Europe Online Gambling Market Size, Growth & Revenue 2025-2034

Europe Online Gambling Market is segmented by Type (Web-based Gambling Platforms, Mobile-based Gambling Applications, Downloadable Gambling Software, Live Dealer Online Gambling, Virtual Reality Gambling), Application (Sports Betting, Casino Games, Poker, Bingo, Lottery), Payment Method (Credit/Debit Cards, E-wallets, Bank Transfers, Cryptocurrency), User Device (Desktop, Smartphone, Tablet), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Online Gambling Market represents a rapidly evolving digital entertainment sector that enables users to place bets and participate in games via internet platforms. This market includes various types such as web-based, mobile-based, downloadable applications, live dealer gaming, and virtual reality interfaces. Key applications span sports betting, casino games, poker, bingo, and lotteries, catering to a broad demographic. Technological progress, including mobile internet accessibility and immersive gaming experiences, fuels market growth. Regulatory reforms across European countries have created a more transparent and secure environment, encouraging participation while enforcing responsible gambling. The market's significance lies in its multifaceted contributions to economic growth, innovation in gaming technologies, and the development of digital payment ecosystems. Robust demand for convenient, real-time betting options and the fusion of entertainment with technology position this market as a strategic growth area within Europe's digital economy.

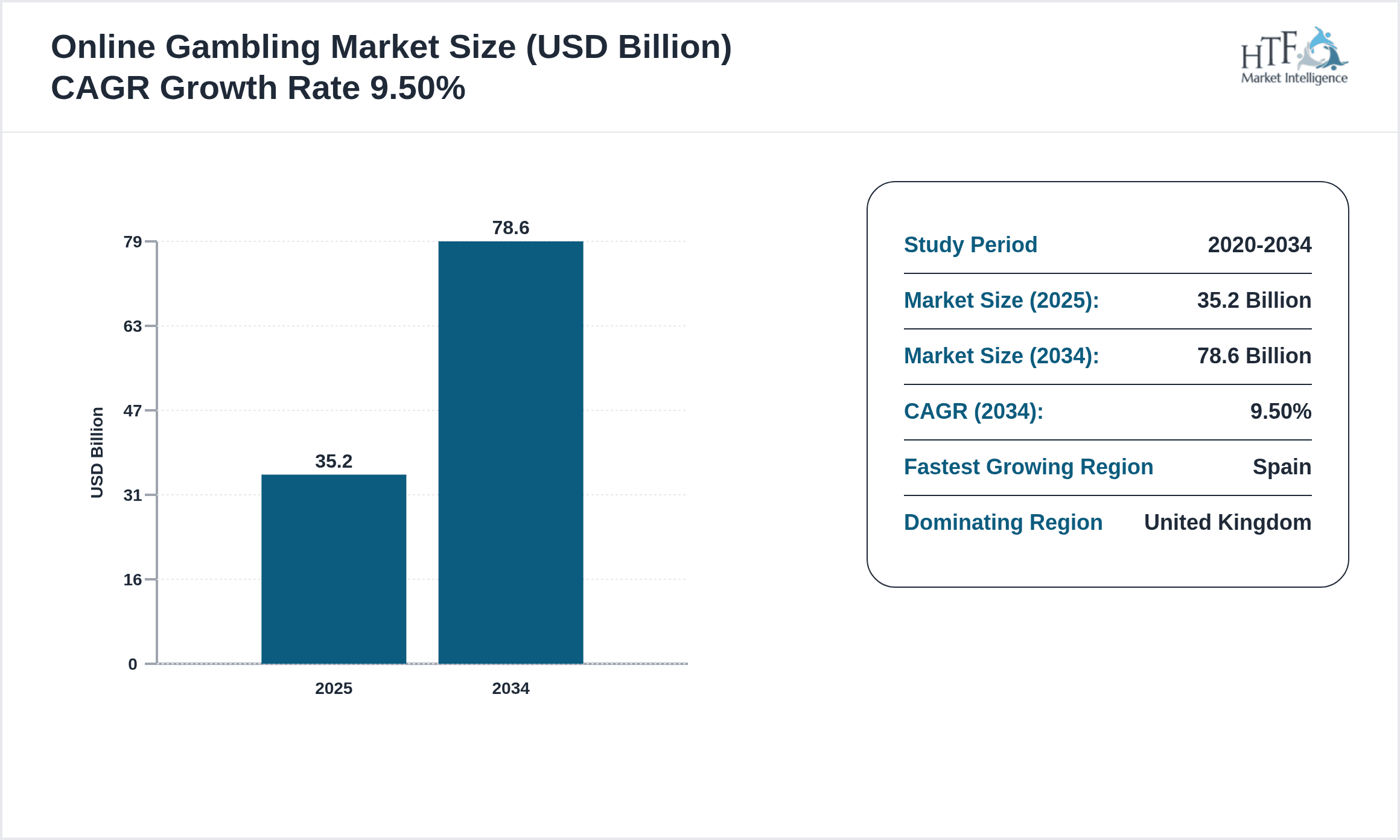

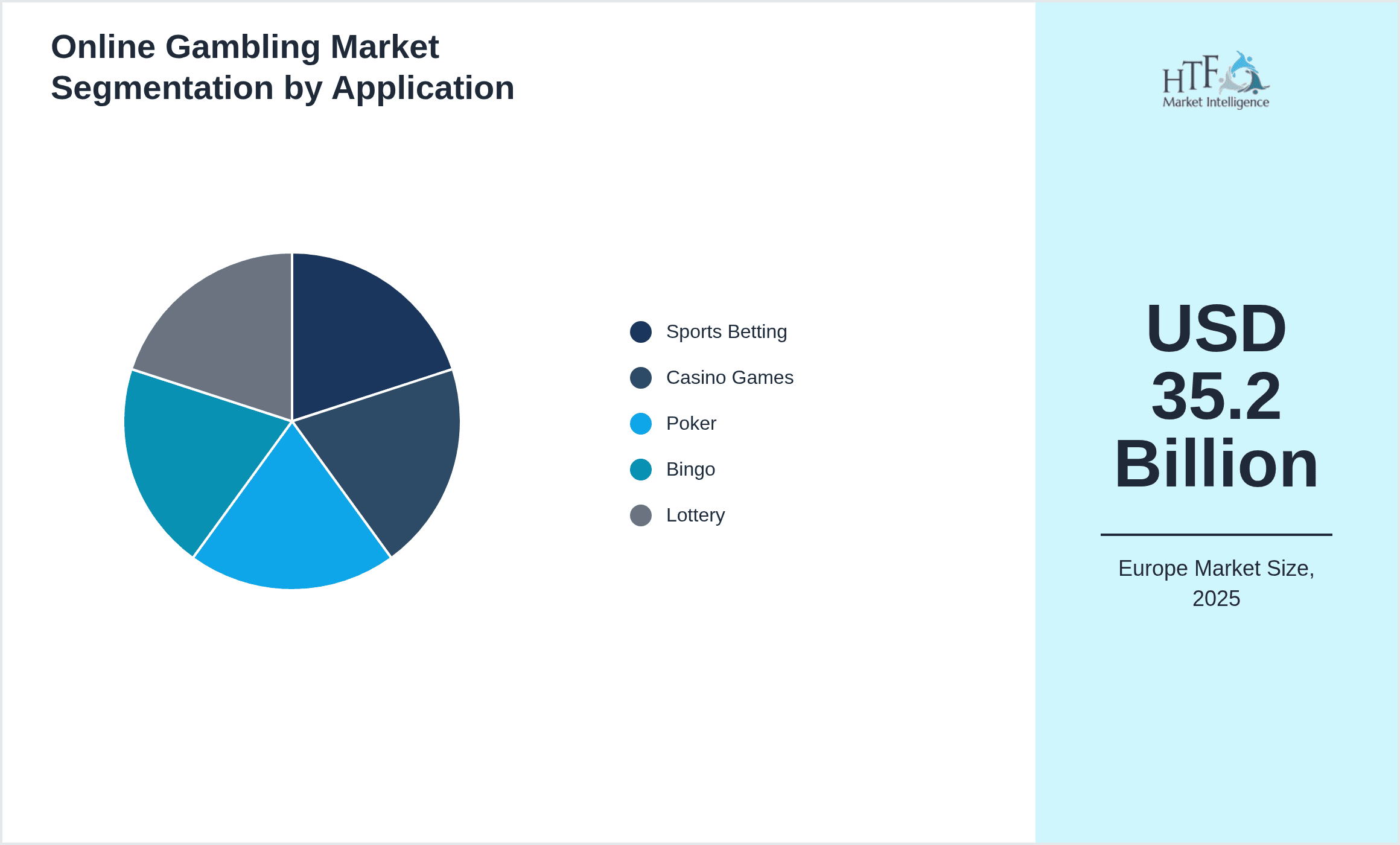

- •The Europe Online Gambling Market is projected to expand from USD 35.2 billion in 2025 to USD 78.6 billion by 2034, reflecting a compound annual growth rate of 9.5%. The United Kingdom dominates the market with a 28% share, driven by mature regulatory frameworks and high consumer adoption. Spain exhibits the fastest growth with a CAGR of 14.2%, fueled by progressive legalization and increasing smartphone penetration. Mobile-based gambling leads product types due to widespread smartphone usage, while virtual reality emerges as the fastest-growing segment with immersive gaming experiences attracting younger demographics. Key players consistently innovate through technology integration and strategic partnerships. Market dynamics reflect rising demand for personalized gaming experiences, cross-platform accessibility, and secure payment solutions, supported by government initiatives aimed at curbing illegal gambling and enhancing player protection.

