South America Packaging Film Market - Outlook 2024-2034

South America Packaging Film Market is segmented by Type (Polyethylene (PE) Films, Polypropylene (PP) Films, Polyvinyl Chloride (PVC) Films, Polyester (PET) Films, Other Specialty Films), Application (Food Packaging, Medical Packaging, Industrial Packaging, Personal Care Packaging, Other Applications), End-Use Industry (Food & Beverage Industry, Healthcare & Pharmaceuticals, Consumer Goods, Automotive, Electronics), Distribution Channel (Direct Sales, Distributors & Wholesalers, E-commerce Platforms), and Geography (Brazil, Argentina, Chile, Peru, Colombia, Rest of South America)

Pricing

Report Overview

Executive Summary

- •The South America Packaging Film market is a vital segment of the regional packaging industry, focused on providing protective and functional plastic films for diverse applications including food preservation, medical products, industrial goods, and personal care items. This market spans various polymer types such as polyethylene, polypropylene, polyvinyl chloride, and polyester, each tailored to meet specific performance criteria like moisture resistance, durability, and transparency. Increasing consumer demand for packaged goods, coupled with rising urbanization and food safety regulations, drives growth across the region. The market also reflects a growing trend towards sustainable packaging solutions, with manufacturers investing in biodegradable and recyclable film technologies. Key use cases include extending shelf life of perishables, safeguarding pharmaceuticals, and enhancing product presentation. South America's market dynamics are shaped by significant contributions from Brazil, Argentina, and Chile, supported by expanding food processing sectors and healthcare infrastructure. Regulatory frameworks emphasize environmental compliance, further influencing product innovation and adoption. Overall, the packaging film market in South America is poised for steady growth, underpinned by technological advancements and evolving consumer preferences.

