Asia-Pacific Artificial Diamond For Jewelry Market Scope & Changing Dynamics 2024-2034

Asia-Pacific Artificial Diamond For Jewelry Market is segmented by Type (Chemical Vapor Deposition (CVD) Diamonds, High Pressure High Temperature (HPHT) Diamonds, Coated Diamonds, Composite Diamonds, Others), Application (Engagement Rings, Earrings, Necklaces, Bracelets, Others), Distribution Channel (Branded Retail Stores, Independent Jewelers, Online Retail, Wholesale Distributors), Manufacturing Technology (CVD Process, HPHT Process, Other Emerging Technologies), and Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

- •The Asia-Pacific Artificial Diamond For Jewelry market is defined by the synthetic production of diamonds tailored specifically for jewelry uses, delivering sustainable and cost-efficient alternatives to natural diamonds. This market includes diamonds produced by Chemical Vapor Deposition (CVD), High Pressure High Temperature (HPHT) methods, as well as coated and composite diamonds. Applications cover a broad spectrum of jewelry items such as engagement rings, earrings, necklaces, and bracelets. The industry operates within a dynamic environment influenced by technological innovations, growing ethical consumerism, and increasing demand for luxury goods across developing and developed Asia-Pacific nations. Market boundaries exclude industrial synthetic diamonds used for non-jewelry purposes. The sector is poised for robust growth driven by rising disposable incomes, expanding retail penetration including e-commerce, and supportive government policies encouraging sustainable luxury. Key countries shaping this market include China, India, Japan, South Korea, Australia, and Southeast Asia, each contributing distinct growth dynamics and consumer preferences.

