United States Perimeter Security Systems Market - United States Size & Outlook 2025-2034

United States Perimeter Security Systems Market is segmented by Product Type (Physical Barriers (Fences, Gates, Bollards), Electronic Surveillance Systems (CCTV, Thermal Cameras), Access Control Systems (Biometric, Card Readers), Intrusion Detection Sensors (Motion Detectors, Infrared Sensors), Integrated Perimeter Security Solutions), Application (Residential Security, Commercial Buildings, Industrial Facilities, Government Installations, Critical Infrastructure Protection), Deployment Model (Cloud-based Security Solutions, On-premise Systems, Hybrid Deployment), Service Type (Installation Services, Maintenance & Support, Monitoring Services, Consulting & Integration), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States Perimeter Security Systems Market is a critical segment within the broader security industry focused on safeguarding physical boundaries across residential, commercial, industrial, governmental, and critical infrastructure domains. It comprises a diverse array of solutions including physical barriers such as fences and gates, electronic surveillance systems involving CCTV and advanced imaging technologies, access control mechanisms like biometric authentication, intrusion detection sensors, and fully integrated security platforms that unify multiple technologies for comprehensive protection. This market's scope also extends to service components such as installation, system integration, and ongoing monitoring, reflecting a holistic approach to perimeter defense. Key drivers include increasing security concerns prompted by rising crime rates and terrorism threats, technological advancements in sensor and AI-powered detection, and regulatory mandates driving adoption across various sectors. The market addresses evolving demands for scalable, efficient, and reliable perimeter security solutions tailored to diverse environments and threat profiles, underpinning its strategic importance in national security and asset protection.

