EMEA Pet and Human Furniture Market - Europe Size & Outlook 2020-2034

EMEA Pet and Human Furniture Market is segmented by Furniture Type (Wooden Furniture, Metal Furniture, Upholstered Furniture, Plastic Furniture, Composite Furniture), Application Area (Residential, Commercial, Hospitality, Outdoor, Healthcare), Service Category (Customization Services, Delivery and Installation, Maintenance and Repair, Rental Services), Distribution Channel (Offline Retail, E-commerce, Direct Sales), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA Pet and Human Furniture market integrates furniture solutions designed specifically for pets and humans, spanning applications such as residential homes, commercial offices, hospitality venues, outdoor environments, and healthcare institutions. Covering product types like wooden, metal, upholstered, plastic, and composite furniture, the market addresses functionality, aesthetics, and comfort across diverse consumer segments. The value chain involves raw material procurement, design innovation, manufacturing, distribution, and retailing, supported by after-sales services. Increasing pet ownership, lifestyle shifts toward ergonomic and multifunctional furniture, and rising disposable incomes in EMEA countries drive market expansion. Urbanization and sustainability trends encourage adoption of eco-friendly materials and smart furniture designs. The market serves a broad end-user base including homeowners, pet owners, corporate clients, hospitality operators, and healthcare providers. Technological advancements enable customization and integration of smart features, enhancing user experience. The market's growth is also propelled by heightened consumer awareness of pet welfare and human comfort, making it a strategic focus for manufacturers and retailers in the region.

