Africa Bauxite Market Scope & Changing Dynamics 2024-2034

Africa Bauxite Market is segmented by Type (Gibbsite (Hydrated Alumina), Boehmite (Aluminum Oxide Hydroxide), Diaspore (Alpha-Alumina Hydroxide), Non-Activated Bauxite, Activated Bauxite), Application (Aluminum Production, Refractory Materials, Chemicals, Cement, Abrasives), Mining Method (Open-Pit Mining, Underground Mining, Hydraulic Mining), End-User Industry (Metallurgical Industry, Construction Industry, Chemical Industry, Abrasive Manufacturing), and Geography (South Africa, Nigeria, Kenya, Algeria, Zambia, Morocco, Ethiopia, Others)

Pricing

Report Overview

Executive Summary

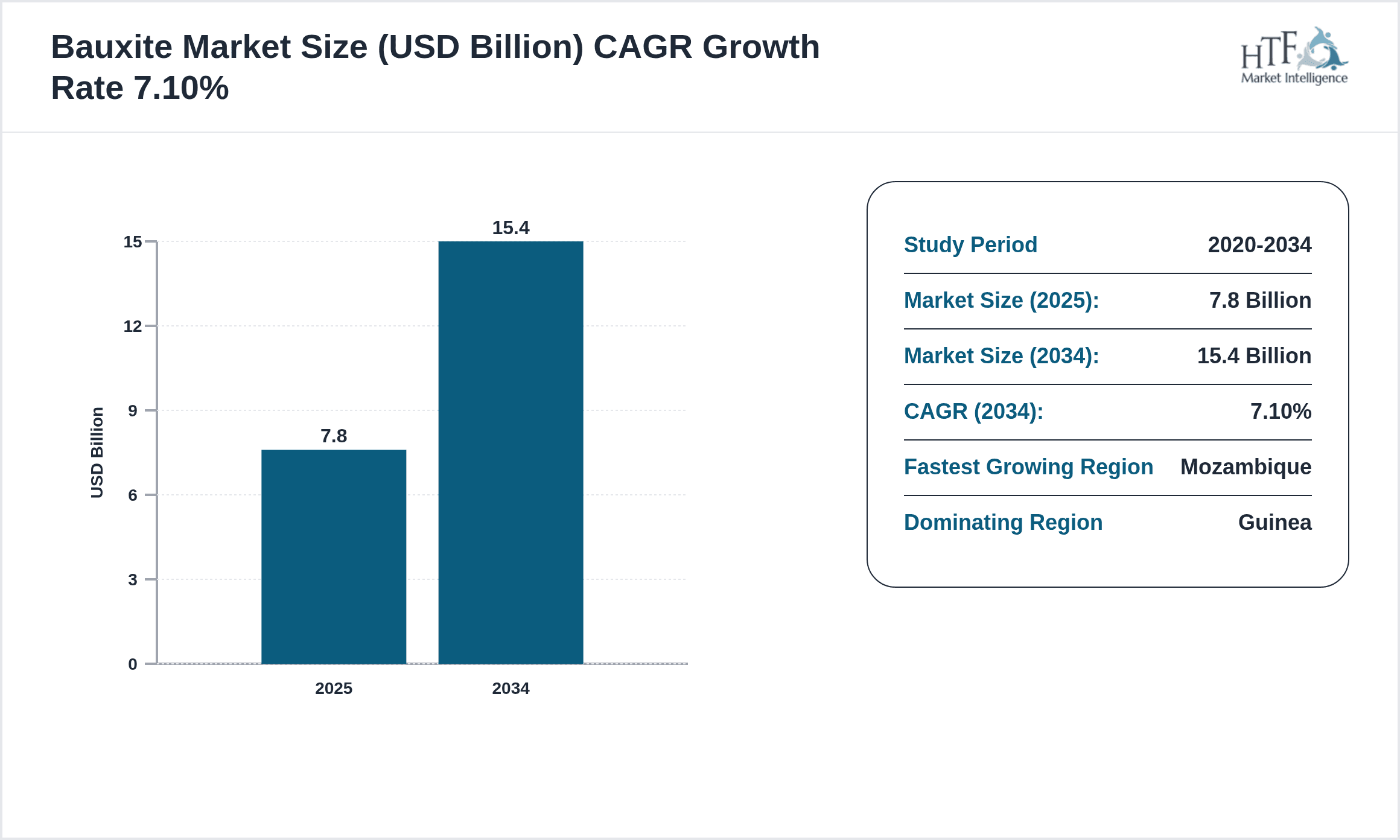

- •The Africa Bauxite market is a critical sector involving the mining and processing of bauxite ore, essential for aluminum production and various industrial applications such as refractory materials, chemicals, cement, and abrasives. Predominantly mined in countries such as Guinea, Ghana, Mozambique, Sierra Leone, and South Africa, the market operates within a diverse framework of mining, beneficiation, and supply chain activities. This market's boundaries include the exploration of different bauxite types—Gibbsite, Boehmite, Diaspore, and activated/non-activated variants—each serving distinct industrial purposes. The industry's scope extends to meet the growing demand from aluminum smelters and manufacturing sectors, supported by Africa's vast natural reserves and increasing infrastructural development. Challenges such as regulatory compliance, environmental concerns, and infrastructural limitations coexist with growth opportunities driven by technological innovations and expanding export markets. This market report provides a comprehensive analysis of segmentations by type and application, regional dynamics, competitive landscape, and future growth prospects through to 2034, highlighting the strategic importance of African bauxite within the global minerals economy.