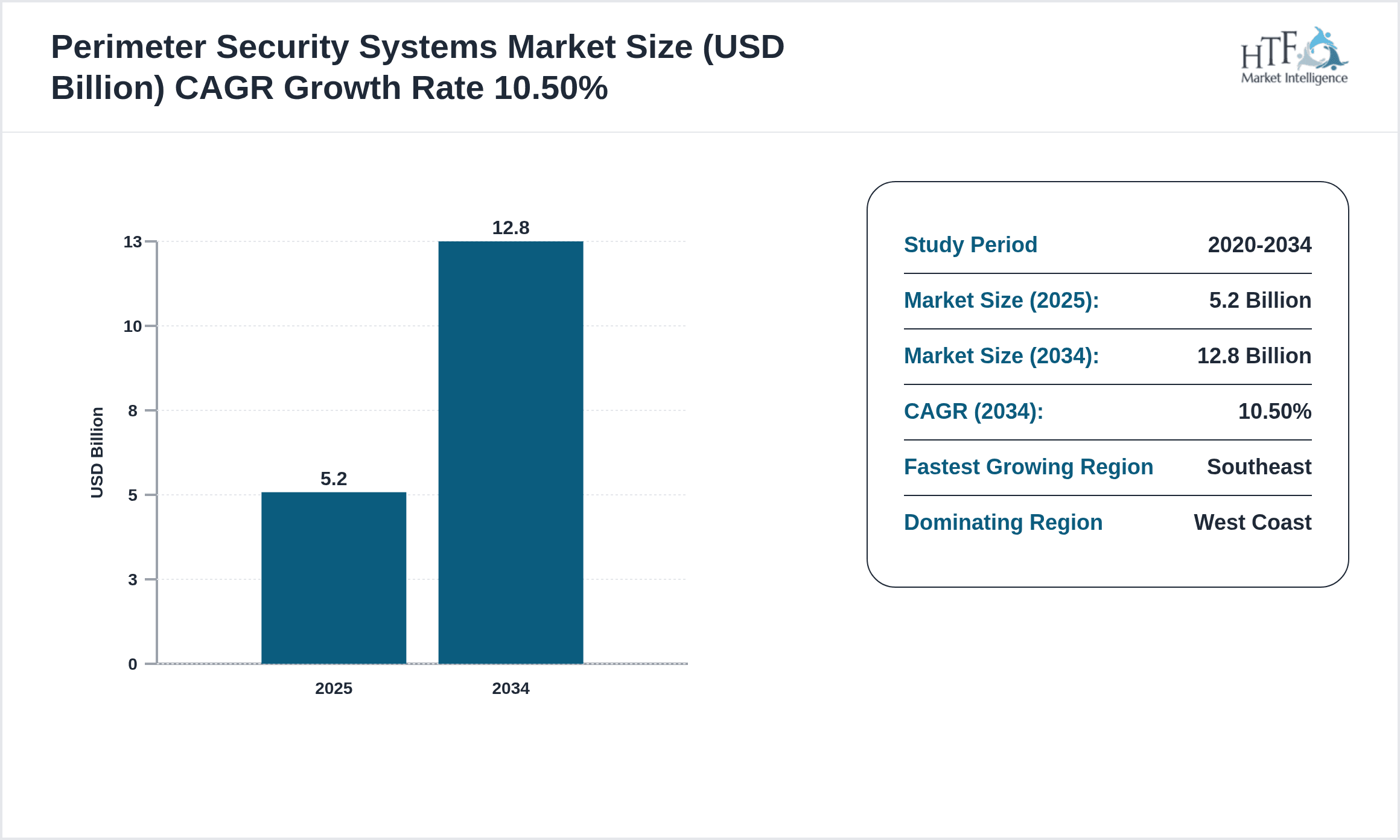

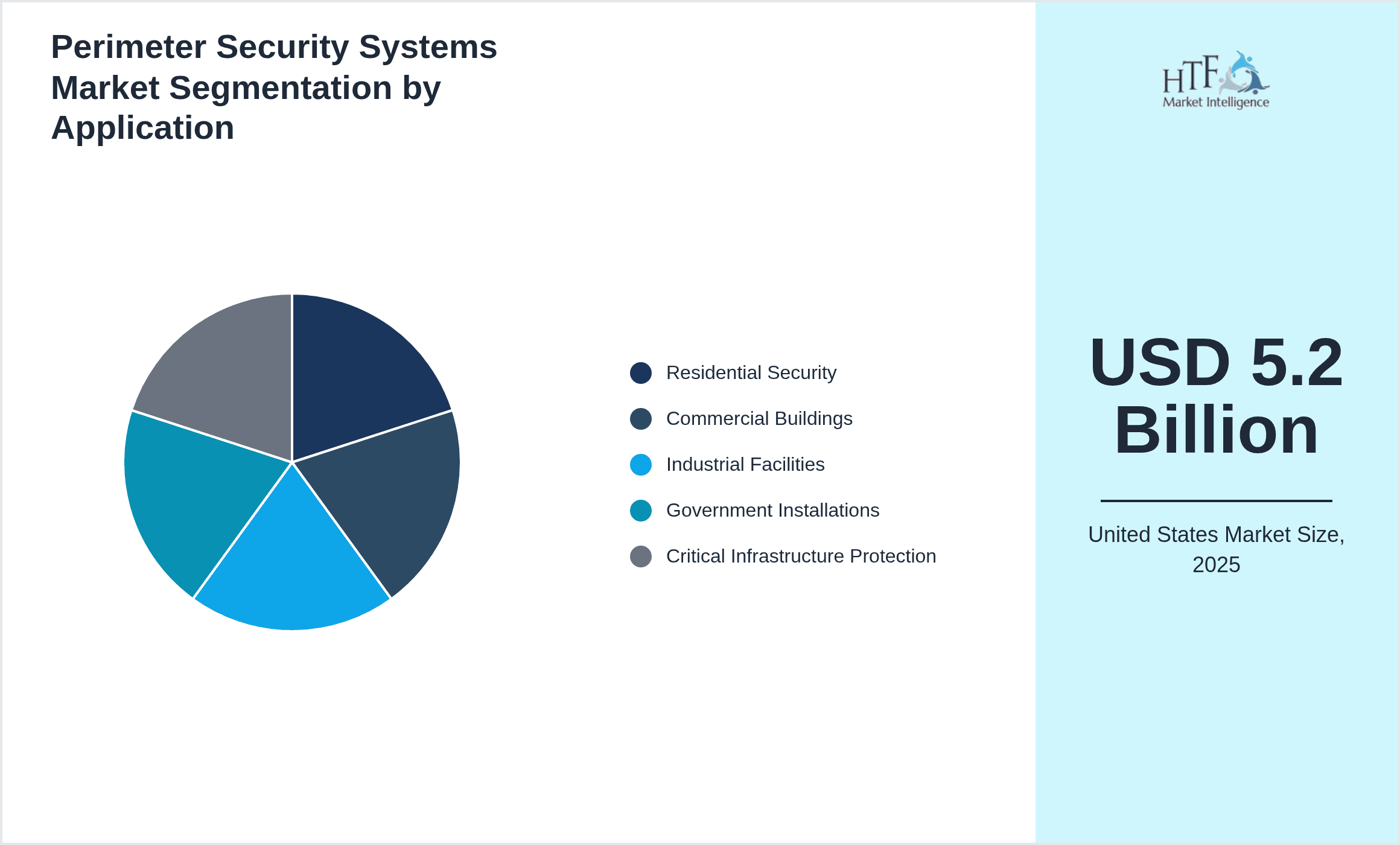

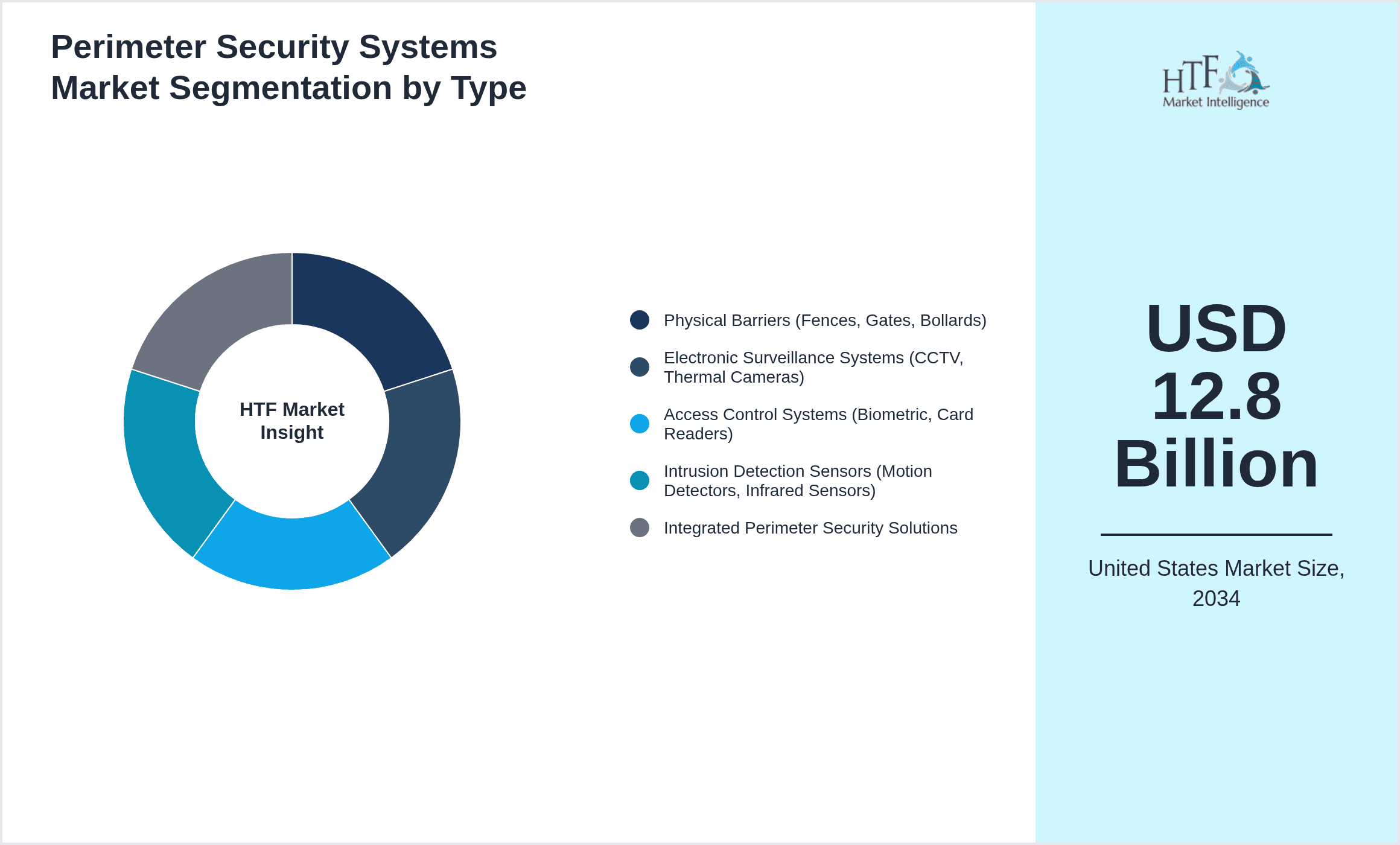

- •In 2025, the United States perimeter security systems market stands at USD 5.2 billion and is forecasted to grow to USD 12.8 billion by 2034, reflecting a compound annual growth rate (CAGR) of 10.5%. Electronic surveillance dominates the product segment, accounting for the largest market share, while integrated systems are the fastest-growing technology reflecting the trend toward unified security management. The West Coast region leads the market in terms of revenue share at 28%, with the Southeast region exhibiting the highest growth rate at 12.8% CAGR, driven by infrastructural development and heightened security investments. Residential and commercial applications remain the largest end-user segments, supported by increasing demand for smart home security and corporate facility protection.

- •This market provides strategic value to stakeholders including security solution providers, infrastructure developers, government agencies, and end users. The integration of advanced technologies such as AI, IoT, and cloud-based monitoring enhances operational efficiency and threat response capabilities. For industries, perimeter security systems are vital in risk mitigation, asset protection, and regulatory compliance. The market’s growth potential is fueled by escalating security challenges and technological innovation, positioning it as a significant area for investment and strategic development within the United States security ecosystem.

