EMEA Aluminum Molybdenum Alloy Market - Outlook 2024-2034

EMEA Aluminum Molybdenum Alloy Market is segmented by Type (Aluminum-Rich Alloys, Balanced Aluminum-Molybdenum Alloys, Molybdenum-Rich Alloys, Specialty Alloys, Custom Composites), Application (Aerospace, Automotive, Construction, Electrical & Electronics, Industrial Machinery), End-User Industry (Aerospace Manufacturers, Automotive OEMs, Construction Firms, Electronics Manufacturers, Heavy Machinery Producers), Distribution Channel (Direct Sales, Distributors and Dealers, Online Platforms), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Aluminum Molybdenum Alloy Market is defined by the production and utilization of specialized aluminum and molybdenum-based alloys tailored for high-performance applications across aerospace, automotive, construction, electrical & electronics, and industrial machinery sectors within Europe, the Middle East, and Africa. These alloys offer superior strength-to-weight ratios, corrosion resistance, and high-temperature durability, meeting stringent industry standards and regulations. The market spans a variety of alloy compositions including aluminum-rich, molybdenum-rich, balanced, specialty, and custom composites designed to fulfill diverse operational requirements. Advanced manufacturing techniques and metallurgical innovations drive product differentiation and performance enhancements. The industry's scope also integrates distribution channels, evolving end-user demands, and regulatory frameworks influencing material selection. This market is vital for supporting technological advancements and sustainability goals across key regional industries, with a growing emphasis on lightweight and high-strength materials to improve energy efficiency and operational longevity in demanding environments.

