Global Smart Implants Devices Market Size, Growth & Revenue 2025-2034

Global Smart Implants Devices Market is segmented by Type (Active Implants, Passive Implants, Bioelectronic Devices, Smart Sensor Implants, Drug Delivery Implants), Application (Orthopedic, Cardiovascular, Neurological, Dental, Others), Service Type (Implant Design and Development, Post-implant Monitoring Services, Device Maintenance and Upgrades, Consultation and Training Services), Deployment Model (Cloud-connected Implants, On-premise Data Management, Hybrid Systems), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

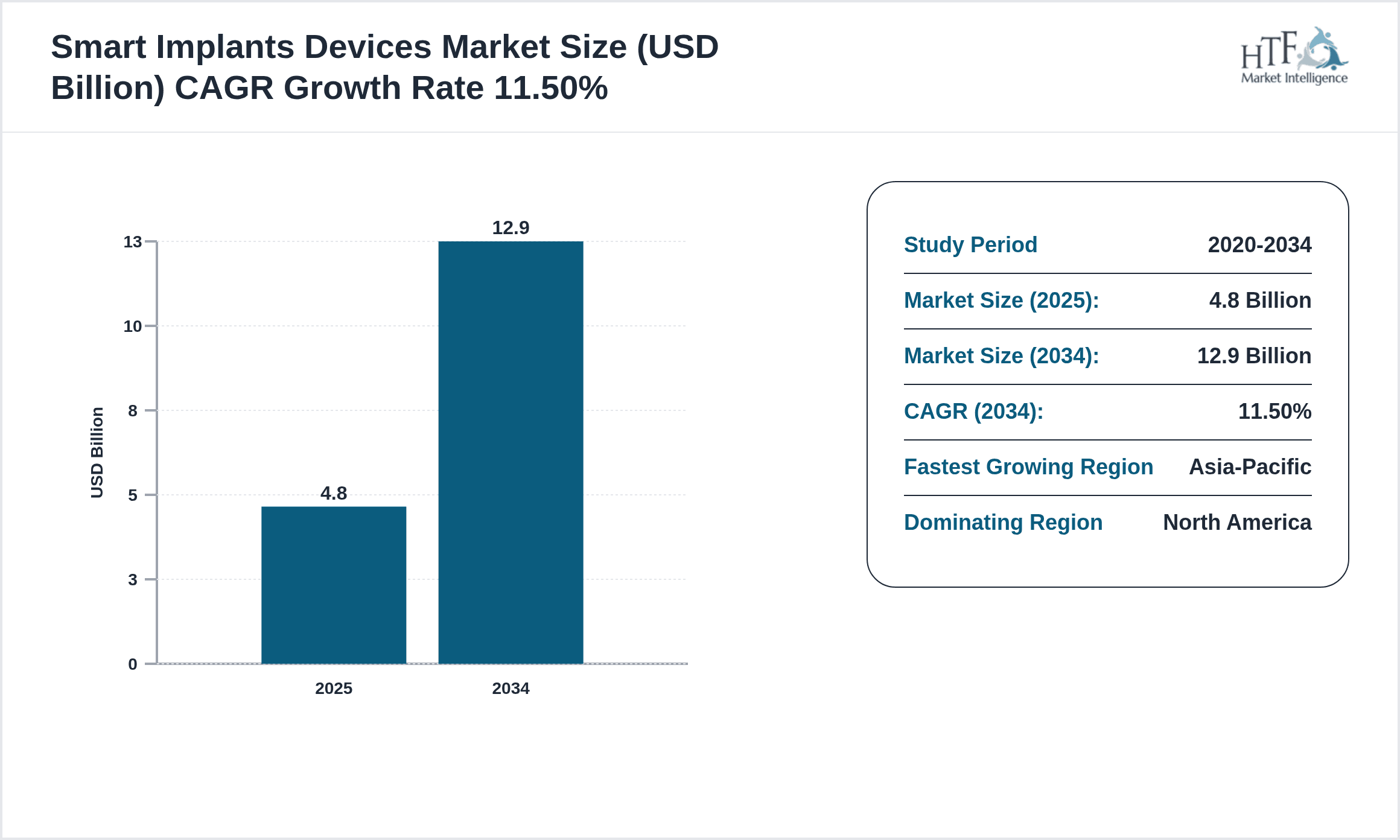

- •The global smart implants devices market represents a rapidly evolving sector within medical technology, focusing on implants that incorporate electronic and sensor technologies to enhance therapeutic efficacy and patient monitoring. This market includes devices used in orthopedic, cardiovascular, neurological, dental, and other medical applications, leveraging innovations such as wireless connectivity, biocompatible materials, and miniaturized electronics. The demand for smart implants is propelled by the rising incidence of chronic diseases, aging populations, technological advancements in implant design, and increasing preference for minimally invasive surgical procedures. Industry stakeholders are investing heavily in R&D to develop bioelectronic devices and active implants that offer improved treatment personalization and real-time health data capture. Regulatory frameworks worldwide are adapting to accommodate these complex devices, ensuring safety and efficacy while fostering innovation. Strategic collaborations among medical device manufacturers, technology firms, and healthcare providers are accelerating market growth. North America leads the market with advanced healthcare infrastructure and high adoption rates, while Asia-Pacific is the fastest growing region due to increasing healthcare investments, expanding patient base, and improving regulatory environment. The market is forecasted to grow at a CAGR of 11.5% from 2025 to 2034, reaching a valuation of USD 12.9 billion, driven by continuous technological breakthroughs and growing clinical acceptance globally.

