EMEA Food and Beverage ERP Systems Market Scope & Changing Dynamics 2024-2034

EMEA Food and Beverage ERP Systems Market is segmented by Type (Cloud-based ERP Systems, On-premise ERP Systems, Hybrid ERP Systems, SaaS ERP Solutions, Hosted ERP Solutions), Application (Production Management, Supply Chain Management, Quality Control, Inventory Management, Sales & Distribution), End User (Food Processing Companies, Beverage Manufacturers, Packaging Firms, Distributors, Retail Chains), Deployment Model (Public Cloud, Private Cloud, On-premise, Hybrid Cloud), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Food and Beverage ERP Systems Market represents a crucial segment of enterprise software designed to optimize and integrate key operational facets of food and beverage companies across Europe, the Middle East, and Africa. Spanning a broad scope from supply chain management to quality control, these ERP systems facilitate transparency, regulatory compliance, and efficient resource utilization. Catering to diverse business scales and types, the solutions include cloud-based, on-premise, hybrid, SaaS, and hosted deployment models that accommodate evolving digital transformation needs. The market addresses critical industry challenges such as traceability, perishable inventory management, and rigorous safety standards, thereby enabling companies to enhance productivity and reduce costs. Increasing consumer demand for quality assurance, coupled with stringent food safety laws in the region, further propels the adoption of ERP systems. This specialized software ecosystem integrates modules for production, inventory, sales, and distribution management, furnishing end-users with comprehensive tools to streamline processes and maintain competitive advantage in a fragmented yet expanding market landscape.

