China Building Integrated Photovoltaic Panel Market Size, Growth & Revenue 2024-2034

China Building Integrated Photovoltaic Panel Market is segmented by Type (Monocrystalline Silicon Panels, Polycrystalline Silicon Panels, Thin-Film Panels, Building Facade Modules, Rooftop Integration Panels), Application (Residential Buildings, Commercial Buildings, Industrial Facilities, Public Infrastructure, Agricultural Structures), Installation Type (New Construction Integration, Retrofit Installation, Modular Systems), Material Technology (Silicon-based Photovoltaics, Thin-Film Photovoltaics, Multi-junction Solar Cells), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Building Integrated Photovoltaic Panel (BIPV) Market is a rapidly evolving sector focused on incorporating photovoltaic technology directly into building materials to generate electricity while serving structural or aesthetic building functions. This market includes a diverse array of product types such as monocrystalline and polycrystalline silicon panels, thin-film panels, and innovative facade modules designed for integration into residential, commercial, industrial, public infrastructure, and agricultural buildings. The market scope extends beyond panel manufacturing to installation, maintenance, and integration with smart energy management systems, reflecting China's strategic push towards sustainable urbanization and carbon neutrality. The increasing governmental emphasis on green buildings, coupled with rising construction activity in urban and rural zones, fuels the demand for BIPV panels. Technological advancements, such as improved efficiency and material durability, further enhance market attractiveness. This market is characterized by intense competition, innovation focus, and a growing ecosystem of suppliers and service providers, playing a pivotal role in China's renewable energy and building sectors.