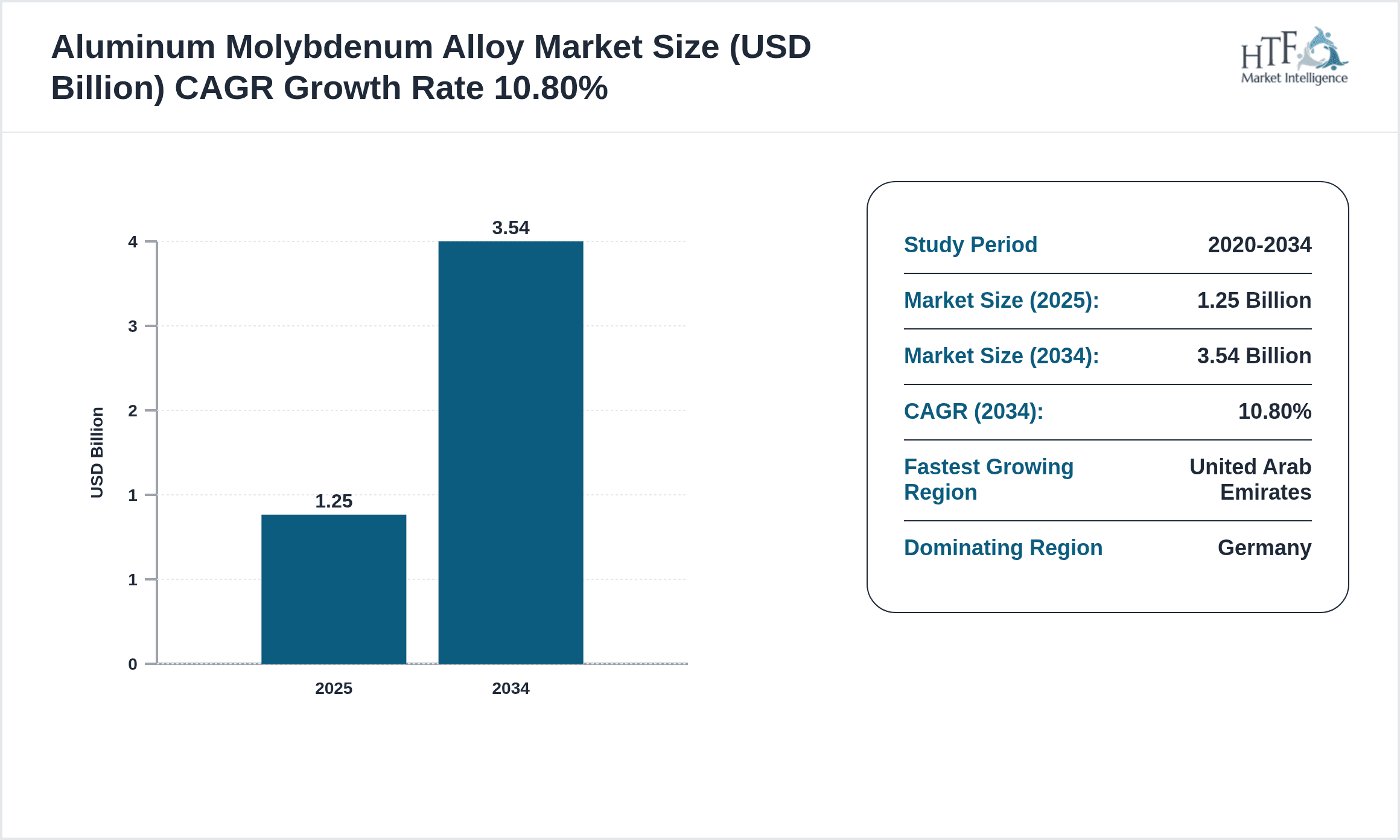

- •Key market highlights exhibit a robust compound annual growth rate (CAGR) of 10.8% from 2024 to 2034, driven by increasing aerospace production, automotive lightweighting initiatives, and infrastructural investments across EMEA. The base market size stood at USD 1.25 Billion in 2024, projected to reach USD 3.54 Billion by 2034. Germany commands a dominant market share of 28%, supported by its advanced manufacturing ecosystem, while the United Arab Emirates is the fastest-growing country with an anticipated CAGR of 14.2%. Aluminum-rich alloys lead product segments, closely followed by specialty alloys which show substantial growth due to rising demand for customized high-performance materials. Applications in aerospace and automotive sectors remain the largest contributors to market revenue, reflecting ongoing industrial modernization and environmental regulations.

- •The value proposition of the EMEA Aluminum Molybdenum Alloy Market lies in delivering advanced materials that enable industries to meet evolving performance, safety, and sustainability standards. These alloys contribute to reducing structural weight, enhancing fuel efficiency, and improving mechanical resilience, which are crucial for aerospace and automotive sectors aiming to reduce carbon footprints. Additionally, the market's strategic importance extends to construction and electrical & electronics industries, where durability and thermal stability are increasingly demanded. Stakeholders, including manufacturers, suppliers, and end-users, benefit from innovations in alloy compositions and processing technologies that expand application possibilities. The market thus serves as a critical enabler for technological progress and economic development across the EMEA region.

Competitive Landscape

The competitive landscape of the EMEA Aluminum Molybdenum Alloy Market is characterized by intense rivalry among established multinational corporations and emerging regional players. Market participants focus heavily on innovation, investing in research and development to create alloys with enhanced properties such as improved strength-to-weight ratio, corrosion resistance, and thermal stability. Strategic partnerships and collaborations with aerospace and automotive OEMs facilitate tailored product development and market penetration. Pricing strategies vary, with premium pricing justified by high-performance specialty alloys, while broader adoption is driven by cost-effective aluminum-rich variants. Distribution channels are well-established across Europe and the Middle East, enabling efficient supply chain operations. Mergers and acquisitions are frequent as companies seek to consolidate capabilities and expand geographic reach. The competitive environment is further influenced by regulatory compliance, sustainability mandates, and the need for rapid product innovation to maintain market leadership.