- •The Europe Online Gambling Market offers significant value to stakeholders including operators, technology providers, regulators, and consumers. For operators, digital platforms provide scalable avenues for revenue generation and customer engagement through innovative game offerings and real-time analytics. Technology providers gain opportunities by delivering cutting-edge solutions such as AI-driven personalization and blockchain for transparent transactions. Regulators benefit from enhanced monitoring capabilities ensuring fair play and responsible gambling adherence, while consumers enjoy accessible, diverse gaming options with improved safety and convenience. The sector’s growth underpins employment in software development, customer service, and payment processing, contributing to broader economic development. Strategic foresight into evolving consumer preferences, regulatory landscapes, and technology trends will be essential for sustained competitive advantage in this vibrant market.

Competitive Landscape

Companies operating in the Europe Online Gambling Market adopt multifaceted strategies to sustain and enhance their market presence. Strategic partnerships with technology vendors and payment solution providers enable seamless user experiences and secure transactions. Global expansion initiatives focus on entering newly regulated European markets, leveraging local licenses and compliance expertise to capitalize on growth opportunities. Product innovation is central, with firms introducing live dealer games, virtual reality experiences, and AI-powered personalization to differentiate offerings and boost customer retention. Technological adoption includes blockchain for transparency, advanced analytics for user behavior insights, and cloud infrastructure for scalable operations. Competitive pricing strategies coupled with tailored promotions and loyalty programs strengthen market positioning. These companies also invest in responsible gambling tools and adhere to stringent regulatory requirements to build consumer trust. Future trends indicate increasing collaboration across the value chain to harness emerging technologies and expand into underserved segments, ensuring sustainable growth amid intensifying competition.

Key Players in Europe Online Gambling Market

- •Flutter Entertainment (Ireland)

- •Entain plc (United Kingdom)

- •Betsson AB (Sweden)

- •888 Holdings plc (United Kingdom)

- •Kindred Group (Sweden)

- •William Hill plc (United Kingdom)

- •The Stars Group (Canada)

- •Betfair (United Kingdom)

- •Ladbrokes Coral Group (United Kingdom)

- •Mr Green (Sweden)

- •NetEnt AB (Sweden)

- •Novomatic AG (Austria)

- •GVC Holdings (United Kingdom)

- •Paddy Power (Ireland)

- •LeoVegas AB (Sweden)

- •Unibet (Malta)

- •Betclic Everest Group (France)

- •Bwin Interactive Entertainment (Austria)

- •888poker (United Kingdom)

- •Casumo (Malta)

- •Betway (Malta)

- •PartyGaming (United Kingdom)

- •Sky Betting & Gaming (United Kingdom)

- •Resorts Digital Gaming (Malta)

- •Gamesys Group (United Kingdom)

Market Breakdown

- •By Type

- ◦Web-based Gambling Platforms

- ◦Mobile-based Gambling Applications

- ◦Downloadable Gambling Software

- ◦Live Dealer Online Gambling

- ◦Virtual Reality Gambling

- •By Application

- ◦Sports Betting

- ◦Casino Games

- ◦Poker

- ◦Bingo

- ◦Lottery

- •By Payment Method

- ◦Credit/Debit Cards

- ◦E-wallets

- ◦Bank Transfers

- ◦Cryptocurrency

- •By User Device

- ◦Desktop

- ◦Smartphone

- ◦Tablet

Growth Dynamics

The Europe Online Gambling Market experiences robust growth driven by rapid smartphone adoption and improved internet infrastructure, enabling seamless access to mobile-based gambling applications. For instance, Spain's regulatory reforms in 2023 expanded licensing, attracting new operators and increasing market penetration. Integration of advanced technologies such as AI and blockchain enhances user experience and transaction security, fostering trust and engagement. Additionally, collaborations between operators and sports organizations boost brand visibility and customer acquisition through sponsorships and exclusive betting offerings. Regulatory clarity in countries like the United Kingdom ensures compliance and reduces illegal betting activities, further legitimizing the market. The increasing popularity of live dealer games and virtual reality gambling caters to consumer demand for immersive experiences, expanding the market’s appeal. Moreover, rising disposable incomes and changing social attitudes toward gambling contribute to consistent user base expansion across major European countries.

