United States Industrial High Power Converters Market Size, Growth & Revenue 2025-2034

United States Industrial High Power Converters Market is segmented by Converter Type (AC-DC Converters, DC-DC Converters, AC-AC Converters, DC-AC Converters, Multilevel Converters), Industrial Application (Power Generation, Renewable Energy, Transportation, Manufacturing, Oil & Gas), Service Type (Installation and Commissioning, Maintenance and Repair, System Integration, Consulting and Engineering Services), Deployment Model (On-Premise, Cloud-Enabled Monitoring, Hybrid), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States Industrial High Power Converters market includes devices that convert electrical power in industrial settings, such as AC-DC, DC-DC, AC-AC, DC-AC, and multilevel converters. These converters serve critical applications including power generation, renewable energy integration, transportation electrification, manufacturing automation, and the oil & gas sector. The market value chain incorporates raw material suppliers, converter manufacturers, system integrators, and end users who require efficient and reliable power conversion solutions. Increasing industrial automation, demand for sustainable energy solutions, and modernization of power infrastructure are key drivers shaping market dynamics. Moreover, technological advancements in semiconductor devices, digital control systems, and thermal management have enhanced converter performance, efficiency, and lifespan. The market is characterized by strategic collaborations, innovation in multilevel and modular converter designs, and rising investments in electric grid modernization projects. Regulatory mandates on energy efficiency and emission reductions further stimulate adoption, positioning this market as a crucial enabler for the United States' industrial electrification and sustainability goals.

