GCC Rotary Indexing Assembly Machine Market - Middle East Size & Outlook 2020-2034

GCC Rotary Indexing Assembly Machine Market is segmented by Rotary Indexing Assembly Machine Type (Mechanical Rotary Indexing Assembly Machines, Pneumatic Rotary Indexing Assembly Machines, Servo Motor Driven Rotary Indexing Machines, Hydraulic Rotary Indexing Assembly Machines, Electric Rotary Indexing Assembly Machines), Application in Manufacturing (Automotive Component Assembly, Electronics Manufacturing Assembly, Medical Device Assembly, Consumer Goods Assembly, Industrial Machinery Assembly), Service Type (Installation and Commissioning Services, Maintenance and Repair Services, Upgrades and Retrofits, After-Sales Technical Support), Deployment Model (On-Premise Deployment, Cloud-Enabled Monitoring Integration, Hybrid Automated Assembly Systems), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

- •The GCC Rotary Indexing Assembly Machine market comprises advanced automated machinery designed to enhance assembly line efficiency through precise rotational indexing technology. These machines are pivotal in manufacturing sectors such as automotive, electronics, medical devices, consumer goods, and industrial machinery, providing high-speed, accurate component assembly. The market covers equipment utilizing diverse technologies including mechanical, pneumatic, servo motor driven, hydraulic, and electric rotary indexing systems. Their use significantly reduces manual labor, optimizes production cycles, and ensures consistent product quality. The GCC region, encompassing Saudi Arabia, United Arab Emirates, Qatar, Kuwait, and Oman, is witnessing rising industrialization and automation adoption, fueling demand for rotary indexing assembly machines. The value chain extends from component suppliers to machine manufacturers and system integrators, culminating in end-users across various manufacturing verticals. Increasing investments in smart factories, government initiatives promoting industrial diversification, and growing demand for efficient production lines underpin market growth. Challenges include high capital expenditure, technical complexity, and the need for skilled operators. Nevertheless, advancements in electric rotary indexing technologies and integration with Industry 4.0 solutions are creating new growth avenues, positioning the GCC market for robust expansion through 2034.