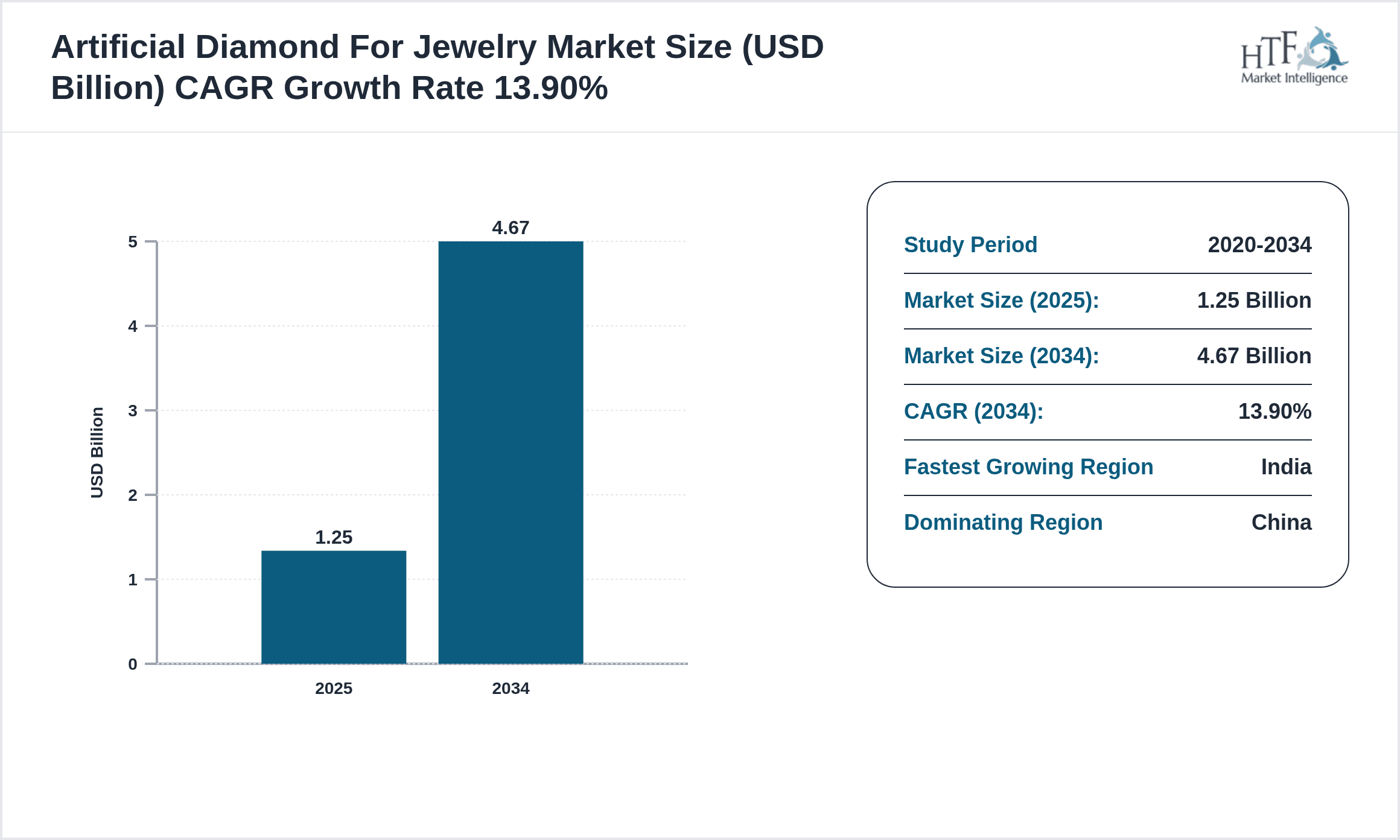

- •Key highlights of the Asia-Pacific Artificial Diamond For Jewelry market reveal a base market size of USD 1.25 Billion in 2024, expected to expand to USD 4.67 Billion by 2034 at a CAGR of 13.9%. China remains the dominant market with a 42% share, driven by strong manufacturing capabilities and consumer demand. India is the fastest-growing country with a CAGR of 17.5%, fueled by burgeoning middle-class purchasing power and increasing awareness of lab-grown diamond benefits. CVD diamonds hold the leading product position due to superior quality and cost advantages, while HPHT diamonds are gaining traction as the fastest-growing type. Engagement rings dominate end-use applications, closely followed by earrings, reflecting cultural trends and gifting practices prevalent across Asia-Pacific. This growth is supported by technological advances, ethical sourcing concerns, and digital retail platforms enabling wider market reach.

- •The Asia-Pacific Artificial Diamond For Jewelry market offers significant value propositions to jewelers, manufacturers, consumers, and investors by providing an innovative alternative to mined diamonds that addresses ethical and environmental concerns. The strategic importance of this market lies in its ability to meet the rising demand for luxury jewelry that is affordable and sustainable, aligning with shifting consumer preferences. Industry stakeholders benefit from enhanced supply chain control, reduced production costs, and the ability to customize offerings to diverse cultural tastes within Asia-Pacific. Furthermore, government support in various countries for high-tech manufacturing and export promotion bolsters market prospects. The expanding online retail ecosystem also facilitates direct consumer engagement and brand differentiation, making this market a focal point for long-term growth and profitability across the jewelry industry.

Competitive Landscape

The Asia-Pacific Artificial Diamond For Jewelry market exhibits intense competition characterized by rapid technological innovation, strategic partnerships, and aggressive market positioning. Key players focus on enhancing diamond quality through advancements in synthesis technologies like CVD and HPHT, differentiating their product portfolios by clarity, color, and cut precision. Market rivalry is heightened by increasing consumer preference for ethically sourced and affordable diamonds, pushing companies to innovate in branding and distribution strategies, including e-commerce and omni-channel retail. Competitive strategies include collaborations with jewelry designers, entry into emerging markets within Asia-Pacific, and diversification into coated and composite diamond offerings. Pricing strategies are tailored to capture both premium and mass-market segments, while intellectual property protection and quality certifications serve as differentiation tools. The market also witnesses consolidation through mergers and acquisitions, enhancing scale and technological capabilities. Regional competition varies, with China leading in production capacity and India emerging as a fast-growing consumer market, while Japan and South Korea emphasize quality and design innovation.