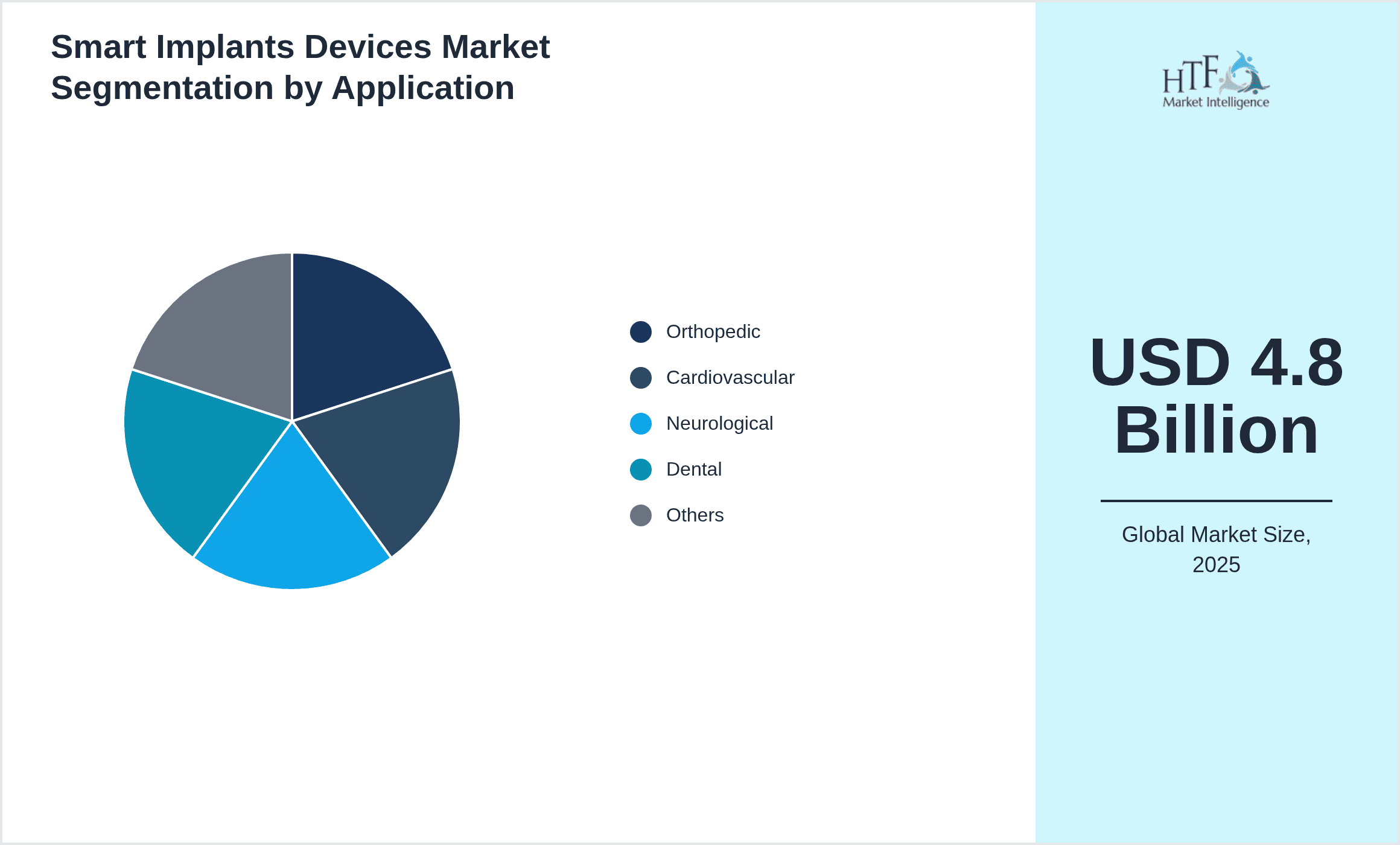

- •Key market highlights include the dominance of active implants as the leading product type, attributed to their wide use in cardiac rhythm management and neurostimulation therapies. Bioelectronic devices represent the fastest growing product segment, fueled by advances in neural interface technology and increasing demand for responsive therapeutic solutions. Orthopedic applications maintain a significant share due to the prevalence of joint disorders and fractures, while cardiovascular smart implants benefit from the rising burden of heart diseases worldwide. The Asia-Pacific region is emerging as a critical growth frontier, supported by growing healthcare expenditure, favorable government policies, and expanding medical device manufacturing capabilities. The market’s compound annual growth rate of 11.5% underscores the robust expansion and increasing adoption of smart implants across healthcare systems globally.

- •The strategic importance of the smart implants devices market lies in its potential to transform patient care through personalized, data-driven therapies and continuous health monitoring. These devices empower clinicians with actionable insights, enabling timely interventions and improved treatment outcomes. The integration of IoT and AI technologies with smart implants is opening new avenues for remote patient management and predictive diagnostics, which are critical in managing chronic conditions and enhancing quality of life. For industries, including medical device manufacturers, healthcare providers, and technology developers, this market offers substantial growth opportunities driven by innovation and unmet clinical needs. Investors and stakeholders are increasingly focusing on this space due to its dynamic growth prospects and potential to revolutionize healthcare delivery worldwide.

Competitive Landscape

The competitive environment of the global smart implants devices market is characterized by rapid technological innovation, strategic alliances, and aggressive product development to capture growing demand. Market players are investing significantly in R&D to enhance device functionality, miniaturization, and wireless communication capabilities. Competitive strategies include mergers and acquisitions to expand product portfolios, geographic reach, and technological expertise. Companies are adopting differentiated pricing models and enhancing distribution networks to increase market penetration across diverse regions. Innovation approaches focus on integrating AI, machine learning, and IoT technologies to improve implant intelligence and patient outcomes. Market positioning is influenced by regulatory approvals, patent portfolios, and strong relationships with healthcare providers. Barriers to entry include high development costs, stringent regulatory requirements, and the need for extensive clinical validation. Regional competition varies, with North America exhibiting a mature competitive landscape and Asia-Pacific offering emerging opportunities for new entrants. Future trends suggest increasing collaboration between technology firms and medical device manufacturers, fostering an ecosystem conducive to sustained innovation and market expansion.

