Europe Petrochemical Catalysts Market Size, Growth & Revenue 2024-2034

Europe Petrochemical Catalysts Market is segmented by Catalyst Type (Zeolite Catalysts, Metal Oxide Catalysts, Silica-Alumina Catalysts, Molecular Sieves, Others), Application Area (Refining, Olefins Production, Polyolefins, Aromatics, Others), End-Use Sector (Petrochemical Plants, Refineries, Polymer Manufacturing Units, Chemical Intermediates Producers), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Petrochemical Catalysts market is a specialized segment within the chemical manufacturing industry focusing on catalysts that facilitate essential petrochemical processes such as refining, olefins production, polyolefins formation, and aromatics synthesis. This market includes diverse catalyst types like zeolite catalysts known for their shape-selective properties, metal oxide catalysts for oxidation and hydrogenation reactions, silica-alumina catalysts widely used in fluid catalytic cracking, and molecular sieves for selective adsorption and separation. The scope covers catalyst development, manufacturing, and application within Europe’s robust petrochemical hubs, including Germany, France, and the United Kingdom. These catalysts improve process efficiency, product quality, and environmental compliance, addressing the evolving demands of petrochemical industries. The market is influenced heavily by technological innovation, stringent environmental regulations, and the transition towards sustainable feedstocks and processes, positioning catalysts as critical enablers of the European petrochemical sector's growth and competitiveness.