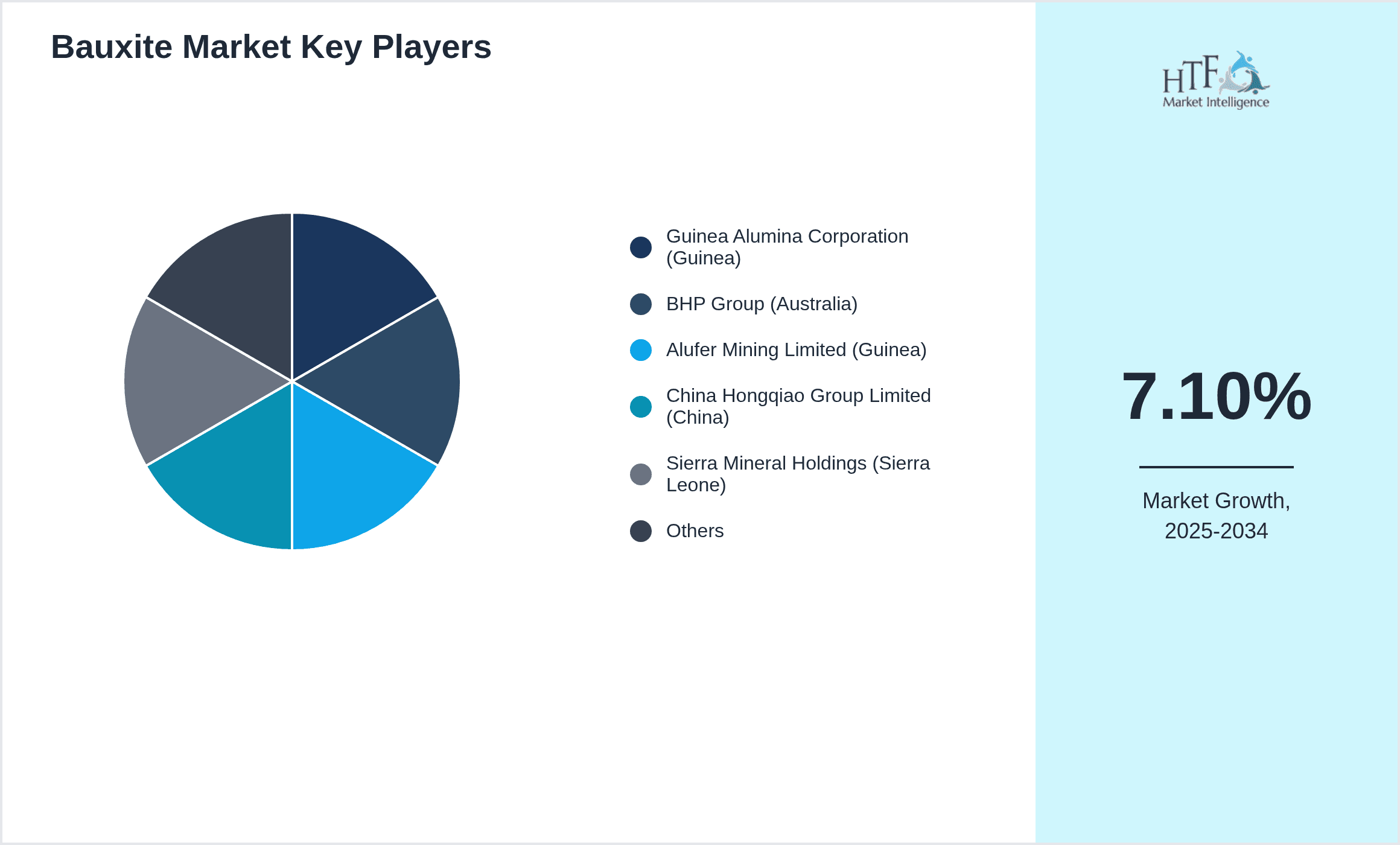

- •Key highlights include a projected CAGR of 7.1% from 2024 to 2034, with market size expected to nearly double from USD 7.8 billion in 2024 to USD 15.4 billion by 2034. Guinea dominates the regional market with a 34% share, while Mozambique is the fastest growing with a CAGR of 9.3%. Gibbsite leads the product segment in market share and application, primarily driven by aluminum production demand. The market is influenced by rising investments in mining infrastructure, increasing aluminum consumption, and evolving regulatory frameworks aimed at sustainable extraction and export practices.

- •Strategically, the Africa Bauxite market holds significant value for stakeholders including mining companies, industrial manufacturers, government bodies, and international investors. It supports regional economic development through export revenues and job creation while contributing to the global aluminum supply chain. The market's growth trajectory is shaped by resource availability, technological advancements in ore processing, and collaborative initiatives across African nations to enhance mining efficiency and environmental stewardship.

Competitive Landscape

Competition in the Africa Bauxite market is characterized by a mix of large multinational mining corporations and regional players leveraging extensive bauxite reserves. Market leaders focus on capacity expansions, operational efficiency, and sustainability to maintain competitive