China Financial Crime Prevention Market Insight 2025-2034

China Financial Crime Prevention Market is segmented by Application (Banking, Insurance, Government, Others), Type (Fraud Detection, AML, KYC, Transaction Monitoring), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Market Definition

When talking about China’s financial crime prevention, it's basically a mix of tech and processes aimed at catching and stopping financial wrongdoing — money laundering, fraud, terrorist funding, identity theft — you name it. This market covers all sorts of sectors — banks, insurers, government bodies, and other financial entities. Solutions are varied: Anti-Money Laundering systems, fraud detection tools, KYC or customer verification setups, and transaction monitoring software that watches for suspicious patterns. The end users are a broad set — from massive state-owned banks with complex legacy systems to nimble fintech startups trying to keep pace. The value chain is fragmented too: you have software vendors, consulting firms, system integrators, and managed security services all playing parts. Adoption isn’t uniform; some regions or sectors lag behind despite obvious risks. The regulatory push in China keeps evolving, forcing firms to upgrade or rethink their approaches, but practical implementation often trips over existing infrastructure or data silos. So, this market is both growing and uneven — driven by rising crime complexity and a patchwork of tech and policy responses.

Report Coverage

- •Drivers

- ◦China’s tightening regulatory environment forces firms to invest in prevention technologies.

- ◦Increasing digitalization of financial services expands the attack surface for criminals.

- ◦Government initiatives to digitize and secure financial supervision.

- ◦Rising incidents of financial fraud and cybercrime increase demand.

- •Trends

- ◦AI and machine learning increasingly used for real-time anomaly detection.

- ◦Blockchain tech being explored for transparency but adoption is uneven.

- ◦Fintech and traditional banks collaborating more on security solutions.

- ◦Cloud-based prevention tools gaining traction despite data concerns.

- •Opportunities

- ◦Growing financial inclusion in less served regions like Southwest and Northwest China.

- ◦Advancement in AI-driven transaction monitoring to catch subtle patterns.

- ◦Demand for integrated cloud solutions that reduce legacy infrastructure reliance.

- ◦Potential for partnerships between tech startups and established financial players.

- •Challenges

- ◦Lots of legacy systems still in place, complicating integration of new tech.

- ◦Data privacy laws and localization requirements restrict data sharing.

- ◦Skilled cybersecurity professionals are in short supply.

- ◦Adoption across sectors and regions is patchy, not consistent.

- •Market Entropy

Market Entropy

The financial crime prevention market in China is a bit of a mixed bag. On one hand, regulatory pressure is pushing firms to adopt advanced tech but on the other, the actual implementation is anything but smooth. In some regions, adoption is fast, like in East and South China, where fintech hubs and big banks lead the charge. Meanwhile, other areas like Northwest and Southwest China lag behind, often due to infrastructure gaps or less regulatory enforcement intensity. Also, the tech itself is unevenly adopted — AI-driven tools get hyped but many firms still rely on manual or semi-automated processes because fully automated systems are expensive or complex to integrate. Privacy regulations add another layer of complexity; firms are cautious with data sharing, which ironically can slow down fraud detection that thrives on data aggregation. So while the market grows steadily, it’s not linear or uniform — more of a patchwork with hotspots of innovation and pockets of inertia.

Merger & Acquisition News

Regional Analysis

China’s financial crime prevention market is dominated by East China, home to Shanghai and other financial hubs. This region benefits from better infrastructure, more sophisticated financial institutions, and a high concentration of fintech firms. South China, including Guangdong, follows closely with rapid fintech adoption and strong government backing for compliance technologies. North China, with Beijing’s regulatory centers, plays a critical role but has a somewhat slower tech adoption curve in some sectors. Central China and Northeast China are moderate players but lag a bit due to less developed financial ecosystems. Southwest China, though smaller in market share, is the fastest growing region due to increasing financial inclusion efforts and government development initiatives that push digital finance adoption. The regional disparity underscores the varied pace at which financial crime prevention technology spreads across the country.