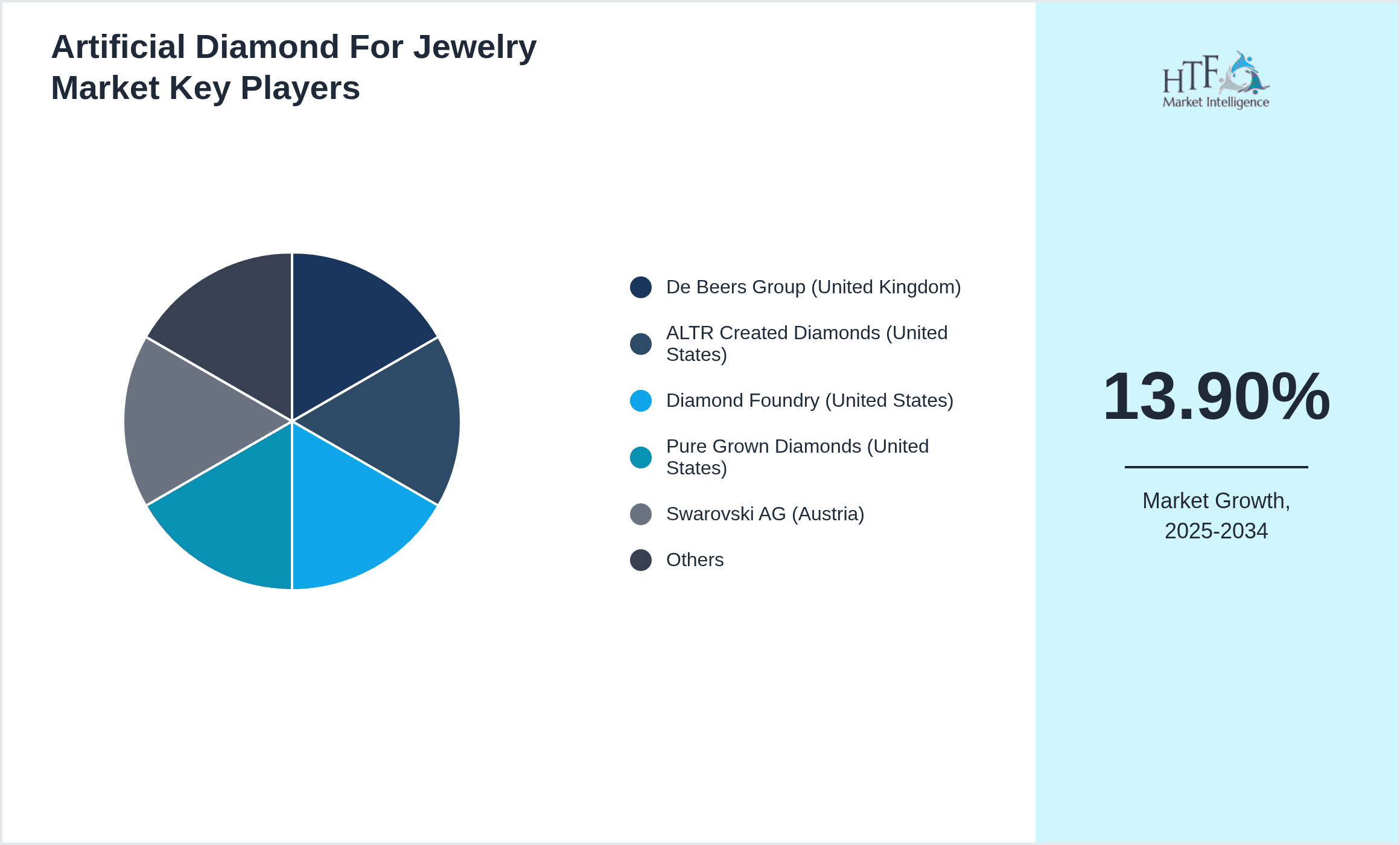

Leading Companies in Artificial Diamond For Jewelry Market

- •De Beers Group (United Kingdom)

