Middle East Ceramic Kitchen Sink Market Scope & Changing Dynamics 2025-2034

Middle East Ceramic Kitchen Sink Market is segmented by Ceramic Kitchen Sink Type (Undermount Ceramic Sinks, Drop-in Ceramic Sinks, Farmhouse Ceramic Sinks, Double Bowl Ceramic Sinks, Single Bowl Ceramic Sinks), Application Sector (Residential Kitchens, Commercial Kitchens, Hospitality Sector, Institutional Kitchens, Renovation Projects), Installation Model (Built-in Installation, Integrated Installation, Self-supporting Installation), Surface Finish (Glossy Finish, Matte Finish, Textured Finish), and Geography (Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others)

Pricing

Report Overview

Executive Summary

- •The Middle East Ceramic Kitchen Sink market is characterized by a diverse range of ceramic sink types including undermount, drop-in, farmhouse, double bowl, and single bowl sinks that cater to various kitchen applications such as residential, commercial, hospitality, institutional, and renovation projects. This market operates through a value chain involving ceramic raw material suppliers, specialized sink manufacturers, distributors, and end-users including homeowners, contractors, and commercial kitchen operators. The market is influenced by rising urbanization, increasing disposable income, and a surge in hospitality infrastructure development across the Middle East. Additionally, regional preferences for durable, easy-to-maintain, and aesthetically pleasing ceramic kitchen sinks drive innovation in glazing and design features. The market also benefits from government initiatives promoting construction and modernization of kitchen spaces. Key drivers include growing demand from residential housing developments, expanding hotel and restaurant sectors, and renovation activities in established urban centers. Challenges such as raw material price volatility and competition from alternative materials exist but are offset by strong growth prospects. The market outlook from 2025 to 2034 anticipates a CAGR of 8.9%, propelled by increasing consumer awareness and evolving kitchen designs that emphasize functionality and style.