Regulatory Landscape

- •China’s regulatory environment for financial crime prevention is aggressive but also complex. The People’s Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC) frequently update AML and KYC guidelines, pushing financial institutions to tighten controls. However, the pace and clarity of regulations sometimes cause confusion. Data localization requirements and cybersecurity laws restrict cross-border data flow, complicating cooperation with global partners. Enforcement is strict in major hubs but more uneven in less developed regions. There’s also a growing emphasis on integrating technology standards and encouraging use of AI and big data analytics for crime detection, but practical implementation is uneven and often slowed by legacy system challenges. Firms often find themselves navigating overlapping regulations, which can lead to compliance fatigue or partial adherence.

- •The Chinese government actively promotes financial security but balances this with concerns over privacy and data sovereignty, leading to sometimes contradictory guidelines. For example, institutions need to share data internally to detect fraud patterns but external sharing is heavily monitored. This dynamic creates operational hurdles and forces many to develop local solutions rather than rely on global platforms. Overall, while the regulatory framework is a strong market driver, it also introduces complexity and uncertainty that firms must carefully manage.

Investment and Funding Scenario

Since 2025, investment in China’s financial crime prevention tech has seen a steady rise, especially from venture capital targeting AI-based startups. State-backed funds also support fintech innovation hubs in Shanghai and Shenzhen, focusing on compliance tech. However, investment is somewhat cautious due to regulatory uncertainties and the high cost of integrating solutions into existing infrastructures. Large tech firms like Ant Financial and Huawei continue to pour resources into developing proprietary solutions, indicating confidence in long-term market potential. Funding is more concentrated in coastal regions, reflecting the uneven geographic adoption of advanced crime prevention technologies.

Competitive Innovation Radar

Innovation in China's financial crime prevention market is largely driven by big local players leveraging AI and big data analytics to build predictive and real-time monitoring tools. Ant Financial's solutions are notable for integrating fraud detection tightly with payment systems, enabling faster alerts. Huawei focuses on infrastructure-level security layers, embedding prevention into networks and data centers. Ping An Technology emphasizes AI-driven KYC and identity verification, offering seamless onboarding experiences. International players like IBM and FICO bring advanced analytics and global compliance frameworks but often face hurdles integrating with local systems or navigating China’s regulatory landscape. Cloud adoption is gradually growing but still challenged by data sovereignty concerns. Despite heavy R&D, many solutions face the practical challenge of patchy implementation due to legacy systems and varying regional readiness, which tempers the innovation impact.