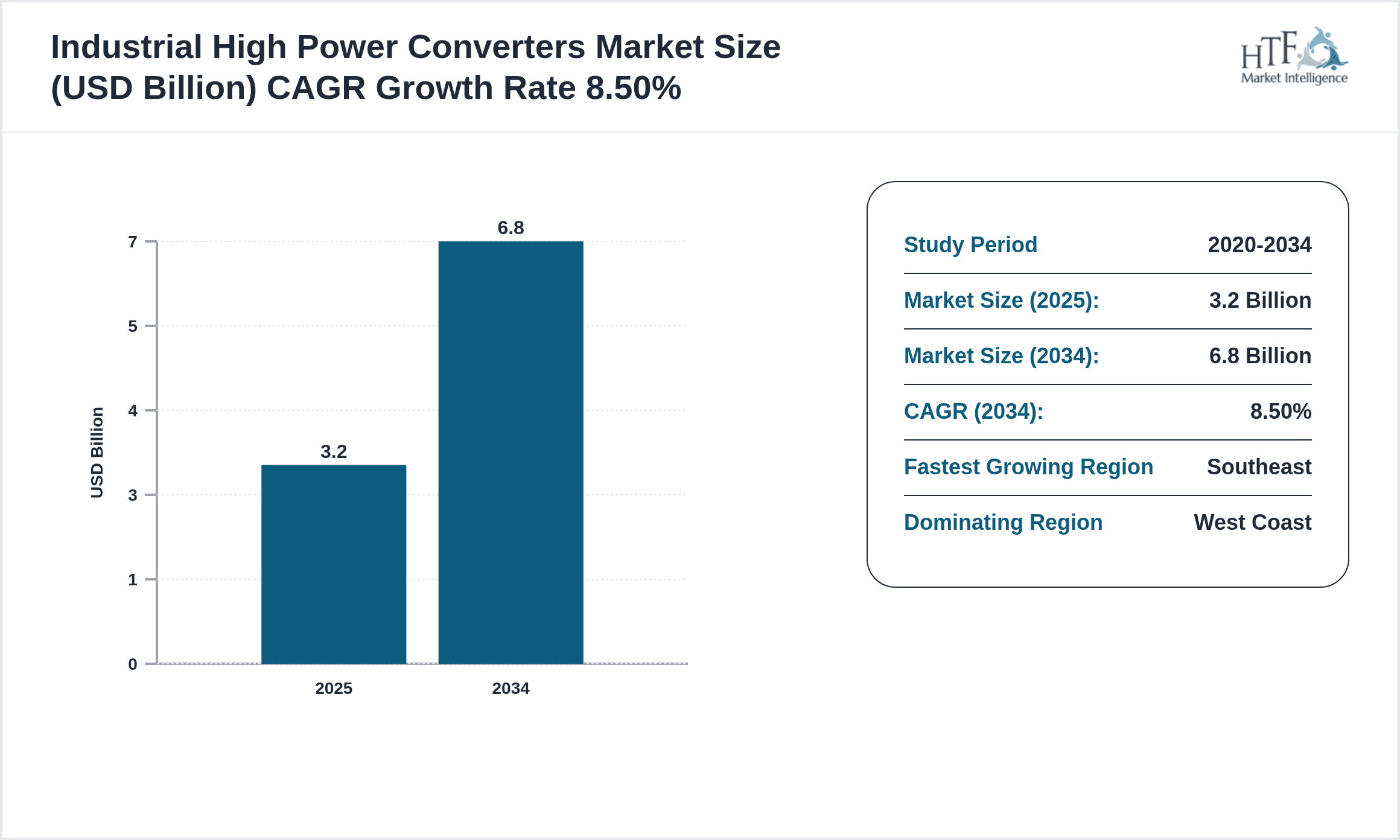

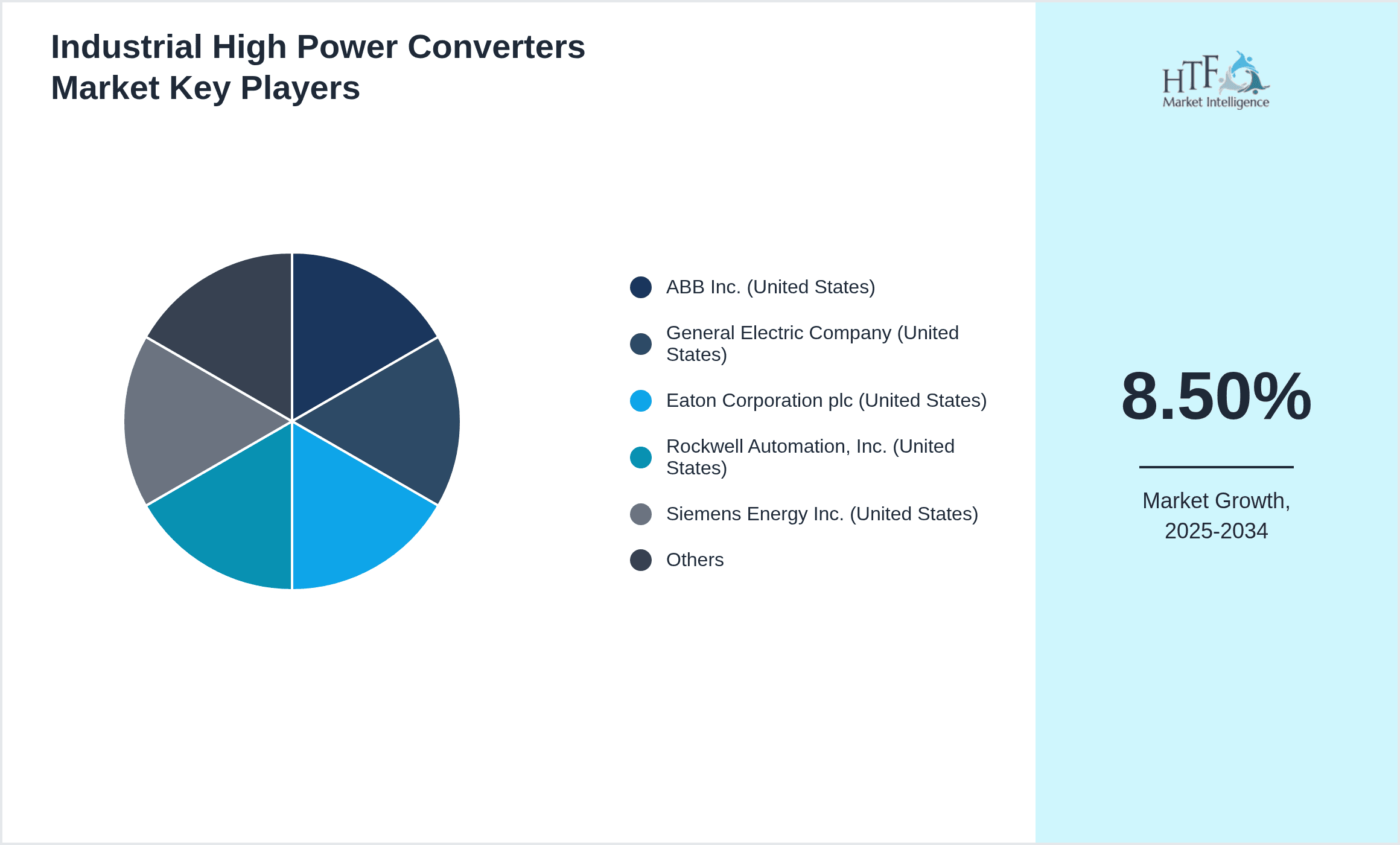

- •Key market highlights include a base market size of USD 3.2 Billion in 2025, projected to reach USD 6.8 Billion by 2034, reflecting a CAGR of 8.5%. The West Coast leads the market with a 31% share supported by robust manufacturing and renewable energy sectors, while the Southeast region is the fastest growing with an 11.3% CAGR driven by expanding industrial infrastructure and energy projects. AC-DC converters dominate product demand, whereas multilevel converters exhibit the highest growth potential due to their efficiency in high voltage applications. Year-on-year growth averages 8.2%, underscoring steady market expansion fueled by government incentives and private sector investments.

- •The market offers substantial value propositions to stakeholders including enhanced energy efficiency, reduced operational costs, and improved system reliability. Industrial end users benefit from tailored converter solutions that support complex load requirements and integration with renewable energy assets. Manufacturers leverage advances in power electronics to differentiate product offerings and enter new segments such as electric vehicles and smart grid applications. Strategic importance is underscored by the role of high power converters in national energy security, grid resilience, and emissions reduction targets, making this market a focal point for both policy makers and investors.

Competitive Landscape

The United States Industrial High Power Converters market is highly competitive, featuring a blend of established multinational corporations and specialized regional players. Market dynamics are influenced by innovation in semiconductor technology, modular design architectures, and digital control capabilities that enhance converter efficiency and reliability. Companies pursue strategic partnerships, mergers and acquisitions, and joint ventures