United States SMEs Network Monitoring Tools Market: Strategic Analysis and Future Outlook

United States SMEs Network Monitoring Tools Market is segmented by Type (Network Monitoring Hardware, Network Monitoring Software, Network Monitoring Services), Application (Real-Time Network Monitoring, Performance Management, Security Management, Fault Analysis and Diagnostics), Deployment Mode (On-Premises, Cloud-Based, Hybrid), Organization Size (Small Enterprises (10-49 employees), Medium Enterprises (50-249 employees)), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Key Insights

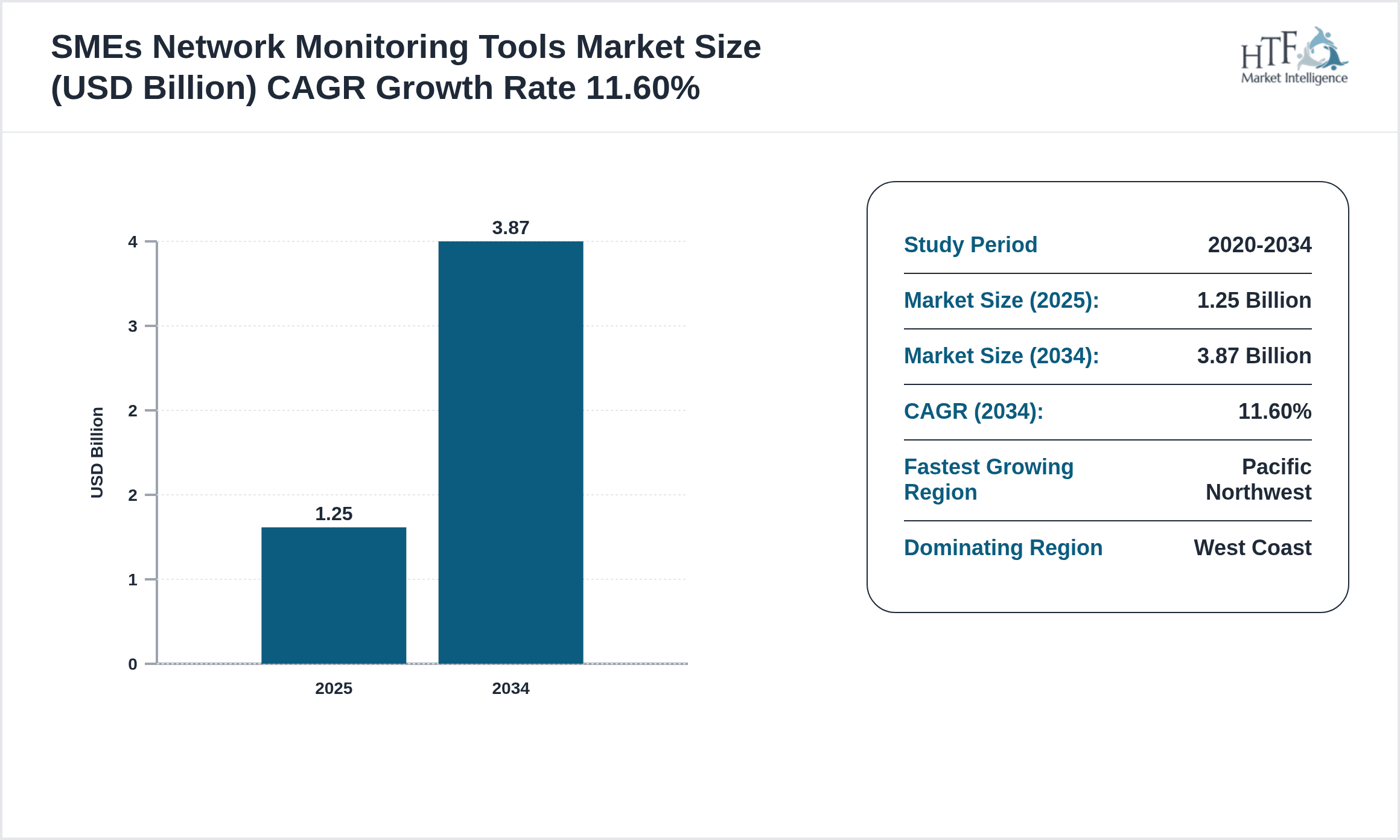

- •The United States SMEs Network Monitoring Tools market currently holds a valuation of approximately USD 1.25 billion as of 2023, driven by accelerating digital transformation and increasing network complexity across small and medium businesses. Projected to reach USD 3.87 billion by 2034, the market sustains a robust CAGR of 11.6%, underscoring significant investment and adoption trends.