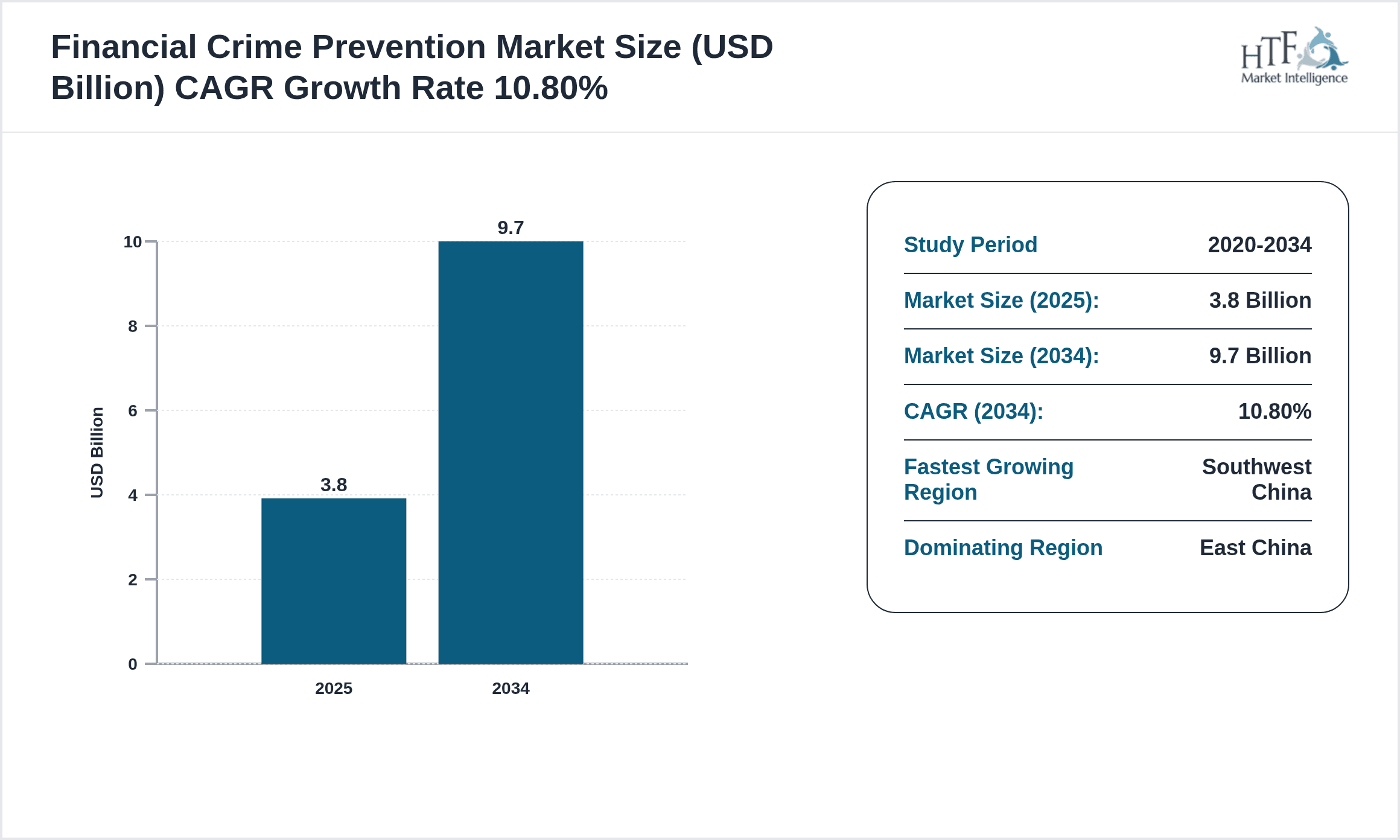

Market Size & Growth Table of China Financial Crime Prevention

- •Base Year Market Size: 3.8 USD Billion (2025)

- •Historical Year Market Size: 2.1 USD Billion (2020)

- •Forecast Year Market Size: 9.7 USD Billion (2034)