to expand product portfolios and geographic reach. Pricing strategies revolve around value-based offerings emphasizing energy savings and total cost of ownership reduction. Distribution channels include direct sales, OEM partnerships, and integrators serving diverse industrial verticals. Barriers to entry include high R&D costs and stringent regulatory standards. The competitive environment is evolving with increasing emphasis on sustainable solutions, IoT-enabled monitoring, and predictive maintenance services, which collectively drive differentiation and customer loyalty. Regional competition varies, with the West Coast and Southeast regions emerging as innovation hubs, while regulatory compliance and supply chain optimization remain critical success factors across the market.

Leading Companies in Industrial High Power Converters Market

- •ABB Inc. (United States)

- •General Electric Company (United States)

- •Eaton Corporation plc (United States)

- •Rockwell Automation, Inc. (United States)

- •Siemens Energy Inc. (United States)

- •Schneider Electric USA, Inc. (United States)

- •Texas Instruments Incorporated (United States)

- •Mitsubishi Electric Power Products, Inc. (United States)

- •Power Electronics, Inc. (United States)

- •Dynapower Company (United States)

- •Semikron Electronics GmbH & Co. KG (United States)

- •Fuji Electric Corp. of America (United States)

- •Littelfuse, Inc. (United States)

- •Cree, Inc. (United States)

- •Infineon Technologies AG (United States)

- •Hitachi Energy USA, Inc. (United States)

- •ON Semiconductor Corporation (United States)

- •Toshiba International Corporation (United States)

- •Alstom Grid Inc. (United States)

- •Delta Electronics, Inc. (United States)

- •Efacec Power Solutions (United States)

- •Semiconductor Components Industries, LLC (United States)

- •Powerex, Inc. (United States)

- •Rexel USA (United States)

- •Yaskawa America, Inc. (United States)