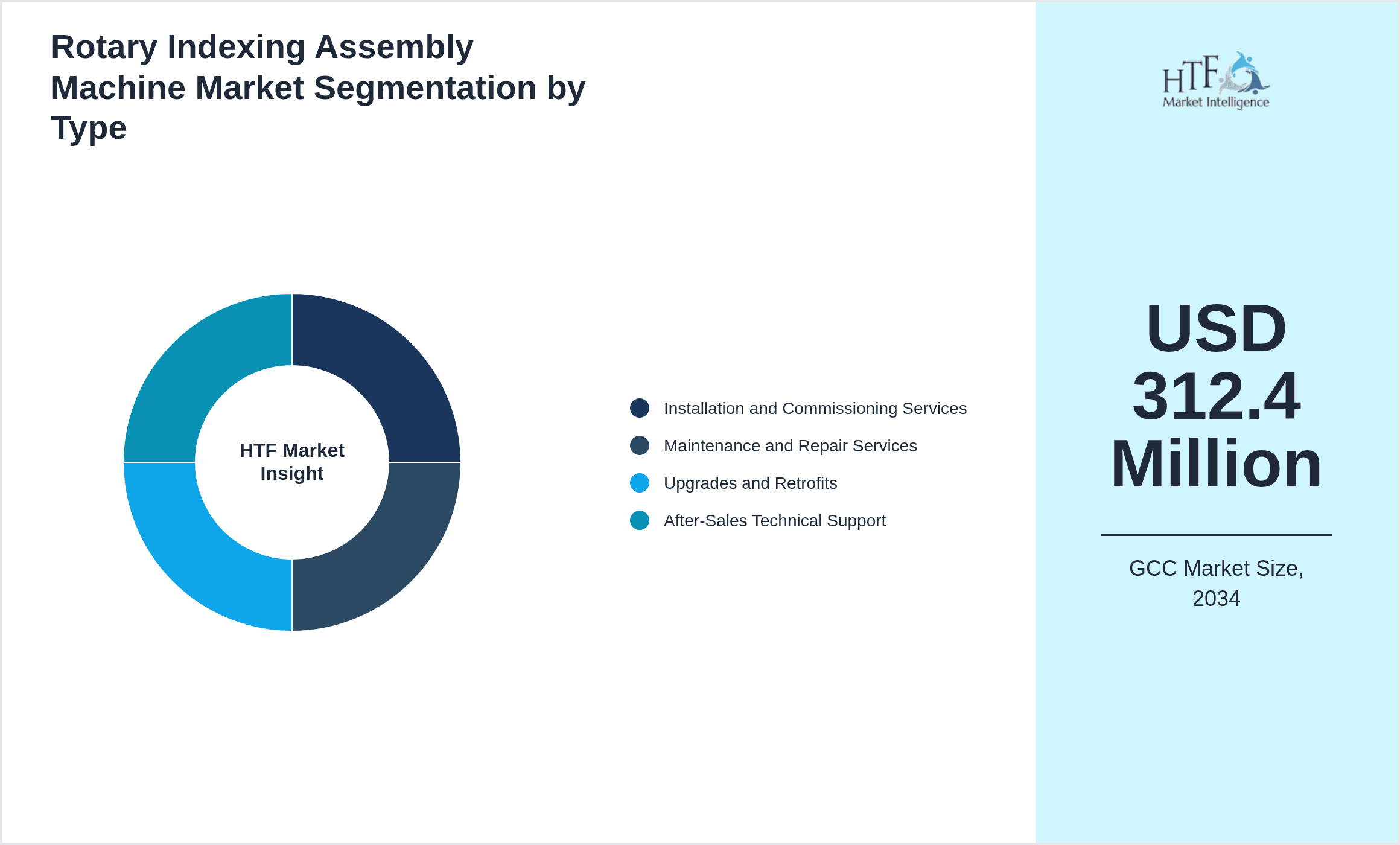

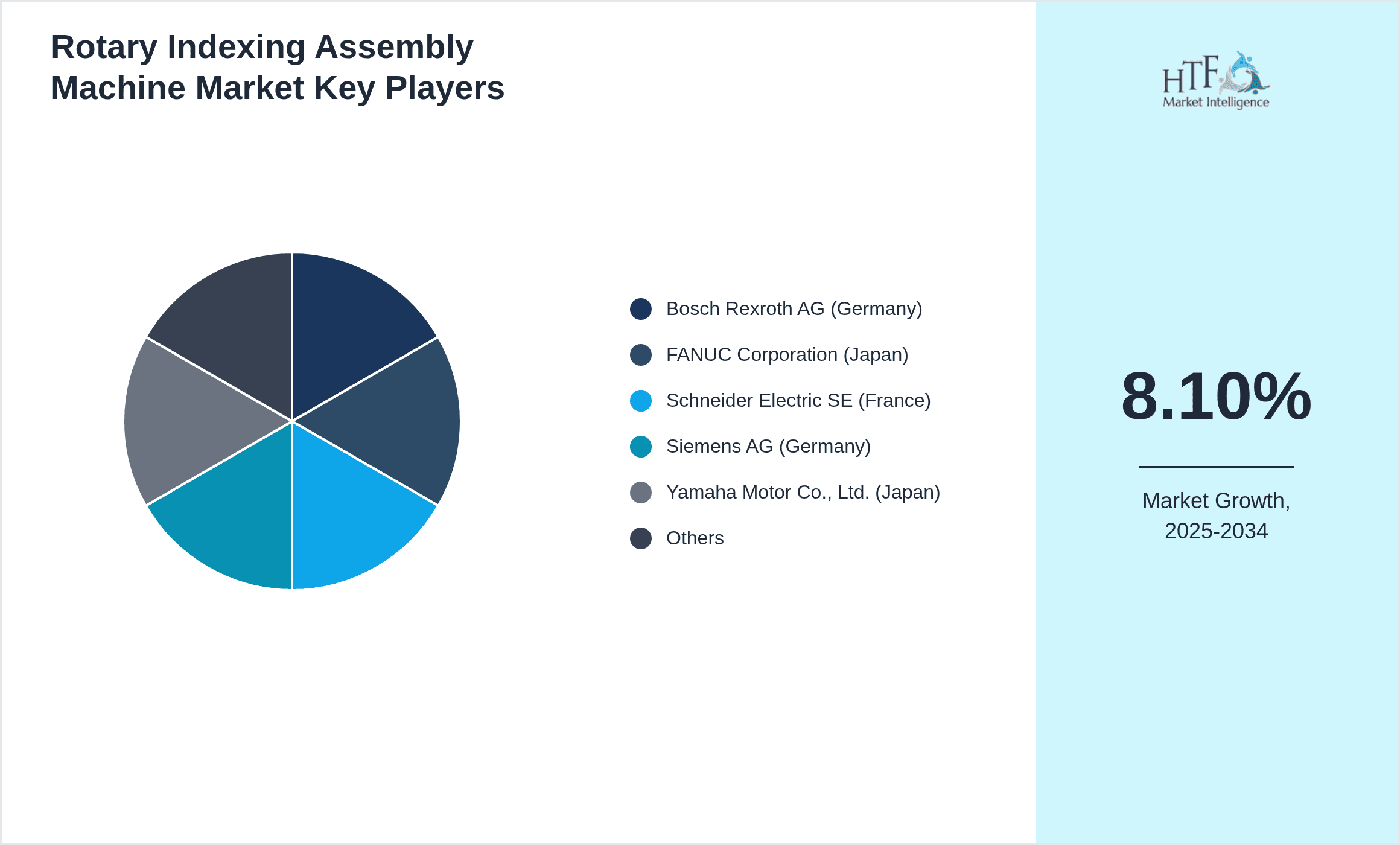

- •Market highlights include a base year size of USD 145.8 million in 2025, with a forecast to reach USD 312.4 million by 2034, reflecting a compound annual growth rate (CAGR) of 8.1%. Saudi Arabia dominates the market with a 34% share, driven by its extensive industrial base and large-scale manufacturing initiatives, while the United Arab Emirates emerges as the fastest-growing country at a CAGR of 10.5%, benefiting from rapid infrastructure development and diversification policies. Servo motor driven rotary indexing machines currently lead the product segment, favored for their precision and energy efficiency, whereas electric rotary indexing machines represent the fastest-growing technology due to advancements in automation and ease of integration with digital factory systems.

- •The GCC Rotary Indexing Assembly Machine market holds strategic value for multiple stakeholders including manufacturers, system integrators, investors, and policymakers. Its growth directly contributes to the region’s industrial competitiveness and manufacturing output quality. The market supports the GCC’s broader economic diversification goals by enabling automation in key sectors, reducing dependency on manual labor, and enhancing export potential of manufactured goods. Stakeholders benefit from opportunities in technology innovation, regional collaborations, and expanding aftermarket services. The market also aligns with sustainable manufacturing practices by promoting energy-efficient machine designs and reducing production waste, reinforcing the region’s commitment to industrial modernization.

Competitive Landscape