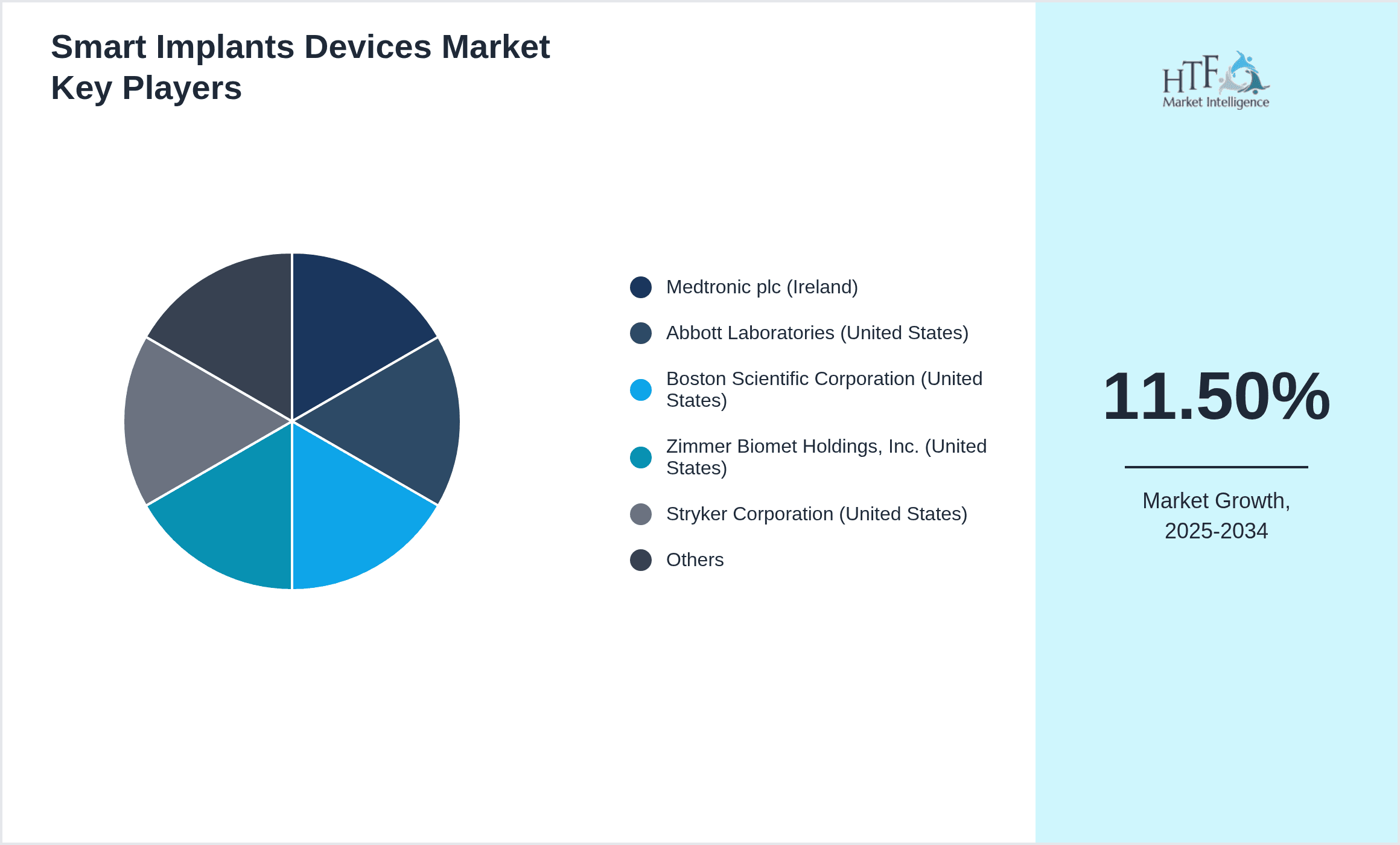

Leading Companies in Smart Implants Devices Market

- •Medtronic plc (Ireland)

- •Abbott Laboratories (United States)

- •Boston Scientific Corporation (United States)

- •Zimmer Biomet Holdings, Inc. (United States)

- •Stryker Corporation (United States)

- •Biotronik SE & Co. KG (Germany)

- •NeuroPace, Inc. (United States)

- •Cochlear Limited (Australia)

- •Smith & Nephew plc (United Kingdom)

- •LivaNova PLC (United Kingdom)