Competitive Landscape

The competitive landscape of the United States perimeter security systems market is characterized by intense rivalry among global and regional players striving to innovate and expand their market presence through differentiated product offerings, strategic partnerships, and acquisitions. Companies focus heavily on research and development to integrate cutting-edge technologies such as AI-driven analytics, IoT connectivity, and cloud-based management platforms, enhancing system capabilities and customer value. Market leaders leverage strong distribution networks and service capabilities to cater to diverse applications ranging from residential to critical infrastructure. Pricing strategies are balanced with value-added services to maintain competitiveness while addressing cost-sensitive segments. Barriers to entry remain significant due to the high technological complexity and stringent regulatory compliance requirements. The evolving competitive dynamics also include consolidation trends, with mergers and acquisitions enabling companies to broaden portfolios and geographic reach, further intensifying market competition and driving innovation.

Prominent Players in Perimeter Security Systems Market

- •Honeywell International Inc. (United States)

- •Johnson Controls International plc (United States)

- •Bosch Security Systems (Germany)

- •FLIR Systems Inc. (United States)

- •Axis Communications AB (Sweden)

- •ADT Inc. (United States)

- •Tyco International (United States)

- •Siemens AG (Germany)

- •Nortech Systems Incorporated (United States)

- •Sensormatic Electronics LLC (United States)

- •Vicon Industries, Inc. (United States)

- •Pelco Inc. (United States)

- •Hanwha Techwin Co., Ltd. (South Korea)

- •Assa Abloy AB (Sweden)

- •Avigilon Corporation (Canada)

- •Schneider Electric SE (France)

- •Dahua Technology Co., Ltd. (China)

- •Genetec Inc. (Canada)

- •FLIR Systems (United States)

- •Magal Security Systems Ltd. (Israel)

- •Bosch Sicherheitssysteme GmbH (Germany)

- •Panasonic Corporation (Japan)

- •Check Point Software Technologies Ltd. (Israel)

- •Johnson Controls (United States)

- •Alarm.com Holdings, Inc. (United States)

Market Breakdown

- •By Product Type

- ◦Physical Barriers (Fences, Gates, Bollards)

- ◦Electronic Surveillance Systems (CCTV, Thermal Cameras)

- ◦Access Control Systems (Biometric, Card Readers)

- ◦Intrusion Detection Sensors (Motion Detectors, Infrared Sensors)

- ◦Integrated Perimeter Security Solutions

- •By Application

- ◦Residential Security

- ◦Commercial Buildings

- ◦Industrial Facilities

- ◦Government Installations

- ◦Critical Infrastructure Protection

- •By Deployment Model

- ◦Cloud-based Security Solutions

- ◦On-premise Systems

- ◦Hybrid Deployment

- •By Service Type

- ◦Installation Services

- ◦Maintenance & Support

- ◦Monitoring Services

- ◦Consulting & Integration

Growth Dynamics

- •Increasing security concerns due to rising crime rates and terrorism threats are driving demand for advanced perimeter security systems across residential, commercial, and government sectors in the United States, resulting in significant market expansion.