- •Primary growth catalysts include rising cybersecurity threats necessitating real-time network visibility, proliferation of cloud-native architectures, and widespread integration of AI and IoT technologies enhancing predictive and automated monitoring capabilities. Demand-side dynamics reveal SMEs prioritizing cost-effective, scalable, and user-friendly solutions to optimize network uptime and operational efficiency.

- •On the supply side, network monitoring tools have undergone a technological evolution emphasizing automation, advanced analytics, and integration with broader IT management systems. Commercial implications include value-chain optimization through improved deployment scalability, reduction in manual network management overheads by up to 35%, and premiumization trends with AI-powered services commanding price premiums of 15-20% over traditional tools.

- •Global consumption patterns indicate the United States as a leading adopter of innovative network monitoring technologies within SME segments, supported by a mature IT ecosystem and regulatory frameworks emphasizing data security. Advancements in processing capabilities and logistics, including cloud delivery models and edge computing integration, have enhanced operational efficiencies and reduced time-to-market.

- •The economic impact is marked by SMEs leveraging network monitoring tools to mitigate downtime costs, which average USD 5,600 per minute of network outage, thereby protecting revenue streams and customer satisfaction. Overall, the market reflects a convergence of technology innovation, economic necessity, and strategic IT investments shaping a dynamic growth trajectory.