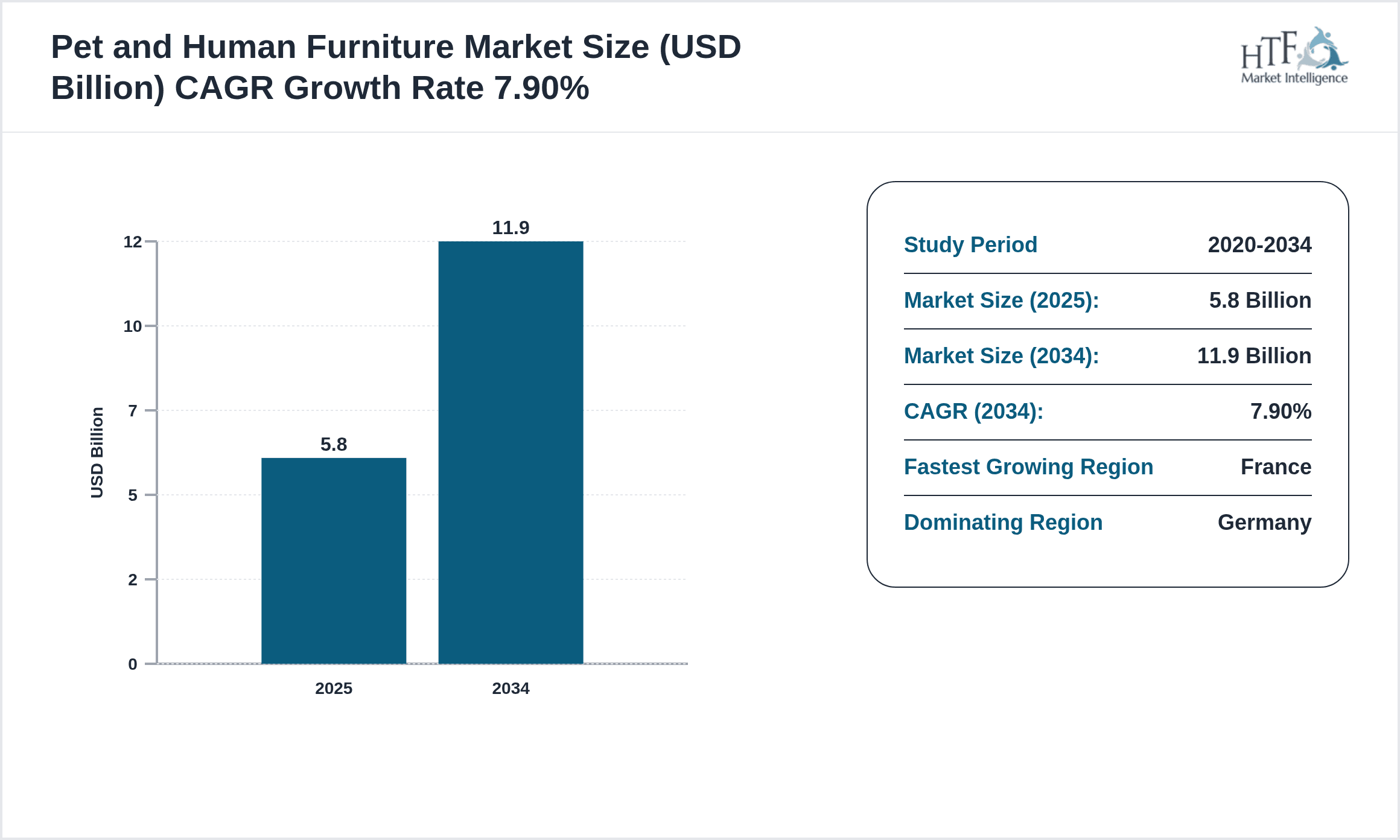

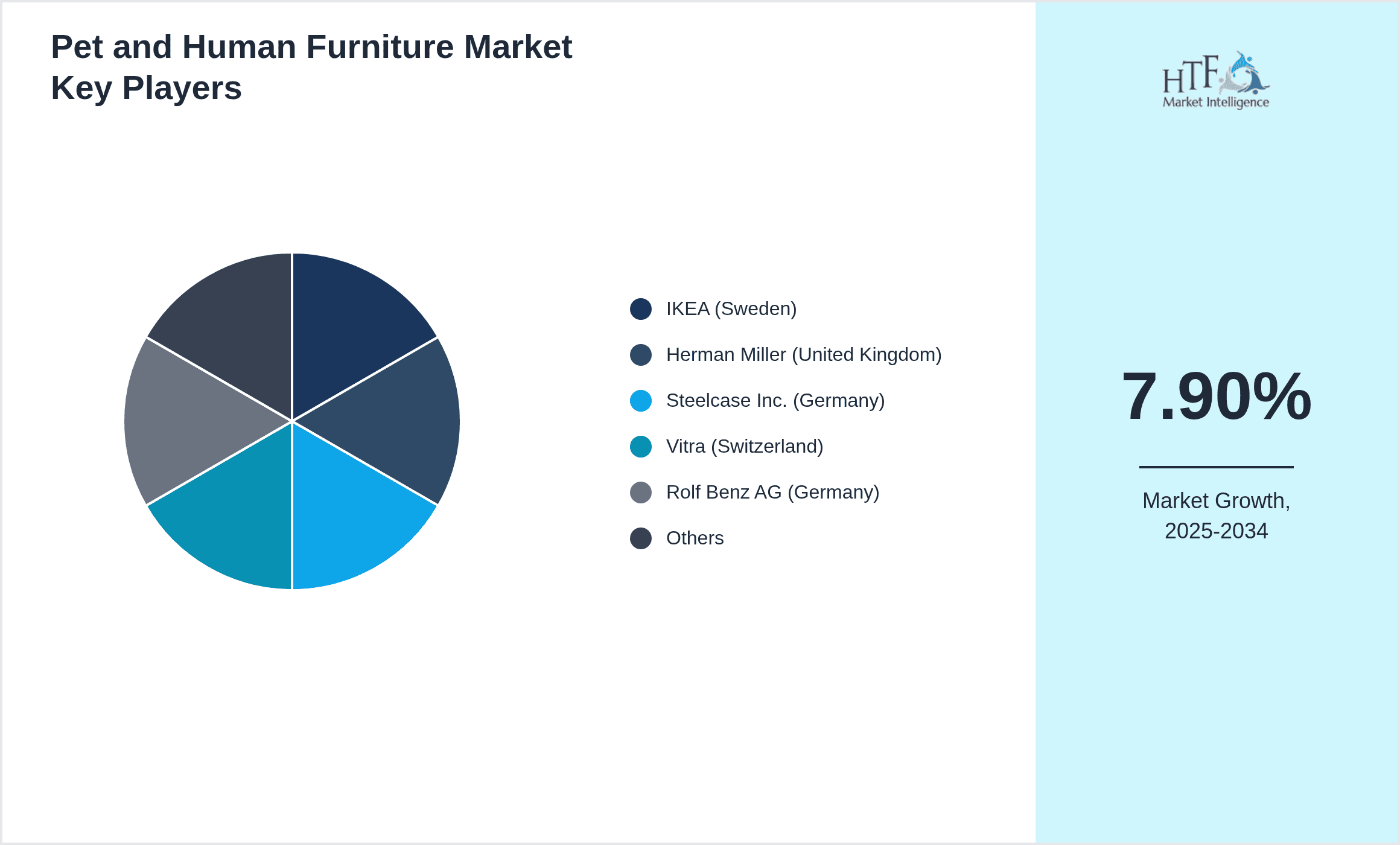

- •Key market highlights indicate a steady CAGR of approximately 7.9% from 2025 to 2034, with the market size expected to more than double from USD 5.8 billion in 2025 to USD 11.9 billion by 2034. Germany dominates the market with a 32% share, driven by its strong manufacturing base and consumer demand, while France is the fastest-growing country with a CAGR of 9.1% attributed to increasing pet adoption and premium furniture consumption. Upholstered furniture is the fastest-growing product type, reflecting consumer preference for comfort and style. Market dynamics are influenced by evolving design trends, sustainability initiatives, and digital transformation in retail channels.

- •The market offers significant value propositions through innovation in multi-use furniture, integration of pet-friendly designs in human furniture, and premiumization across segments. Strategic importance lies in catering to rising pet ownership and human lifestyle changes, enabling manufacturers to leverage cross-segment synergies. Stakeholders including designers, manufacturers, retailers, and end-users benefit from enhanced product offerings, expanding distribution networks, and growing consumer demand for customized and sustainable furniture solutions in EMEA.

Competitive Landscape

The EMEA Pet and Human Furniture market is characterized by intense competition among established multinational corporations, specialized niche manufacturers, and emerging regional players. Market dynamics revolve around continuous product innovation, with companies investing in ergonomic designs, sustainable materials, and integration