Market Breakdown

- •By Converter Type

- ◦AC-DC Converters

- ◦DC-DC Converters

- ◦AC-AC Converters

- ◦DC-AC Converters

- ◦Multilevel Converters

- •By Industrial Application

- ◦Power Generation

- ◦Renewable Energy

- ◦Transportation

- ◦Manufacturing

- ◦Oil & Gas

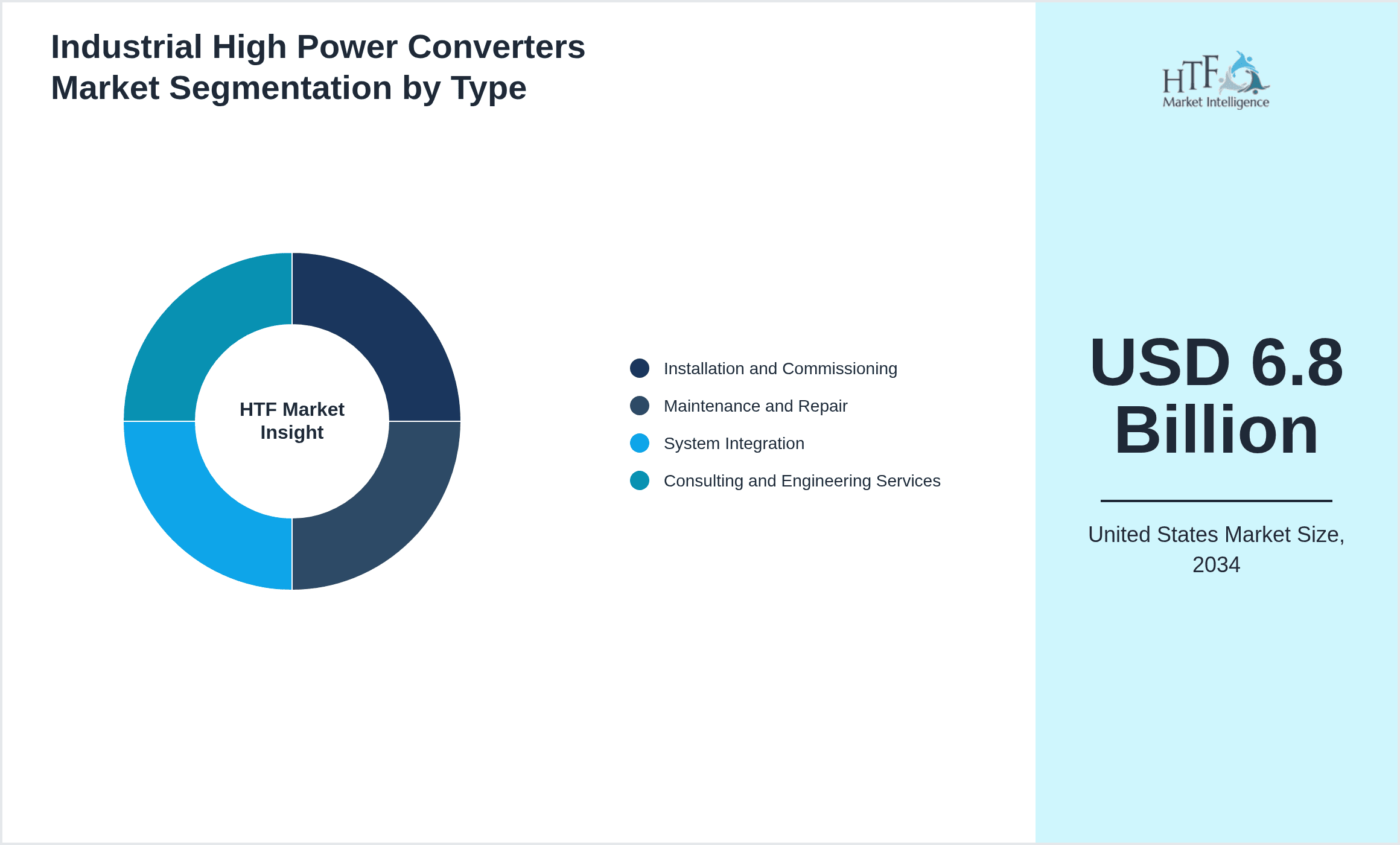

- •By Service Type

- ◦Installation and Commissioning

- ◦Maintenance and Repair

- ◦System Integration

- ◦Consulting and Engineering Services

- •By Deployment Model

- ◦On-Premise

- ◦Cloud-Enabled Monitoring

- ◦Hybrid

Growth Dynamics

- •Expansion of renewable energy projects in the United States, such as solar and wind farms, drives demand for high power converters capable of efficient grid integration and energy conversion, supported by government incentives and sustainability goals.