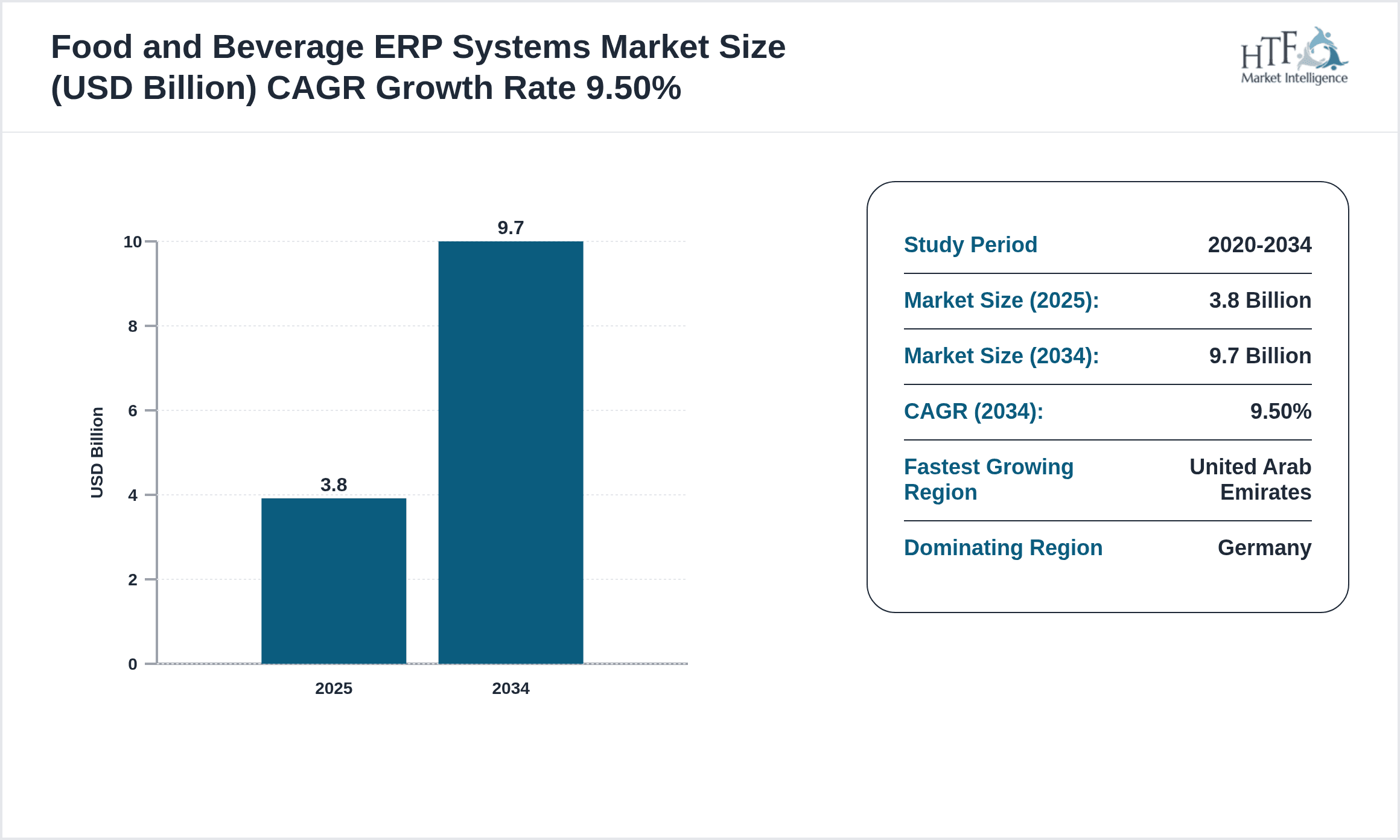

- •Key market highlights reveal a robust compound annual growth rate (CAGR) of 9.5% forecasted from 2024 to 2034, driven primarily by cloud-based ERP solutions which dominate the product landscape, accounting for 40% market share in 2024. Germany leads in regional market share at 28%, followed by France and the United Kingdom, while the United Arab Emirates emerges as the fastest-growing country with a CAGR of 14.2%. The escalating need for real-time data analytics, enhanced supply chain visibility, and regulatory compliance are pivotal growth factors. Additionally, the adoption of SaaS models is accelerating due to their scalability and cost-efficiency, marking it as the fastest growing product type. Year-over-year growth stands at approximately 9.1%, indicating sustained demand and market maturity with increasing integration of digital technologies across the EMEA food and beverage sector.

- •The strategic importance of Food and Beverage ERP Systems in EMEA is underscored by their ability to unify complex operational facets, enabling stakeholders including manufacturers, distributors, and retailers to make data-driven decisions. These systems deliver value by enhancing traceability, reducing waste, and ensuring compliance with diverse food safety regulations prevalent throughout the region. The adoption of advanced ERP solutions supports innovation, operational excellence, and agility in responding to evolving consumer preferences and supply chain disruptions. For technology vendors and investors, the market represents an expanding opportunity, fueled by digitization trends and regulatory mandates. The integration of AI and IoT within ERP platforms further enhances predictive capabilities and operational efficiency, positioning these solutions as indispensable tools in the competitive food and beverage industry landscape across EMEA.

Competitive Landscape

The EMEA Food and Beverage ERP Systems Market features a highly competitive environment characterized by a mix of global ERP providers and specialized regional vendors. Market competition is driven by innovation in cloud and SaaS offerings, with companies focusing on scalability, customization, and compliance to differentiate their solutions. Strategic alliances, product enhancements, and customer-centric service models are prominent competitive strategies. Vendors are investing heavily in developing AI-powered analytics, IoT integrations, and mobile ERP functionalities to capture greater market share. Pricing strategies vary from subscription-based models to perpetual licenses, catering to diverse customer requirements across small, medium, and large enterprises. Regional competition is influenced by differing regulatory landscapes, requiring flexible deployment options and localized support. The rivalry fosters continuous product development and mergers & acquisitions activity, enabling market consolidation and expansion of service portfolios to address evolving customer demands in EMEA.