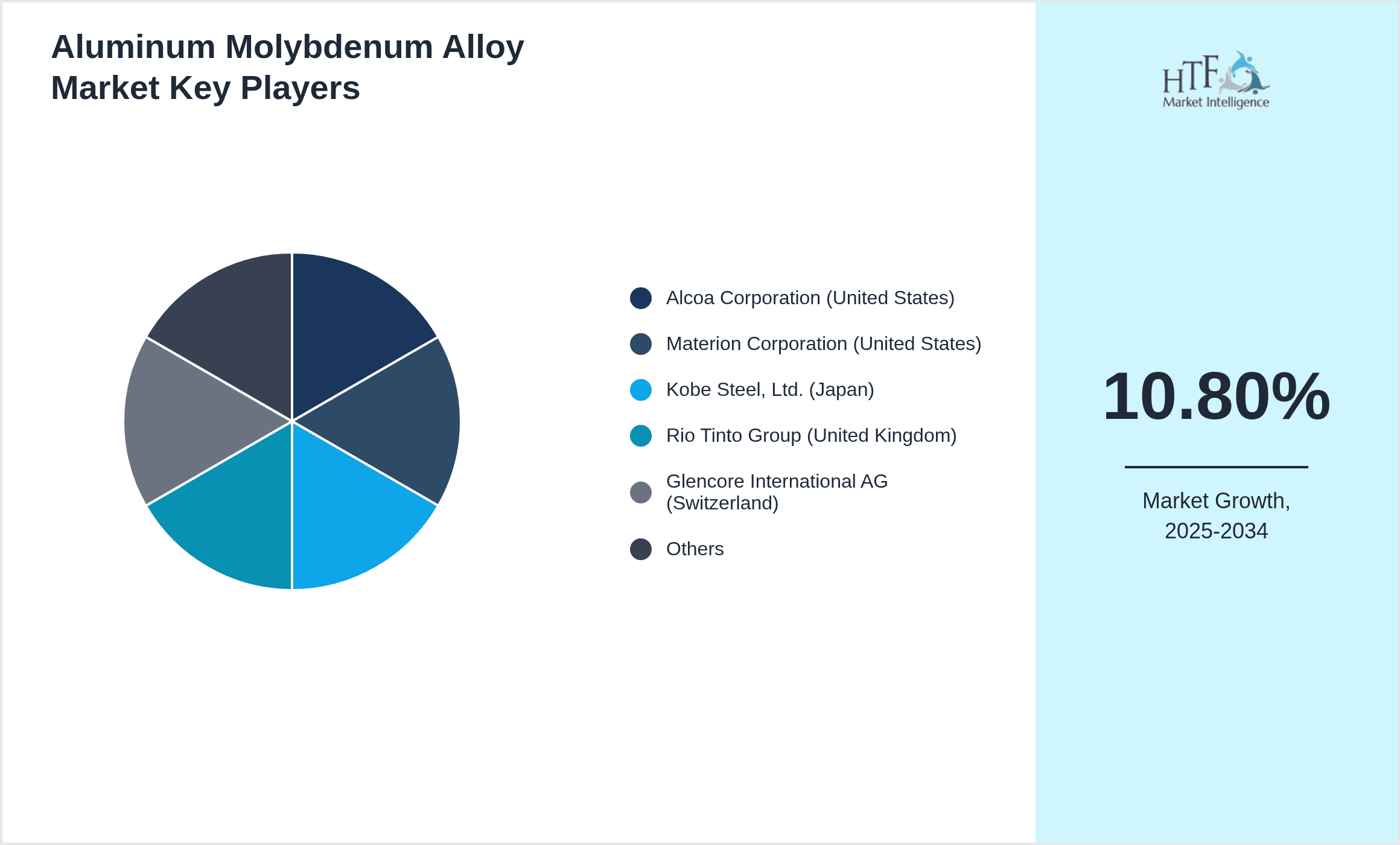

Leading Companies in Aluminum Molybdenum Alloy Market

- •Alcoa Corporation (United States)

- •Materion Corporation (United States)

- •Kobe Steel, Ltd. (Japan)

