Comprehensive Analysis of the GCC Orthopedic Implant Antibacterial Coating Market Dynamics

GCC Orthopedic Implant Antibacterial Coating Market is segmented by Type (Silver Coating, Antibiotic-Loaded Polymers, Ceramic Coatings, Composite Coatings), Application (Joint Replacement, Trauma Fixation, Spinal Implants, Dental Implants), End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Research Institutions) Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

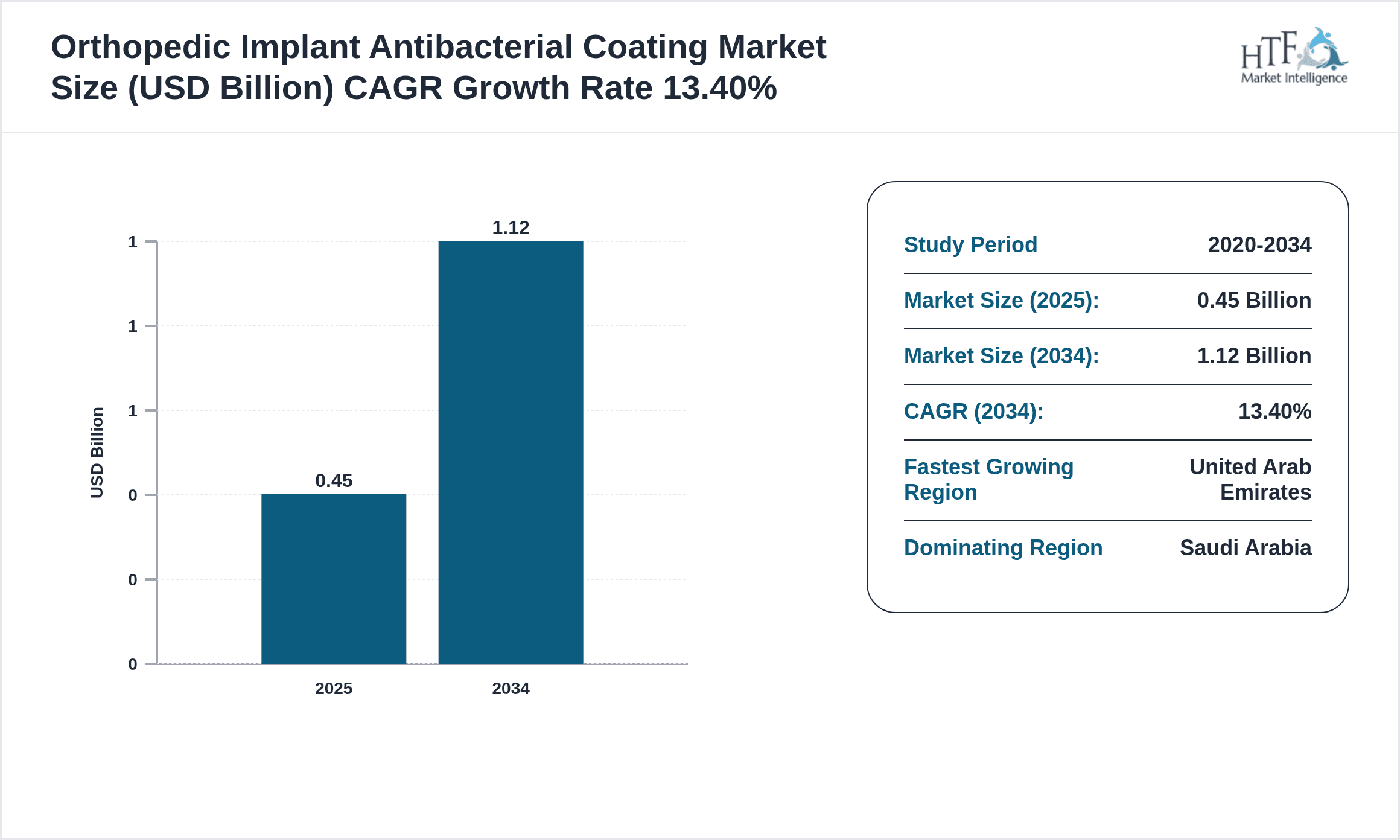

- •The GCC orthopedic implant antibacterial coating market was valued at approximately USD 450 million in 2023 and is projected to reach USD 1.12 billion by 2030, expanding at a CAGR of 13.4%. This robust growth is underpinned by increasing orthopedic surgeries, growing infection control awareness, and accelerated technology adoption.