advantages. Innovation is driven by advancements in beneficiation techniques and automation, improving yield and reducing environmental footprint. Rivalry intensifies as new entrants seek to capitalize on rising global aluminum demand, prompting strategic partnerships and investment in logistics infrastructure. Pricing strategies are influenced by global commodity trends and export tariffs, while companies differentiate through product quality and supply reliability. Regional cooperation and government policies also shape competitive dynamics by facilitating access to resources and infrastructure development. Future trends point towards increased vertical integration, digital transformation, and adoption of greener mining practices to address sustainability and compliance challenges.

Leading Companies in Africa Bauxite Market

- •Guinea Alumina Corporation (Guinea)

- •BHP Group (Australia)

- •Alufer Mining Limited (Guinea)

- •China Hongqiao Group Limited (China)

- •Sierra Mineral Holdings (Sierra Leone)

- •Mozambique Aluminum Company (Mozambique)

- •Rio Tinto Group (United Kingdom/Australia)

- •Ghana Bauxite Company (Ghana)

- •Alcoa Corporation (United States)

- •Vale S.A. (Brazil)

- •Eramet Group (France)

- •South32 Limited (Australia)

- •Minera Alumbrera (Argentina)

- •Norsk Hydro ASA (Norway)

- •Aluminium Bahrain B.S.C. (Bahrain)

- •Alumina Limited (Australia)

- •Jiangxi Copper Corporation (China)

- •Alumicor Limited (South Africa)

- •Vedanta Resources (United Kingdom)

