United States Industrial Kilns for Ceramics and Advanced Materials Market Size, Growth & Revenue 2025-2034

United States Industrial Kilns for Ceramics and Advanced Materials Market is segmented by Kiln Type (Tunnel Kilns, Roller Hearth Kilns, Shuttle Kilns, Vacuum Kilns, Rotary Kilns), Application Segment (Ceramic Manufacturing, Advanced Materials Production, Refractory Processing, Electronics Components, Aerospace Components), Service Type (Installation & Commissioning, Maintenance & Repair, Upgrades & Retrofits, Consulting & Training), Deployment Model (On-premise Kiln Systems, Custom Engineered Solutions, Modular Kiln Systems), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States Industrial Kilns for Ceramics and Advanced Materials market involves the production and application of specialized kiln equipment designed to meet the thermal processing needs of ceramics and advanced materials manufacturing. These kilns facilitate critical processes such as firing, sintering, and heat treatment for diverse applications including ceramic manufacturing, refractory materials, electronics, aerospace, and specialty components. The market encompasses various kiln types such as tunnel kilns, roller hearth kilns, shuttle kilns, vacuum kilns, and rotary kilns, each optimized for specific material properties and production volumes. Key end-users include ceramic producers, advanced material manufacturers, aerospace component fabricators, and electronics companies requiring precise thermal control. The value chain integrates raw material suppliers, kiln manufacturers, technology providers, system integrators, and end-users, with a growing focus on energy efficiency and automation to enhance productivity and reduce environmental impact. The market has seen steady growth driven by advances in kiln technology, rising demand for high-performance ceramics and materials, and the expanding aerospace and electronics industries. Regional dynamics indicate the West Coast as the dominating region due to its concentration of advanced materials and aerospace manufacturing, while the Southeast shows the fastest growth fueled by increased industrial investments and infrastructure development. The forecast period through 2034 anticipates robust CAGR supported by innovation, regulatory compliance, and growing industrial applications.