- •Boston Scientific Corporation (United States)

- •NuVasive, Inc. (United States)

- •Globus Medical, Inc. (United States)

- •Becton, Dickinson and Company (United States)

- •Elekta AB (Sweden)

- •Integra LifeSciences Holdings Corporation (United States)

- •Johnson & Johnson (United States)

- •Fresenius Medical Care AG & Co. KGaA (Germany)

- •Implantable Therapeutics, Inc. (United States)

- •Natus Medical Incorporated (United States)

- •Stimwave LLC (United States)

- •MicroPort Scientific Corporation (China)

- •Striker Neurovascular (United States)

- •Medacta International SA (Switzerland)

- •ResMed Inc. (United States)

Market Breakdown

- •By Type

- ◦Active Implants

- ◦Passive Implants

- ◦Bioelectronic Devices

- ◦Smart Sensor Implants

- ◦Drug Delivery Implants

- •By Application

- ◦Orthopedic

- ◦Cardiovascular

- ◦Neurological

- ◦Dental

- ◦Others

- •By Service Type

- ◦Implant Design and Development

- ◦Post-implant Monitoring Services

- ◦Device Maintenance and Upgrades

- ◦Consultation and Training Services

- •By Deployment Model

- ◦Cloud-connected Implants

- ◦On-premise Data Management

- ◦Hybrid Systems

Growth Dynamics

The growth of the global smart implants devices market is primarily driven by the increasing incidence of chronic diseases such as arthritis, cardiovascular disorders, and neurological conditions that require implantable therapeutic solutions. Technological advancements in microelectronics and sensor technologies have enabled the development of sophisticated implants capable of real-time physiological monitoring and targeted therapy. The rising geriatric population worldwide is expanding the patient base for orthopedic and cardiovascular implants, boosting demand significantly. Moreover, the adoption of minimally invasive surgical techniques and enhanced implant biocompatibility have improved patient outcomes, encouraging wider clinical acceptance. Government initiatives and funding to promote digital health and medical device innovation further stimulate market expansion. Increasing awareness among healthcare providers and patients about the benefits of smart implants reinforces growth prospects. Together, these factors contribute to the robust CAGR of 11.5% anticipated through 2034, positioning smart implants as a critical component of future healthcare delivery.

Market Trends

A prominent trend within the smart implants devices market is the integration of artificial intelligence and machine learning algorithms to enhance implant functionality and patient monitoring accuracy. Manufacturers are increasingly incorporating wireless communication protocols, such as Bluetooth and NFC, enabling seamless data transfer to healthcare professionals for remote monitoring. Personalized medicine is gaining traction, with implants tailored to individual patient anatomies and therapeutic needs through 3D printing and advanced imaging technologies. The convergence of smart implants with wearable devices is creating comprehensive health ecosystems, facilitating continuous data collection and proactive healthcare management. Sustainability and biocompatible material innovations are also influencing implant development to reduce adverse reactions and improve long-term device performance. These trends collectively reflect the market's evolution towards smarter, connected, and patient-centric implant solutions.

Market Opportunities

The global smart implants devices market presents significant opportunities in emerging economies where healthcare infrastructure is rapidly developing and the patient population is expanding. Untapped segments such as neurological and drug delivery implants offer potential for innovation and market penetration due to unmet clinical needs. Advances in bioelectronics and nanotechnology can lead to the creation of next-generation implants with enhanced precision and multifunctionality. Collaborations between medical device companies and technology firms can accelerate product development and broaden application scopes. Additionally, increasing government funding for digital health initiatives and favorable regulatory reforms in key regions create a conducive environment for market expansion. These opportunities enable stakeholders to capitalize on growing demand and technological progress to drive sustainable growth.

Market Challenges

Despite the promising growth prospects, the smart implants devices market faces challenges including high development and manufacturing costs that limit accessibility in price-sensitive regions. Stringent regulatory requirements and lengthy approval processes can delay product launches and increase compliance burdens. Technical complexities related to device miniaturization, long-term biocompatibility, and battery life pose ongoing development hurdles. Data security and patient privacy concerns arising from wireless and cloud-connected implants require robust cybersecurity measures. Furthermore, limited awareness among healthcare providers in emerging markets and resistance to adopting new technologies can impede market penetration. Addressing these challenges is critical for market players to achieve widespread adoption and realize the full potential of smart implant technologies.