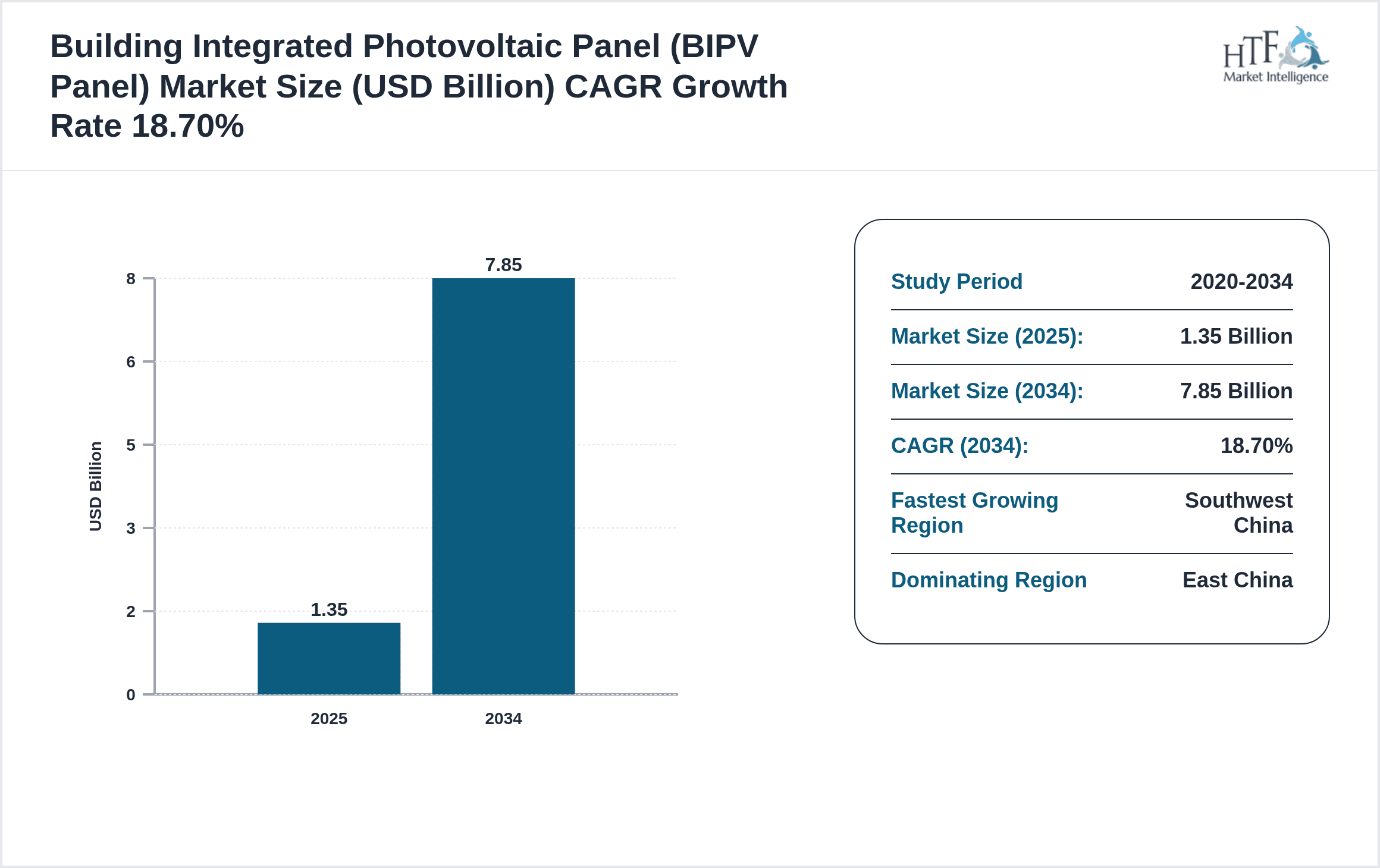

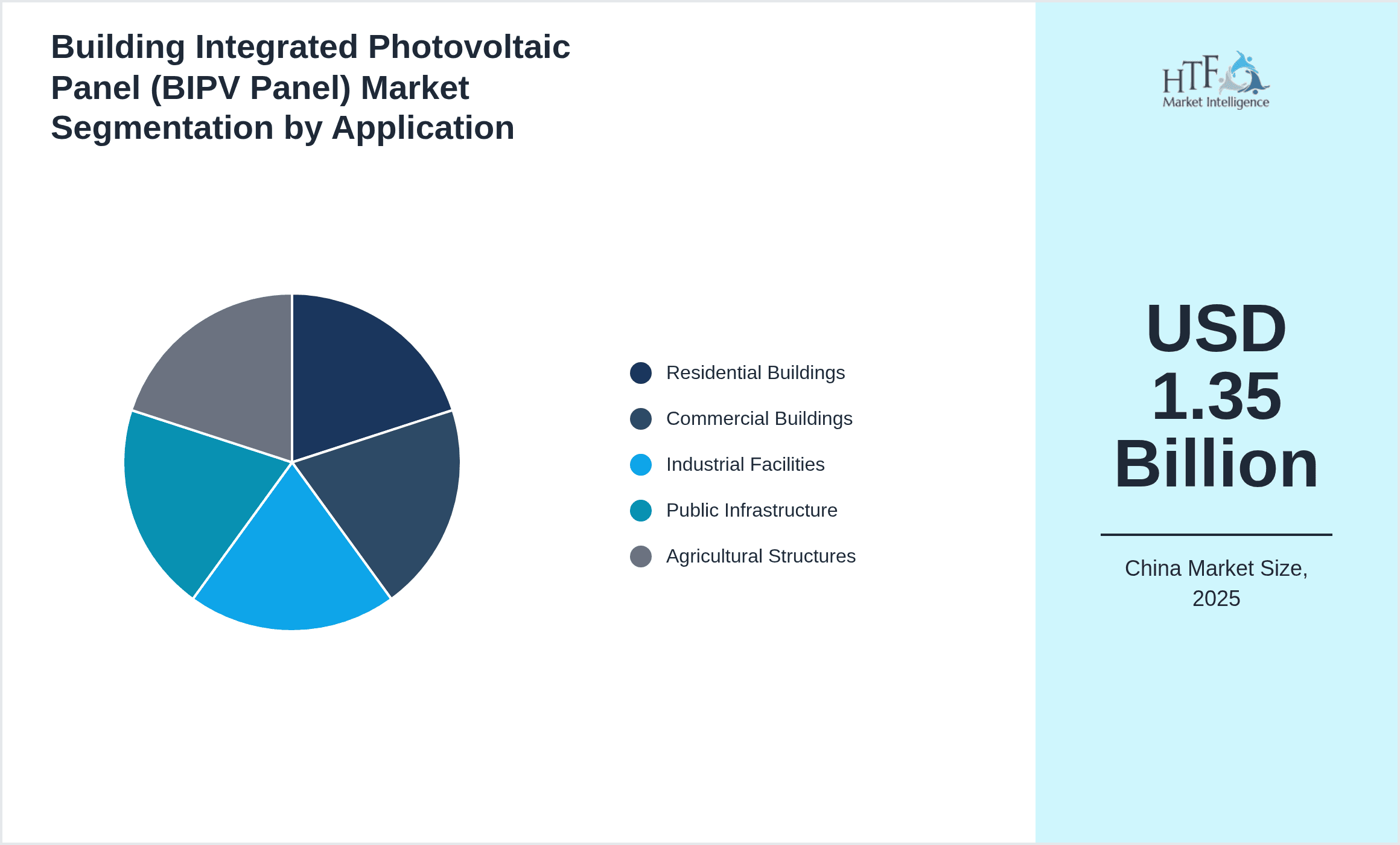

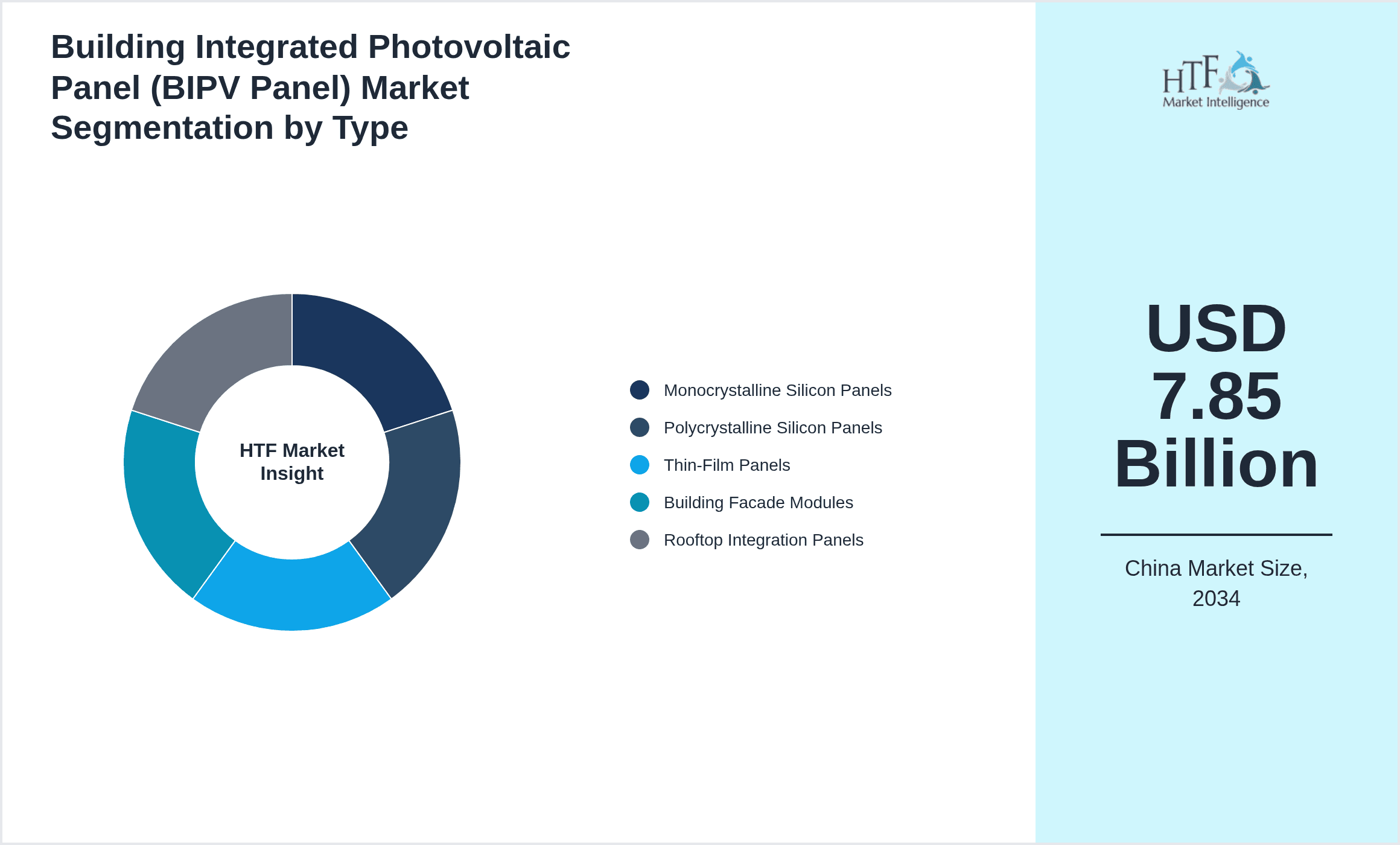

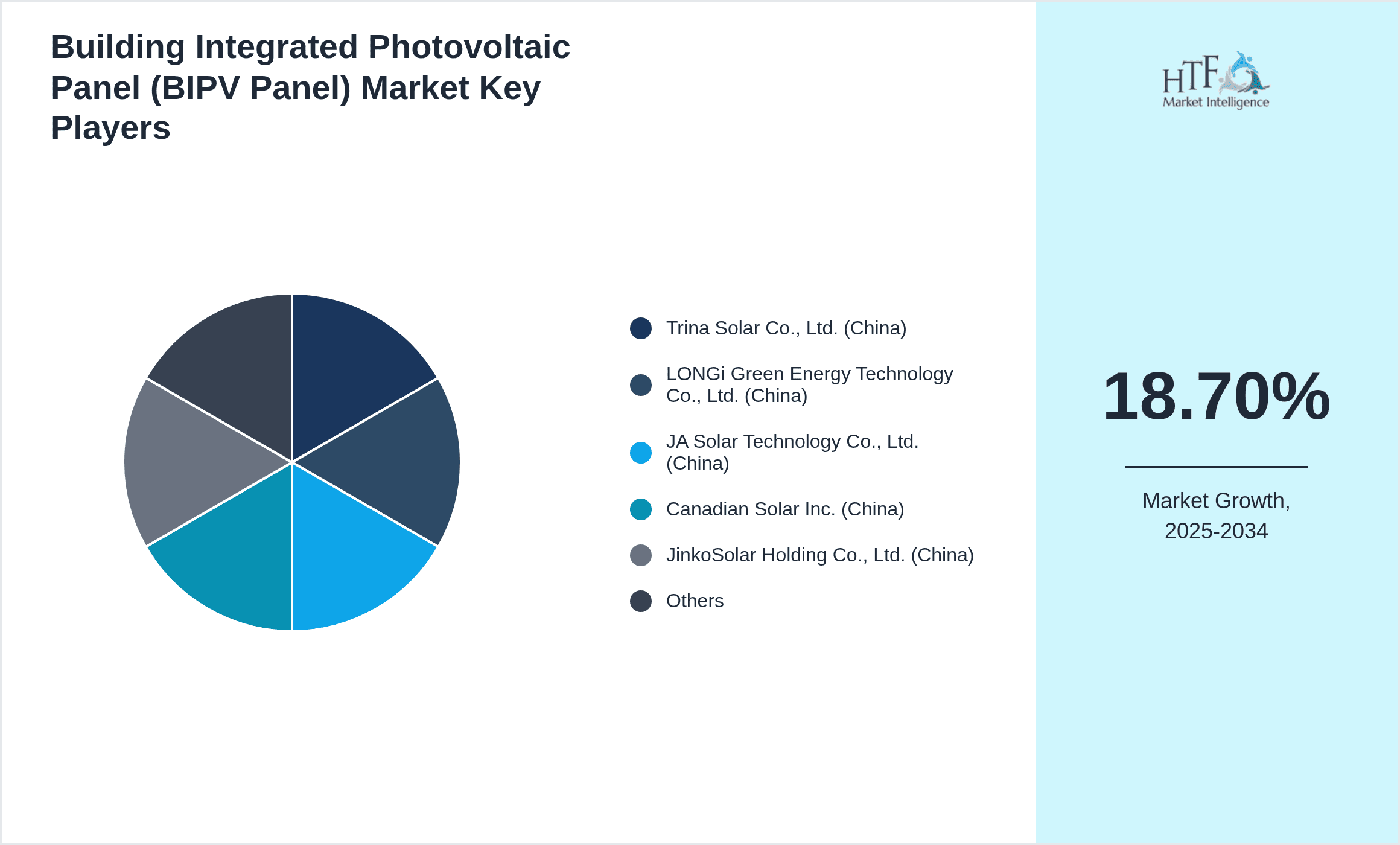

- •Key highlights include a projected market CAGR of 18.7% between 2024 and 2034, with the market size expected to grow from USD 1.35 billion in 2024 to USD 7.85 billion by 2034. East China dominates the market with a 38% share, while Southwest China is the fastest growing region with a CAGR of 22.3%. Monocrystalline silicon panels currently lead the product segment, but building facade modules are gaining rapid traction. Applications in residential and commercial buildings account for the largest consumption, driven by urban development and energy efficiency regulations. The market is supported by strong government policies, subsidies, and increasing environmental awareness among consumers and developers.

- •The value proposition of the China BIPV market lies in its dual functionality as a building material and energy generator, reducing electricity costs and carbon footprint while enhancing building aesthetics and compliance with green building standards. It offers strategic benefits to manufacturers, construction companies, and energy