- •Marsa Maroc (Morocco)

- •Companhia Brasileira de Alumínio (Brazil)

- •China Minmetals Corporation (China)

- •Aluminium Corporation of China (China)

- •East African Mining Corporation (Kenya)

- •African Mining and Exploration plc (Nigeria)

Market Breakdown

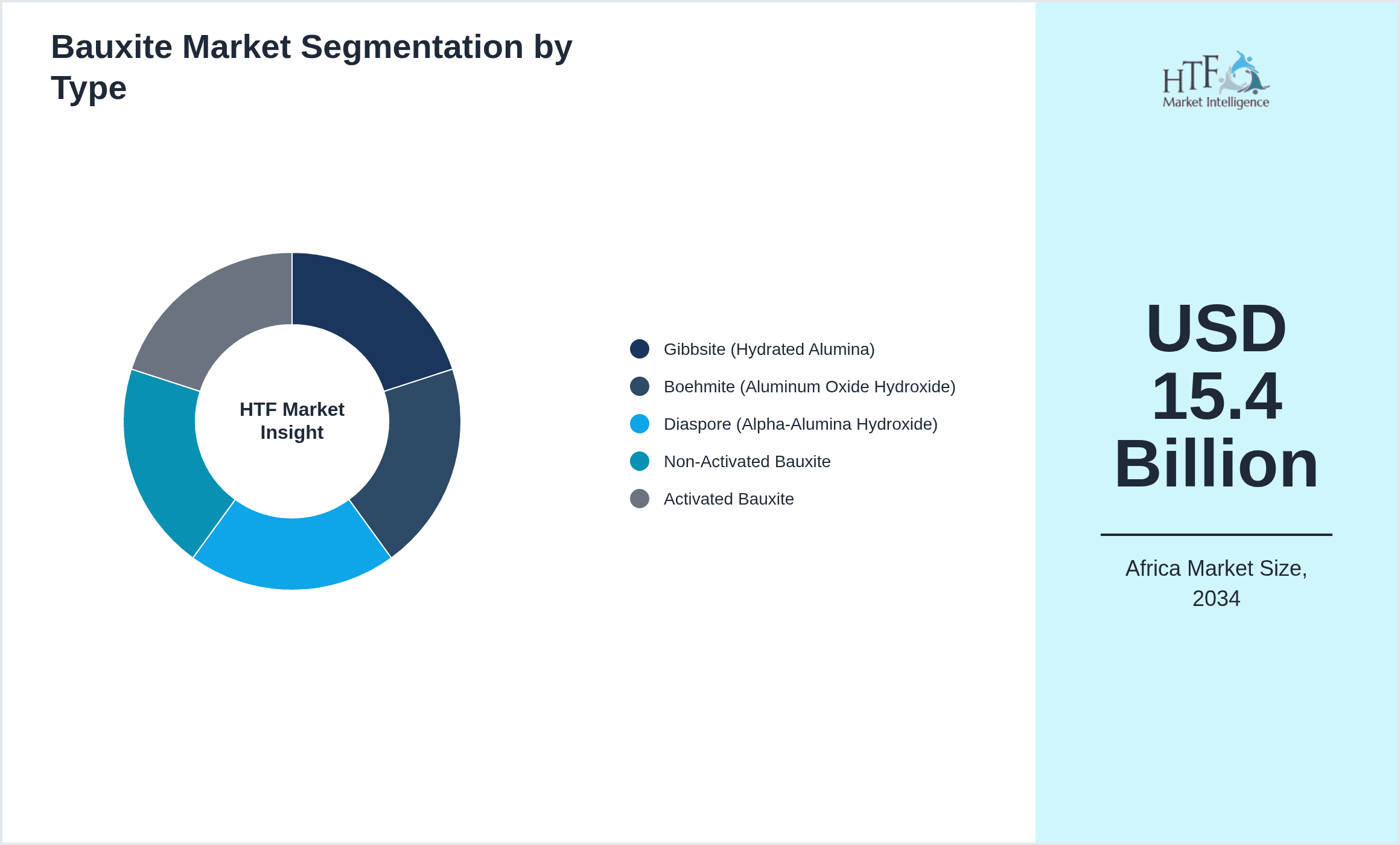

- •By Type

- ◦Gibbsite (Hydrated Alumina)