- •Rio Tinto Group (United Kingdom)

- •Glencore International AG (Switzerland)

- •Aleris Corporation (United States)

- •Constellium SE (France)

- •AMAG Austria Metall AG (Austria)

- •Aluminium Bahrain B.S.C. (Bahrain)

- •Hydro Aluminium ASA (Norway)

- •Norsk Titanium AS (Norway)

- •Novelis Inc. (United States)

- •Metalcorp Group (United Arab Emirates)

- •Thyssenkrupp AG (Germany)

- •Outokumpu Oyj (Finland)

- •Elkem ASA (Norway)

- •Aluminium Dunkerque (France)

- •Alro S.A. (Romania)

- •Trimet Aluminium SE (Germany)

- •Mubadala Investment Company (United Arab Emirates)

- •Eramet Group (France)

- •AMAG Rolling GmbH (Austria)

- •Constellium Rolled Products Ravenswood LLC (United States)

- •Sapa Group (Norway)

- •Befesa S.A. (Spain)

Market Breakdown

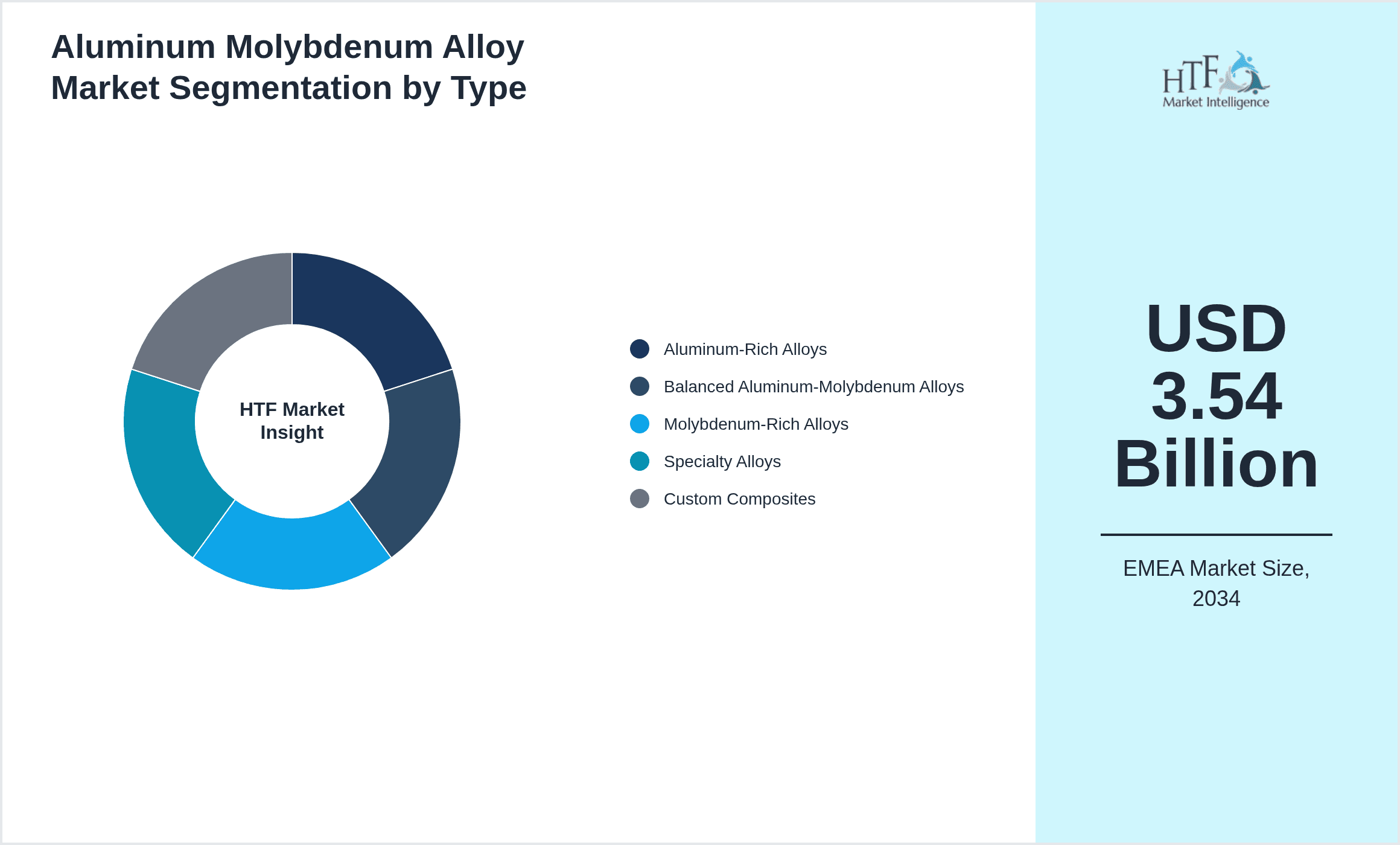

- •By Type

- ◦Aluminum-Rich Alloys

- ◦Balanced Aluminum-Molybdenum Alloys

- ◦Molybdenum-Rich Alloys

- ◦Specialty Alloys

- ◦Custom Composites

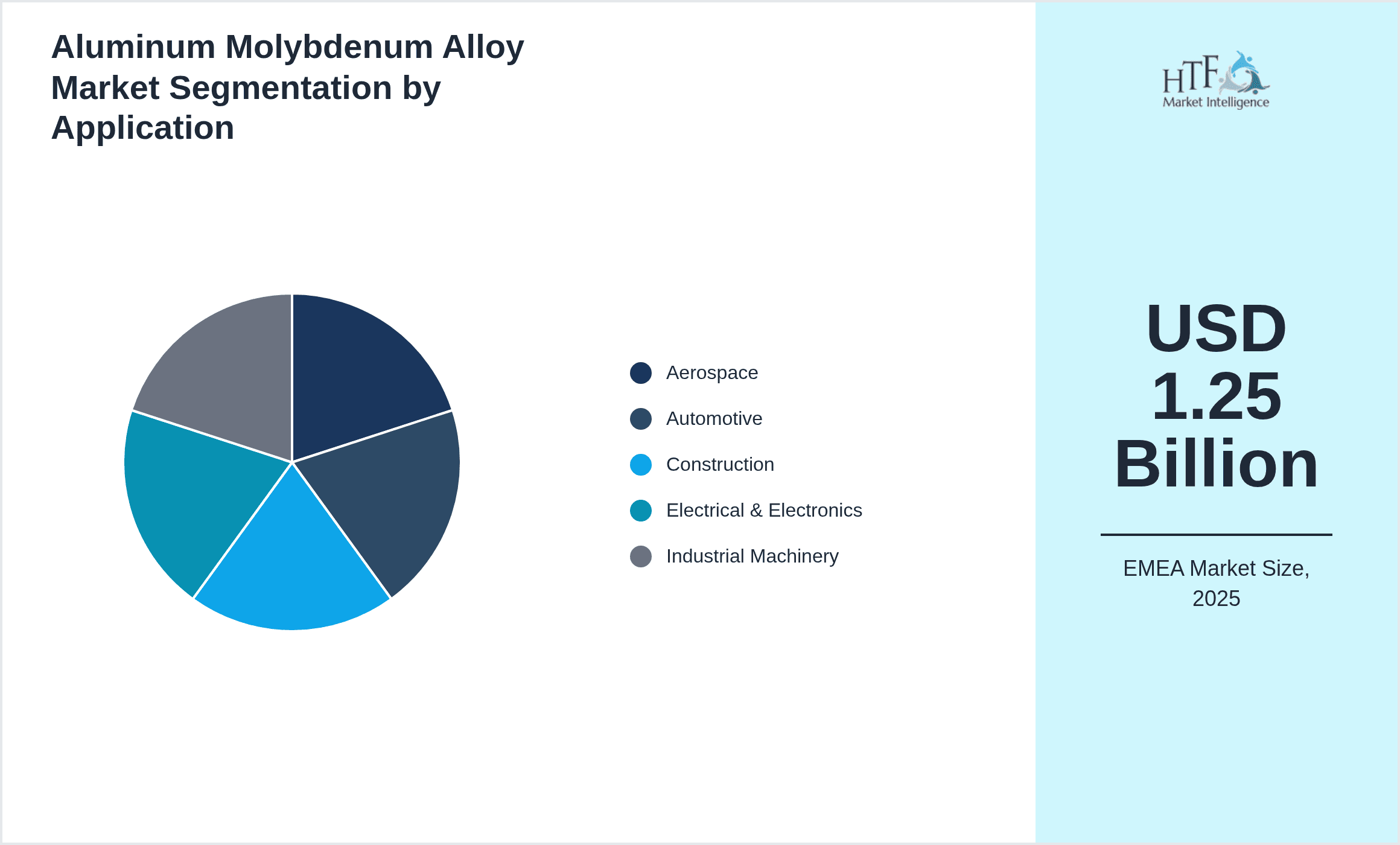

- •By Application

- ◦Aerospace

- ◦Automotive

- ◦Construction

- ◦Electrical & Electronics

- ◦Industrial Machinery

- •By End-User Industry

- ◦Aerospace Manufacturers

- ◦Automotive OEMs

- ◦Construction Firms

- ◦Electronics Manufacturers

- ◦Heavy Machinery Producers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Dealers

- ◦Online Platforms

Growth Dynamics