- •Advancements in power semiconductor technologies, including wide bandgap materials like SiC and GaN, enhance converter efficiency and thermal performance, enabling adoption in high voltage industrial applications and electric transportation systems.

- •Rising industrial automation and electrification initiatives across manufacturing sectors increase the need for reliable, scalable power conversion solutions that support complex motor drives and process controls, fostering market growth.

- •Stringent energy efficiency regulations and emission reduction mandates incentivize industries to upgrade existing power infrastructure with advanced converters that reduce losses and improve operational sustainability.

- •Integration of IoT and digital monitoring in power converters facilitates predictive maintenance and real-time performance optimization, attracting investments for smart factory and grid modernization projects.

- •Growing electrification in transportation, including electric trains and heavy-duty vehicles, necessitates robust high power converters tailored for harsh industrial environments and variable load conditions.

- •Increasing venture capital and private equity funding in innovative power electronics startups accelerates development and commercialization of next-generation converter technologies, expanding market opportunities.

Market Trends

- •Adoption of modular multilevel converters is rising due to their superior scalability, reduced harmonic distortion, and enhanced fault tolerance in high voltage industrial applications, reflected in growing deployments across power utilities.

- •Hybrid deployment models combining on-premise hardware with cloud-enabled monitoring platforms are gaining traction, enabling improved asset management and remote diagnostics for industrial converters.

- •Sustainability-focused innovation leads to integration of energy storage systems with high power converters, facilitating grid balancing and renewable energy smoothing applications, showcased by pilot projects in multiple states.

- •Collaborations between semiconductor manufacturers and converter producers accelerate development of SiC and GaN-based modules, driving improvements in converter efficiency and market competitiveness.

- •Increasing use of artificial intelligence and machine learning algorithms in converter control systems enhances predictive maintenance capabilities and operational reliability in industrial settings.

- •The trend towards electrification of industrial transport fleets stimulates demand for converters with enhanced power density and thermal management suited to mobile applications.

- •Emerging regulations around grid interconnection standards are influencing converter design, pushing manufacturers to innovate compliant and adaptive power conversion solutions.

Market Opportunities

- •Expansion of offshore wind energy projects presents significant opportunities for high power converter manufacturers to supply robust, efficient solutions tailored for harsh marine environments.

- •Increasing adoption of electric vehicles and charging infrastructure in commercial transport sectors opens new avenues for converters designed for high power density and rapid response capabilities.

- •Development of smart grid technologies and microgrid solutions drives demand for converters with advanced communication protocols and grid support functionalities.

- •Modernization of aging industrial power infrastructure offers potential for retrofit and upgrade projects utilizing next-generation converter technologies to improve energy efficiency and reliability.

- •Growing focus on energy storage integration in industrial applications necessitates specialized converters that enable bi-directional power flow and seamless energy management.

- •Collaborations with tech startups focused on AI-enabled power electronics can accelerate innovation and provide competitive differentiation in the converter market.

- •Government funding and incentives for clean energy projects provide financial support for adoption of advanced power conversion equipment across multiple industrial verticals.

Market Challenges

- •High initial capital expenditure for advanced high power converters and associated infrastructure limits adoption, particularly among small and medium-sized industrial enterprises.

- •Complexity in design and integration of multilevel and modular converters requires skilled engineering resources, creating barriers for widespread deployment and increasing project timelines.

- •Supply chain disruptions in critical semiconductor components, exacerbated by global geopolitical tensions, hinder timely production and delivery of power converters.

- •Stringent regulatory compliance demands necessitate continuous product certification and testing efforts, increasing operational costs and delaying market entry for new technologies.

- •Competition from low-cost international manufacturers pressures pricing and profitability margins for U.S.-based converter producers.

- •Limited awareness and adoption of IoT-enabled smart converters in traditional industrial sectors slow digital transformation and associated efficiency gains.

- •Thermal management challenges in high power applications require ongoing innovation to prevent equipment failure and maintain system reliability under demanding conditions.