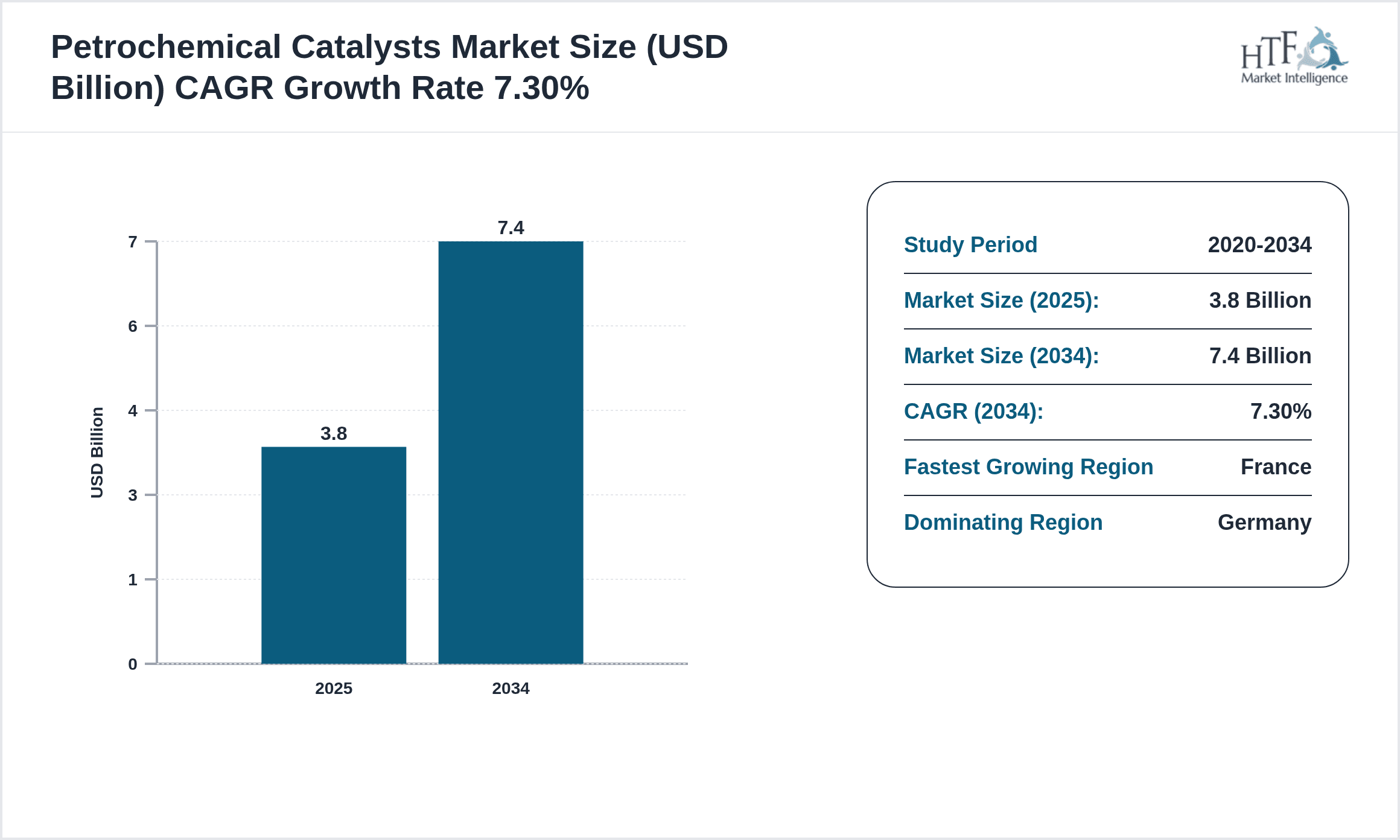

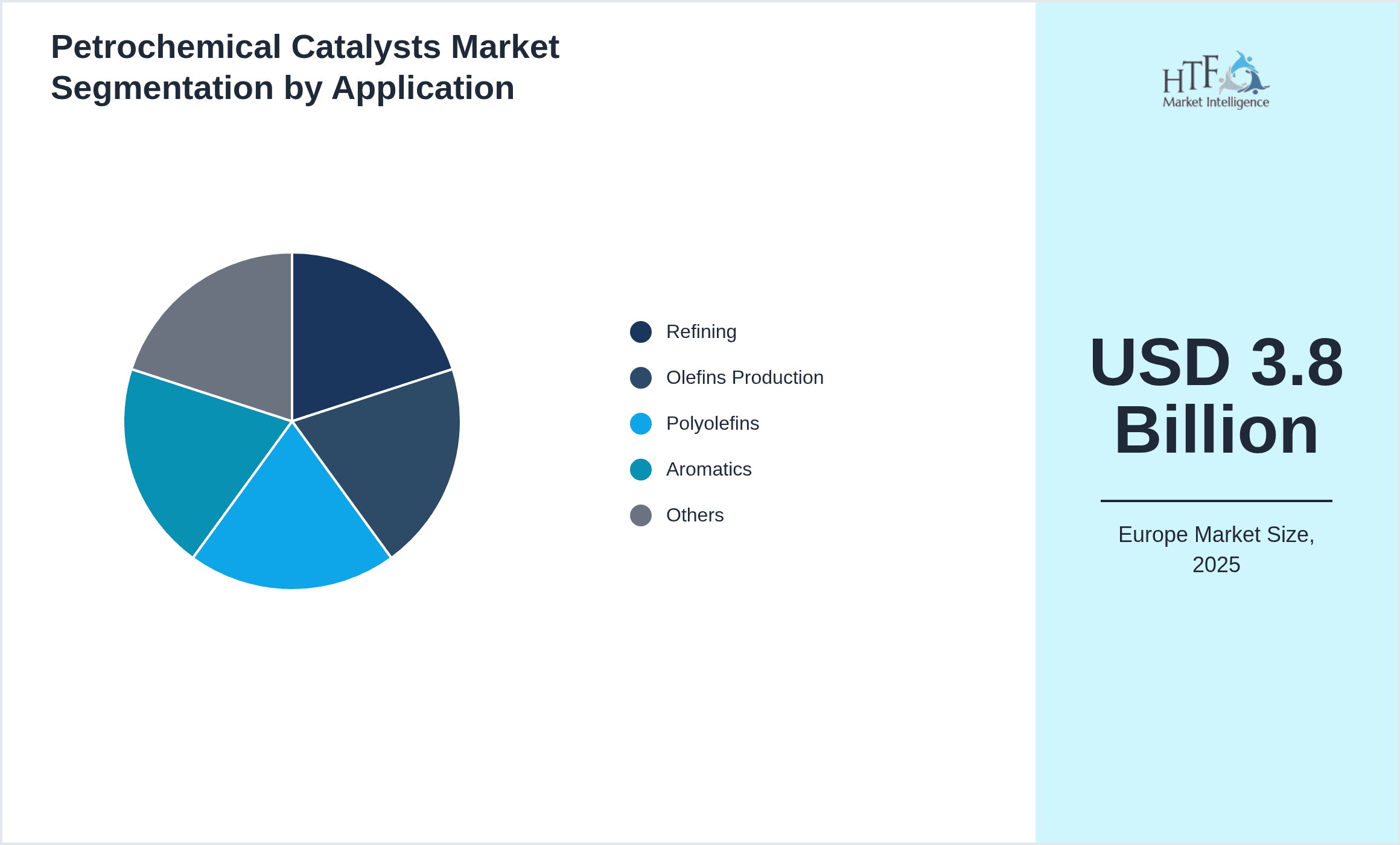

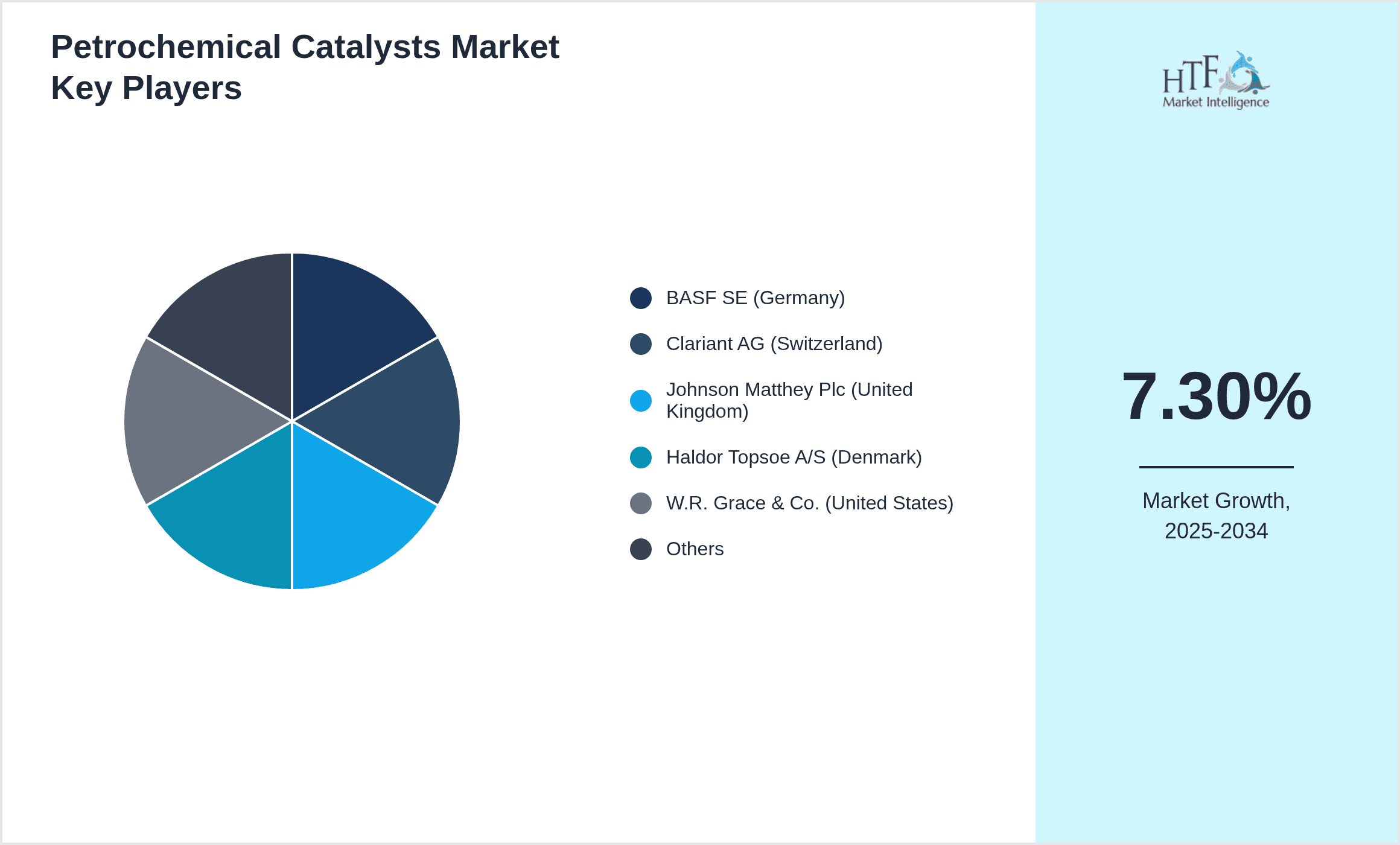

- •Key market highlights include a projected compound annual growth rate (CAGR) of 7.3% from 2024 to 2034, driven by increased demand for advanced catalysts in refining and polyolefins production. The market valuation is estimated at USD 3.8 Billion in 2024, expected to reach USD 7.4 Billion by 2034. Zeolite catalysts dominate the product segment due to their extensive use in refining and cracking processes, while metal oxide catalysts are emerging as the fastest-growing type, favored for their effectiveness in oxidation reactions. Germany leads as the dominant regional market with a 28% share, followed by France growing rapidly at a 9.1% CAGR. Applications in refining and olefins production account for the largest shares, reflecting Europe's focus on fuel production and basic chemicals manufacturing.

- •The Europe Petrochemical Catalysts market offers strategic value to chemical manufacturers, refining companies, and catalyst producers by enabling process optimization, energy efficiency, and compliance with environmental standards. These catalysts are essential for meeting Europe's ambitious carbon reduction targets