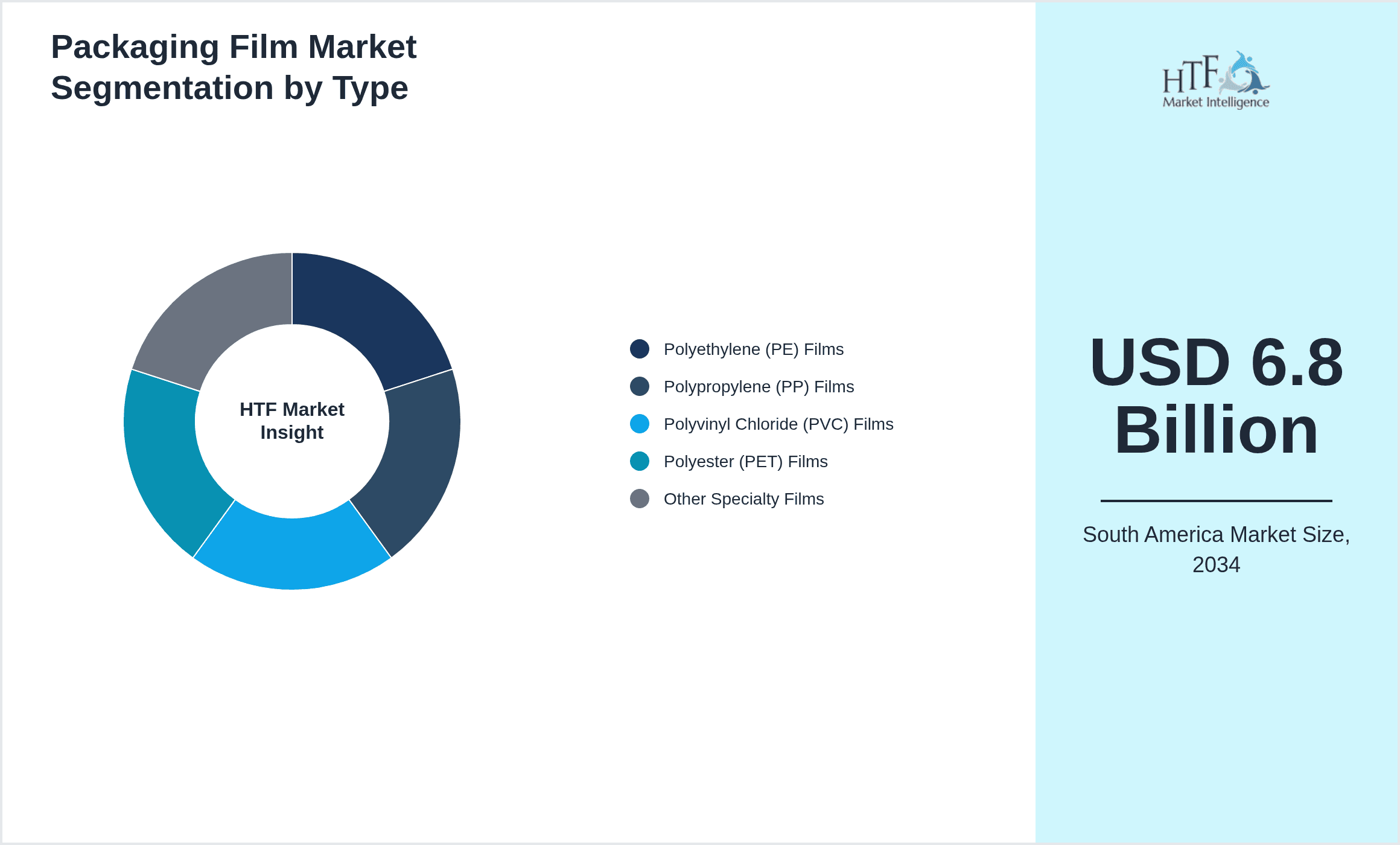

- •Key market highlights include a base market size of USD 3.5 Billion in 2024, with projections to reach USD 6.8 Billion by 2034, reflecting a CAGR of 6.9%. Brazil dominates with a 38% market share, followed by Argentina and Chile, the latter showing the fastest growth at 8.5% CAGR. Polyethylene leads product types due to its cost-effectiveness and versatility, while polyester films are rapidly gaining traction for high-barrier applications. Food packaging remains the largest application segment, driven by the expanding food processing industry and growing demand for packaged convenience foods. The market is also witnessing increased investments in sustainable films, responding to regulatory pressures and consumer demand for eco-friendly packaging. These factors collectively position the South America Packaging Film market for significant expansion through 2034.

- •This market presents substantial value propositions to packaging manufacturers, food processors, pharmaceutical companies, and retail sectors by enabling product protection, shelf life extension, and compliance with safety standards. The strategic importance of the packaging film industry in South America lies in its role supporting the supply chain efficiency and meeting consumer expectations for quality and sustainability. Market stakeholders benefit from innovations in material science and processing technologies that reduce costs and environmental impact. Additionally, robust growth in emerging economies within the region offers new opportunities for regional and global players to expand their footprint and leverage local manufacturing capabilities.

Competitive Landscape

The South America Packaging Film market exhibits a competitive landscape shaped by both multinational corporations and regional manufacturers. Market players focus heavily on innovation, particularly in developing sustainable and high-performance films to meet evolving regulatory and consumer demands. Competition centers on product differentiation through improved barrier properties, cost efficiency, and environmental friendliness. Companies engage in strategic partnerships and collaborations to expand distribution networks and enhance technological capabilities. Market rivalry intensifies as firms seek to capture growing demand in key countries such as Brazil and Chile, leveraging local production facilities to reduce costs and improve supply chain agility. Pricing strategies remain competitive, with emphasis on value-added products and customized solutions. The market also faces entry barriers due to capital-intensive manufacturing processes and stringent quality standards. Future trends indicate increasing consolidation via mergers and acquisitions, and growing investments in R&D to maintain competitive advantage and cater to niche market segments.