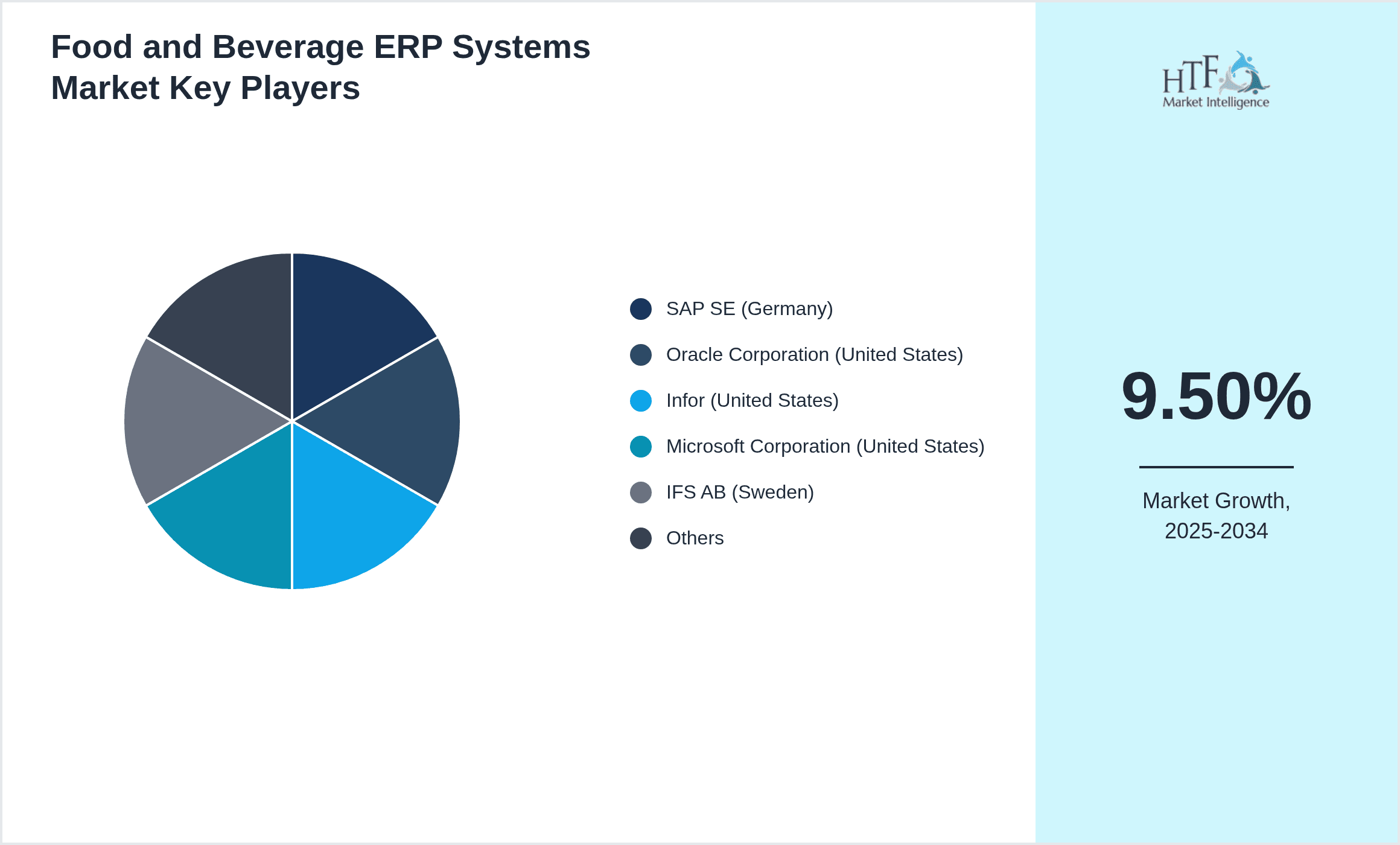

Leading Companies in Food and Beverage ERP Systems Market

- •SAP SE (Germany)

- •Oracle Corporation (United States)

- •Infor (United States)

- •Microsoft Corporation (United States)

- •IFS AB (Sweden)

- •Sage Group plc (United Kingdom)

- •Epicor Software Corporation (United States)

- •Plex Systems (United States)

- •Unit4 (Netherlands)

- •IFS (Sweden)

- •Workday, Inc. (United States)

- •QAD Inc. (United States)

- •SYSPRO (South Africa)

- •Ramco Systems (India)

- •Oracle NetSuite (United States)

- •Deltek, Inc. (United States)

- •Exact (Netherlands)

- •Priority Software (Israel)

- •abas ERP (Germany)

- •IFS Food & Beverage Solutions (Sweden)

- •ProAlpha Group (Germany)