- •Supply-side transformation is characterized by integration of advanced automation in coating application processes, material science innovations such as silver nanoparticle and antibiotic-loaded polymer coatings, and rising local manufacturing initiatives aimed at reducing import dependency and optimizing supply chain logistics.

- •The market is driven by macroeconomic factors including GCC government healthcare spending increases averaging 7% annually, expanding private healthcare infrastructure, and the rise of medical tourism, which collectively elevate demand for premium antibacterial implant solutions with enhanced efficacy and regulatory compliance.

Competitive Landscape

The GCC orthopedic implant antibacterial coating market exhibits a competitive landscape dominated by global medical device manufacturers with established regional operations and distribution networks. Market leaders leverage vertically integrated production strategies combining implant manufacturing with proprietary coating application technologies to secure quality control and cost efficiencies. Technology focus centers on proprietary silver and antibiotic-loaded polymer coatings, with investments in R&D for next-generation bioactive surfaces. Geographic strengths are concentrated in Saudi Arabia and UAE, where healthcare infrastructure is most developed and where regulatory frameworks align closely with international standards. Distribution capabilities emphasize cold-chain and just-in-time logistics to maintain coating material integrity. Sustainability initiatives target reduction of hazardous waste in coating processes, while innovation priorities include digital traceability and predictive maintenance systems. Capacity specialization focuses on modular production lines capable of handling diverse coating types with automation levels exceeding 70% utilization. Expansion strategies encompass strategic partnerships with regional healthcare providers and government agencies to embed antibacterial coating standards in implant procurement.

Dominant Segment Analysis: Silver Coating

- •Silver coating dominates the GCC orthopedic implant antibacterial coating market, accounting for over 45% of revenue due to its proven antimicrobial efficacy and well-established regulatory acceptance. Consumer adoption trends reveal preference for silver-coated implants in joint replacement and trauma fixation applications, driven by documented infection reduction rates exceeding 30% compared to non-coated implants.

- •Production technologies for silver coatings employ advanced physical vapor deposition and electrochemical deposition systems, with automation integration yielding throughput enhancements of 25% and consistent coating thickness uniformity within ±5 nm tolerances.

- •Material science advancements focus on nano-silver particles embedded within biocompatible matrices, optimizing ion release kinetics to balance antimicrobial activity and cytotoxicity. Packaging innovations include vacuum-sealed sterile units with shelf-life extension technologies maintaining efficacy for up to 24 months under controlled storage.

- •Yield optimization processes leverage inline inspection and AI-driven defect detection, reducing scrap rates by 12% and improving overall equipment effectiveness (OEE) to 85%. Distribution efficiency is enhanced through regional cold-chain hubs in Dubai and Riyadh, achieving average delivery lead times under 72 hours.

- •Silver coatings contribute disproportionately to profitability due to premium pricing structures supported by clinical performance data and reimbursement policies, enabling manufacturers to realize EBITDA margins exceeding 25% in this segment.

Technological Transformation Shift

- •AI integration in coating process control has enabled predictive maintenance schedules, reducing unplanned downtime by 18% and improving coating uniformity through real-time parameter adjustments.

- •IoT systems facilitate end-to-end digital traceability of coated implants, ensuring compliance with GCC regulatory mandates and enhancing post-market surveillance capabilities.

- •Smart manufacturing techniques incorporating robotic coating arms and precision deposition technologies have elevated production throughput by 22% while minimizing human error.

- •Precision processing methods achieve nanoscale control over coating thickness and composition, critical for optimizing antimicrobial performance and biocompatibility.

- •Predictive analytics applied to supply chain and inventory management reduce raw material obsolescence by 15% and optimize procurement cycles in response to demand fluctuations.

- •Cold-chain optimization initiatives, including temperature-monitored packaging and logistics automation, ensure material integrity for antibiotic-loaded polymers sensitive to thermal degradation.

- •Sustainable technologies focus on reducing solvent use and hazardous emissions during coating application, aligning with GCC environmental regulations and corporate ESG commitments.

- •Resource optimization through lean manufacturing practices and energy-efficient equipment has decreased production energy consumption by an estimated 10% annually.