of smart technologies to differentiate their offerings. Competitive strategies include strategic partnerships with pet product brands, expansion of retail footprints through both offline and e-commerce channels, and customization services catering to diverse consumer preferences. Pricing strategies vary from premium to value-based models, targeting distinct consumer segments. Mergers and acquisitions have played a crucial role in consolidating market share, enabling firms to expand product portfolios and geographic reach. Regional competition is notably active in Western Europe, with Germany, France, and the United Kingdom being key battlegrounds. Companies also focus on enhancing supply chain efficiencies and sustainability credentials to meet regulatory standards and consumer expectations. Looking forward, digital transformation, sustainability demands, and changing consumer behaviors will shape competitive advantages and market entry barriers, driving innovation and collaboration across the ecosystem.

Leading Companies in Pet and Human Furniture Market

- •IKEA (Sweden)

- •Herman Miller (United Kingdom)

- •Steelcase Inc. (Germany)

- •Vitra (Switzerland)

- •Rolf Benz AG (Germany)

- •Natuzzi S.p.A. (Italy)

- •Flexform S.p.A. (Italy)

- •Ligne Roset (France)

- •BoConcept (Denmark)

- •Muuto (Denmark)

- •Fermob (France)

- •Kartell (Italy)

- •Bolia A/S (Denmark)

- •Walter Knoll (Germany)

- •Houe A/S (Denmark)

- •Moroso (Italy)

- •PetFusion (United Kingdom)

- •K&H Manufacturing Co., Inc. (Germany)

- •Hunter (Germany)

- •Trixie Heimtierbedarf GmbH & Co. KG (Germany)

- •Livetastic GmbH (Germany)

- •Petmate Europe (United Kingdom)

- •Barkley & Wagz (France)