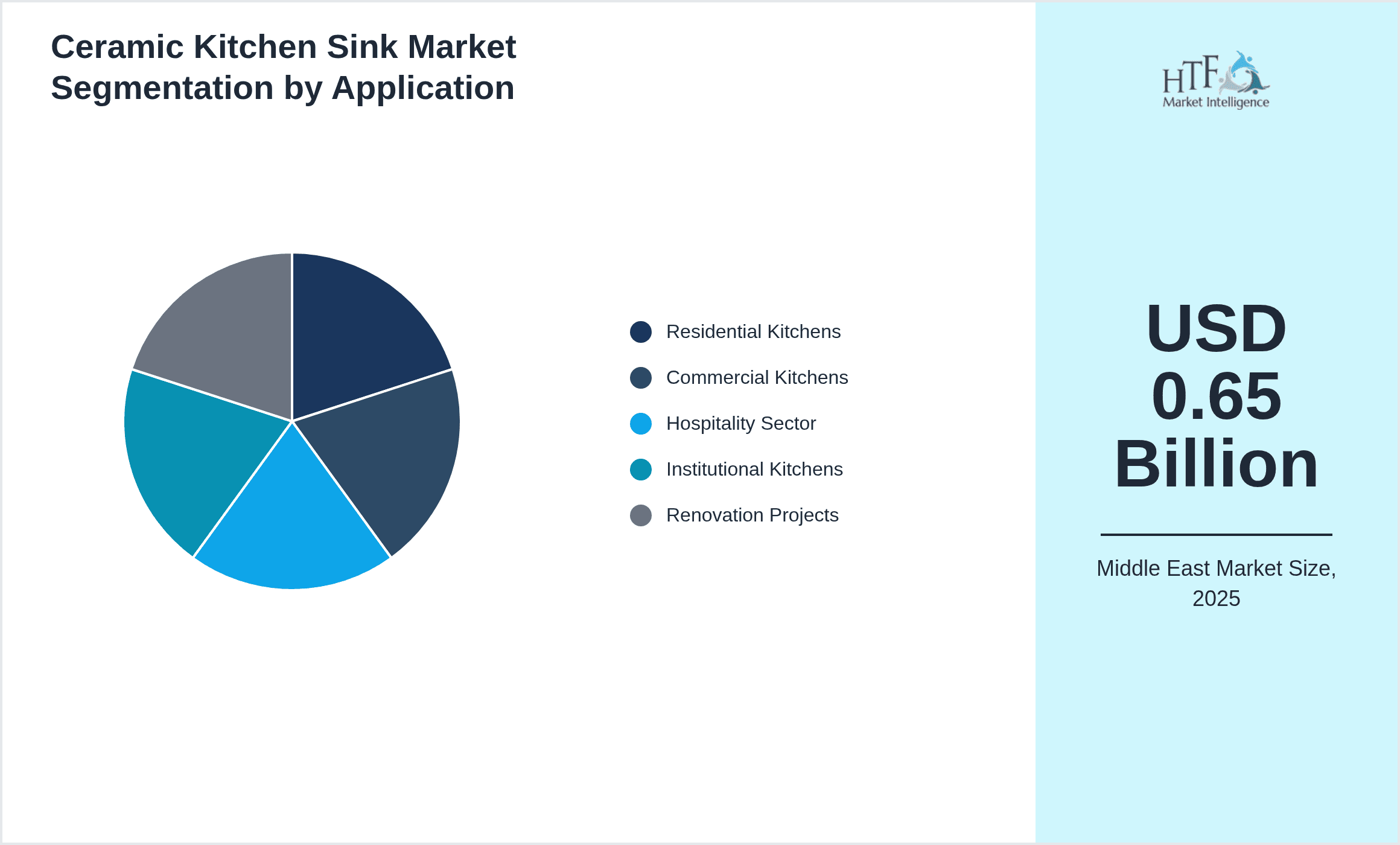

- •Key market highlights include a base market size of USD 0.65 Billion in 2025 expanding to USD 1.45 Billion by 2034, representing a robust CAGR of 8.9%. The United Arab Emirates dominates the regional market due to its advanced construction sector and hospitality industry, while Qatar exhibits the fastest growth driven by infrastructure investments and rising residential developments. Undermount ceramic sinks are the leading product type, favored for their sleek integration and ease of maintenance. Farmhouse ceramic sinks are the fastest growing segment as consumer tastes shift toward traditional and rustic kitchen aesthetics. Year-on-year growth averages 8.5%, reflecting consistent market expansion fueled by both new construction and renovation activities.

- •This market holds strategic importance for manufacturers, distributors, and designers within kitchen fixture industries. It offers opportunities for innovation in ceramic materials and designs aligned with regional preferences and sustainability trends. The market also supports stakeholders involved in urban development and hospitality sectors by supplying essential kitchen components. Investors benefit from the expanding middle-class population and government infrastructure programs that stimulate demand for quality kitchen fixtures. Overall, the Middle East Ceramic Kitchen Sink market presents a compelling value proposition for companies aiming to capitalize on evolving kitchen trends and regional economic growth.

Competitive Landscape

The competitive environment in the Middle East Ceramic Kitchen Sink market is defined by a blend of international manufacturers and regional suppliers vying for market share through innovation, quality, and distribution efficiency. Market players employ strategies such as product differentiation via advanced ceramic glazing techniques, customization to meet local aesthetic preferences, and partnerships with construction and hospitality companies to secure long-term contracts. Pricing strategies balance premium product offerings with competitively priced alternatives to address diverse consumer segments. Distribution channels encompass direct sales, retail partnerships, and e-commerce platforms, enhancing reach across urban and emerging markets in key countries. Additionally, companies are investing in sustainable manufacturing processes to align with increasing environmental regulations and consumer demands for eco-friendly products. Mergers and acquisitions, while limited in the recent period, are anticipated to rise as firms seek regional consolidation to leverage economies of scale and local expertise. The market’s entry barriers include the need for technological expertise in ceramic manufacturing and established relationships with construction and design firms. Regional competition is intensified by the presence of local ceramic producers offering cost-effective solutions tailored to Middle Eastern market nuances. Future competitive trends point towards digital marketing adoption, expanded product portfolios with smart kitchen integration, and enhanced after-sales services to strengthen customer loyalty.

Prominent Players in Ceramic Kitchen Sink Market

- •Franke Middle East FZE (United Arab Emirates)

- •Kohler Middle East FZE (United Arab Emirates)

- •Roca Middle East (Spain - Regional Operations)

- •Villeroy & Boch AG (Germany - Regional Operations)

- •Duravit AG (Germany - Regional Operations)

- •Grohe AG (Germany - Regional Operations)

- •Blanco GmbH + Co KG (Germany - Regional Operations)

- •E.C.A. Middle East (Turkey - Regional Operations)

- •Ideal Standard International (United Kingdom - Regional Operations)

- •Swan Corporation (United Arab Emirates)

- •Hussain Ceramics (United Arab Emirates)

- •Royal Ceramic Industries (Saudi Arabia)

- •Al Tayer Group (United Arab Emirates)

- •Al Jenaibi Ceramics (United Arab Emirates)

- •Interceramic Middle East (Mexico - Regional Operations)

- •Cotto (Thailand - Regional Operations)

- •Lixil Corporation (Japan - Regional Operations)

- •Marazzi Group (Italy - Regional Operations)

- •American Standard Brands (United States - Regional Operations)

- •Simas Ceramica (Italy - Regional Operations)