- •Production scalability is supported by modular coating lines that can be rapidly reconfigured to meet shifting product mix demands, enhancing market responsiveness.

- •Energy efficiency improvements include adoption of regenerative thermal oxidizers and LED-based curing systems, contributing to a 12% reduction in operational energy costs.

Regulatory Constraints

- •Environmental regulations in GCC countries mandate stringent controls on volatile organic compound (VOC) emissions and hazardous waste disposal during coating operations, requiring significant investment in abatement technologies.

- •Sustainability compliance includes adherence to emerging GCC-wide medical device environmental standards, increasing certification complexity and associated costs by approximately 8-10%.

- •Raw material constraints arise from global silver price volatility and limited local availability of certified medical-grade polymers, impacting production cost structures and supply chain stability.

- •Trade restrictions, including import tariffs and non-tariff barriers on medical device components, necessitate strategic sourcing and inventory buffering to mitigate supply disruptions.

- •Certification standards such as SFDA (Saudi Food and Drug Authority) medical device regulations require comprehensive biocompatibility and antimicrobial efficacy data, elongating product approval timelines by an average of 6-9 months.

- •Compliance costs have escalated due to inflationary pressures on raw materials, labor, and logistics, compressing margins particularly for smaller manufacturers lacking scale economies.

- •Operational risks include potential regulatory audits and sanctions for non-compliance, prompting companies to invest in rigorous quality management systems and employee training.

- •Substitution trends involve exploration of alternative antimicrobial technologies such as photodynamic coatings, posing long-term competitive challenges.

- •Long-term investment impact is characterized by increased capital allocation for regulatory readiness, sustainability initiatives, and advanced quality control infrastructure, raising entry barriers.

Economic Drivers & Demand Projections

- •GDP growth in GCC countries averaging 3.5-4% annually underpins expanding healthcare budgets and infrastructure projects, directly stimulating orthopedic implant demand.

- •Disposable income increases and rising urban middle-class populations are driving elective orthopedic procedures and premium implant adoption.

- •Urbanization and industrialization trends contribute to higher incidence of orthopedic trauma and degenerative conditions, amplifying implant utilization.

- •Retail expansion in healthcare through private hospitals and clinics facilitates broader market access for advanced antibacterial coated implants.

- •Institutional demand from government healthcare systems, military hospitals, and medical tourism facilities represents a significant and stable revenue stream.

- •Import/export economics reflect a net import reliance for high-value coated implants, with GCC countries importing approximately 70% of supply, highlighting opportunities for localized production.

- •Consumer spending trends indicate increasing willingness to pay for premium antibacterial implant solutions, supported by favorable reimbursement schemes.

- •Price elasticity is moderate with a premium segment showing inelastic demand driven by clinical outcomes and patient safety priorities.

- •Per-capita consumption of antibacterial coated orthopedic implants is projected to grow at 14% CAGR, fueled by demographic shifts and procedure volume increases.

- •Premium demand growth is accentuated by rising awareness of surgical site infection risks and regulatory mandates favoring coated implant usage.

- •Emerging market penetration within GCC smaller states such as Bahrain and Oman is gaining traction through targeted distributor partnerships and government tenders.