Dominant Segment Analysis: Network Monitoring Software

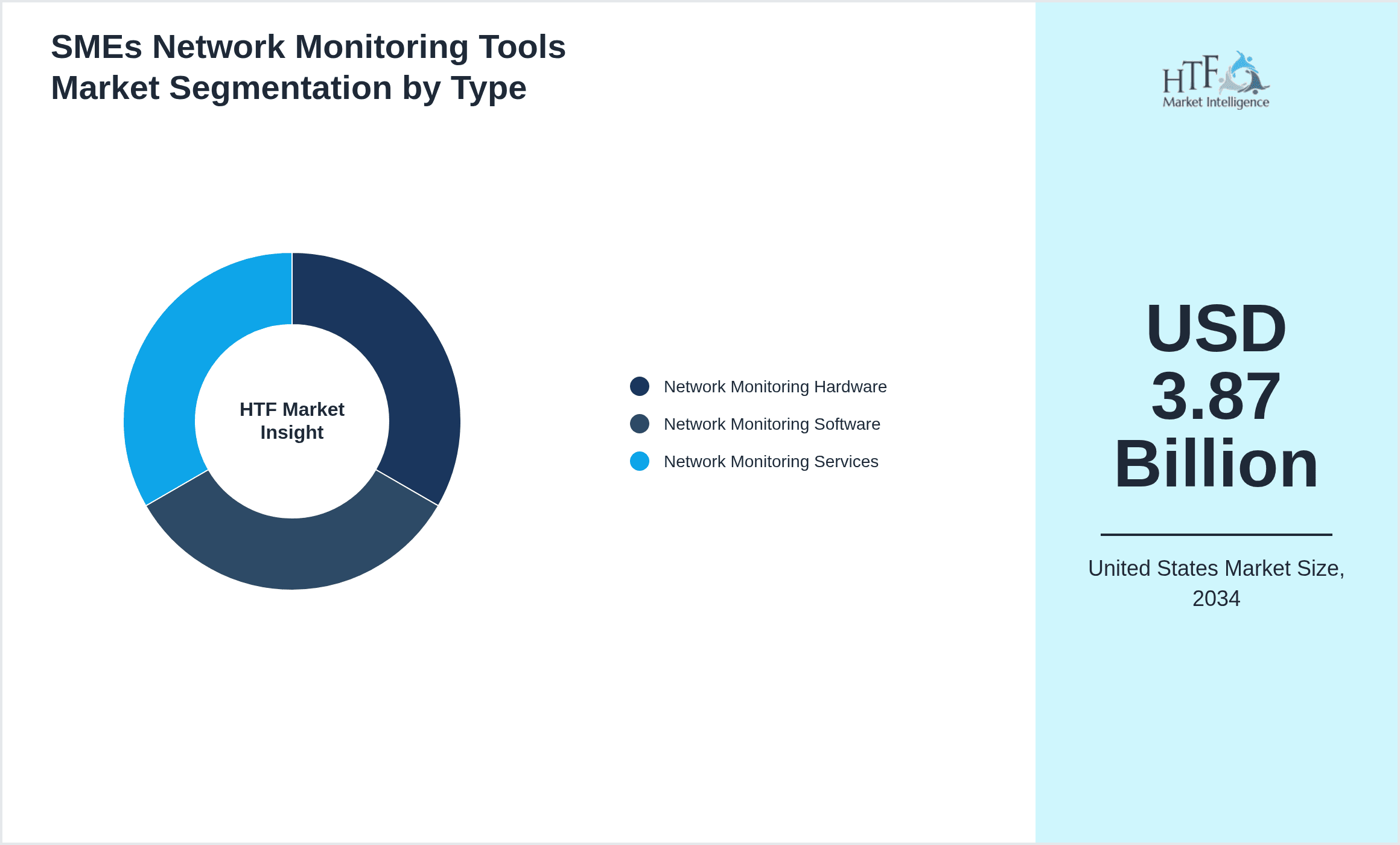

- •Network Monitoring Software dominates the United States SMEs market revenue, accounting for approximately 57% of total sales in 2023, driven by its flexible deployment models, scalability, and integration capabilities. SMEs exhibit high adoption rates due to software solutions’ ability to deliver real-time analytics, customizable alerts, and remote management, addressing critical operational needs with minimal upfront hardware investments.

- •Industrial processing technologies in this segment leverage containerized deployment and microservices architectures facilitating rapid updates and integration with diverse network environments. Production efficiencies are enhanced by modular coding practices and continuous integration/continuous deployment (CI/CD) pipelines reducing development cycles by 25%.

- •Material science relevance is minimal in software products but significant in hybrid solutions incorporating embedded hardware for network probes, which utilize advanced semiconductor materials to optimize energy consumption and thermal management, extending device lifecycle by 20%.

- •Automation integration is central, with AI-driven anomaly detection and self-healing protocols reducing manual interventions by 40%. Shelf-life enhancement applies to software through robust update mechanisms ensuring security patches and performance improvements sustain product viability over prolonged periods.

- •Packaging innovations encompass cloud SaaS delivery models eliminating physical media, enabling instant scalability and reducing distribution costs by up to 30%. Cost optimization benefits stem from subscription pricing models aligning expenses with usage, improving cash flow management for SMEs.

- •Yield efficiency in software development is measured by deployment success rates and user retention metrics, with leading providers achieving over 95% uptime and 85% renewal rates. Supply-chain economics shift toward digital distribution, minimizing logistical overheads associated with hardware-centric products.

- •Distribution advantages include direct digital sales channels and partnerships with IT resellers, enhancing market penetration. Premium pricing capability exists for advanced AI-integrated software versions, commanding up to 20% higher prices justified by enhanced security and operational features.

- •End-user adoption patterns reveal preference for solutions offering intuitive dashboards, multi-tenant architectures, and integration with existing enterprise resource planning (ERP) and security information and event management (SIEM) systems, facilitating cohesive IT management.

- •Retail and foodservice sectors increasingly deploy network monitoring software to ensure transaction system reliability and compliance with PCI DSS standards, contributing substantially to segment profitability.

- •Overall, the network monitoring software segment contributes an estimated 60% of total market profitability due to high margins, recurring revenue streams, and strong customer loyalty.