- •The increasing demand for lightweight and high-strength materials in the aerospace sector is propelling the growth of aluminum molybdenum alloys in EMEA. Airlines and defense contractors are prioritizing fuel efficiency and durability, driving adoption of these advanced alloys.

- •Automotive manufacturers across EMEA are intensifying lightweighting efforts to comply with stringent emission regulations, resulting in higher utilization of aluminum-molybdenum alloys for structural and engine components.

- •Technological advancements in alloy processing techniques, such as powder metallurgy and additive manufacturing, are enabling production of complex, high-performance components, expanding market applications.

- •Sustainability initiatives and increasing focus on recyclable materials are encouraging the use of aluminum molybdenum alloys, which offer excellent recyclability compared to other metal composites.

- •Government infrastructure investments in construction and industrial sectors within the region are driving demand for durable alloys capable of withstanding harsh environmental conditions.

Market Trends

- •There is a rising trend towards customization of aluminum molybdenum alloys tailored for specific industry needs, allowing manufacturers to optimize mechanical and thermal properties for niche applications.

- •Adoption of digital technologies such as AI-driven alloy design and advanced simulation tools is accelerating R&D cycles and improving alloy performance prediction.

- •Collaborations between alloy producers and end-user industries are becoming more common to co-develop materials that meet evolving regulatory and performance standards.

- •Sustainability and circular economy principles are shaping product development strategies, with increased emphasis on material lifecycle management and recycling.

- •Market players are investing in capacity expansions and regional production hubs to better serve localized demand and reduce supply chain disruptions.

Market Opportunities

- •Emerging aerospace markets in the Middle East offer significant growth potential for aluminum molybdenum alloys due to expanding aircraft manufacturing and maintenance activities.

- •Increasing electrification in automotive industry opens opportunities for alloys with superior thermal management properties suitable for electric vehicle components.

- •Expansion of renewable energy infrastructure in Europe creates demand for durable alloy materials in wind turbines and solar panel frameworks.

- •Growth in industrial machinery manufacturing in Eastern Europe provides avenues for adoption of high-strength, corrosion-resistant alloys to improve equipment lifespan.

- •Advancements in additive manufacturing present opportunities for producing complex alloy components with reduced waste and lower costs.