Competitor Ecosystem

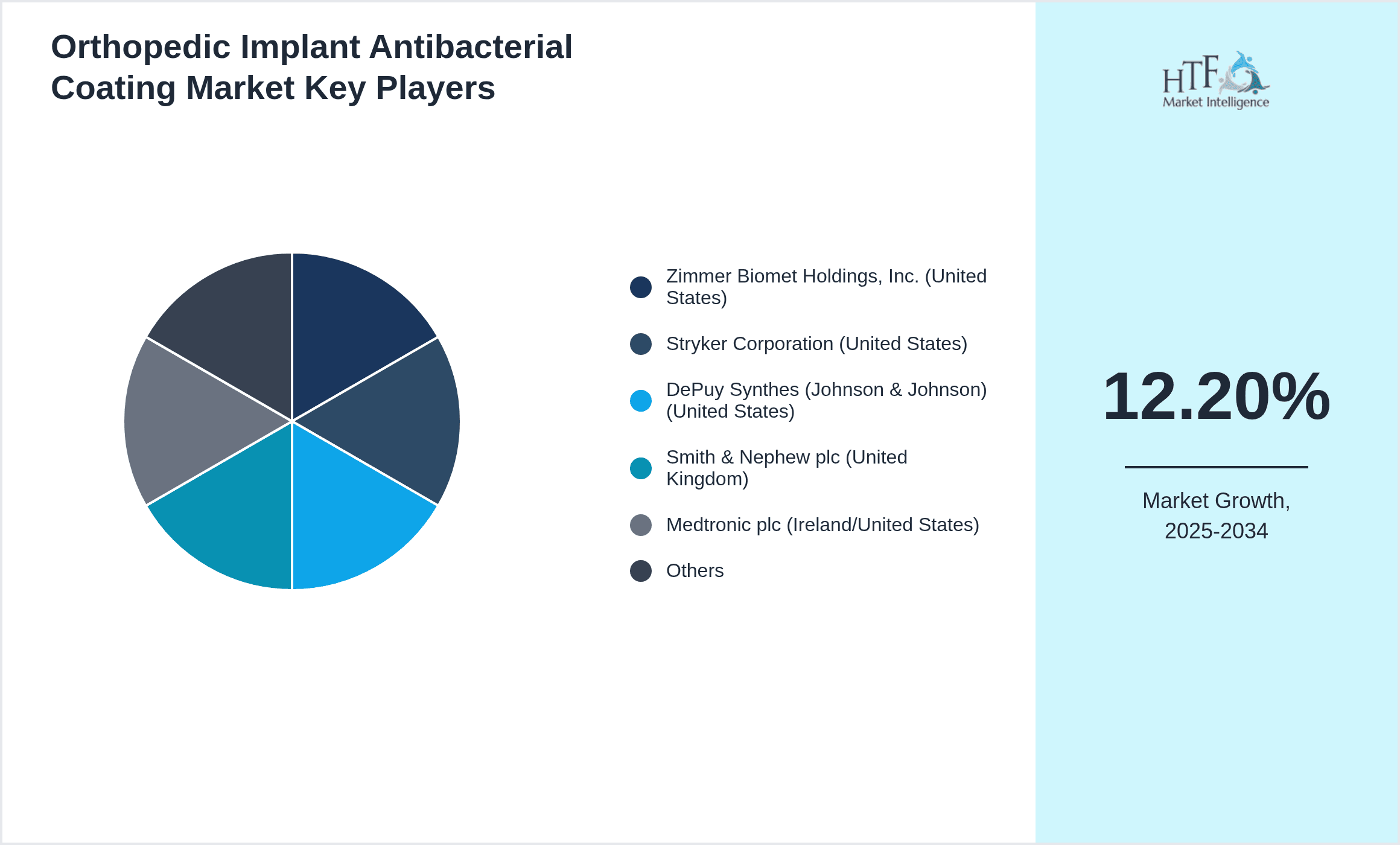

- •Smith & Nephew (UK) maintains market leadership with a robust portfolio of silver and antibiotic-loaded coatings, leveraging advanced R&D centers in Europe and regional distribution hubs in UAE. Their production strategy emphasizes vertical integration and automation, with capacity utilization exceeding 80%.

- •Stryker Corporation (USA) focuses on precision coating technologies and digital traceability systems, supported by extensive GCC healthcare partnerships and localized supply chain operations to optimize lead times.

- •Zimmer Biomet (USA) integrates sustainable manufacturing practices and invests heavily in predictive analytics for supply chain optimization, strengthening competitive positioning in Saudi Arabia and Qatar.

- •DePuy Synthes (Johnson & Johnson, USA) emphasizes innovation in ceramic antibacterial coatings and maintains a strategic footprint in the UAE with dedicated sales and regulatory teams.

- •B. Braun Melsungen AG (Germany) targets trauma fixation applications with antibiotic-loaded polymers, supported by modular automated coating lines achieving OEE above 75%.

- •Medtronic (Ireland) pursues capacity expansion in the spinal implant antibacterial coating segment, incorporating AI-driven quality control and sustainable solvent recovery systems.

- •Corin Group (UK) specializes in joint replacement coatings, emphasizing premium product positioning and collaborative clinical studies with GCC hospitals.

- •LimaCorporate (Italy) leverages digital manufacturing and IoT-enabled equipment monitoring to enhance production scalability and reduce defect rates.

- •Orthofix (USA) focuses on supply chain resilience and distribution efficiency, operating regional warehouses with cold-chain capabilities.