providers by enabling integration of renewable energy at the point of use. Stakeholders benefit from growing policy support, technological innovations, and expanding applications across multiple building types, positioning BIPV as a cornerstone in China's energy transition and sustainable infrastructure development.

Competitive Landscape

The competitive landscape of the China Building Integrated Photovoltaic Panel market is characterized by a diverse mix of domestic and international manufacturers striving for technological innovation, cost efficiency, and expansive market reach. Leading firms focus heavily on R&D investments to enhance panel efficiency, durability, and aesthetic integration, differentiating their offerings through customized solutions for varied building applications. Competition is intensified by government incentives that encourage local manufacturing and adoption, fostering an environment of rapid product development and price competition. Strategic partnerships between technology providers, construction companies, and energy utilities have become prevalent to accelerate project deployment and scale. Mergers and acquisitions are reshaping the market structure, enabling companies to consolidate capabilities and expand geographic coverage within China’s segmented regional zones. The rivalry also extends to distribution channels and after-sales services, with firms investing in comprehensive support networks to secure long-term customer loyalty. Overall, the market is expected to see continued innovation-driven competition, supporting sustainable growth and adoption of BIPV technologies nationwide.

Leading Companies in Building Integrated Photovoltaic Panel Market

- •Trina Solar Co., Ltd. (China)

- •LONGi Green Energy Technology Co., Ltd. (China)

- •JA Solar Technology Co., Ltd. (China)

- •Canadian Solar Inc. (China)

- •JinkoSolar Holding Co., Ltd. (China)

- •Hanergy Thin Film Power Group Ltd. (China)

- •Risen Energy Co., Ltd. (China)

- •Yingli Green Energy Holding Company Limited (China)

- •GCL-Poly Energy Holdings Limited (China)

- •BYD Company Ltd. (China)

- •Suntech Power Holdings Co., Ltd. (China)

- •ET Solar Group (China)

- •Seraphim Solar System Co., Ltd. (China)

- •Talesun Solar (China)

- •Suntech Power (China)

- •Zhongli Talesun Solar Co., Ltd. (China)

- •Chint Power Systems Co., Ltd. (China)

- •Himin Solar Co., Ltd. (China)

- •Phono Solar Technology Co., Ltd. (China)