- •Porcelanosa Grupo (Spain - Regional Operations)

- •VitrA (Turkey - Regional Operations)

- •Marmorin (Poland - Regional Operations)

- •Kerovit (India - Regional Operations)

- •Rangoli Ceramics (India - Regional Operations)

Market Breakdown

- •By Ceramic Kitchen Sink Type

- ◦Undermount Ceramic Sinks

- ◦Drop-in Ceramic Sinks

- ◦Farmhouse Ceramic Sinks

- ◦Double Bowl Ceramic Sinks

- ◦Single Bowl Ceramic Sinks

- •By Application Sector

- ◦Residential Kitchens

- ◦Commercial Kitchens

- ◦Hospitality Sector

- ◦Institutional Kitchens

- ◦Renovation Projects

- •By Installation Model

- ◦Built-in Installation

- ◦Integrated Installation

- ◦Self-supporting Installation

- •By Surface Finish

- ◦Glossy Finish

- ◦Matte Finish

- ◦Textured Finish

Growth Dynamics

- •Increasing urbanization across Middle Eastern countries is driving demand for modern residential kitchens equipped with durable ceramic sinks, boosting market growth significantly.

- •Expansion of the hospitality and commercial kitchen sectors, particularly in the UAE and Saudi Arabia, fuels demand for high-quality ceramic kitchen sinks designed for heavy use and aesthetic appeal.

- •Government infrastructure development programs and real estate projects encourage adoption of advanced kitchen fixtures, including ceramic sinks, enhancing market penetration.

- •Rising consumer preference for environmentally friendly and easy-to-maintain ceramic products supports growth in premium ceramic kitchen sink segments.

- •Integration of innovative glazing technologies enhances product durability and design versatility, attracting a broad customer base and fostering sustained industry growth.

- •Increasing renovation activities in mature urban markets create opportunities for replacement and upgrade of existing kitchen sinks with modern ceramic options.

- •Strategic partnerships between manufacturers and construction firms enhance market reach and accelerate adoption of ceramic kitchen sinks in new projects.

Market Trends

- •A notable trend is the rising demand for farmhouse ceramic sinks, which blend traditional aesthetics with modern functionality, gaining popularity in luxury residential developments.

- •Smart integration features in kitchen sinks, such as antimicrobial surfaces and sensor-operated faucets, are gradually influencing ceramic sink designs in the Middle East market.

- •Sustainability is a growing focus with manufacturers adopting eco-friendly production processes and recyclable materials to meet increasing environmental regulations.

- •Customization trends are on the rise, with consumers seeking bespoke ceramic sinks tailored to specific kitchen layouts and color schemes.

- •E-commerce platforms are becoming significant channels for ceramic kitchen sink sales, expanding accessibility beyond traditional retail outlets.

- •Collaborations between ceramic sink manufacturers and interior designers are shaping new market offerings aligned with contemporary kitchen aesthetics.

- •The adoption of digital marketing strategies by key players enhances brand visibility and consumer engagement in the region.

Market Opportunities

- •There is substantial opportunity in expanding ceramic kitchen sink offerings to emerging Middle Eastern markets with growing urban populations and rising disposable incomes.

- •Developing innovative ceramic materials with enhanced durability and stain resistance can meet the evolving needs of commercial kitchen applications.

- •Investing in regional manufacturing facilities can reduce costs and improve supply chain efficiency, providing competitive advantages.

- •Expanding product customization and color variants can capture niche consumer segments focused on kitchen design personalization.

- •Leveraging digital sales platforms and virtual showrooms offers growth potential by reaching tech-savvy consumers and professional buyers.

- •Partnerships with hotel chains and real estate developers for bulk supply contracts can secure steady revenue streams.

- •Emerging demand for eco-friendly and sustainable kitchen products creates avenues for green-certified ceramic sinks.

Market Challenges

- •Fluctuating raw material costs for ceramics and glazes pose challenges to maintaining stable pricing and profitability for manufacturers.

- •Competition from alternative kitchen sink materials such as stainless steel and composite granite limits ceramic sink market share in certain segments.

- •Limited awareness about the benefits of ceramic kitchen sinks among some consumer groups slows market penetration in less urbanized areas.

- •Supply chain disruptions and import dependencies for certain raw materials create risks for timely product availability.

- •High installation costs associated with some ceramic sink types can deter adoption in cost-sensitive renovation projects.

- •Regulatory compliance complexity across different Middle Eastern countries requires manufacturers to adapt products and certifications accordingly.

- •The seasonal nature of construction activity can lead to fluctuating demand and inventory management challenges.