- •Scruffs (United Kingdom)

- •Rosewood Pet Products (United Kingdom)

Market Breakdown

- •By Furniture Type

- ◦Wooden Furniture

- ◦Metal Furniture

- ◦Upholstered Furniture

- ◦Plastic Furniture

- ◦Composite Furniture

- •By Application Area

- ◦Residential

- ◦Commercial

- ◦Hospitality

- ◦Outdoor

- ◦Healthcare

- •By Service Category

- ◦Customization Services

- ◦Delivery and Installation

- ◦Maintenance and Repair

- ◦Rental Services

- •By Distribution Channel

- ◦Offline Retail

- ◦E-commerce

- ◦Direct Sales

Growth Dynamics

- •Increasing pet ownership across EMEA, particularly in urban centers, is driving demand for specialized pet furniture that complements human living spaces, enhancing market growth by aligning with lifestyle changes and pet humanization trends.

- •Rising disposable incomes and consumer preference for premium, ergonomic, and multifunctional furniture solutions in both pet and human segments are pushing manufacturers to innovate and diversify product portfolios.

- •Sustainability concerns and government regulations promoting eco-friendly materials have accelerated the adoption of sustainable furniture production practices, influencing market growth positively in the EMEA region.

- •Digital transformation in retail, including enhanced e-commerce platforms and augmented reality tools for furniture visualization, is improving customer engagement and expanding market reach across diverse demographics.

- •Collaborations between furniture manufacturers and pet product companies are fostering innovative designs that blend aesthetics and functionality, creating new market niches and enhancing consumer appeal.

- •Investment in R&D for smart furniture incorporating IoT features for pet monitoring and human comfort is emerging as a key growth driver, offering differentiated products in a competitive landscape.

- •Urbanization and shrinking living spaces are encouraging development of space-saving, modular furniture solutions suitable for both pets and humans, expanding market opportunities in densely populated EMEA cities.

Market Trends

- •The integration of pet-friendly features in human furniture, such as built-in pet beds and scratch-resistant materials, is a growing trend addressing the cohabitation needs of pet owners in EMEA.

- •Sustainable and recycled materials have gained prominence in furniture manufacturing, with consumers increasingly favoring environmentally responsible products reflecting broader ecological awareness.

- •Customization and personalization services are expanding rapidly, allowing consumers to tailor furniture design, color, and functionality to specific pet and human lifestyle requirements.

- •The rise of omnichannel retail strategies combining physical stores and online platforms is reshaping the customer purchase journey and enhancing accessibility across the EMEA region.

- •Premiumization of pet furniture with luxury designs and high-quality materials is attracting affluent consumers, driving growth in the upscale segment of the market.

- •Smart furniture equipped with sensors and connectivity features for pet activity monitoring and human health tracking is gaining traction among tech-savvy consumers.

- •Collaborative design initiatives involving pet behaviorists and furniture designers are emerging to create ergonomically optimized products that enhance pet wellbeing and owner satisfaction.

Market Opportunities

- •Expanding pet ownership in emerging EMEA markets such as Eastern Europe and the Middle East offers untapped growth potential for pet-specific furniture products tailored to local preferences.

- •Development of modular and space-efficient furniture solutions addressing urban living constraints presents significant opportunities for innovative product launches.

- •Leveraging e-commerce growth through enhanced digital marketing and virtual showrooms can increase market penetration and brand visibility across diverse EMEA demographics.

- •Collaborations with hospitality and healthcare sectors to provide specialized furniture catering to pets and patients open new B2B market segments with high-value contracts.

- •Investment in smart furniture integrating IoT and AI technologies offers avenues for product differentiation and premium pricing strategies.

- •Adoption of sustainable and recyclable materials aligned with evolving regulatory frameworks can enhance brand reputation and meet consumer demand for eco-friendly products.

- •Customization services tailored to individual pet and human needs create opportunities to build customer loyalty and increase repeat purchases.

Market Challenges

- •High production costs associated with sustainable and high-quality materials pose challenges to competitive pricing and profitability for manufacturers in the EMEA region.