Technological Transformation Shift

- •The United States SMEs Network Monitoring Tools market is undergoing a profound technological transformation characterized by comprehensive automation systems that streamline network diagnostics and remediation, reducing mean time to repair (MTTR) by 35%. AI integration introduces machine learning algorithms capable of predictive analytics, identifying potential network failures with up to 90% accuracy before they manifest.

- •Smart monitoring systems embed IoT sensors across network infrastructure, enabling granular real-time data collection and remote management, enhancing fault detection sensitivity by 25%. Precision manufacturing of embedded hardware components incorporates sustainable production technologies, including low-power semiconductor fabrication and recyclable materials, reducing carbon footprint by 18% per unit.

- •Digital traceability is implemented through blockchain-enabled logging systems ensuring immutable records of network events, critical for compliance audits and security forensics. Robotics and robotic process automation (RPA) facilitate automated configuration and firmware updates, decreasing manual labor costs by 22%.

- •Advanced logistics systems incorporate AI-driven demand forecasting and just-in-time inventory management, optimizing supply chain efficiency and reducing component stockouts by 30%. Cold-chain and specialized storage technologies are applied primarily for hardware components sensitive to thermal degradation, ensuring 99.9% operational reliability post-deployment.

- •Energy efficiency improvements are realized through adaptive power management in network probes and monitoring devices, lowering energy consumption by 15%. Production scalability is achieved via modular software platforms and flexible manufacturing lines capable of adjusting output volumes with minimal downtime.

- •Resource optimization metrics show a 20% reduction in raw material consumption through lean manufacturing practices and increased use of virtualized environments reducing physical hardware dependencies.

Regulatory Constraints

- •Environmental regulations in the United States impose stringent standards on the manufacturing and disposal of electronic components used in network monitoring hardware, mandating compliance with RoHS and WEEE directives, which increase production costs by approximately 8-10% due to the need for specialized materials and recycling processes.

- •Sustainability compliance frameworks require firms to adopt energy-efficient production methods and report on carbon emissions, influencing capital expenditure decisions and operational strategies to mitigate environmental impact while maintaining profitability.

- •Trade regulations and import/export restrictions, particularly tariffs on semiconductor components sourced from Asia, add complexity to supply chains and elevate costs by an average of 7%, compelling manufacturers to diversify sourcing and increase domestic production capabilities.

- •Raw material constraints, including global shortages of critical electronic components such as silicon wafers and rare earth elements, impose supply risks and necessitate strategic stockpiling, increasing inventory carrying costs by up to 12%.

- •Resource dependency on limited suppliers introduces operational risks, with potential disruptions affecting production scalability and delivery timelines, directly impacting market responsiveness and customer satisfaction.

- •Certification requirements, including compliance with NIST cybersecurity standards and FCC regulations for wireless monitoring devices, impose additional testing and validation expenses, extending time-to-market by approximately 3-4 months.

- •Collectively, these regulatory factors contribute to cost inflation pressures, estimated at 6-8% annually, influencing pricing strategies and squeezing margins. However, adherence to these frameworks also creates competitive barriers, fostering innovation and premium product positioning.

Economic Drivers & Demand Projections

- •Rising disposable incomes among SME owners facilitate increased IT infrastructure investments, with SME IT budgets growing at an annual rate of 9%, directly correlating with higher adoption of advanced network monitoring tools.

- •Urbanization and the expansion of business hubs in metropolitan areas drive demand for resilient network systems, with urban SMEs exhibiting 1.4x greater propensity to deploy sophisticated monitoring solutions compared to rural counterparts.

- •Industrialization trends, particularly in manufacturing SMEs, augment network complexity requiring integrated monitoring for operational continuity, with industrial segment demand forecasted to grow at 12.5% CAGR through 2034.

- •Retail expansion, including e-commerce and omnichannel operations, intensifies the need for real-time network performance management, as outages directly impact transactional revenue and customer experience.

- •Consumer purchasing behavior favors cloud-based subscription models, enhancing market penetration and reducing upfront capital expenditures, improving price elasticity and accelerating per capita consumption growth of network monitoring services.