- •Technological advancements such as AI-powered analytics, IoT integration, and cloud-based monitoring enhance system capabilities, offering improved detection accuracy and real-time response, which accelerates adoption among end users.

- •Government regulations and mandates focusing on critical infrastructure protection and national security compliance compel organizations to deploy comprehensive perimeter security solutions, boosting market growth.

- •The increasing trend of smart homes and smart city initiatives fosters demand for integrated perimeter security solutions that provide seamless interoperability and remote management features.

- •Rising investments in infrastructure development and industrial expansion in regions such as the Southeast and West Coast of the United States fuel the need for robust perimeter security systems, contributing to market growth.

- •Growing awareness about cybersecurity threats coupled with physical security integration encourages organizations to adopt unified security platforms, enhancing market potential for integrated systems.

- •Increasing availability of financing options and security-as-a-service models lowers entry barriers for small and medium enterprises, expanding the customer base for perimeter security products and services.

Market Trends

- •The adoption of AI and machine learning technologies in perimeter security systems is revolutionizing threat detection by enabling predictive analytics and reducing false alarms, as demonstrated by leading providers enhancing their product portfolios.

- •Integration of video surveillance with access control and intrusion detection into unified platforms is gaining traction, offering end users enhanced situational awareness and streamlined security management.

- •The rise of cloud-based perimeter security solutions facilitates remote monitoring and scalability, aligning with the increasing demand for flexible security infrastructures in commercial and government applications.

- •Sustainability considerations are influencing product development, with manufacturers focusing on energy-efficient surveillance equipment and eco-friendly materials for physical barriers.

- •Collaborations between technology firms and security service providers are accelerating innovation and expanding market reach, exemplified by strategic partnerships announced in recent years.

- •Consumer preference shifts towards smart, automated security solutions integrated with mobile platforms are shaping product design and service offerings in the residential segment.

- •Emergence of edge computing in perimeter security systems enhances real-time processing capabilities, reducing latency and dependence on centralized data centers.

Market Opportunities

- •Expanding urbanization and increasing government expenditure on critical infrastructure protection present significant growth avenues for perimeter security system providers in the United States.

- •The growing adoption of integrated security solutions combining physical and cybersecurity measures opens new market segments and cross-selling opportunities.

- •Emerging technologies such as drone surveillance and AI-based threat detection offer innovation potential for market participants to differentiate their offerings and capture new clientele.

- •Geographic expansion into underserved sub-regions like the Southeast and Midwest provides opportunities for market penetration and revenue diversification.

- •Development of security-as-a-service models and subscription-based offerings lowers adoption barriers, particularly among small and medium-sized enterprises, broadening the market base.

- •Strategic partnerships with construction and infrastructure firms enable early integration of perimeter security systems in new developments, enhancing sales pipelines.

- •Increasing demand for retrofit solutions in aging facilities creates opportunities for service providers specializing in system upgrades and integration.

Market Challenges

- •High initial investment costs for advanced perimeter security systems can deter adoption among cost-sensitive segments, limiting market penetration especially in small residential and commercial setups.

- •Integration complexities arising from combining multiple security technologies and legacy systems pose technical challenges and increase installation time and costs.

- •Privacy concerns and regulatory compliance related to surveillance and data handling may restrict deployment or necessitate costly adjustments, impacting market growth.

- •Shortage of skilled technicians and security professionals in certain regions hampers efficient installation, maintenance, and system management capabilities.

- •Rapid technological obsolescence requires continuous investment in R&D and product upgrades, pressuring profit margins and operational sustainability.

- •Market fragmentation with numerous small players creates intense competition and pricing pressures, complicating market consolidation efforts.

- •Supply chain disruptions affecting critical hardware components can delay product delivery and impact customer satisfaction.