Prominent Players in Packaging Film Market

- •Bemis Company, Inc. (United States)

- •Amcor plc (Australia)

- •Berry Global, Inc. (United States)

- •Innovia Films Ltd. (United Kingdom)

- •Jindal Poly Films Ltd. (India)

- •Cosmo Films Ltd. (India)

- •Sealed Air Corporation (United States)

- •Uflex Ltd. (India)

- •Toray Industries, Inc. (Japan)

- •Mitsubishi Polyester Film GmbH (Germany)

- •SKC, Inc. (South Korea)

- •Coveris Holdings S.A. (Austria)

- •Clondalkin Group Holdings B.V. (Netherlands)

- •Polyplex Corporation Ltd. (India)

- •Taghleef Industries Inc. (United Arab Emirates)

- •Avery Dennison Corporation (United States)

- •Flex Films (India)

- •Constantia Flexibles Group GmbH (Austria)

- •Mondi Group (United Kingdom/Austria)

- •Treofan Group (Germany)

- •Jiangsu Sanfangxiang Group Co., Ltd. (China)

- •RKW Group (Germany)

- •Uflex S.A. (Brazil)

- •Plastipak Holdings, Inc. (United States)

- •Novelis Inc. (United States)

Market Breakdown

- •By Type

- ◦Polyethylene (PE) Films

- ◦Polypropylene (PP) Films

- ◦Polyvinyl Chloride (PVC) Films

- ◦Polyester (PET) Films

- ◦Other Specialty Films

- •By Application

- ◦Food Packaging

- ◦Medical Packaging

- ◦Industrial Packaging

- ◦Personal Care Packaging

- ◦Other Applications

- •By End-Use Industry

- ◦Food & Beverage Industry

- ◦Healthcare & Pharmaceuticals

- ◦Consumer Goods

- ◦Automotive

- ◦Electronics

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦E-commerce Platforms

Growth Dynamics

- •Rising demand for packaged food products in South America, driven by urbanization and changing consumer lifestyles, is boosting the need for durable and flexible packaging films that preserve freshness and extend shelf life.

- •Technological advancements in biodegradable and recyclable packaging films are stimulating market growth by addressing environmental concerns and regulatory mandates on plastic waste reduction.

- •Increasing healthcare infrastructure expansion and demand for sterile medical packaging solutions are propelling growth in medical-grade packaging films within the region.

- •Investment in modern manufacturing facilities and adoption of advanced extrusion and coating techniques enhance film quality and production efficiency, positively impacting market expansion.

- •Growing export activities in food and pharmaceutical sectors in countries like Brazil and Chile create additional demand for high-performance packaging films that meet international standards.

Market Trends

- •Adoption of sustainable packaging solutions including compostable and recyclable films is gaining momentum among manufacturers and consumers, reflecting increased environmental consciousness.

- •Integration of smart packaging technologies such as QR codes and freshness indicators within films is emerging, enhancing consumer engagement and product traceability.

- •Shift towards lightweight and multi-layer films combining barrier and mechanical properties to optimize material usage and reduce transportation costs is a notable trend.

- •Growth in e-commerce retailing drives demand for protective and tamper-evident packaging films, leading to new product developments tailored to shipping requirements.

- •Collaborations between chemical producers and packaging companies focus on developing bio-based polymers, aiming to replace conventional petrochemical-derived films.

Market Opportunities

- •Expanding food processing industries in Argentina and Peru offer untapped markets for packaging films with specific barrier properties to enhance product shelf life and safety.

- •Growing pharmaceutical manufacturing in South America opens avenues for medical-grade films that comply with stringent safety and hygiene standards.

- •Emerging demand for eco-friendly packaging materials presents opportunities for manufacturers to innovate and capture market share with biodegradable film products.

- •Increasing consumer preference for convenience foods fuels demand for resealable and microwavable packaging films, encouraging product development in this segment.

- •Digitalization in packaging, including smart film technologies and anti-counterfeit solutions, provides potential for value-added offerings and differentiation.

Market Challenges

- •Fluctuating raw material prices, especially for petrochemical-based polymers, create cost volatility impacting profit margins for packaging film manufacturers.

- •Stringent environmental regulations necessitate costly investments in sustainable technologies, posing financial challenges for small and medium players in the market.

- •Limited recycling infrastructure in several South American countries restricts circular economy initiatives and affects adoption rates of recyclable packaging films.

- •High import duties and logistical complexities increase costs and limit access to advanced packaging materials and machinery in some regional markets.

- •Competition from alternative packaging materials such as paper and glass challenges plastic film usage, requiring continuous innovation and marketing efforts.

Regulatory Framework

- •Between 2019 and 2024, South American countries have implemented stricter regulations on plastic waste management, including mandates on reducing single-use plastics and promoting recyclability in packaging films.