- •CAGR: 10.8%

- •Year-on-Year Growth: 11.4%

Regional Performance Analysis

- •Dominating Region: East China

- •Fastest Growing Region: Southwest China

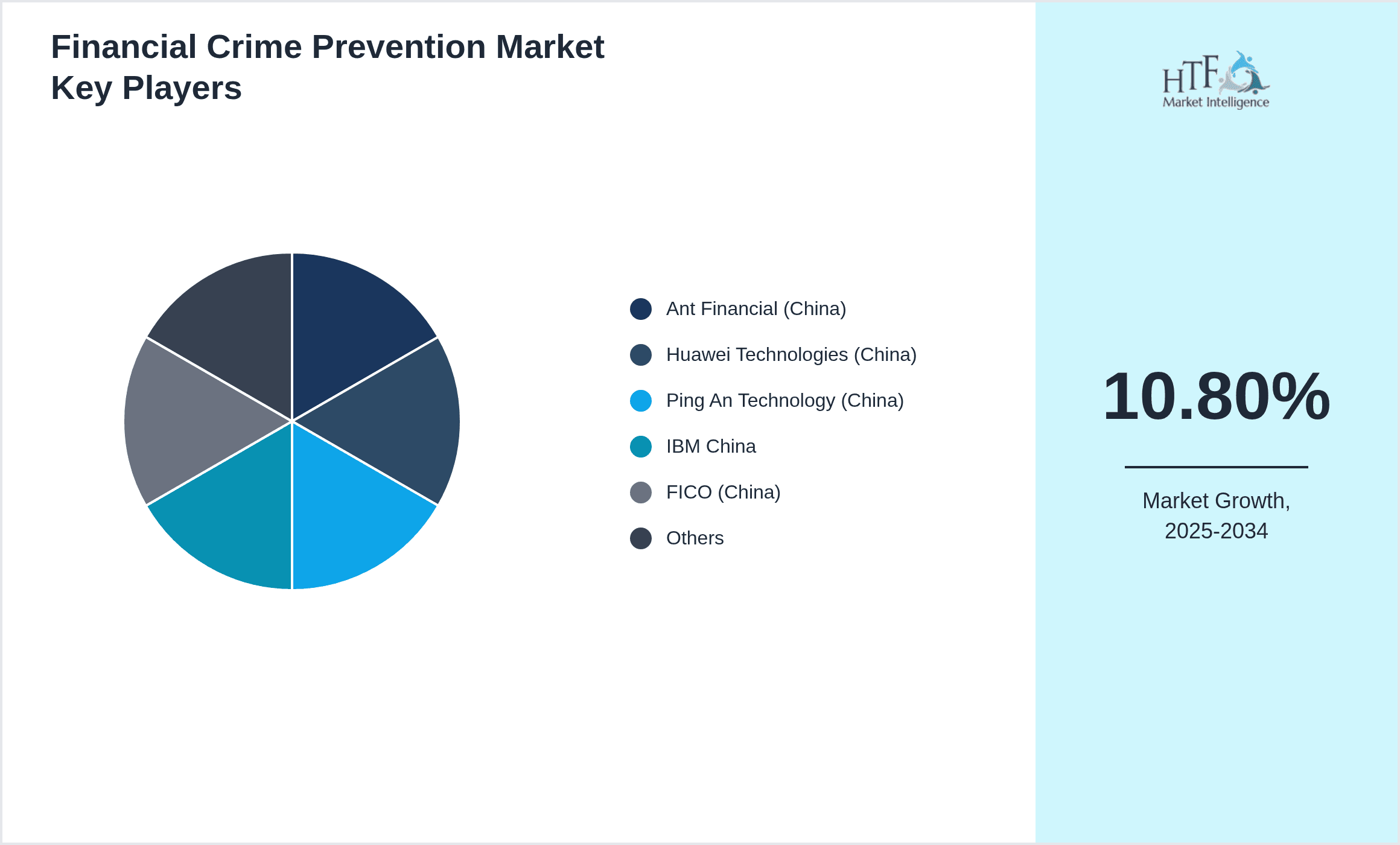

Players List

- •Ant Financial (China)

- •Huawei Technologies (China)

- •Ping An Technology (China)

- •IBM China

- •FICO (China)

- •Oracle Financial Services (China)

Competitive Analysis

The China financial crime prevention market is a dynamic landscape marked by a blend of domestic innovation and global expertise. Local giants like Ant Financial and Huawei dominate with deep integration into China’s financial ecosystem and regulatory environment, giving them an edge in customer reach and compliance alignment. They’ve built tailored solutions that mesh well with local payment systems and government mandates. Meanwhile, international firms such as IBM and FICO bring advanced analytics and broad compliance experience but often struggle with localization and regulatory nuances, slowing their market penetration. Market competition is intense but also cooperative in places, with partnerships forming between fintech startups and established banks to combine agility and scale. Yet, challenges remain — especially integrating new tech with entrenched legacy systems and navigating China’s complex regulatory maze. This creates opportunities for niche players that can bridge gaps or provide specialized services. The competitive field is evolving fast, driven by rapid technological advances and shifting regulatory demands, but progress is uneven across regions and sectors.

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 9.7 Billion |

| CAGR | 10.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.4% |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Ant Financial (China), Huawei Technologies (China), Ping An Technology (China), IBM China, FICO (China), Oracle Financial Services (China) |

China Financial Crime Prevention Market Insight 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.