- •Aiko Solar Energy Co., Ltd. (China)

- •GCL System Integration Technology Co., Ltd. (China)

- •Shanghai Electric Group Co., Ltd. (China)

- •Chint Group (China)

- •Wuxi Suntech Power Co., Ltd. (China)

- •Seraphim Energy Group Limited (China)

Market Breakdown

- •By Type

- ◦Monocrystalline Silicon Panels

- ◦Polycrystalline Silicon Panels

- ◦Thin-Film Panels

- ◦Building Facade Modules

- ◦Rooftop Integration Panels

- •By Application

- ◦Residential Buildings

- ◦Commercial Buildings

- ◦Industrial Facilities

- ◦Public Infrastructure

- ◦Agricultural Structures

- •By Installation Type

- ◦New Construction Integration

- ◦Retrofit Installation

- ◦Modular Systems

- •By Material Technology

- ◦Silicon-based Photovoltaics

- ◦Thin-Film Photovoltaics

- ◦Multi-junction Solar Cells

Growth Dynamics

- •Robust government policies and subsidies aimed at reducing carbon emissions and promoting green buildings have significantly propelled the adoption of BIPV panels in China. Programs such as the ‘Green Building Action Plan’ and renewable energy targets provide strong financial incentives and regulatory support for developers integrating photovoltaic technology into new and existing buildings.