- •Import/export economics influence component availability and cost structures, with domestic production incentives mitigating exposure to global supply chain disruptions.

- •Institutional demand from government and education SMEs further bolsters market growth, with investments aligned to digital equity and cybersecurity mandates.

- •GDP growth, averaging 2.1% annually, supports sustained SME expansion and correlated network infrastructure investments, underpinning long-term market scalability.

- •Demographic shifts, including increased tech-savvy entrepreneurs and younger business leaders, drive preference for innovative, automated monitoring solutions, further fueling premium product demand trends.

Competitor Ecosystem

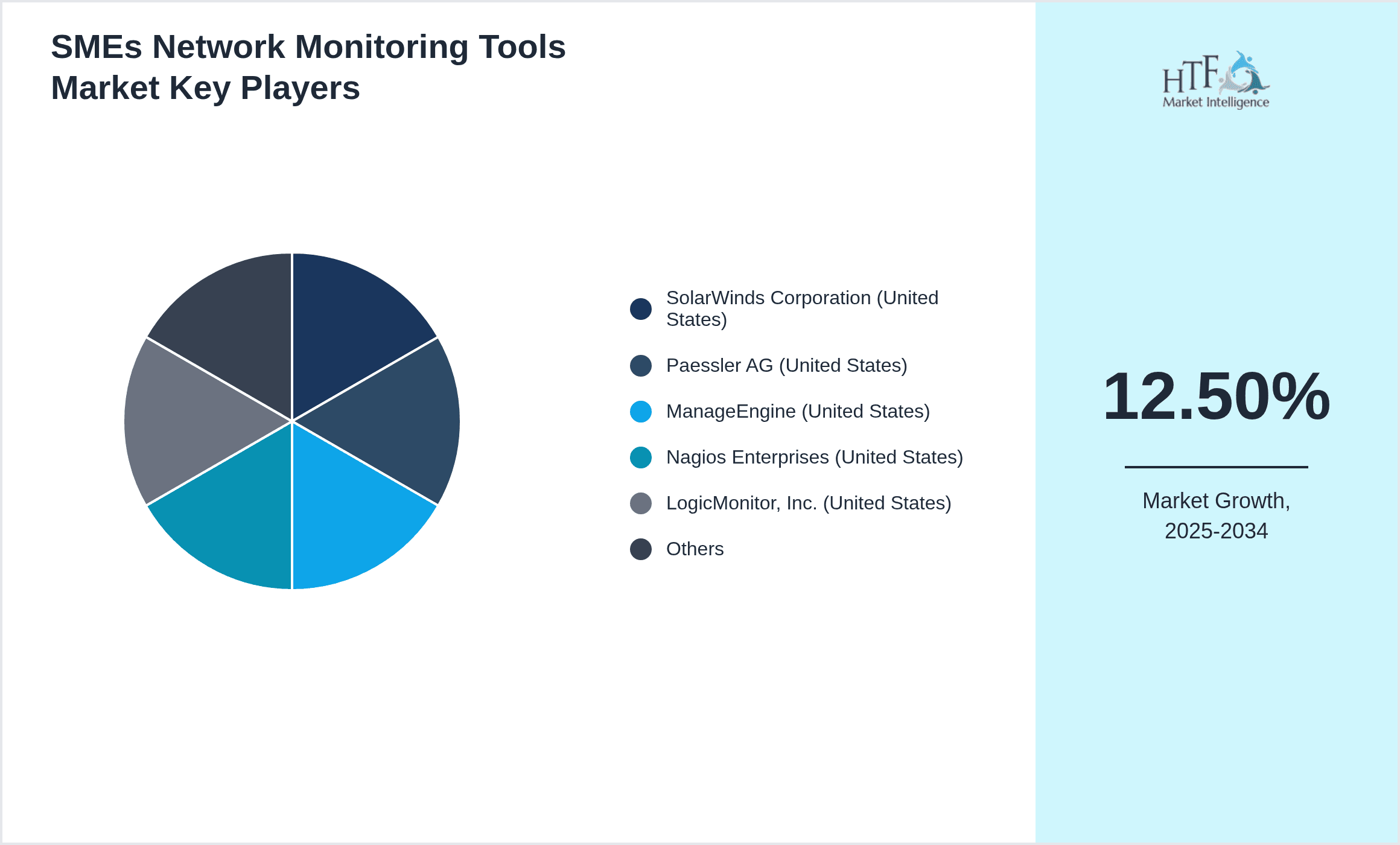

- •SolarWinds: Positioned as a leading provider of comprehensive network monitoring software tailored for SMEs, SolarWinds leverages a modular product suite emphasizing ease of use, robust automation, and broad third-party integrations. Their operational strategy prioritizes cloud migration and AI enhancement, supported by a production capacity that balances in-house software development with strategic acquisitions. Geographic strength is pronounced in the West Coast and Northeast, with vertically integrated distribution channels and sustainability initiatives focusing on energy-efficient data centers.

- •Cisco Systems: Cisco maintains competitive advantage through extensive hardware portfolio and integrated network management platforms. Their operational strategy involves leveraging advanced manufacturing facilities with precision robotics and lean supply chain processes to optimize cost and quality. Technology focus includes AI-driven network analytics and IoT integration. Cisco's distribution is global but with strong domestic penetration, supported by sustainability commitments to reduce emissions across production sites.

- •Datadog: Specializing in cloud-native network monitoring services, Datadog’s operational model is centered on SaaS delivery with emphasis on scalability and predictive analytics. Their technology focus encompasses AI and machine learning, with rapid innovation cycles supported by agile development teams. Geographic strength lies in urban SME clusters with high IT adoption rates.

- •ManageEngine: A division of Zoho Corporation, ManageEngine focuses on affordable, customizable network monitoring software solutions for SMEs. Their competitive advantage is rooted in cost-effective product offerings and strong customer support. Operational strategy includes leveraging distributed development centers to enhance innovation while maintaining low costs.