Regulatory Framework

- •The Energy Independence and Security Act (EISA) of 2007-2025 mandates efficiency standards for power conversion equipment, requiring manufacturers to comply with minimum performance criteria that reduce energy losses and carbon emissions.

- •Federal Energy Regulatory Commission (FERC) regulations enforce grid interconnection standards and reliability requirements for high power converters used in utility-scale applications, impacting design and operational protocols.

- •The National Electrical Code (NEC) updates between 2020 and 2025 include provisions for safety standards specific to high voltage converter installations, ensuring user protection and equipment integrity.

- •Environmental Protection Agency (EPA) rules targeting reduction of hazardous substances in electronic equipment affect material selection and manufacturing processes of industrial converters.

- •State-level incentives and mandates, such as California’s Title 24 and New York’s REV initiative, promote adoption of energy-efficient power electronics, encouraging integration of advanced converters in industrial and commercial facilities.

Market Intelligence

- •15th January 2025, ABB Inc. announced the launch of its new high power modular multilevel converter platform designed for renewable energy applications. The platform features enhanced scalability, fault tolerance, and digital control integration enabling efficient grid connection of large-scale solar and wind farms across the United States. ABB targets utility and industrial clients aiming to modernize aging power infrastructure with this solution. The advanced converter supports wide voltage ranges and incorporates IoT-enabled monitoring for predictive maintenance, reducing downtime and operational costs. This launch reinforces ABB's strategic focus on sustainable energy markets and technological leadership in power electronics. Source: ABB Official Press Release

- •22nd March 2025, Eaton Corporation introduced a next-generation SiC-based AC-DC converter targeting electric vehicle charging stations and industrial motor drives. This converter delivers higher efficiency, reduced thermal losses, and improved power density compared to traditional silicon devices. Eaton's innovation aims to meet growing demands in electrification and smart manufacturing sectors. The product supports fast charging infrastructure and integrates with digital energy management platforms, enhancing grid stability and user experience. This development underscores Eaton’s commitment to sustainable industrial solutions and expanding its footprint in the U.S. power conversion market. Source: Eaton Corporation Press Release

- •10th May 2025, Rockwell Automation, Inc. announced a strategic partnership with a Silicon Valley startup specializing in AI-driven power converter diagnostics. The collaboration focuses on integrating artificial intelligence and machine learning algorithms into Rockwell’s industrial power converter portfolio to optimize operational efficiency and predictive maintenance capabilities. This initiative aims to reduce unplanned downtime and extend equipment lifespan for manufacturing clients. The partnership leverages Rockwell’s extensive industrial automation expertise and the startup’s innovative software solutions, positioning both companies to capture emerging opportunities in smart factory transformations. Source: Rockwell Automation News

- •30th August 2025, Siemens Energy Inc. completed acquisition of a U.S.-based power electronics company specializing in multilevel converter technologies for heavy industrial applications. The acquisition enhances Siemens' product offerings in the industrial high power converter segment and accelerates its roadmap for grid modernization projects. Siemens plans to integrate the acquired company’s advanced semiconductor modules and digital control systems into its portfolio, improving converter efficiency and reliability. This strategic move strengthens Siemens’ competitive position in the United States and aligns with increasing market demand for energy-efficient power conversion solutions. Source: Siemens Energy Corporate Announcement

- •Source: ABB Official Press Release, Eaton Corporation Press Release, Rockwell Automation News, Siemens Energy Corporate Announcement

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.2 Billion |

| Forecast Year Market Size | USD 6.8 Billion |

| CAGR | 8.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.2% |

| Scope of Report | Market is segmented by Converter Type (AC-DC Converters, DC-DC Converters, AC-AC Converters, DC-AC Converters, Multilevel Converters), Industrial Application (Power Generation, Renewable Energy, Transportation, Manufacturing, Oil & Gas), Service Type (Installation and Commissioning, Maintenance and Repair, System Integration, Consulting and Engineering Services), Deployment Model (On-Premise, Cloud-Enabled Monitoring, Hybrid) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | ABB Inc. (United States), General Electric Company (United States), Eaton Corporation plc (United States), Rockwell Automation, Inc. (United States), Siemens Energy Inc. (United States) |

United States Industrial High Power Converters Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.