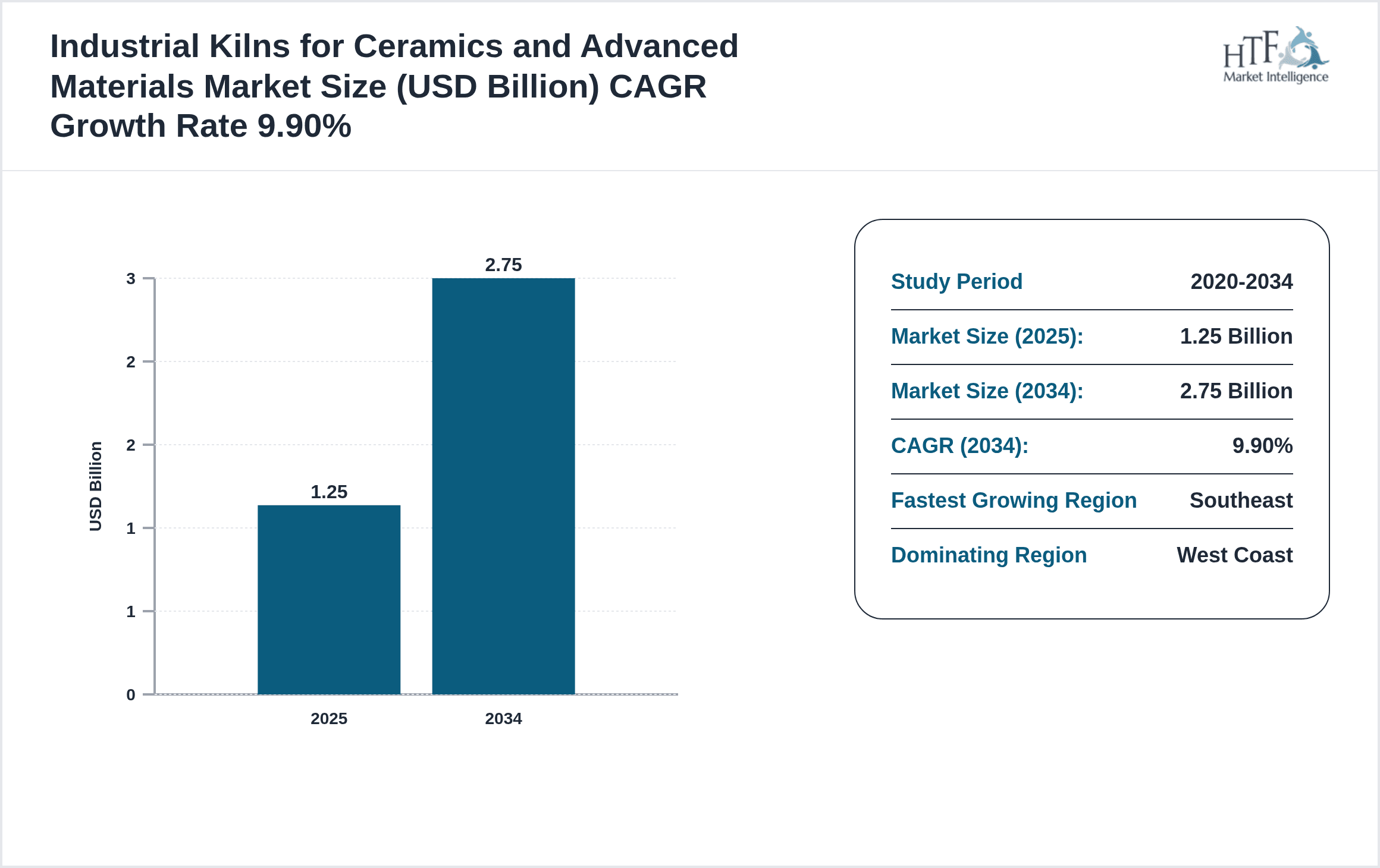

- •Key market highlights include a base market size of USD 1.25 Billion in 2025 and a projected growth to USD 2.75 Billion by 2034, representing a compound annual growth rate (CAGR) of 9.9%. Year-on-year growth is estimated at 9.5%, reflecting strong demand across ceramic and advanced materials sectors. Tunnel kilns remain the leading product type, favored for their energy efficiency and continuous operation, while vacuum kilns exhibit the fastest growth due to their suitability for high-precision advanced materials processing. The West Coast dominates market share with 30%, driven by established aerospace and electronics manufacturing hubs, while the Southeast region leads in growth momentum with a 12.5% CAGR. Market drivers include technological innovation, increased industrial automation, and expanding aerospace manufacturing. Challenges such as high capital investment and regulatory compliance persist but are counterbalanced by opportunities in emerging applications and energy-efficient kiln technologies.

- •The value proposition of the United States Industrial Kilns market lies in its critical role in enabling advanced manufacturing capabilities for ceramics and high-performance materials essential to various industries including aerospace, electronics, and specialty manufacturing. Strategic importance is underscored by the need for precision thermal processing to enhance product quality, performance, and energy efficiency. Stakeholders including kiln manufacturers, industrial end-users, and technology developers benefit from market growth driven by innovation, demand for sustainability, and evolving industrial requirements. The market also presents investment opportunities in advanced kiln technologies and automation solutions that reduce operational costs and carbon footprint, positioning the sector as a vital enabler of United States manufacturing competitiveness.

Competitive Landscape

The competitive environment for industrial kilns in the United States is characterized by a combination of established global manufacturers and specialized regional producers focusing on innovation, product differentiation, and customer-centric solutions. Market dynamics include intense competition on technological advancement, particularly in energy efficiency, automation, and process control capabilities. Leading companies leverage strategic partnerships, mergers and acquisitions, and R&D investments to expand their product portfolios and geographic reach. Pricing strategies are balanced with quality and technology offerings to maintain market share in a capital-intensive industry. Distribution channels encompass direct sales, OEM partnerships, and service agreements, enhancing customer retention. Competitive advantages are often derived from proprietary kiln designs, customization capabilities, and comprehensive after-sales support. Barriers to entry are significant due to high capital requirements and technical expertise, which favor established players. Regional competition focuses on meeting localized industry demands, with the West Coast and Southeast regions being critical competitive battlegrounds. Future trends indicate increased adoption of digitalization and IoT integration for predictive maintenance and process optimization, intensifying innovation-driven competition.