- •Technological advancements in solar cell efficiency and aesthetic integration allow BIPV panels to function seamlessly as building materials, increasing consumer acceptance and expanding application scope. Innovations such as semi-transparent panels and customizable facade designs attract architects and developers seeking both energy performance and visual appeal.

- •Rapid urbanization and infrastructure development across East, South, and Southwest China have increased demand for sustainable construction materials, creating substantial growth opportunities for BIPV panel manufacturers and installers in these regions.

- •Rising energy costs and increasing awareness of environmental impact among commercial and residential property owners drive investments in on-site renewable energy generation through BIPV integration, enabling long-term savings and regulatory compliance.

- •Strategic collaborations between photovoltaic manufacturers, construction firms, and technology providers facilitate integrated solutions and faster market penetration, fostering ecosystem development and enhancing competitive advantage across China’s segmented regional markets.

Market Trends

- •The China BIPV market is witnessing a surge in adoption of building facade modules that combine solar energy generation with architectural design, driven by demand for energy-efficient skyscrapers and commercial complexes in urban centers like Shanghai and Shenzhen.

- •Integration of smart energy management systems with BIPV installations is becoming increasingly prevalent, enabling real-time monitoring, optimized energy usage, and enhanced grid interaction that align with China’s smart city initiatives.

- •Manufacturers are shifting towards the use of advanced thin-film technologies that reduce weight and increase flexibility, allowing for more versatile applications such as curved surfaces and retrofitting older buildings.

- •Rising environmental regulations and certification standards for green buildings are influencing design choices, promoting the use of BIPV panels that meet stringent sustainability criteria and contribute to higher building valuation.

- •Collaborations between solar technology companies and construction material suppliers are intensifying, leading to innovations in hybrid materials that combine photovoltaic properties with structural strength.

Market Opportunities

- •Expanding urbanization in Western and Southwest China offers untapped markets for BIPV applications, particularly in smart city projects and new residential developments aiming for energy self-sufficiency and sustainability.

- •Rising demand for retrofit solutions in existing buildings presents a significant growth avenue, as older infrastructure undergoes modernization to meet new energy efficiency standards using modular BIPV systems.

- •Advancements in multi-junction and perovskite solar cell technologies promise higher efficiencies at lower costs, enabling next-generation BIPV products that could disrupt current market dynamics and broaden adoption.

- •Government initiatives encouraging rural electrification and agricultural building modernization create niche opportunities for BIPV integration in farming facilities and community infrastructure, enhancing energy access and sustainability.

- •Strategic partnerships between technology providers and construction companies can accelerate large-scale BIPV deployments in public infrastructure projects, including schools, hospitals, and transportation hubs across key Chinese provinces.

Market Challenges

- •High initial capital expenditure and complex installation requirements for BIPV systems remain significant barriers, particularly for small and medium-sized enterprises and residential customers seeking affordable renewable energy solutions.

- •Lack of standardized testing and certification processes for building-integrated photovoltaic products in China leads to market fragmentation and challenges in quality assurance and consumer confidence.

- •Technical challenges related to durability, weather resistance, and long-term performance of integrated panels in diverse climatic zones across China impact adoption rates and increase maintenance costs.

- •Competition from traditional solar panel installations and other renewable energy sources can limit BIPV market penetration, as stakeholders weigh cost-benefit trade-offs and return on investment timelines.

- •Limited awareness among architects and construction professionals about the benefits and design possibilities of BIPV technology constrains integration in mainstream building projects.

Regulatory Framework

- •Between 2019 and 2024, China introduced the ‘Green Building Action Plan’ mandating increased use of renewable energy technologies including BIPV in public and commercial buildings, setting clear targets for solar energy integration.

- •The ‘Renewable Energy Law’ amendments implemented in 2022 strengthened subsidy schemes and financial incentives for BIPV adoption, encouraging private sector investments and accelerating market growth in key provinces.