- •ALTR Created Diamonds (United States)

- •Diamond Foundry (United States)

- •Pure Grown Diamonds (United States)

- •Swarovski AG (Austria)

- •Lucara Diamond Corp. (Canada)

- •Tiffany & Co. (United States)

- •Chow Tai Fook Jewellery Group (Hong Kong)

- •Laxmi Diamond (India)

- •Shenzhen Kingsgem Technology Co., Ltd. (China)

- •MiaDonna Inc. (United States)

- •IIa Technologies Pte Ltd (Singapore)

- •Scio Diamond Technology Corporation (United States)

- •Zircon Diamonds (India)

- •D.NEA (South Korea)

- •ALROSA (Russia)

- •Rio Tinto (Australia)

- •Kiran Gems (India)

- •LTI Diamond Technology (South Korea)

- •Sino Diamonds (China)

- •Shining Star Diamonds (India)

- •Diamond Nexus Labs (United States)

- •Venus Jewel (India)

- •Sarine Technologies Ltd. (Israel)

- •Diamond Standard (United States)

Market Breakdown

- •By Type

- ◦Chemical Vapor Deposition (CVD) Diamonds

- ◦High Pressure High Temperature (HPHT) Diamonds

- ◦Coated Diamonds

- ◦Composite Diamonds

- ◦Others

- •By Application

- ◦Engagement Rings

- ◦Earrings

- ◦Necklaces

- ◦Bracelets

- ◦Others

- •By Distribution Channel

- ◦Branded Retail Stores

- ◦Independent Jewelers

- ◦Online Retail

- ◦Wholesale Distributors

- •By Manufacturing Technology

- ◦CVD Process

- ◦HPHT Process

- ◦Other Emerging Technologies

Growth Dynamics

The Asia-Pacific Artificial Diamond For Jewelry market is propelled by increasing consumer awareness regarding the ethical and environmental benefits of lab-grown diamonds compared to mined stones. Rising disposable incomes and luxury spending in countries like China and India have expanded demand, especially among younger demographics seeking affordable yet high-quality alternatives. Technological advancements in CVD and HPHT processes have enhanced diamond quality and reduced production costs, further driving market penetration. Additionally, the proliferation of online retail platforms has expanded reach and accessibility for synthetic diamonds across urban and semi-urban areas. Government initiatives promoting sustainable manufacturing and exports bolster the regional supply chain. These combined factors create a favorable growth environment projected to sustain high double-digit CAGR through 2034, with significant opportunities in personalized jewelry and emerging markets within Southeast Asia.

Market Trends

Current market trends highlight a growing preference for ethically sourced and environmentally friendly jewelry, with artificial diamonds gaining acceptance as a socially responsible luxury choice. Increasing collaborations between synthetic diamond manufacturers and established jewelry brands are driving product innovation and consumer trust. Digital transformation is reshaping retail with virtual try-on technologies and augmented reality enhancing customer experiences. Customization and bespoke designs powered by AI and advanced cutting techniques are attracting millennials and Gen Z consumers. Furthermore, emerging markets in Southeast Asia are witnessing rapid adoption due to urbanization and increasing digital literacy. These trends collectively influence product development, marketing strategies, and distribution channels, positioning the Asia-Pacific artificial diamond market for sustained expansion.

Market Opportunities

The Asia-Pacific Artificial Diamond For Jewelry market presents substantial opportunities in expanding penetration into untapped regional markets such as Indonesia, Vietnam, and Malaysia, driven by rising middle-class incomes and evolving fashion consciousness. Investment in R&D to improve diamond synthesis efficiency and reduce costs can unlock new segments. Growing demand for customized and ethically produced jewelry opens avenues for niche product offerings and direct-to-consumer models via e-commerce. Strategic partnerships with luxury brands and digital marketing initiatives can enhance brand visibility and consumer engagement. Additionally, government support for high-tech manufacturing hubs in China, India, and South Korea offers incentives for production scale-up and exports, strengthening the regional value chain and global competitiveness.