Key Participants in Industrial Kilns for Ceramics and Advanced Materials Market

- •Nabertherm GmbH (Germany)

- •L&L Special Furnace Co. Inc. (United States)

- •Thermcraft Inc. (United States)

- •CM Furnaces, Inc. (United States)

- •Carbolite Gero Ltd. (United Kingdom)

- •Ipsen USA (United States)

- •Miller Furnace Company, Inc. (United States)

- •Aichelin Group (Austria)

- •Despatch Industries (United States)

- •Carpco, Inc. (United States)

- •Harper International Corporation (United States)

- •Neytech, LLC (United States)

- •Koyo Thermo Systems Co., Ltd. (Japan)

- •Restar Group (Japan)

- •Lenton Furnaces (United Kingdom)

- •Heraeus Holding GmbH (Germany)

- •FCT Furnaces, Inc. (United States)

- •Furnace Engineering, Inc. (United States)

- •Thermcraft Europe (United Kingdom)

- •MTI Corporation (United States)

- •Heraeus Noblelight America LLC (United States)

- •Carbolite Gero Inc. (United States)

- •Nabertherm Inc. (United States)

- •L&L Special Furnace Co. (Canada)

- •Thermcraft Asia (China)

Market Breakdown

- •By Kiln Type

- ◦Tunnel Kilns

- ◦Roller Hearth Kilns

- ◦Shuttle Kilns

- ◦Vacuum Kilns

- ◦Rotary Kilns

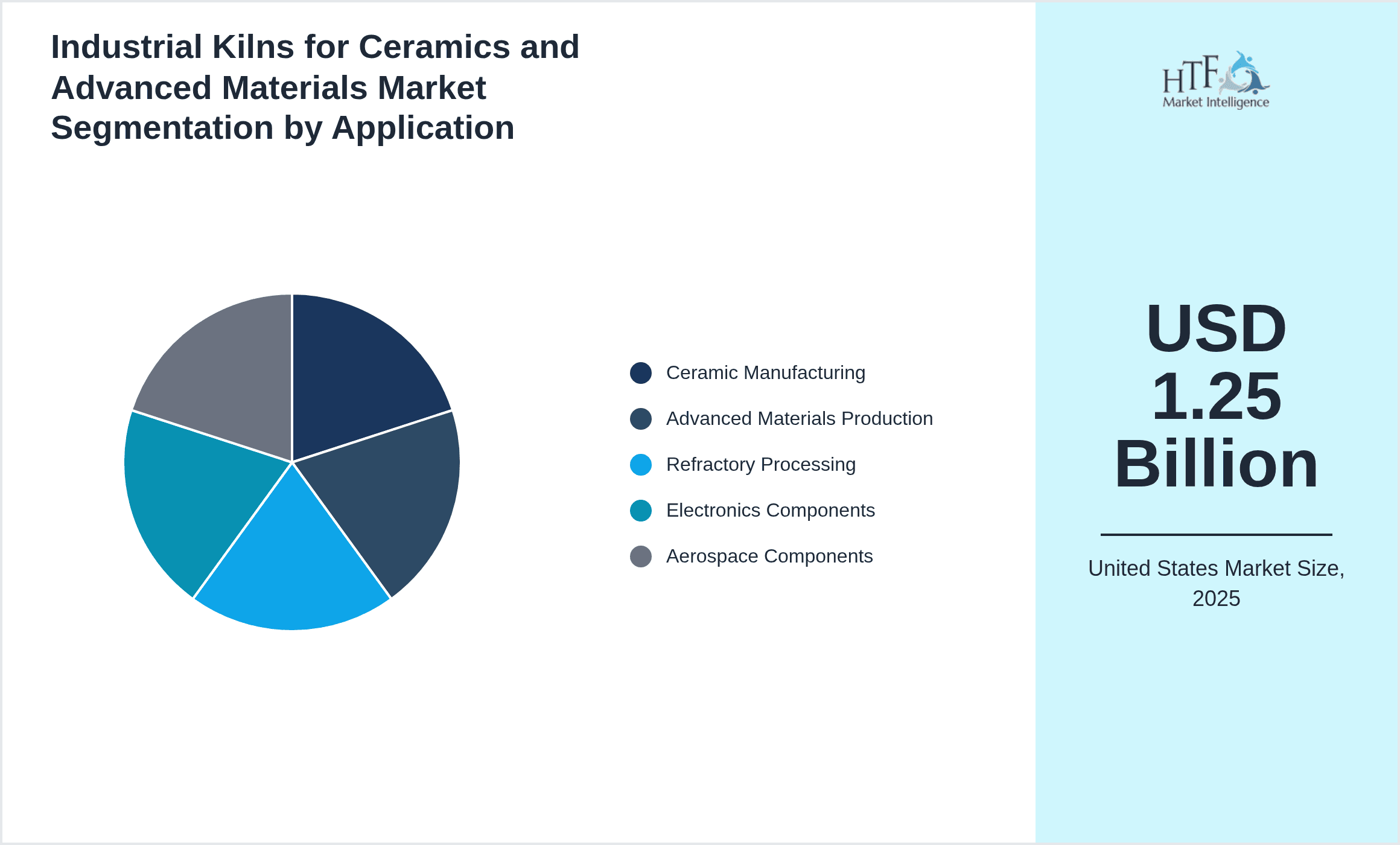

- •By Application Segment

- ◦Ceramic Manufacturing

- ◦Advanced Materials Production

- ◦Refractory Processing

- ◦Electronics Components

- ◦Aerospace Components

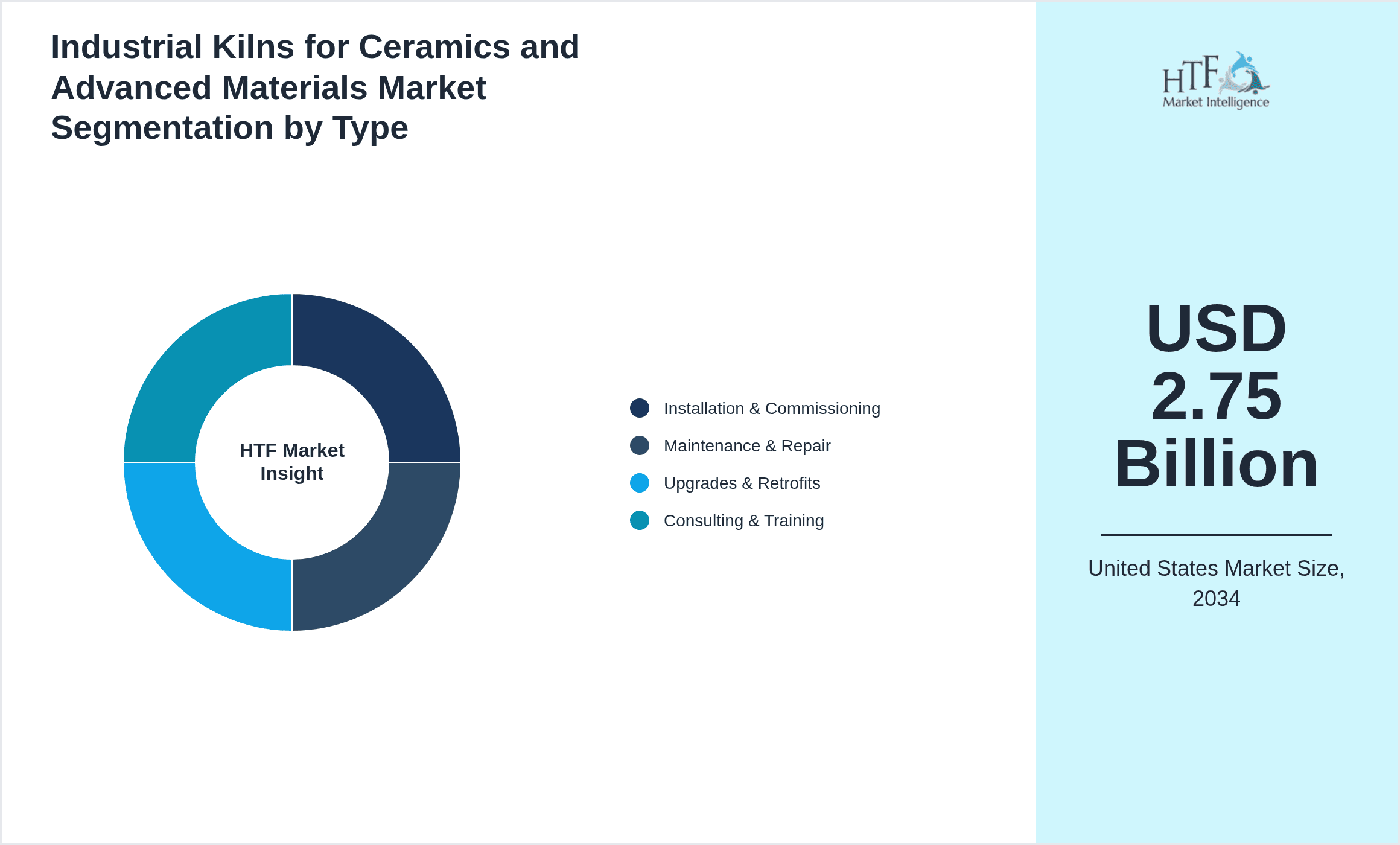

- •By Service Type

- ◦Installation & Commissioning

- ◦Maintenance & Repair

- ◦Upgrades & Retrofits

- ◦Consulting & Training

- •By Deployment Model

- ◦On-premise Kiln Systems

- ◦Custom Engineered Solutions

- ◦Modular Kiln Systems

Growth Dynamics

- •Rising demand for high-performance ceramics and advanced materials in aerospace and electronics sectors is propelling the adoption of industrial kilns with precise thermal capabilities, facilitating market growth through 2034.