- •Microsoft Dynamics 365 (United States)

- •SAP Business One (Germany)

- •Oracle JD Edwards (United States)

- •Infor CloudSuite Food & Beverage (United States)

Market Breakdown

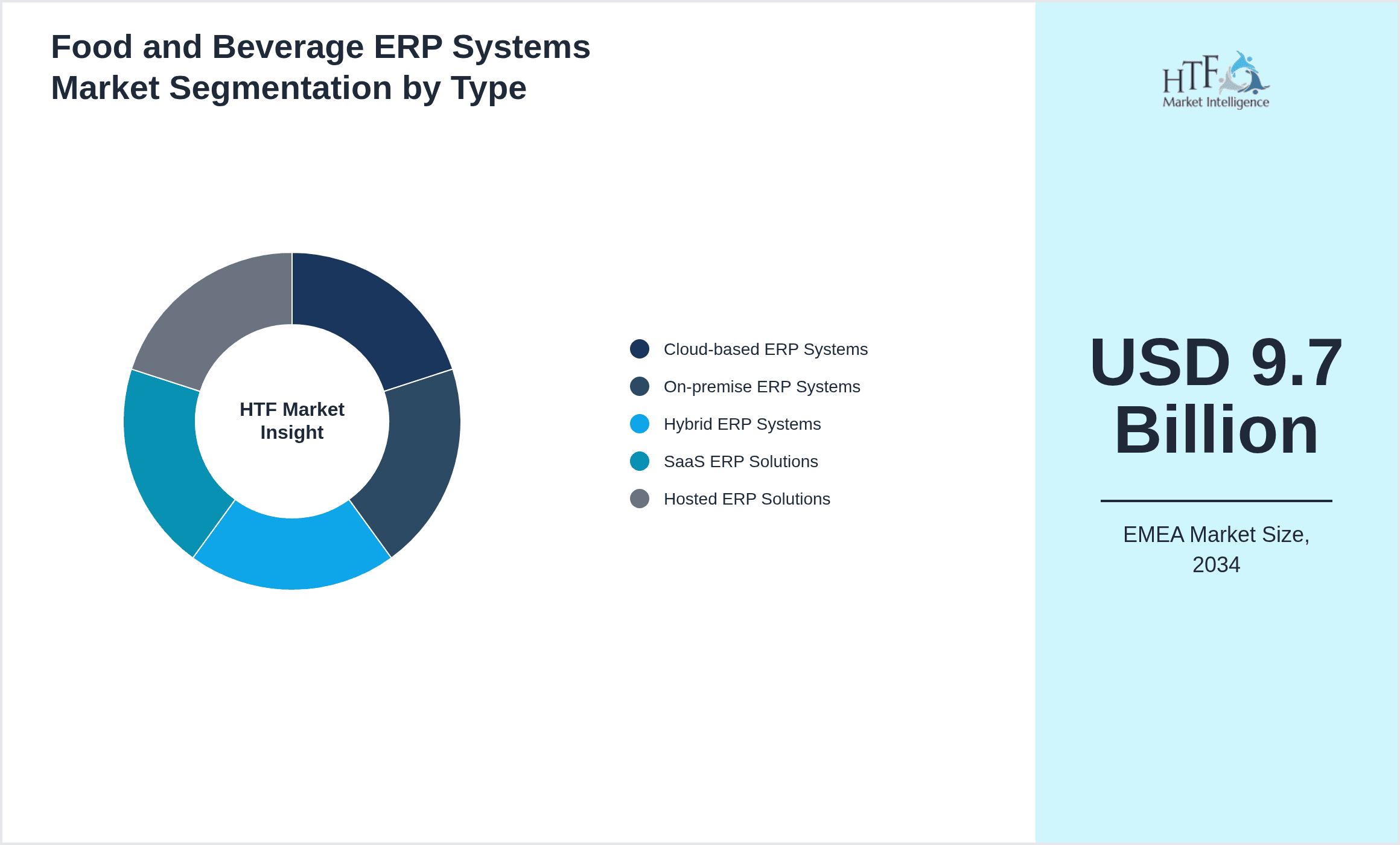

- •By Type

- ◦Cloud-based ERP Systems

- ◦On-premise ERP Systems

- ◦Hybrid ERP Systems

- ◦SaaS ERP Solutions

- ◦Hosted ERP Solutions

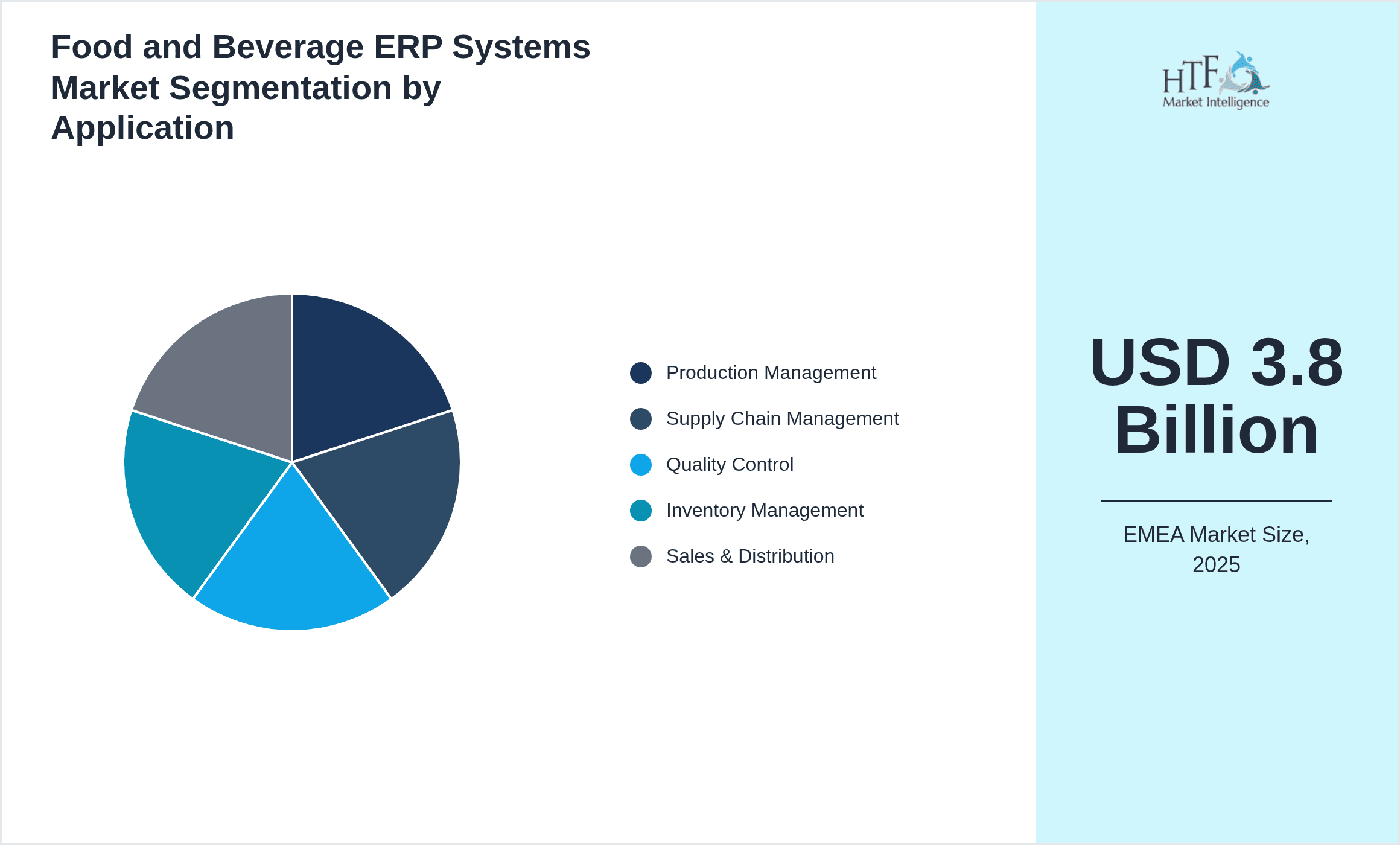

- •By Application

- ◦Production Management

- ◦Supply Chain Management

- ◦Quality Control

- ◦Inventory Management

- ◦Sales & Distribution

- •By End User

- ◦Food Processing Companies

- ◦Beverage Manufacturers

- ◦Packaging Firms

- ◦Distributors

- ◦Retail Chains

- •By Deployment Model

- ◦Public Cloud

- ◦Private Cloud

- ◦On-premise

- ◦Hybrid Cloud

Growth Dynamics

- •The increasing demand for real-time data analytics in food and beverage manufacturing drives the adoption of ERP systems by enabling enhanced decision-making and operational transparency. Companies are leveraging these capabilities to reduce production waste and improve quality control adherence.

- •Cloud-based ERP solutions are gaining traction due to their flexible deployment and lower upfront costs, allowing small and medium enterprises across EMEA to digitally transform without large capital expenditure. This shift is catalyzing market growth and expanding user base.

- •Stringent food safety regulations in the European Union and Middle East necessitate comprehensive traceability and compliance features, compelling manufacturers to implement advanced ERP systems to meet legal mandates and avoid costly penalties.

- •Integration of Internet of Things (IoT) technology with ERP platforms facilitates real-time monitoring of production lines and supply chains, offering predictive maintenance and enhanced inventory accuracy, which boosts operational efficiency across the region.