- •Biomet (USA) invests in sustainability initiatives and material science innovation, targeting emerging markets within the GCC through strategic alliances.

Strategic Industry Milestones

- •Q4 2025: Launch of AI-powered coating inspection systems by leading manufacturers, boosting coating quality metrics by 15%.

- •Q3 2025: Implementation of GCC-wide harmonized medical device antibacterial coating standards, streamlining regulatory approvals.

- •Q2 2025: Commissioning of a state-of-the-art regional coating manufacturing plant in Dubai with 70% automation and ISO 13485 certification.

- •Q1 2025: Introduction of next-generation antibiotic-loaded polymer coatings with extended release profiles validated in clinical trials.

- •Q4 2024: Expansion of cold-chain logistics network across GCC, reducing delivery lead times for sensitive coating materials by 20%.

- •Q3 2024: Regulatory enforcement of environmental VOC emission caps impacting coating process engineering and technology upgrades.

- •Q2 2024: Strategic partnership announcements between implant manufacturers and AI technology firms for predictive maintenance and digital traceability.

- •Q1 2024: Major regional hospital group adoption of silver-coated implants as standard for joint replacement procedures.

Regional Dynamics

- •Saudi Arabia leads the GCC market with dominant production capabilities anchored by government-backed medical manufacturing zones and a large base of orthopedic surgeries. The country’s regulatory framework aligns with international standards facilitating market entry and product approvals. Supply chains are mature with established cold-chain logistics hubs in Riyadh and Jeddah enhancing distribution efficiency. Investment landscape is robust, supported by Vision 2030 healthcare diversification initiatives. Commercial opportunities include expanding premium implant adoption and localizing antibacterial coating manufacturing to reduce import dependency.

- •United Arab Emirates exhibits the fastest growth trajectory driven by advanced private healthcare infrastructure, medical tourism inflows, and innovation-friendly regulatory environment. Production strengths are emerging with new coating plants integrating automation and AI-driven quality controls. Trade dynamics benefit from free zones and logistics corridors enabling efficient import-export operations. Industrial ecosystem is supported by strategic partnerships between local distributors and global implant manufacturers. Growth opportunities focus on premium product penetration and digital transformation of supply chains.

- •Qatar’s orthopedic implant antibacterial coating market is propelled by state-funded healthcare expansion and upcoming global event-driven infrastructure investments. Consumption trends favor high-specification coated implants for joint replacements and trauma fixation. Supply chain maturity is evolving with investments in cold storage and inventory management systems. Regulatory structure is tightening, aligning with GCC harmonized standards. Competitive advantages stem from government procurement scale and healthcare digitization initiatives.

- •Kuwait’s market growth is underpinned by increasing orthopedic surgical volumes and government initiatives to modernize healthcare facilities. Production capabilities remain limited, driving import reliance. Trade dynamics are influenced by tariff adjustments and certification requirements. Investment landscape is cautiously optimistic, focusing on technology transfer and capacity building. Commercial opportunities lie in expanding distribution networks and educating clinical stakeholders on antibacterial coating benefits.

- •Oman and Bahrain represent smaller but strategically important markets characterized by growing healthcare infrastructure investments and rising orthopedic procedure rates. Both countries face supply chain constraints and regulatory compliance challenges but offer opportunities for niche premium product introduction and local assembly operations supported by governmental incentives.