and circular economy initiatives, supporting the transition to cleaner and more sustainable petrochemical processes. The market's growth is underpinned by innovation in catalyst formulations, integration with digital process controls, and collaborative ventures among key industry players. Stakeholders benefit from the ability to reduce operational costs, enhance product yields, and improve feedstock flexibility, making this market a critical component of Europe’s industrial ecosystem and energy transformation strategies.

Competitive Landscape

The Europe Petrochemical Catalysts market is characterized by intense competition among multinational chemical companies, specialty catalyst manufacturers, and regional players. Market dynamics are shaped by continuous innovation in catalyst technologies, with companies investing heavily in R&D to develop catalysts that offer higher efficiency, selectivity, and longer operational lifespans. Competitive strategies include strategic partnerships, joint ventures, and capacity expansions to strengthen regional footprints. Firms also compete on sustainability credentials by developing eco-friendly catalysts that comply with stringent European environmental regulations. Pricing strategies focus on value-based pricing aligned with performance benefits, while customer relationships are fostered through technical support and customization services. Barriers to entry are significant due to high capital requirements, proprietary technologies, and established supply chains. The competitive landscape is further influenced by mergers and acquisitions, which consolidate market positions and expand product portfolios, ensuring that innovation and responsiveness to market needs remain pivotal in maintaining leadership.

Leading Companies in Petrochemical Catalysts Market

- •BASF SE (Germany)

- •Clariant AG (Switzerland)

- •Johnson Matthey Plc (United Kingdom)

- •Haldor Topsoe A/S (Denmark)

- •W.R. Grace & Co. (United States)

- •Axens (France)

- •Evonik Industries AG (Germany)

- •Shell Catalysts & Technologies (Netherlands)

- •Clariant Catalysts (Germany)

- •Sud-Chemie AG (Germany)

- •Zeochem AG (Switzerland)

- •Honeywell UOP (United States)

- •Cepsa Química (Spain)

- •Sasol Ltd. (South Africa)

- •Mitsubishi Chemical Corporation (Japan)

- •LyondellBasell Industries (Netherlands)

- •Nouryon (Netherlands)

- •Clariant International Ltd. (Switzerland)

- •Chemviron Carbon (Belgium)

- •Arkema SA (France)

- •Evonik Catalysts (Germany)