Market Trends

Europe Online Gambling is witnessing a surge in live dealer and virtual reality gaming, leveraging immersive technologies to replicate authentic casino atmospheres online. Operators like Kindred Group and Betsson AB invest heavily in VR platforms to attract tech-savvy millennials. Mobile gambling continues to dominate due to widespread smartphone penetration and enhanced app functionalities, offering features such as in-play betting and personalized promotions. Regulatory bodies across Europe emphasize responsible gambling, prompting providers to integrate AI-driven monitoring tools for early detection of addictive behaviors. Furthermore, cryptocurrency adoption facilitates anonymous and swift transactions, appealing to a niche segment. Cross-platform compatibility and the rise of social gaming elements foster community engagement, expanding user retention. Strategic partnerships between gambling operators and sports leagues enhance fan interaction through exclusive betting content. These trends position the market to capitalize on evolving digital lifestyles and regulatory support for innovation.

Market Opportunities

The Europe Online Gambling Market offers vast opportunities through expansion into underpenetrated countries such as Italy and France, where regulatory liberalization is ongoing. Emerging technologies like virtual reality and augmented reality provide avenues for next-generation gaming experiences, attracting younger demographics and increasing session durations. The rising integration of AI enables personalized gaming journeys, predictive analytics, and enhanced fraud detection, improving customer satisfaction and operational efficiency. Payment innovation, including cryptocurrency acceptance and instant e-wallet solutions, reduces transaction friction and broadens accessibility. Operators can capitalize on cross-selling opportunities by bundling sports betting with casino offerings, leveraging comprehensive platforms. Additionally, partnerships with esports organizations unlock access to rapidly growing esports wagering markets. Government initiatives promoting legal online gambling and cracking down on illegal operators further create a favorable environment for market growth. These opportunities collectively position players to innovate and diversify revenue streams while aligning with regulatory frameworks.

Market Challenges

The Europe Online Gambling Market faces significant challenges including stringent and varying regulatory environments across countries, imposing compliance complexities and operational costs for operators. For example, Germany’s updated Glücksspielstaatsvertrag in 2023 introduced restrictive betting limits and advertising rules, affecting revenue potential. Rising concerns over gambling addiction necessitate investment in responsible gaming tools and limit promotional aggressiveness, potentially reducing user acquisition. High competition drives price wars and margin pressures, especially among mobile-based platforms striving to maintain customer loyalty. Additionally, the proliferation of illegal and unlicensed operators undermines market integrity and diverts revenue. Data privacy regulations such as GDPR impose rigorous data management requirements, increasing compliance burdens. Payment processing challenges, including delayed transaction approvals and fraud risks, may deter user engagement. These challenges require operators to adopt robust compliance frameworks, innovate responsibly, and foster trust to sustain long-term growth.

Regulatory Framework

Over the last five years, European countries have intensified regulation of online gambling to enhance consumer protection and market transparency. The United Kingdom’s Gambling Commission updated its licensing and advertising standards in 2021 to enforce stricter controls on customer affordability assessments and promote safer gambling. Germany implemented the Interstate Treaty on Gambling in 2021, harmonizing online betting laws with stringent limits on stakes and deposit caps. France reinforced compliance requirements through ARJEL guidelines focusing on anti-money laundering and responsible gambling in 2022. Spain’s Directorate General for the Regulation of Gambling expanded licensing frameworks in 2023, facilitating new market entrants under strict operational oversight. These regulations collectively aim to curb illegal gambling, safeguard vulnerable populations, and establish a level playing field for operators, shaping a regulated yet competitive environment across Europe.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Industry Publications, Company Announcements, Regulatory Filings

Regional Outlook

The United Kingdom currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Spain is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 35.2 Billion |

| Forecast Year Market Size | USD 78.6 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.3% |

| Scope of Report | Market is segmented by Type (Web-based Gambling Platforms, Mobile-based Gambling Applications, Downloadable Gambling Software, Live Dealer Online Gambling, Virtual Reality Gambling), Application (Sports Betting, Casino Games, Poker, Bingo, Lottery), Payment Method (Credit/Debit Cards, E-wallets, Bank Transfers, Cryptocurrency), User Device (Desktop, Smartphone, Tablet) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Flutter Entertainment (Ireland), Entain plc (United Kingdom), Betsson AB (Sweden), 888 Holdings plc (United Kingdom), Kindred Group (Sweden), William Hill plc (United Kingdom), The Stars Group (Canada), Betfair (United Kingdom), Ladbrokes Coral Group (United Kingdom), Mr Green (Sweden), NetEnt AB (Sweden), Novomatic AG (Austria), GVC Holdings (United Kingdom), Paddy Power (Ireland), LeoVegas AB (Sweden), Unibet (Malta), Betclic Everest Group (France), Bwin Interactive Entertainment (Austria), 888poker (United Kingdom), Casumo (Malta), Betway (Malta), PartyGaming (United Kingdom), Sky Betting & Gaming (United Kingdom), Resorts Digital Gaming (Malta), Gamesys Group (United Kingdom) |

Europe Online Gambling Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.