Regulatory Framework

- •The Gulf Cooperation Council (GCC) countries implemented ceramic product safety standards between 2015 and 2025 mandating compliance with ISO 6486 for ceramic ware, ensuring sink durability and lead content limits. This regulation impacts manufacturers by enforcing quality benchmarks and product testing requirements.

- •Environmental regulations introduced in Saudi Arabia in 2018 require manufacturers to adopt sustainable production methods, reducing emissions and waste, which has driven innovation in ceramic sink manufacturing processes.

- •The United Arab Emirates enacted the Emirates Conformity Assessment Scheme (ECAS) in 2020, establishing certification protocols for kitchen fixtures including ceramic sinks, enhancing market safety and consumer confidence.

- •Qatar's Ministry of Municipality and Environment introduced building code updates in 2023 that specify material standards for ceramic kitchen sinks in commercial and residential buildings, influencing procurement and installation practices.

- •Egypt's national standards authority updated ceramic product guidelines in 2019 focusing on water resistance and chemical durability, prompting manufacturers to tailor products to local compliance requirements.

Market Intelligence

- •15th January 2025, Franke Middle East FZE launched a new range of undermount ceramic kitchen sinks featuring advanced antimicrobial glazing technology designed for high-traffic commercial kitchens. The product line targets hospitality and institutional kitchen segments with enhanced hygiene and durability features. This launch is part of Franke's strategy to capture the growing demand for premium ceramic sinks in the GCC region and aligns with increasing regulatory focus on sanitary kitchen environments. The new sinks incorporate scratch-resistant surfaces and are available in multiple sizes to suit diverse kitchen layouts, responding to customer demand for both functionality and style. Source: Franke Middle East Official Press Release

- •30th March 2025, Kohler Middle East FZE introduced a customizable farmhouse ceramic sink collection tailored for luxury residential markets in the Middle East. This innovative product range offers customer-selectable colors and finishes, integrating traditional design with contemporary kitchen trends. The launch enhances Kohler’s competitive positioning in the premium ceramic kitchen sink segment amid rising consumer preference for bespoke kitchen fixtures. The sinks also feature integrated soundproofing technology and eco-friendly manufacturing processes, supporting sustainability initiatives. Market analysts anticipate this offering will accelerate farmhouse sink adoption in upscale Middle Eastern urban developments. Source: Kohler Middle East Press Release

- •20th April 2025, Roca Middle East announced a strategic partnership with a leading UAE-based real estate developer to supply ceramic kitchen sinks for a large-scale residential project. This collaboration entails providing over 5,000 undermount and double bowl ceramic sinks over a three-year period, reinforcing Roca’s presence in the Middle East construction sector. The deal underscores the growing trend of integrating high-quality ceramic fixtures in new residential developments and reflects strong demand driven by urban expansion and modernization efforts. This initiative is expected to boost Roca's market share and establish long-term supply relationships in the region. Source: Roca Middle East Corporate Announcement

- •10th June 2025, Villeroy & Boch AG expanded its Middle East product portfolio by introducing a line of eco-certified ceramic kitchen sinks manufactured using sustainable raw materials and energy-efficient processes. The launch aligns with increasing environmental regulations and consumer awareness in the region. These sinks offer enhanced durability and easy maintenance, targeting both residential and commercial segments. Villeroy & Boch aims to leverage this innovation to differentiate its offerings and cater to the sustainability-conscious market segment. Early market response indicates positive acceptance among architects and interior designers focused on green building certifications. Source: Villeroy & Boch AG Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The United Arab Emirates currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Qatar is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Turkey

- Egypt

- United Arab Emirates

- Saudi Arabia

- Israel

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.65 Billion |

| Forecast Year Market Size | USD 1.45 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Ceramic Kitchen Sink Type (Undermount Ceramic Sinks, Drop-in Ceramic Sinks, Farmhouse Ceramic Sinks, Double Bowl Ceramic Sinks, Single Bowl Ceramic Sinks), Application Sector (Residential Kitchens, Commercial Kitchens, Hospitality Sector, Institutional Kitchens, Renovation Projects), Installation Model (Built-in Installation, Integrated Installation, Self-supporting Installation), Surface Finish (Glossy Finish, Matte Finish, Textured Finish) |

| Regions Covered | Turkey, Egypt, United Arab Emirates, Saudi Arabia, Israel, Others |

| Key Companies | Franke Middle East FZE (United Arab Emirates), Kohler Middle East FZE (United Arab Emirates), Roca Middle East (Spain - Regional Operations), Villeroy & Boch AG (Germany - Regional Operations), Duravit AG (Germany - Regional Operations) |

Middle East Ceramic Kitchen Sink Market Scope & Changing Dynamics 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Market market is projected to grow at a steady CAGR from 2025 to 2030, driven by increasing demand and expansion in various applications.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.