- •New national standards for photovoltaic modules and building material integration were released in 2023, establishing testing protocols, safety requirements, and performance benchmarks to ensure product reliability.

- •Provincial governments in East and South China have enacted additional regulations promoting green construction certifications that favor BIPV usage, including expedited permitting processes and tax rebates.

- •Government programs supporting rural electrification and sustainable agriculture infrastructure launched in 2021 provide targeted funding to deploy BIPV panels in agricultural buildings, expanding market reach beyond urban centers.

Market Intelligence

- •15th January 2025, Trina Solar Co., Ltd. launched an innovative building facade photovoltaic module featuring enhanced energy conversion efficiency and customizable design patterns aimed at high-rise commercial buildings in East China. This product integrates seamlessly with various architectural styles and includes smart monitoring capabilities for optimized energy management, reflecting Trina Solar’s commitment to advancing sustainable urban infrastructure. The launch is expected to boost Trina’s market share in the competitive BIPV segment by addressing growing demand for aesthetic and functional solar solutions. Source: Trina Solar Official Press Release

- •8th March 2025, JA Solar Technology Co., Ltd. introduced a new range of flexible thin-film photovoltaic panels designed specifically for retrofit installations on existing residential buildings in South China. These lightweight panels facilitate easier installation with minimal structural modifications and offer enhanced durability against humid coastal climates. The innovative product line targets expanding green building initiatives and aims to capture market share in the residential BIPV segment, highlighting JA Solar’s strategic focus on diversification and technological leadership. Source: JA Solar Corporate Announcement

- •20th April 2025, LONGi Green Energy Technology Co., Ltd. announced a strategic partnership with leading Chinese construction firms to co-develop integrated solar building solutions for large-scale public infrastructure projects in North and Central China. The collaboration focuses on combining LONGi’s high-efficiency monocrystalline panels with advanced construction materials to deliver cost-effective, energy-generating building envelopes. This initiative is expected to accelerate BIPV adoption in government-funded projects and strengthen LONGi’s regional market presence. Source: LONGi Press Release

- •10th May 2025, Canadian Solar Inc. expanded its manufacturing capacity in China by inaugurating a new facility dedicated to producing building facade photovoltaic modules with improved thermal regulation and enhanced aesthetic options. The expansion aims to meet increasing demand from commercial and industrial building sectors in Southwest China and supports Canadian Solar’s ambition to lead in the BIPV market segment by offering technologically advanced, customizable solutions. Source: Canadian Solar Industry News

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.35 Billion |

| Forecast Year Market Size | USD 7.85 Billion |

| CAGR | 18.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 18.4% |

| Scope of Report | Market is segmented by Type (Monocrystalline Silicon Panels, Polycrystalline Silicon Panels, Thin-Film Panels, Building Facade Modules, Rooftop Integration Panels), Application (Residential Buildings, Commercial Buildings, Industrial Facilities, Public Infrastructure, Agricultural Structures), Installation Type (New Construction Integration, Retrofit Installation, Modular Systems), Material Technology (Silicon-based Photovoltaics, Thin-Film Photovoltaics, Multi-junction Solar Cells) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Trina Solar Co., Ltd. (China), LONGi Green Energy Technology Co., Ltd. (China), JA Solar Technology Co., Ltd. (China), Canadian Solar Inc. (China), JinkoSolar Holding Co., Ltd. (China), Hanergy Thin Film Power Group Ltd. (China), Risen Energy Co., Ltd. (China), Yingli Green Energy Holding Company Limited (China), GCL-Poly Energy Holdings Limited (China), BYD Company Ltd. (China), Suntech Power Holdings Co., Ltd. (China), ET Solar Group (China), Seraphim Solar System Co., Ltd. (China), Talesun Solar (China), Suntech Power (China), Zhongli Talesun Solar Co., Ltd. (China), Chint Power Systems Co., Ltd. (China), Himin Solar Co., Ltd. (China), Phono Solar Technology Co., Ltd. (China), Aiko Solar Energy Co., Ltd. (China), GCL System Integration Technology Co., Ltd. (China), Shanghai Electric Group Co., Ltd. (China), Chint Group (China), Wuxi Suntech Power Co., Ltd. (China), Seraphim Energy Group Limited (China) |

China Building Integrated Photovoltaic Panel Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.