- ◦Boehmite (Aluminum Oxide Hydroxide)

- ◦Diaspore (Alpha-Alumina Hydroxide)

- ◦Non-Activated Bauxite

- ◦Activated Bauxite

- •By Application

- ◦Aluminum Production

- ◦Refractory Materials

- ◦Chemicals

- ◦Cement

- ◦Abrasives

- •By Mining Method

- ◦Open-Pit Mining

- ◦Underground Mining

- ◦Hydraulic Mining

- •By End-User Industry

- ◦Metallurgical Industry

- ◦Construction Industry

- ◦Chemical Industry

- ◦Abrasive Manufacturing

Growth Dynamics

- •Increasing global demand for aluminum, driven by sectors such as automotive and construction, significantly propels Africa's bauxite market growth, with countries like Guinea expanding mining capacity to meet export requirements.

- •Technological advancements in ore beneficiation and processing improve yield and quality of bauxite, enabling African producers to enhance competitiveness and reduce operational costs.

- •Government initiatives focusing on mining sector reforms and infrastructure development facilitate easier access to mining sites and export logistics, boosting market expansion.

- •Rising foreign direct investment from global mining firms fosters capital inflows and knowledge transfer, supporting modernization and sustainability efforts in the African bauxite industry.

- •Growing environmental awareness and stricter regulations encourage adoption of sustainable mining practices, enhancing market resilience and long-term viability.

Market Trends

- •The shift towards value-added processing within Africa sees increased investments in alumina refining facilities, aiming to capture higher margins and reduce dependency on raw ore exports.

- •Digitalization and automation in mining operations are becoming prevalent, improving operational efficiency, safety, and real-time monitoring of production and environmental parameters.

- •Strategic partnerships between mining companies and local governments promote community development and infrastructure projects, aligning business interests with social responsibility goals.

- •Sustainability and carbon footprint reduction initiatives are gaining traction, with companies investing in renewable energy and waste management technologies at mining sites.

- •Market diversification efforts include exploring new applications for bauxite in chemical and abrasive industries, broadening demand beyond traditional aluminum production.

Market Opportunities

- •Expansion of alumina refining capacity within Africa presents an opportunity to increase value addition and capture more revenue domestically, reducing raw material export dependency.

- •Developing infrastructure such as railways and ports can enhance export capabilities and reduce logistics costs, opening new markets for African bauxite producers.

- •Emerging applications of bauxite in specialty chemicals and refractory materials create niche markets with higher profit margins and less competition.

- •Investment in sustainable mining technologies offers long-term cost savings and compliance advantages, positioning companies favorably amid tightening environmental regulations.

- •Regional trade agreements within Africa can facilitate cross-border investments and supply chain integration, strengthening the competitive position of African bauxite globally.

Market Challenges

- •Infrastructural deficiencies such as inadequate transportation networks and unreliable power supply hinder efficient mining operations and increase operational costs in many African countries.

- •Regulatory uncertainties and lengthy permitting processes create barriers to entry and delay project development, affecting market growth and investor confidence.

- •Environmental concerns related to mining impacts, including deforestation and water pollution, pose reputational risks and may result in stricter compliance requirements.

- •Competition from established global bauxite producers outside Africa exerts pricing pressure and challenges market share retention for African exporters.

- •Limited technological adoption and skills shortages restrict operational efficiency and innovation capacity among smaller and mid-tier mining companies.

Regulatory Framework

- •Between 2019 and 2024, multiple African nations including Guinea and Ghana implemented mining code reforms mandating greater environmental safeguards, royalty adjustments, and community benefit sharing, which increased compliance complexities but improved sustainability oversight.

- •Enhanced enforcement of export regulations and licensing procedures emerged in Mozambique and Sierra Leone, aiming to curb illegal mining activities and ensure equitable resource nationalization.