- •Technological advancements in kiln automation and energy efficiency, including integration of IoT and advanced control systems, are enhancing operational productivity and reducing energy consumption, driving market expansion.

- •Government initiatives promoting energy-efficient manufacturing processes and environmental sustainability are encouraging investments in modern kiln technologies, supporting industry-wide adoption and growth.

- •Increasing industrialization and infrastructure development in the Southeastern United States is creating new demand centers for industrial kilns, contributing to the region's status as the fastest-growing market segment.

- •Rising adoption of advanced materials requiring specialized firing environments, such as vacuum kilns for electronics and aerospace components, is driving the diversification of kiln product offerings and fueling market growth.

- •Strategic collaborations and R&D investments by kiln manufacturers to develop customized solutions for specific industrial applications are positioning the market for sustained growth and technological leadership.

- •The expanding ceramic manufacturing sector for industrial and consumer applications continues to require reliable, high-capacity kiln systems, underpinning steady demand and capacity expansions nationwide.

Market Trends

- •Adoption of smart kiln technologies with real-time monitoring and predictive maintenance capabilities is transforming operational efficiency, reducing downtime, and enhancing product quality across ceramics and advanced materials manufacturing.

- •Shift towards environmentally sustainable kiln operations driven by regulatory pressure and corporate responsibility is encouraging the development of low-emission and energy-saving kiln designs.

- •Increased use of vacuum and controlled atmosphere kilns is enabling the production of high-purity advanced materials, expanding application scopes in electronics and aerospace industries.

- •Modular and customizable kiln systems are gaining popularity due to their flexibility, scalability, and reduced installation times, catering to diverse production requirements in small and medium enterprises.

- •Integration of digital twins and simulation software in kiln design and operation is improving process optimization and reducing trial-and-error in manufacturing setups.

- •Collaborations between kiln manufacturers and material producers are fostering innovation in kiln processes tailored to new material formulations, accelerating adoption of next-generation ceramics.

- •Rising investments in automation and robotics in kiln handling systems are enhancing safety and throughput, reflecting a broader trend toward Industry 4.0 in manufacturing facilities.

Market Opportunities

- •Expansion of advanced material manufacturing for aerospace and electronics presents opportunities for customized vacuum and roller hearth kilns designed for precision and contamination control.

- •Growing ceramic tile and sanitary ware manufacturing industries in emerging U.S. regions offer potential for deploying energy-efficient tunnel and shuttle kilns to reduce operational costs.

- •Rising interest in sustainable manufacturing provides a fertile ground for innovation in low-emission kiln technologies and retrofitting existing installations to meet new environmental standards.

- •Development of modular kiln systems for small and medium enterprises enables market penetration into previously underserved segments requiring flexible production capabilities.

- •Strategic partnerships with OEMs and material technology firms can foster co-development of kiln solutions, enhancing product quality and opening new application markets.

- •Investment in digitalization and IoT-enabled kiln management systems offers opportunities to enhance operational transparency and predictive maintenance services as value-added offerings.

- •Infrastructure growth and industrial diversification in the Southeast United States create fertile grounds for kiln market expansion targeting new manufacturing hubs.

Market Challenges

- •High initial capital investment and long payback periods for advanced kiln systems remain significant barriers to adoption, particularly among small manufacturers.

- •Stringent environmental and safety regulations require continuous compliance efforts and technology upgrades, increasing operational complexity and costs.

- •Limited availability of skilled technical personnel to operate and maintain sophisticated kiln systems restricts market growth and operational efficiency.

- •Competition from imported kiln equipment with lower cost structures poses challenges for domestic manufacturers to maintain pricing power and market share.

- •Rapid technological changes necessitate frequent product updates, creating challenges in inventory management and customer education.

- •Supply chain disruptions affecting critical kiln components and raw materials have led to delays and increased costs, impacting project timelines.

- •Integration of new technologies such as IoT and automation requires significant upfront investments and change management, which some end-users are hesitant to undertake.