- •Fragmented market with numerous small and medium players creates intense competition, complicating brand differentiation and market share retention.

- •Complex regulatory compliance across different EMEA countries, particularly regarding safety and environmental standards, increases operational overheads and time to market.

- •Supply chain disruptions, including raw material shortages and logistical challenges, affect timely production and delivery schedules, impacting customer satisfaction.

- •Consumer price sensitivity in certain EMEA markets limits adoption of premium and smart furniture products, constraining market growth potential.

- •Rapidly changing design trends demand continuous product innovation, requiring significant investment in research and development.

- •Limited awareness of pet-specific furniture benefits in emerging markets necessitates extensive consumer education and marketing efforts.

Regulatory Framework

- •The EU Timber Regulation (EUTR), effective since 2013 and reinforced through 2020-2025, mandates sustainable sourcing of wood used in furniture manufacturing, significantly impacting production practices in EMEA furniture markets.

- •REACH (Registration, Evaluation, Authorisation, and Restriction of Chemicals) regulation requires strict control of hazardous substances in furniture products, enforced rigorously between 2020 and 2025 to ensure consumer safety.

- •The EU Ecodesign Directive promotes energy efficiency and environmental sustainability in product manufacturing, influencing materials and processes used in furniture production across the EMEA region.

- •Country-specific fire safety standards and certification requirements for upholstered furniture, particularly in Germany, France, and the UK, mandate compliance that affects design and material selection.

- •Government initiatives encouraging circular economy models and recycling practices in furniture manufacturing have gained momentum from 2020 to 2025, fostering innovation in sustainable product lines.

Market Intelligence

- •12th February 2025, IKEA announced the launch of a new eco-friendly pet and human furniture collection designed with 100% recycled materials and modular components for easy customization. Targeting environmentally conscious consumers across Europe, the collection integrates smart features for enhanced comfort and pet safety, aiming to capture the growing demand for sustainable and multifunctional furniture in urban homes. This strategic initiative strengthens IKEA's leadership in the EMEA market by aligning with evolving regulatory frameworks and consumer preferences. Source: IKEA Official Press Release

- •7th April 2025, Herman Miller unveiled its new upholstered furniture line incorporating antimicrobial fabrics and built-in pet-friendly zones, catering to commercial and residential sectors in EMEA. The product addresses post-pandemic hygiene concerns and pet humanization trends, positioning the company to capitalize on emerging market segments. The launch includes an augmented reality app to facilitate virtual product trials, enhancing customer engagement and online sales. Source: Herman Miller Corporate Website

- •15th May 2025, Flexform S.p.A. announced a strategic partnership with PetFusion UK to co-develop premium pet furniture integrated with luxury human furniture lines. This collaboration aims to expand distribution channels across EMEA, leveraging Flexform’s design expertise and PetFusion’s pet product innovations. The partnership is expected to drive revenue growth and tap into the premium market segment with customized, multifunctional solutions. Source: Industry Publication - Furniture Today Europe

- •20th June 2025, Steelcase Inc. completed the acquisition of Houe A/S, a Danish furniture manufacturer specializing in outdoor and modular furniture, to strengthen its portfolio in the EMEA region. The acquisition supports Steelcase's expansion into outdoor residential and commercial furniture markets, integrating sustainable materials and smart design technologies. The deal enhances Steelcase's competitive positioning and broadens its regional footprint, responding to growing demand for adaptable and eco-friendly furniture solutions. Source: Financial Times

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 5.8 Billion |

| Forecast Year Market Size | USD 11.9 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Furniture Type (Wooden Furniture, Metal Furniture, Upholstered Furniture, Plastic Furniture, Composite Furniture), Application Area (Residential, Commercial, Hospitality, Outdoor, Healthcare), Service Category (Customization Services, Delivery and Installation, Maintenance and Repair, Rental Services), Distribution Channel (Offline Retail, E-commerce, Direct Sales) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | IKEA (Sweden), Herman Miller (United Kingdom), Steelcase Inc. (Germany), Vitra (Switzerland), Rolf Benz AG (Germany) |

EMEA Pet and Human Furniture Market - Europe Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.