Market Challenges

Key challenges include consumer skepticism regarding the value and authenticity of artificial diamonds compared to natural stones, which may limit adoption in traditional markets. High initial capital investment for advanced synthesis equipment creates entry barriers for smaller manufacturers. Regulatory complexities across different Asia-Pacific countries concerning certification, labeling, and import/export restrictions pose compliance challenges. The market also faces pricing pressure from natural diamond producers and counterfeit products. Supply chain disruptions, particularly due to geopolitical tensions and trade policies, can impact raw material availability. Additionally, rapid technological changes require continuous innovation, demanding significant R&D expenditure and skilled workforce availability, which are not uniformly accessible across the region.

Regulatory Framework

Between 2019 and 2024, several Asia-Pacific countries have introduced regulations mandating clear disclosure of artificial diamond origin to protect consumers and maintain market transparency. China implemented labeling standards requiring certification for lab-grown diamonds sold domestically, enhancing consumer confidence. India’s Bureau of Indian Standards (BIS) updated guidelines to include synthetic diamond specifications and testing protocols, facilitating standardized quality control. Japan reinforced import regulations ensuring compliance with ethical sourcing norms. Additionally, trade agreements promoting technology transfer and export facilitation have been enacted across ASEAN countries, supporting industry growth. These regulatory frameworks collectively improve market integrity, encourage ethical business practices, and provide a structured environment conducive to innovation and investment within the Asia-Pacific artificial diamond jewelry sector.

Market Intelligence

- •15th January 2024, Chow Tai Fook Jewellery Group launched a new collection featuring premium CVD diamonds, targeting millennials in China with advanced customization options and digital engagement strategies. The collection emphasizes sustainability and affordability, reinforcing the brand's leadership in the artificial diamond segment. This initiative aligns with rising demand for ethical luxury and is expected to boost market share significantly. Source: Chow Tai Fook Official Press Release.

- •10th September 2023, Laxmi Diamond announced the expansion of its HPHT diamond production facilities in Gujarat, India, aiming to triple output capacity by 2025. The investment enhances supply capabilities to meet growing domestic and export demand, positioning the company as a key supplier in Asia-Pacific. The move underscores commitment to technological advancement and cost competitiveness. Source: Industry Publication.

- •5th March 2024, Shenzhen Kingsgem Technology Co., Ltd. introduced a proprietary coating technology that improves the durability and brilliance of synthetic diamonds used in jewelry. This innovation provides enhanced product differentiation and is expected to attract premium retail partners across Southeast Asia. The company plans to license the technology to select collaborators. Source: Company Website.

- •20th November 2023, IIa Technologies Pte Ltd partnered with major online jewelry platforms in South Korea to offer virtual try-on experiences featuring lab-grown diamond collections. This collaboration leverages augmented reality to increase consumer engagement and conversion rates amid rising e-commerce trends. Source: Industry News Portal.

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 4.67 Billion |

| CAGR | 13.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 13.1% |

| Scope of Report | Market is segmented by Type (Chemical Vapor Deposition (CVD) Diamonds, High Pressure High Temperature (HPHT) Diamonds, Coated Diamonds, Composite Diamonds, Others), Application (Engagement Rings, Earrings, Necklaces, Bracelets, Others), Distribution Channel (Branded Retail Stores, Independent Jewelers, Online Retail, Wholesale Distributors), Manufacturing Technology (CVD Process, HPHT Process, Other Emerging Technologies) |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | De Beers Group (United Kingdom), ALTR Created Diamonds (United States), Diamond Foundry (United States), Pure Grown Diamonds (United States), Swarovski AG (Austria) |

Asia-Pacific Artificial Diamond For Jewelry Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.