- •Rising consumer demand for clean-label and organic products drives manufacturers to optimize production processes with ERP systems that support complex ingredient tracking and certification management, fostering product differentiation and market expansion.

Market Trends

- •Adoption of Artificial Intelligence (AI) modules within ERP solutions is transforming the food and beverage sector by automating demand forecasting and enabling smarter supply chain management, leading to reduced costs and improved service levels.

- •The increasing prevalence of SaaS ERP models is shifting market dynamics by providing scalable, subscription-based software tailored to the unique needs of food and beverage companies, especially startups and SMEs in emerging EMEA economies.

- •Sustainability initiatives are prompting ERP vendors to include carbon footprint tracking and waste reduction analytics, aligning with corporate social responsibility goals and regulatory frameworks in the region.

- •Enhanced mobile ERP applications are enabling remote monitoring and management of production and distribution channels, improving responsiveness and operational agility in an increasingly digitalized market environment.

- •Collaborative platforms integrated with ERP systems are fostering ecosystem partnerships between suppliers, manufacturers, and retailers, streamlining workflows and enhancing transparency across the food and beverage value chain.

Market Opportunities

- •Expanding penetration of cloud infrastructure and increasing internet accessibility in Middle East and Africa present untapped opportunities for ERP vendors to capture emerging markets with tailored, cost-effective solutions.

- •Growing demand for personalized nutrition and functional foods creates a niche for ERP systems with advanced recipe management and batch tracking features to support innovation and compliance.