Regulatory Framework

- •Between 2020 and 2025, the United States introduced enhanced critical infrastructure protection regulations mandating stricter perimeter security standards for government and utility facilities, requiring comprehensive surveillance and access control systems.

- •The Federal Trade Commission (FTC) increased oversight on data privacy related to surveillance technologies, imposing compliance requirements on data storage, handling, and consumer notification.

- •State-level regulations in California and New York have implemented specific guidelines for video surveillance usage in public and private properties to balance security needs with privacy rights.

- •The Department of Homeland Security (DHS) launched initiatives promoting cybersecurity integration with physical security systems, encouraging adoption through grants and incentive programs.

- •Several states have enacted laws governing the installation of biometric access control devices, requiring transparency, consent, and data protection measures in line with national privacy frameworks.

Market Intelligence

- •15th January 2025, Honeywell International Inc. unveiled an advanced Integrated Perimeter Security Platform combining AI-powered video analytics, access control, and intrusion detection into a unified cloud-based solution. Targeting critical infrastructure and commercial sectors, this product enhances threat detection accuracy and enables real-time monitoring via mobile applications. The launch aims to address increasing security complexities and operational efficiency demands in the United States market, positioning Honeywell as a leader in next-generation perimeter security solutions. Source: Official Honeywell press release.

- •22nd March 2025, Johnson Controls International plc introduced a new biometric access control system featuring facial recognition and liveness detection technologies. Designed for high-security government and industrial applications, the system integrates seamlessly with existing electronic surveillance networks and supports cloud-enabled remote management. This innovation reflects Johnson Controls’ commitment to enhancing perimeter security through advanced authentication methods and scalable deployment options. Source: Johnson Controls corporate announcement.

- •10th June 2025, ADT Inc. announced a strategic partnership with a leading AI software developer to integrate machine learning algorithms into their perimeter intrusion detection products. This collaboration aims to reduce false alarms and improve threat identification accuracy for residential and commercial clients across the United States. The initiative is expected to expand ADT’s product portfolio and strengthen its market position in intelligent security solutions. Source: ADT official news.

- •5th September 2025, FLIR Systems Inc. completed the acquisition of a startup specializing in drone-based perimeter surveillance technology. This move accelerates FLIR’s entry into aerial security monitoring, offering enhanced coverage and rapid threat response capabilities. The acquisition supports FLIR’s strategic goal of broadening its perimeter security offerings with innovative technologies tailored for large industrial and government facilities. Source: FLIR Systems press release.

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 5.2 Billion |

| Forecast Year Market Size | USD 12.8 Billion |

| CAGR | 10.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10% |

| Scope of Report | Market is segmented by Product Type (Physical Barriers (Fences, Gates, Bollards), Electronic Surveillance Systems (CCTV, Thermal Cameras), Access Control Systems (Biometric, Card Readers), Intrusion Detection Sensors (Motion Detectors, Infrared Sensors), Integrated Perimeter Security Solutions), Application (Residential Security, Commercial Buildings, Industrial Facilities, Government Installations, Critical Infrastructure Protection), Deployment Model (Cloud-based Security Solutions, On-premise Systems, Hybrid Deployment), Service Type (Installation Services, Maintenance & Support, Monitoring Services, Consulting & Integration) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | Honeywell International Inc. (United States), Johnson Controls International plc (United States), Bosch Security Systems (Germany), FLIR Systems Inc. (United States), Axis Communications AB (Sweden), ADT Inc. (United States), Tyco International (United States), Siemens AG (Germany), Nortech Systems Incorporated (United States), Sensormatic Electronics LLC (United States), Vicon Industries, Inc. (United States), Pelco Inc. (United States), Hanwha Techwin Co., Ltd. (South Korea), Assa Abloy AB (Sweden), Avigilon Corporation (Canada), Schneider Electric SE (France), Dahua Technology Co., Ltd. (China), Genetec Inc. (Canada), FLIR Systems (United States), Magal Security Systems Ltd. (Israel), Bosch Sicherheitssysteme GmbH (Germany), Panasonic Corporation (Japan), Check Point Software Technologies Ltd. (Israel), Johnson Controls (United States), Alarm.com Holdings, Inc. (United States) |

United States Perimeter Security Systems Market - United States Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.