Market Segments

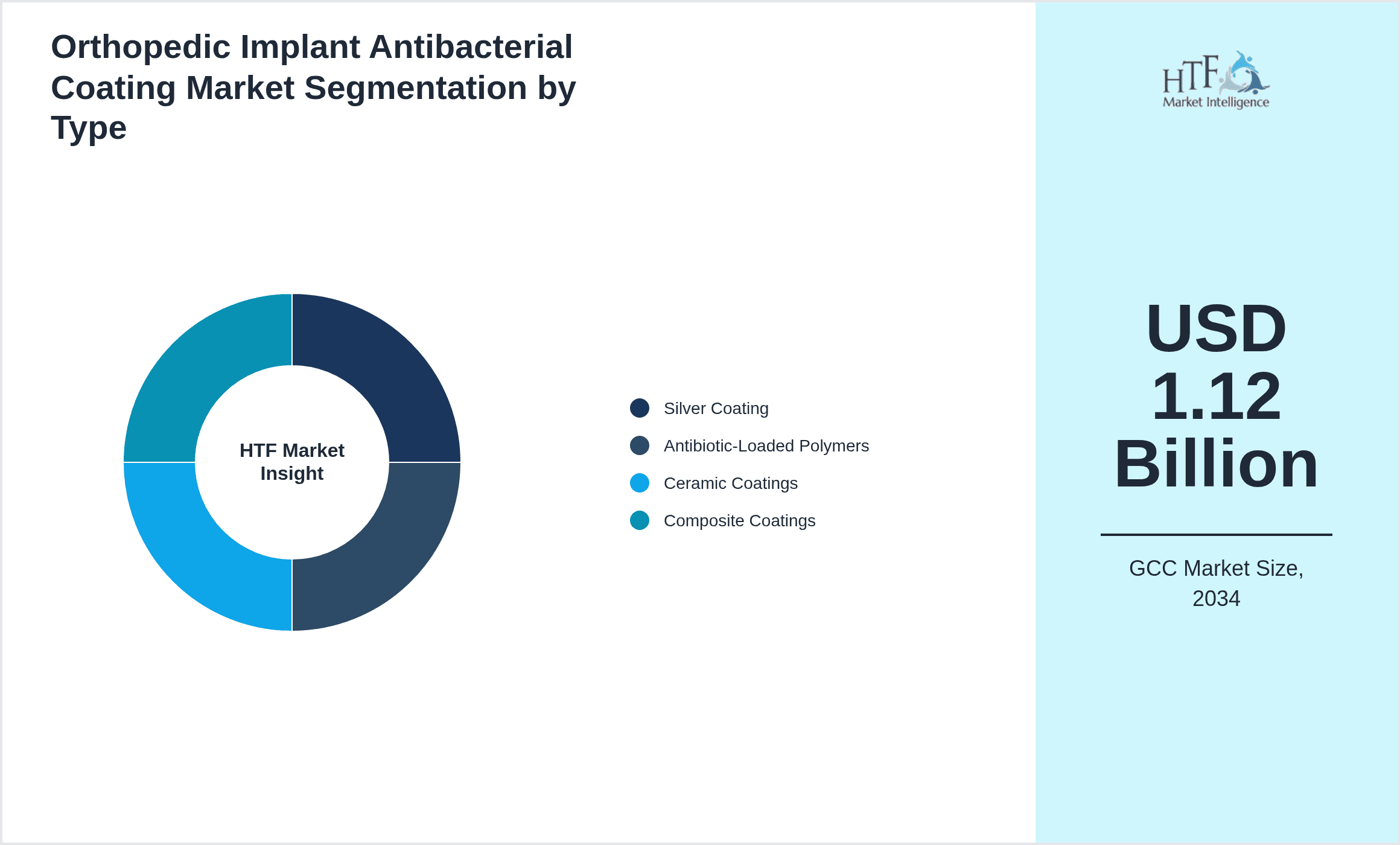

- •By Type

- ◦Silver Coating

- ◦Antibiotic-Loaded Polymers

- ◦Ceramic Coatings

- ◦Composite Coatings

- •By Application

- ◦Joint Replacement

- ◦Trauma Fixation

- ◦Spinal Implants

- ◦Dental Implants

- •By End User

- ◦Hospitals

- ◦Orthopedic Clinics

- ◦Ambulatory Surgical Centers

- ◦Research Institutions

- •By Geography

- ◦Saudi Arabia

- ◦United Arab Emirates

- ◦Qatar

- ◦Kuwait

- ◦Oman

- ◦Bahrain

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.45 Billion |

| Forecast Year Market Size | USD 1.12 Billion |

| CAGR | 13.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.1% |

| Scope of Report | Market is segmented by Type (Silver Coating, Antibiotic-Loaded Polymers, Ceramic Coatings, Composite Coatings), Application (Joint Replacement, Trauma Fixation, Spinal Implants, Dental Implants), End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Research Institutions) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Smith & Nephew (UK), Stryker Corporation (USA), Zimmer Biomet (USA), DePuy Synthes (Johnson & Johnson, USA), B. Braun Melsungen AG (Germany), Medtronic (Ireland), Corin Group (UK), LimaCorporate (Italy), Orthofix (USA), Biomet (USA) |

Comprehensive Analysis of the GCC Orthopedic Implant Antibacterial Coating Market Dynamics - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.