- •Strategic partnerships between ERP providers and local food industry associations can facilitate market education and adoption, accelerating digital transformation in traditionally manual operational segments.

- •Integration of blockchain technology with ERP systems offers transparency and enhanced traceability, opening new avenues for food safety assurance and consumer trust enhancement across EMEA markets.

- •Increasing government incentives for digitalization and Industry 4.0 adoption in Europe provide financial support mechanisms that ERP vendors can leverage to expand their footprint and client base.

Market Challenges

- •High initial costs and complexity of ERP system implementation present barriers for small food and beverage enterprises, especially in developing EMEA economies with limited IT infrastructure.

- •Data security and privacy concerns, intensified by regional regulations such as GDPR, impose stringent compliance requirements that complicate ERP deployment and cloud adoption strategies.

- •Fragmented market landscape with diverse regulatory environments across EMEA countries challenges vendors to develop highly customizable ERP solutions to meet localized needs effectively.

- •Resistance to change and lack of skilled personnel in traditional manufacturing settings hinder the smooth integration of ERP systems and limit technology adoption rates.

- •Interoperability issues between legacy systems and modern ERP platforms create operational inefficiencies and require significant investment in system integration and staff training.

Regulatory Framework

- •From 2019 to 2024, the European Union reinforced the Food Traceability Regulation (EU No 2017/625) mandating enhanced tracking of food products throughout the supply chain, compelling ERP systems to incorporate advanced traceability modules to ensure compliance.