- •Tosoh Corporation (Japan)

- •Catalysts Technologies (Germany)

- •Borealis AG (Austria)

- •Linde plc (Ireland)

Market Breakdown

- •By Catalyst Type

- ◦Zeolite Catalysts

- ◦Metal Oxide Catalysts

- ◦Silica-Alumina Catalysts

- ◦Molecular Sieves

- ◦Others

- •By Application Area

- ◦Refining

- ◦Olefins Production

- ◦Polyolefins

- ◦Aromatics

- ◦Others

- •By End-Use Sector

- ◦Petrochemical Plants

- ◦Refineries

- ◦Polymer Manufacturing Units

- ◦Chemical Intermediates Producers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Rising demand for efficient refining catalysts in Europe’s mature oil refining sector is accelerating market growth, driven by the need to process heavier crude feeds and produce cleaner fuels meeting stringent EU emission standards.

- •Technological advancements in catalyst formulations, particularly in zeolite and metal oxide catalysts, are enhancing process selectivity and lifespan, enabling producers to increase throughput while reducing operational costs.

- •Increasing investments in polyolefins production capacity in Europe, fueled by demand for lightweight and recyclable plastics, are driving catalyst consumption in polymerization processes.

- •Government policies and environmental regulations promoting sustainable chemical manufacturing incentivize the adoption of advanced catalysts that reduce greenhouse gas emissions and improve energy efficiency.

- •Strategic collaborations between catalyst manufacturers and petrochemical companies foster innovation and customized solutions, accelerating market penetration and expanding end-use applications.

Market Trends

- •The shift toward bio-based feedstocks in Europe is prompting catalyst developers to innovate with bi-functional catalysts capable of processing renewable raw materials alongside conventional hydrocarbons.

- •Digitalization and data analytics integration in catalyst performance monitoring enable predictive maintenance and optimized process control, enhancing operational efficiency in petrochemical plants.

- •An increasing focus on circular economy principles is driving the development of recyclable catalysts and processes that minimize waste generation and facilitate catalyst regeneration.

- •Emerging trends include the use of nanotechnology in catalyst design, improving surface area and active site availability for superior catalytic activity and selectivity.

- •Collaborative innovation hubs in Europe are accelerating knowledge sharing and technology transfer among catalyst producers, research institutions, and end-users.

Market Opportunities

- •Expanding olefins production capacity in Eastern Europe presents untapped markets for advanced catalysts tailored to new petrochemical complexes and modernization projects.

- •Growing demand for specialty polymers and high-performance materials opens opportunities for catalyst innovations targeting niche applications with stringent quality requirements.

- •Integration of green hydrogen in refining and chemical synthesis processes offers potential for developing catalysts optimized for hydrogenation reactions under sustainable conditions.

- •Collaborations between catalyst manufacturers and technology startups can accelerate commercialization of novel catalyst materials and eco-friendly production methods.

- •Government incentives for decarbonization and energy-efficient technologies provide financial support for catalyst development projects aligned with Europe’s climate goals.

Market Challenges

- •High costs associated with developing and scaling advanced catalyst technologies pose financial challenges for smaller players and limit rapid market penetration.

- •Stringent environmental regulations require continuous catalyst innovation to meet evolving emission standards, increasing R&D pressure and compliance costs.

- •Fluctuating crude oil prices and feedstock availability impact demand for petrochemical catalysts, creating market volatility and planning uncertainties.

- •Competition from alternative catalyst technologies and imports from low-cost regions intensifies price pressures on European catalyst manufacturers.

- •Supply chain disruptions, including raw material shortages and logistical constraints, affect catalyst production schedules and delivery reliability.

Regulatory Framework

- •The European Union’s REACH regulation, updated between 2019 and 2024, mandates comprehensive chemical safety assessments for catalyst components, impacting formulation and usage standards across member states.

- •EU Emissions Trading System (ETS) revisions introduced in 2023 require petrochemical producers to reduce carbon emissions, incentivizing adoption of catalysts that improve process efficiency and lower greenhouse gas output.