- •Safety standards aligned with international best practices were adopted regionally, requiring improved worker protections and operational safety protocols across bauxite mining sites.

- •Government incentives for foreign investment in mining infrastructure, including tax breaks and streamlined approvals, were introduced to stimulate capital inflows and industry modernization.

- •Environmental impact assessment (EIA) requirements became more rigorous, demanding comprehensive studies before project approvals, thereby increasing project timelines but promoting ecological preservation.

Market Intelligence

- •15th January 2025, Guinea Alumina Corporation announced the commissioning of a new bauxite processing plant equipped with state-of-the-art beneficiation technology designed to increase alumina yield by 20%, targeting both domestic and export markets. This strategic expansion aligns with the company’s commitment to sustainable mining and enhancing supply chain efficiency in West Africa. The facility is expected to generate over 500 direct jobs and strengthen Guinea’s position as a global bauxite supplier. Source: Official Company Announcement

- •8th March 2025, Alufer Mining Limited unveiled a strategic partnership with a European technology provider to implement automation and digital monitoring systems in their bauxite mines across Guinea. This initiative aims to improve operational safety, reduce costs, and optimize resource utilization. The integration of real-time data analytics is projected to enhance decision-making processes and environmental compliance, contributing to long-term sustainable growth. Source: Industry Publication

- •22nd June 2024, Mozambique Aluminum Company completed a significant acquisition of a mid-sized bauxite mine in the Tete province, expanding its resource base and production capacity by 15%. This move is part of the company’s strategic plan to diversify geographic presence within Africa and capitalize on rising global aluminum demand. The acquisition also includes commitments to local community development and environmental management programs. Source: Company Press Release

- •10th October 2024, Ghana Bauxite Company launched an innovative waste recycling program to convert mining tailings into usable construction materials. This initiative not only reduces environmental impact but also creates additional revenue streams and supports circular economy principles. The program has received positive feedback from government agencies and industry stakeholders, reinforcing the company’s leadership in sustainable mining practices. Source: Official Website

Regional Outlook

The Guinea currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Mozambique is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- South Africa

- Nigeria

- Kenya

- Algeria

- Zambia

- Morocco

- Ethiopia

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 7.8 Billion |

| Forecast Year Market Size | USD 15.4 Billion |

| CAGR | 7.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.1% |

| Scope of Report | Market is segmented by Type (Gibbsite (Hydrated Alumina), Boehmite (Aluminum Oxide Hydroxide), Diaspore (Alpha-Alumina Hydroxide), Non-Activated Bauxite, Activated Bauxite), Application (Aluminum Production, Refractory Materials, Chemicals, Cement, Abrasives), Mining Method (Open-Pit Mining, Underground Mining, Hydraulic Mining), End-User Industry (Metallurgical Industry, Construction Industry, Chemical Industry, Abrasive Manufacturing) |

| Regions Covered | South Africa, Nigeria, Kenya, Algeria, Zambia, Morocco, Ethiopia, Others |

| Key Companies | Guinea Alumina Corporation (Guinea), BHP Group (Australia), Alufer Mining Limited (Guinea), China Hongqiao Group Limited (China), Sierra Mineral Holdings (Sierra Leone), Mozambique Aluminum Company (Mozambique), Rio Tinto Group (United Kingdom/Australia), Ghana Bauxite Company (Ghana), Alcoa Corporation (United States), Vale S.A. (Brazil), Eramet Group (France), South32 Limited (Australia), Minera Alumbrera (Argentina), Norsk Hydro ASA (Norway), Aluminium Bahrain B.S.C. (Bahrain), Alumina Limited (Australia), Jiangxi Copper Corporation (China), Alumicor Limited (South Africa), Vedanta Resources (United Kingdom), Marsa Maroc (Morocco), Companhia Brasileira de Alumínio (Brazil), China Minmetals Corporation (China), Aluminium Corporation of China (China), East African Mining Corporation (Kenya), African Mining and Exploration plc (Nigeria) |

Africa Bauxite Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.