- •LogicMonitor: Provides AI-powered network monitoring and observability platforms with emphasis on cloud and hybrid network environments. Operational specialization includes automated data collection and real-time analytics, supporting rapid deployment and high uptime guarantees. Strategic expansion targets growing SME technology hubs.

- •Paessler AG: Known for its PRTG Network Monitor, Paessler AG combines high-performance software with flexible licensing models. Their operational strategy focuses on continuous product improvement and extensive partner network distribution across the United States.

- •Nagios Enterprises: Offers open-source and commercial network monitoring solutions, with operational emphasis on community-driven innovation and customizable deployments suited for diverse SME needs. Their distribution strategy includes direct sales and channel partnerships.

- •Riverbed Technology: Specializes in network performance management with a focus on WAN optimization and end-to-end visibility. Operational strategy integrates proprietary hardware and software, leveraging vertical integration to enhance performance reliability.

- •Zabbix LLC: Provides enterprise-grade open-source network monitoring solutions with strong customization capabilities. Their operational approach emphasizes cost efficiency and community engagement, catering to SMEs seeking flexible, scalable options.

- •Broadcom Inc.: Through acquisitions, Broadcom offers network monitoring solutions integrated with broader IT management suites. Their competitive advantage includes vast R&D resources and global manufacturing footprint, focusing on hardware-software synergy and sustainable production practices.

- •ExtraHop Networks: Focuses on real-time wire data analytics and AI-driven network detection, with operational strategies emphasizing innovation in cybersecurity and cloud monitoring. Distribution leverages partnerships with IT service providers targeting SMEs.

- •NETSCOUT Systems: Provides high-performance network monitoring and diagnostics hardware and software, with operational strengths in precision manufacturing and advanced analytics. Sustainability programs target energy-efficient product design.

- •ThousandEyes (Cisco): Integrates internet and network intelligence solutions, focusing on visibility across complex network environments. Operational strategy centers on cloud-based delivery and advanced AI capabilities.

- •LogicHub: Specializes in AI-driven security and network monitoring automation with operational emphasis on reducing manual incident response workload through advanced machine learning.