Market Challenges

- •High production costs associated with molybdenum extraction and alloy processing limit market penetration, especially in cost-sensitive end-use segments.

- •Volatility in raw material prices, particularly molybdenum, pose supply chain risks and impact pricing strategies for alloy manufacturers.

- •Stringent environmental regulations concerning mining and metal processing increase compliance burdens and operating expenses for industry players.

- •Limited availability of skilled workforce with expertise in advanced metallurgical techniques restricts capacity expansion and innovation pace.

- •Competition from alternative lightweight materials such as titanium alloys and composites challenges the market share of aluminum molybdenum alloys.

Regulatory Framework

- •Between 2019 and 2024, the European Union implemented REACH regulations requiring comprehensive chemical safety assessments for alloy constituents, affecting production compliance.

- •The EU's Circular Economy Action Plan introduced mandates on metal recycling rates and waste reduction, driving alloy manufacturers to enhance recyclability and material recovery processes.

- •Environmental permitting and emissions standards under the Industrial Emissions Directive impose operational restrictions on smelting and processing facilities across EMEA.

- •Country-specific mandates such as Germany’s Metal Industry Environmental Guidelines require adoption of cleaner production technologies and regular environmental reporting.

- •Government incentives in Middle Eastern countries encourage investment in advanced manufacturing technologies to boost regional production capacity of specialty alloys.

Market Intelligence

- •15th February 2025, Constellium SE announced the launch of a new high-strength aluminum molybdenum alloy specifically engineered for aerospace structural applications. This alloy offers a 15% improvement in strength-to-weight ratio while maintaining excellent corrosion resistance, meeting the demanding safety standards of leading aerospace manufacturers. The product launch is expected to strengthen Constellium’s position in the European aerospace materials market. The company also highlighted plans to ramp up production capacity at its French manufacturing facilities to meet anticipated demand growth in the EMEA region. Source: Official Company Release

- •28th April 2025, AMAG Austria Metall AG unveiled an innovative specialty aluminum molybdenum composite designed to enhance thermal conductivity for electric vehicle battery enclosures. The new material supports improved battery safety and efficiency, aligning with the automotive sector's transition towards electrification. AMAG’s R&D investment in this segment underscores its strategic focus on sustainable mobility solutions across Europe. Production is slated to commence in Q3 2025 with initial shipments targeted at major European automotive OEMs. Source: Industry Publication

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 3.54 Billion |

| CAGR | 10.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.3% |

| Scope of Report | Market is segmented by Type (Aluminum-Rich Alloys, Balanced Aluminum-Molybdenum Alloys, Molybdenum-Rich Alloys, Specialty Alloys, Custom Composites), Application (Aerospace, Automotive, Construction, Electrical & Electronics, Industrial Machinery), End-User Industry (Aerospace Manufacturers, Automotive OEMs, Construction Firms, Electronics Manufacturers, Heavy Machinery Producers), Distribution Channel (Direct Sales, Distributors and Dealers, Online Platforms) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Alcoa Corporation (United States), Materion Corporation (United States), Kobe Steel, Ltd. (Japan), Rio Tinto Group (United Kingdom), Glencore International AG (Switzerland), Aleris Corporation (United States), Constellium SE (France), AMAG Austria Metall AG (Austria), Aluminium Bahrain B.S.C. (Bahrain), Hydro Aluminium ASA (Norway), Norsk Titanium AS (Norway), Novelis Inc. (United States), Metalcorp Group (United Arab Emirates), Thyssenkrupp AG (Germany), Outokumpu Oyj (Finland), Elkem ASA (Norway), Aluminium Dunkerque (France), Alro S.A. (Romania), Trimet Aluminium SE (Germany), Mubadala Investment Company (United Arab Emirates), Eramet Group (France), AMAG Rolling GmbH (Austria), Constellium Rolled Products Ravenswood LLC (United States), Sapa Group (Norway), Befesa S.A. (Spain) |

EMEA Aluminum Molybdenum Alloy Market - Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.