- •The Industrial Emissions Directive (IED) sets strict limits on pollutants released from petrochemical operations, compelling catalyst suppliers to develop low-impact, high-performance products compliant with these norms.

- •National regulations in Germany and France have introduced additional standards for hazardous waste management related to spent catalysts, affecting disposal and recycling practices since 2021.

- •Government incentives and funding programs across Europe support research into sustainable catalyst technologies, reinforcing innovation aligned with the European Green Deal objectives.

Market Intelligence

- •15th January 2025, BASF SE announced the launch of a next-generation zeolite catalyst designed to enhance cracking efficiency and extend catalyst life in European refineries. This product integrates advanced pore structure modulation technology, enabling higher selectivity and reduced coke formation, which improves refinery throughput and lowers operational costs. The catalyst targets compliance with stringent EU sulfur regulations and offers compatibility with renewable feedstocks, reflecting BASF’s strategy to support sustainable refining processes. This innovation strengthens BASF's position in Europe’s catalyst market and aligns with evolving industry demands for cleaner fuels. Source: BASF Official Press Release

- •22nd March 2025, Johnson Matthey Plc introduced a proprietary metal oxide catalyst optimized for olefins production with improved resistance to deactivation and enhanced oxidative stability. This catalyst targets European petrochemical complexes aiming to expand ethylene and propylene output while reducing energy consumption. The product launch follows extensive pilot testing, demonstrating a 15% increase in catalyst lifespan and a 10% improvement in selectivity compared to legacy catalysts. Johnson Matthey’s innovation supports circular economy goals by facilitating feedstock flexibility and lowering carbon footprints. Source: Johnson Matthey Corporate News

- •5th June 2025, Clariant AG completed a strategic partnership with a leading European polymer manufacturer to co-develop silica-alumina catalysts tailored for next-generation polyolefin production. The collaboration aims to accelerate commercialization of catalysts with enhanced activity and recyclability features, supporting sustainable polymer manufacturing initiatives. This partnership reflects Clariant’s commitment to innovation and market expansion within Europe’s evolving petrochemical landscape, addressing demand for lightweight and eco-friendly plastic materials. Source: Clariant Annual Report

- •30th April 2025, Haldor Topsoe A/S expanded its European catalyst production capacity by inaugurating a new manufacturing facility in Denmark. The state-of-the-art plant focuses on advanced molecular sieve catalyst production aimed at aromatics and refining applications. This expansion enhances supply chain resilience and enables faster delivery to European customers, supporting growing demand and technological innovation. The facility incorporates sustainable manufacturing practices, including energy-efficient systems and waste reduction measures, aligning with Haldor Topsoe’s sustainability objectives. Source: Haldor Topsoe Corporate Announcement

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 7.4 Billion |

| CAGR | 7.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.1% |

| Scope of Report | Market is segmented by Catalyst Type (Zeolite Catalysts, Metal Oxide Catalysts, Silica-Alumina Catalysts, Molecular Sieves, Others), Application Area (Refining, Olefins Production, Polyolefins, Aromatics, Others), End-Use Sector (Petrochemical Plants, Refineries, Polymer Manufacturing Units, Chemical Intermediates Producers), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | BASF SE (Germany), Clariant AG (Switzerland), Johnson Matthey Plc (United Kingdom), Haldor Topsoe A/S (Denmark), W.R. Grace & Co. (United States), Axens (France), Evonik Industries AG (Germany), Shell Catalysts & Technologies (Netherlands), Clariant Catalysts (Germany), Sud-Chemie AG (Germany), Zeochem AG (Switzerland), Honeywell UOP (United States), Cepsa Química (Spain), Sasol Ltd. (South Africa), Mitsubishi Chemical Corporation (Japan), LyondellBasell Industries (Netherlands), Nouryon (Netherlands), Clariant International Ltd. (Switzerland), Chemviron Carbon (Belgium), Arkema SA (France), Evonik Catalysts (Germany), Tosoh Corporation (Japan), Catalysts Technologies (Germany), Borealis AG (Austria), Linde plc (Ireland) |

Europe Petrochemical Catalysts Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.