- •The introduction of the General Data Protection Regulation (GDPR) in 2018 and its enforcement through 2024 has necessitated strict data handling and privacy controls within ERP platforms deployed across EMEA, influencing system architecture and vendor policies.

- •The EU's Farm to Fork Strategy, launched in 2020, emphasizes sustainability and safety, requiring ERP systems to support environmental impact tracking and reporting, aligning with regional legislative goals by 2024.

- •Middle Eastern countries, including UAE and Saudi Arabia, have updated their food safety laws between 2019 and 2024, enhancing certification and quality control requirements that ERP systems must accommodate to facilitate compliance.

- •New regulations on electronic invoicing and tax reporting across various EMEA countries introduced between 2019 and 2024 have driven the integration of financial compliance modules within ERP solutions to streamline audits and filings.

Market Intelligence

- •15th February 2025, SAP SE announced the launch of its new cloud-native Food and Beverage ERP suite tailored for EMEA manufacturers, featuring AI-driven demand forecasting and enhanced compliance management. This product aims to support digital transformation initiatives by providing real-time analytics and seamless integration with IoT devices to optimize production and supply chain operations across the region. The launch reinforces SAP's commitment to addressing sector-specific challenges and expanding its cloud ERP footprint in Europe, the Middle East, and Africa. Source: SAP Official Press Release.

- •3rd October 2024, Oracle Corporation introduced an upgraded SaaS ERP platform with advanced blockchain-enabled traceability features designed specifically for the EMEA food and beverage market. The innovation enables manufacturers and distributors to ensure transparent and secure provenance tracking, enhancing food safety adherence and consumer trust. Oracle’s strategic focus on SaaS solutions reflects the shifting demand toward scalable and flexible ERP deployments in the region’s dynamic market. Source: Oracle Corporate Announcement.

- •1st June 2025, Infor expanded its regional presence by partnering with a leading Middle Eastern food processing conglomerate to implement its CloudSuite Food & Beverage ERP solution. This strategic collaboration aims to digitize manufacturing workflows, improve quality control, and streamline supply chain management, positioning Infor as a preferred vendor in the fast-growing Middle Eastern market. The partnership highlights the vendor’s focus on tailored industry-specific ERP offerings in the EMEA region. Source: Infor Corporate News.

- •20th March 2025, Microsoft Corporation announced a strategic upgrade to its Dynamics 365 ERP platform with embedded AI capabilities for predictive maintenance and energy optimization, addressing sustainability goals in the European food and beverage industry. This enhancement supports manufacturers in reducing operational costs and carbon footprint while complying with evolving environmental regulations. The move is expected to accelerate ERP adoption among sustainability-conscious enterprises across EMEA. Source: Microsoft Newsroom.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 9.7 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Scope of Report | Market is segmented by Type (Cloud-based ERP Systems, On-premise ERP Systems, Hybrid ERP Systems, SaaS ERP Solutions, Hosted ERP Solutions), Application (Production Management, Supply Chain Management, Quality Control, Inventory Management, Sales & Distribution), End User (Food Processing Companies, Beverage Manufacturers, Packaging Firms, Distributors, Retail Chains), Deployment Model (Public Cloud, Private Cloud, On-premise, Hybrid Cloud) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | SAP SE (Germany), Oracle Corporation (United States), Infor (United States), Microsoft Corporation (United States), IFS AB (Sweden), Sage Group plc (United Kingdom), Epicor Software Corporation (United States), Plex Systems (United States), Unit4 (Netherlands), IFS (Sweden), Workday, Inc. (United States), QAD Inc. (United States), SYSPRO (South Africa), Ramco Systems (India), Oracle NetSuite (United States), Deltek, Inc. (United States), Exact (Netherlands), Priority Software (Israel), abas ERP (Germany), IFS Food & Beverage Solutions (Sweden), ProAlpha Group (Germany), Microsoft Dynamics 365 (United States), SAP Business One (Germany), Oracle JD Edwards (United States), Infor CloudSuite Food & Beverage (United States) |

EMEA Food and Beverage ERP Systems Market Scope & Changing Dynamics 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.