- •Brazil introduced the National Solid Waste Policy which enforces producer responsibility for packaging waste, encouraging manufacturers to adopt sustainable film materials and recycling initiatives.

- •Argentina has enacted labeling requirements for packaging to improve consumer awareness about recyclability and environmental impact, influencing packaging film formulations.

- •Chile's regulations promote the substitution of conventional plastics with biodegradable and compostable alternatives in packaging applications, accelerating innovation in film products.

- •Regional trade agreements include environmental provisions that impact packaging standards and encourage harmonization of sustainable packaging regulations across South America.

Market Intelligence

- •15th January 2025, Amcor plc announced the launch of its new biodegradable polyethylene film designed specifically for food packaging applications in South America. The product features enhanced barrier properties and complies with regional compostability standards, aiming to reduce plastic waste and meet increasing consumer demand for sustainable packaging. This innovation positions Amcor as a leading player in eco-friendly packaging solutions within the region, targeting major food processors in Brazil and Argentina. Source: Official Amcor press release

- •28th March 2025, Bemis Company, Inc. introduced an advanced multilayer polypropylene film for medical packaging with superior sterilization resistance and extended shelf life. The new film is tailored for pharmaceutical companies expanding their manufacturing footprint in Chile and Peru, supporting stringent regulatory compliance. The launch underscores Bemis's commitment to innovation and regional market expansion by addressing growing healthcare packaging needs. Source: Bemis corporate announcement

- •12th May 2025, Berry Global, Inc. expanded its manufacturing capacity in Brazil by inaugurating a new extrusion line dedicated to high-barrier polyester films. This investment enhances production capabilities to serve the fast-growing food packaging segment and enables faster delivery times to key South American customers. Berry Global's strategic expansion reflects confidence in the region's sustained demand growth and aligns with their sustainability goals by incorporating recycled content in film production. Source: Berry Global official website

- •7th August 2025, Innovia Films Ltd. announced a strategic partnership with a leading South American packaging distributor to introduce innovative cellulose-based films in the region. These films offer excellent biodegradability and strength, targeting the personal care and specialty food markets. The collaboration aims to accelerate adoption of sustainable packaging solutions and broaden Innovia’s footprint in emerging markets across South America. Source: Innovia Films press release

Regional Outlook

The Brazil currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Chile is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Brazil

- Argentina

- Chile

- Peru

- Colombia

- Rest of South America

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.5 Billion |

| Forecast Year Market Size | USD 6.8 Billion |

| CAGR | 6.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.7% |

| Scope of Report | Market is segmented by Type (Polyethylene (PE) Films, Polypropylene (PP) Films, Polyvinyl Chloride (PVC) Films, Polyester (PET) Films, Other Specialty Films), Application (Food Packaging, Medical Packaging, Industrial Packaging, Personal Care Packaging, Other Applications), End-Use Industry (Food & Beverage Industry, Healthcare & Pharmaceuticals, Consumer Goods, Automotive, Electronics), Distribution Channel (Direct Sales, Distributors & Wholesalers, E-commerce Platforms) |

| Regions Covered | Brazil, Argentina, Chile, Peru, Colombia, Rest of South America |

| Key Companies | Bemis Company, Inc. (United States), Amcor plc (Australia), Berry Global, Inc. (United States), Innovia Films Ltd. (United Kingdom), Jindal Poly Films Ltd. (India), Cosmo Films Ltd. (India), Sealed Air Corporation (United States), Uflex Ltd. (India), Toray Industries, Inc. (Japan), Mitsubishi Polyester Film GmbH (Germany), SKC, Inc. (South Korea), Coveris Holdings S.A. (Austria), Clondalkin Group Holdings B.V. (Netherlands), Polyplex Corporation Ltd. (India), Taghleef Industries Inc. (United Arab Emirates), Avery Dennison Corporation (United States), Flex Films (India), Constantia Flexibles Group GmbH (Austria), Mondi Group (United Kingdom/Austria), Treofan Group (Germany), Jiangsu Sanfangxiang Group Co., Ltd. (China), RKW Group (Germany), Uflex S.A. (Brazil), Plastipak Holdings, Inc. (United States), Novelis Inc. (United States) |

South America Packaging Film Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.