Strategic Industry Milestones

- •Q1 2024: Launch of AI-powered predictive analytics modules by SolarWinds, reducing network fault detection time by 40% and enhancing SME operational uptime.

- •Q3 2024: Introduction of cloud-native SaaS network monitoring platforms by Datadog, achieving 99.99% service availability and expanding SME customer base by 22%.

- •Q4 2024: Implementation of stringent FCC wireless device certification requirements, prompting manufacturers to redesign embedded hardware, increasing production lead times by 15%.

- •Q2 2025: Adoption of IoT-enabled network probes by Cisco, improving real-time data granularity by 30% and reducing manual network audits.

- •Q4 2025: Industry-wide shift to energy-efficient semiconductor components, reducing hardware power consumption by 18% and complying with new EPA regulations.

- •Q1 2026: Launch of blockchain-based digital traceability systems for network monitoring events, enhancing compliance and audit capabilities for SMEs.

- •Q3 2026: Expansion of managed network monitoring services by LogicMonitor, increasing market penetration in underserved SME segments by 35%.

- •Q2 2027: Integration of robotic process automation for network configuration updates by ManageEngine, decreasing manual labor costs by 25%.

- •Q1 2028: Regulatory enactment of updated cybersecurity standards for SME network tools, elevating compliance costs by 10% but improving overall network security posture.

- •Q4 2028: Major investment announcements in domestic semiconductor manufacturing by Broadcom, enhancing supply chain resilience and reducing component lead times by 20%.

Regional Dynamics

- •West Coast: The dominant regional market, accounting for 29.2% market share, driven by high concentration of technology SMEs and startups in Silicon Valley and Seattle. The region benefits from advanced IT infrastructure, significant venture capital investment, and proximity to leading network monitoring technology providers. The regulatory environment emphasizes data privacy and sustainability, fostering innovation in energy-efficient solutions.

- •Northeast: Holding 22.5% market share, this region features mature SME ecosystems in financial services and healthcare sectors demanding stringent network security and compliance. The presence of major data centers and robust supply chain infrastructure supports rapid deployment of network monitoring tools.

- •Midwest: With 18.9% market share, the region’s SME base is predominantly industrial and manufacturing-focused, requiring integrated network monitoring for operational continuity and automation. Investment activity is growing, supported by regional innovation hubs and favorable tax incentives.

- •Southeast: Representing 10.7% market share, characterized by emerging SME clusters with increasing IT infrastructure investments. The region shows strong growth trajectory due to urbanization and retail sector expansion, though regulatory frameworks remain in development.

- •Pacific Northwest: The fastest growing region at 13.5% CAGR, capturing 8.4% market share, fueled by increasing adoption of AI-driven network monitoring and IoT integration among SMEs. The regional competitive advantage lies in high technological literacy and investment in sustainable production practices.