Regulatory Framework

Between 2020 and 2025, regulatory bodies globally have enhanced frameworks to address the unique challenges posed by smart implants, focusing on safety, efficacy, and data security. The U.S. Food and Drug Administration (FDA) has introduced guidance on cybersecurity for medical devices, requiring manufacturers to implement risk management and post-market surveillance protocols. The European Union implemented the Medical Device Regulation (MDR) in 2021, setting stricter standards for clinical evaluation, traceability, and post-market monitoring, impacting market entry strategies. In Asia-Pacific, countries such as Japan and South Korea have updated their regulatory pathways to expedite approvals while maintaining rigorous safety standards. Additionally, standards organizations like the International Organization for Standardization (ISO) have published specific guidelines on implantable device biocompatibility and wireless communication. These evolving regulations necessitate comprehensive compliance efforts from manufacturers to ensure market access, patient safety, and alignment with technological advancements in smart implants.

Market Intelligence

- •15th January 2025, Medtronic plc announced the launch of its next-generation active smart implant designed for cardiac rhythm management, featuring enhanced wireless connectivity and AI-driven adaptive pacing algorithms. This device aims to improve patient outcomes by providing personalized therapy adjustments and remote monitoring capabilities, targeting the growing population with chronic heart conditions globally. The launch is expected to strengthen Medtronic’s market leadership and accelerate adoption in both developed and emerging markets. Source: Medtronic Official Press Release.

- •22nd March 2025, Abbott Laboratories introduced a bioelectronic implant system for neurological disorders that integrates real-time neural signal processing with cloud-based analytics. This innovation offers unprecedented precision in monitoring and treating epilepsy and Parkinson’s disease, enabling clinicians to optimize therapies dynamically. The product is positioned to disrupt traditional treatment paradigms and expand Abbott’s portfolio in neurotechnology. Source: Abbott Laboratories Corporate Announcement.

- •10th May 2025, Boston Scientific Corporation completed the acquisition of a pioneering smart sensor implant startup to bolster its portfolio in orthopedic and dental smart implants. This strategic move aims to leverage advanced sensor technologies and expand Boston Scientific's footprint in minimally invasive implant solutions. The acquisition is expected to enhance product innovation and provide competitive advantages in key regional markets. Source: Boston Scientific Press Release.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 12.9 Billion |

| CAGR | 11.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.3% |

| Scope of Report | Market is segmented by Type (Active Implants, Passive Implants, Bioelectronic Devices, Smart Sensor Implants, Drug Delivery Implants), Application (Orthopedic, Cardiovascular, Neurological, Dental, Others), Service Type (Implant Design and Development, Post-implant Monitoring Services, Device Maintenance and Upgrades, Consultation and Training Services), Deployment Model (Cloud-connected Implants, On-premise Data Management, Hybrid Systems) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Medtronic plc (Ireland), Abbott Laboratories (United States), Boston Scientific Corporation (United States), Zimmer Biomet Holdings, Inc. (United States), Stryker Corporation (United States), Biotronik SE & Co. KG (Germany), NeuroPace, Inc. (United States), Cochlear Limited (Australia), Smith & Nephew plc (United Kingdom), LivaNova PLC (United Kingdom), Boston Scientific Corporation (United States), NuVasive, Inc. (United States), Globus Medical, Inc. (United States), Becton, Dickinson and Company (United States), Elekta AB (Sweden), Integra LifeSciences Holdings Corporation (United States), Johnson & Johnson (United States), Fresenius Medical Care AG & Co. KGaA (Germany), Implantable Therapeutics, Inc. (United States), Natus Medical Incorporated (United States), Stimwave LLC (United States), MicroPort Scientific Corporation (China), Striker Neurovascular (United States), Medacta International SA (Switzerland), ResMed Inc. (United States) |

Global Smart Implants Devices Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.