Regulatory Framework

- •The Clean Air Act amendments between 2020 and 2025 have imposed stricter emission controls on industrial kilns, requiring manufacturers to adopt low-NOx burners and advanced filtration systems to comply with EPA standards.

- •Occupational Safety and Health Administration (OSHA) regulations updated in 2023 mandate enhanced worker safety protocols and kiln operation training, influencing market adoption of automated and remote-controlled kiln systems.

- •State-level energy efficiency mandates, particularly in California and the Northeast, have driven investments in energy-saving kiln technologies and retrofitting initiatives during the 2020–2025 period.

- •The Resource Conservation and Recovery Act (RCRA) regulations enforced stricter waste management and disposal practices for kiln byproducts, impacting manufacturing processes and equipment design.

- •Federal incentives and tax credits introduced in 2024 for clean manufacturing technologies have encouraged investments in energy-efficient kiln systems, supporting market growth and modernization efforts.

Market Intelligence

- •15th January 2025, L&L Special Furnace Co. Inc. launched an advanced modular vacuum kiln system designed for high-precision ceramic and advanced material production. The new kiln features enhanced thermal uniformity, reduced energy consumption by 15%, and integrated IoT-enabled monitoring for real-time process optimization. Targeting aerospace and electronics manufacturers, this system aims to improve product quality and reduce operational costs. The launch underscores L&L’s commitment to innovation and sustainability in the United States industrial kiln market. Source: Official L&L Special Furnace Co. Press Release.

- •20th March 2025, Ipsen USA introduced a state-of-the-art roller hearth kiln incorporating AI-driven control systems for adaptive thermal processing. This innovation allows dynamic adjustment of firing cycles based on material characteristics, enhancing throughput by 20% and reducing waste. Positioned to serve the growing advanced materials sector, Ipsen’s kiln supports energy efficiency goals and regulatory compliance. The product launch reflects a broader industry trend towards automation and smart manufacturing. Source: Ipsen USA Corporate Announcement.

- •5th June 2025, Thermcraft Inc. announced a strategic partnership with a leading aerospace materials developer to co-design custom vacuum kiln solutions tailored for next-generation composite materials. This collaboration focuses on enhancing thermal precision and process repeatability to meet stringent aerospace industry standards. The initiative is expected to accelerate market adoption of advanced kiln technologies in high-growth sectors, reinforcing Thermcraft’s competitive positioning. Source: Thermcraft Inc. Press Release.

- •10th September 2024, Nabertherm GmbH completed the acquisition of a US-based kiln service provider, expanding its service footprint in the United States. The acquisition strengthens Nabertherm’s after-sales service capabilities, including maintenance, repair, and retrofitting, supporting customer retention and operational efficiency. This move reflects consolidation trends within the industrial kiln market aimed at enhancing comprehensive customer solutions. Source: Nabertherm Official Website.

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 2.75 Billion |

| CAGR | 9.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.5% |

| Scope of Report | Market is segmented by Kiln Type (Tunnel Kilns, Roller Hearth Kilns, Shuttle Kilns, Vacuum Kilns, Rotary Kilns), Application Segment (Ceramic Manufacturing, Advanced Materials Production, Refractory Processing, Electronics Components, Aerospace Components), Service Type (Installation & Commissioning, Maintenance & Repair, Upgrades & Retrofits, Consulting & Training), Deployment Model (On-premise Kiln Systems, Custom Engineered Solutions, Modular Kiln Systems) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | Expansion of advanced material manufacturing for aerospace and electronics presents opportunities for customized vacuum and roller hearth kilns designed for precision and contamination control., Growing ceramic tile and sanitary ware manufacturing industries in emerging U.S. regions offer potential for deploying energy-efficient tunnel and shuttle kilns to reduce operational costs., Rising interest in sustainable manufacturing provides a fertile ground for innovation in low-emission kiln technologies and retrofitting existing installations to meet new environmental standards., Development of modular kiln systems for small and medium enterprises enables market penetration into previously underserved segments requiring flexible production capabilities., Strategic partnerships with OEMs and material technology firms can foster co-development of kiln solutions, enhancing product quality and opening new application markets., Investment in digitalization and IoT-enabled kiln management systems offers opportunities to enhance operational transparency and predictive maintenance services as value-added offerings., Infrastructure growth and industrial diversification in the Southeast United States create fertile grounds for kiln market expansion targeting new manufacturing hubs. |

United States Industrial Kilns for Ceramics and Advanced Materials Market Size, Growth & Revenue 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.