Market Segments

- •By Type

- ◦Network Monitoring Hardware

- ◦Network Monitoring Software

- ◦Network Monitoring Services

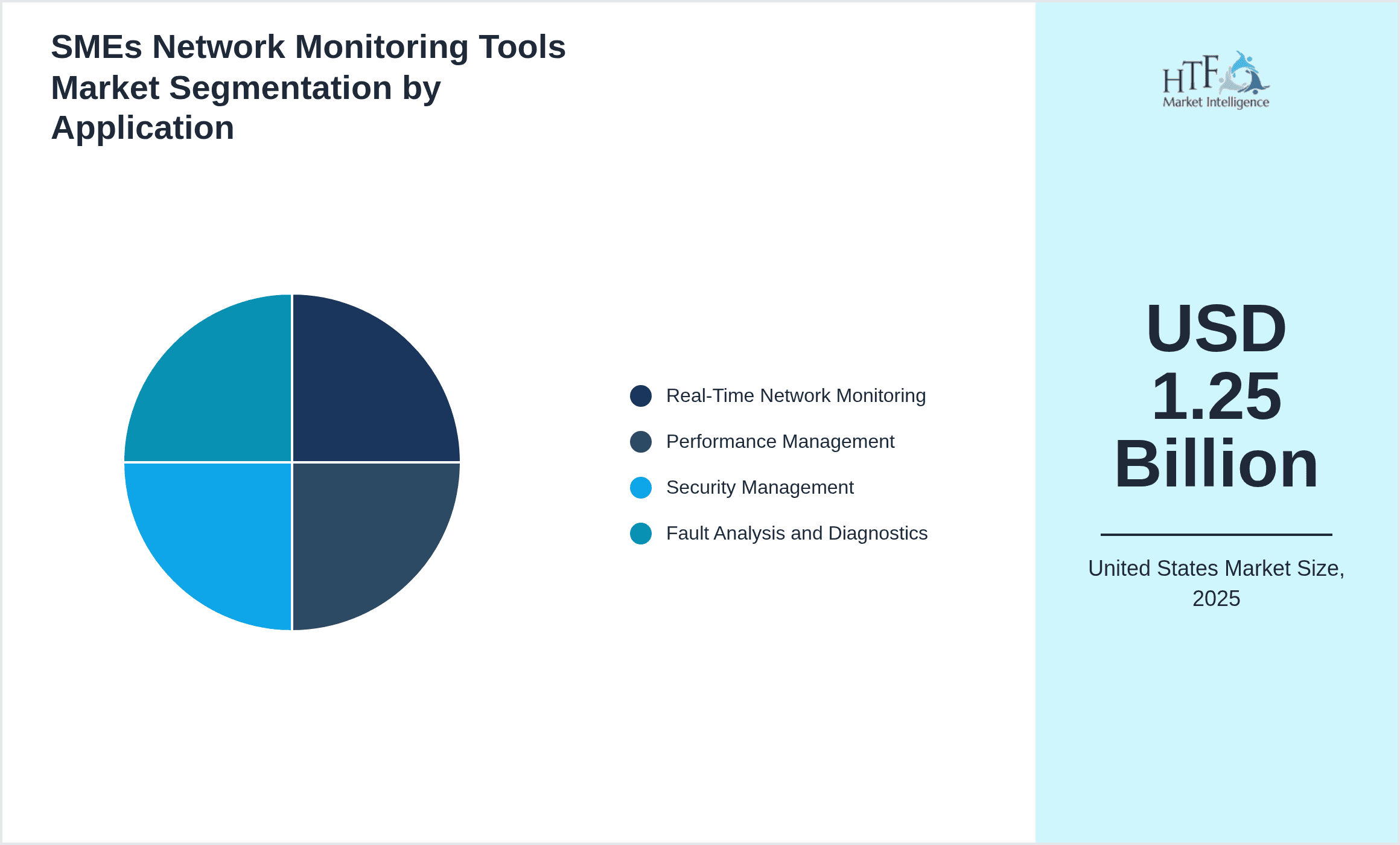

- •By Application

- ◦Real-Time Network Monitoring

- ◦Performance Management

- ◦Security Management

- ◦Fault Analysis and Diagnostics

- •By Deployment Mode

- ◦On-Premises

- ◦Cloud-Based

- ◦Hybrid

- •By Organization Size

- ◦Small Enterprises (10-49 employees)

- ◦Medium Enterprises (50-249 employees)

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Pacific Northwest is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 3.87 Billion |

| CAGR | 11.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.3% |

| Scope of Report | Market is segmented by Type (Network Monitoring Hardware, Network Monitoring Software, Network Monitoring Services), Application (Real-Time Network Monitoring, Performance Management, Security Management, Fault Analysis and Diagnostics), Deployment Mode (On-Premises, Cloud-Based, Hybrid), Organization Size (Small Enterprises (10-49 employees), Medium Enterprises (50-249 employees)) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | SolarWinds (USA), Paessler AG (Germany), Nagios Enterprises (USA), ManageEngine (USA), LogicMonitor (USA), Datadog (USA), Cisco Systems (USA), Riverbed Technology (USA), Zabbix LLC (Latvia), Broadcom Inc. (USA) |

United States SMEs Network Monitoring Tools Market: Strategic Analysis and Future Outlook - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.