosting demand for glass wool and fiberglass products designed specifically for sound absorption in residential and commercial buildings.

- •Emerging regulations mandating higher energy efficiency standards in new buildings are creating consistent demand growth, encouraging manufacturers to innovate and upgrade product portfolios to comply with evolving codes.

Market Opportunities

- •Expanding infrastructure development in western and southwestern China presents significant opportunities for insulation manufacturers to tap into underpenetrated regional markets, supported by government investment in urbanization and industrial parks.

- •Growing demand for energy-efficient retrofitting in existing commercial and residential buildings opens avenues for specialized insulation solutions that improve thermal performance without extensive structural modifications.

- •Innovation in composite insulation materials combining fiberglass with other advanced fibers offers potential for high-performance products targeting automotive and industrial sectors with stringent thermal and acoustic requirements.

- •Strategic partnerships with real estate developers and government agencies to promote green building certifications can enhance market penetration and brand recognition for insulation manufacturers.

- •Adoption of digital marketing and direct-to-consumer sales models can increase market access in tier-2 and tier-3 cities, expanding the customer base beyond traditional commercial channels.

- •Increasing investments in cold chain infrastructure and refrigerated transport logistics create niche opportunities for high-performance insulation materials designed for temperature-sensitive applications.

- •Rising consumer preference for healthier indoor environments drives demand for non-toxic, hypoallergenic insulation products, enabling differentiation and premium pricing strategies.

Market Challenges

- •Fluctuating raw material prices, particularly for silica sand and recycled glass, pose challenges to cost management and pricing stability, impacting profit margins for insulation manufacturers in China.

- •Stringent environmental regulations and complex compliance requirements increase operational costs and necessitate continuous investment in cleaner production technologies.

- •High initial installation costs and lack of consumer awareness regarding long-term energy savings can hinder the adoption of advanced insulation materials in certain residential segments.

- •Competition from alternative insulation materials such as polyurethane foam and cellulose fiber presents market share challenges, requiring manufacturers to emphasize product differentiation and performance benefits.

- •Fragmented distribution networks and logistical complexities across vast geographic zones in China can delay delivery and increase costs, especially in remote and less developed regions.

- •Limited availability of skilled labor and technical expertise for installation and maintenance affects the quality and effectiveness of insulation solutions, impacting market reputation.

- •The impact of global supply chain disruptions and trade tensions can affect import-dependent raw materials and components, creating supply uncertainties.

Regulatory Framework

- •Between 2020 and 2025, China's Ministry of Housing and Urban-Rural Development implemented the Green Building Evaluation Standard (GBES), mandating energy-efficient insulation materials in new constructions. This regulation requires adherence to thermal performance benchmarks and promotes the use of environmentally friendly insulation products, significantly influencing market demand.

- •The 2021 revision of the Energy Conservation Law introduced stricter energy-saving targets for public and commercial buildings, compelling developers to adopt high-quality glass wool and fiberglass insulation. Compliance has become a key factor in construction project approvals, enhancing market growth opportunities.

- •National standards such as GB/T 17794-2020 specify testing methods for thermal insulation materials, including glass wool and fiberglass, ensuring product quality and safety. Manufacturers must comply with these standards to maintain market access and consumer confidence.

- •Regional regulations in provinces like Guangdong and Jiangsu have introduced additional environmental controls on manufacturing emissions and waste disposal for insulation producers, promoting sustainable production practices and encouraging investment in cleaner technologies.

- •Government incentives, including subsidies and tax benefits for green building materials under the 14th Five-Year Plan (2021-2025), support the adoption of advanced insulation products. These policies aim to reduce carbon emissions and improve energy efficiency across residential and industrial sectors.

Market Intelligence

- •15th March 2025, Jushi Group announced the launch of a new high-performance fiberglass insulation product designed specifically for automotive applications. The product features enhanced thermal resistance and lightweight properties, aiming to improve vehicle energy efficiency and passenger comfort. This launch positions Jushi Group to capture growing demand from China's expanding automotive sector, particularly electric vehicle manufacturers seeking advanced insulation materials. The company highlighted its commitment to innovation and sustainability in product development, aligning with national green manufacturing policies. Source: Jushi Group Official Press Release.

- •22nd July 2025, Saint-Gobain inaugurated a new state-of-the-art manufacturing facility in East China focused on producing eco-friendly glass wool insulation products. The facility incorporates advanced production technologies that reduce carbon emissions and increase production efficiency. Saint-Gobain aims to strengthen its market leadership and meet rising demand driven by green building regulations and urban development initiatives. The investment also includes R&D centers to accelerate innovation in insulation technologies tailored to China’s unique climate and construction needs. Source: Saint-Gobain Corporate Website.

- •10th September 2024, Owens Corning entered into a strategic partnership with a leading Chinese construction conglomerate to supply fiberglass insulation materials for large-scale commercial projects in South China. The collaboration focuses on integrating high-performance insulation solutions that meet stringent energy-saving criteria and enhance building sustainability. This alliance enables Owens Corning to expand its footprint in China’s southern regional markets while providing tailored products for diverse construction requirements. The partnership exemplifies growing industry collaboration to promote energy-efficient building practices. Source: Owens Corning Press Release.

- •30th January 2025, China National Building Material Company completed the acquisition of a regional insulation manufacturer specializing in foam glass products. The acquisition expands CNBM’s product portfolio and manufacturing capacity, enhancing its competitive position in the insulation market. The move is expected to facilitate technology transfer and enable CNBM to offer a broader range of high-performance, environmentally friendly insulation solutions. This strategic acquisition aligns with CNBM’s growth objectives and commitment to sustainable building materials. Source: Industry Publication - Building Materials News.

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.2 Billion |

| Forecast Year Market Size | USD 8.9 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Product Type (Glass Wool, Fiberglass, Foam Glass, Mineral Wool, Others), Application (Building Insulation, HVAC Systems, Industrial Insulation, Acoustic Insulation, Automotive Insulation), Service Type (Installation Services, Maintenance Services, Consulting Services, After-Sales Support), Regional Deployment (East China, South China, North China, Central China, Northeast China, Northwest China, Southwest China) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Saint-Gobain (France), Owens Corning (United States), Jushi Group (China), Nippon Sheet Glass Co., Ltd. (Japan), Kaiser Fiber Glass Group (China) |

China Glass Wool or Fiberglass Insulation Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.