The GCC Rotary Indexing Assembly Machine market is characterized by a competitive environment where global machinery manufacturers and regional system integrators collaborate and compete to capture market share. Key competitive strategies include product innovation focused on increasing precision, energy efficiency, and integration capabilities with Industry 4.0 technologies such as IoT and AI-driven predictive maintenance. Companies differentiate themselves through customization options tailored to specific manufacturing processes prevalent in the GCC, such as automotive and electronics assembly. Strategic partnerships between international OEMs and local distributors enable deeper market penetration and enhanced after-sales support. Market entry barriers include high capital investments and the necessity for skilled workforce training. Pricing strategies are influenced by the demand for high-quality, durable machinery balanced against cost sensitivities of regional manufacturers. Mergers and acquisitions, though limited in recent years, provide avenues for consolidation and expansion of technology portfolios. Regional competition is intensified by government incentives promoting local manufacturing capabilities, while digital transformation initiatives propel adoption of advanced rotary indexing solutions. Future trends point toward increasing modularity, automation, and sustainability features, shaping the competitive landscape decisively.

Prominent Players in GCC Rotary Indexing Assembly Machine Market

- •Bosch Rexroth AG (Germany)

- •FANUC Corporation (Japan)

- •Schneider Electric SE (France)

- •Siemens AG (Germany)

- •Yamaha Motor Co., Ltd. (Japan)

- •KUKA AG (Germany)

- •Rockwell Automation, Inc. (United States)

- •Mitsubishi Electric Corporation (Japan)

- •ABB Ltd. (Switzerland)

- •SMC Corporation (Japan)

- •Parker Hannifin Corporation (United States)

- •JTEKT Corporation (Japan)

- •Dürr AG (Germany)

- •Haas Automation, Inc. (United States)

- •Camozzi Automation S.p.A. (Italy)

- •Kawasaki Heavy Industries, Ltd. (Japan)

- •Emerson Electric Co. (United States)

- •Nord Drivesystems Group (Germany)

- •Omron Corporation (Japan)

- •B&R Industrial Automation GmbH (Austria)

- •Schunk GmbH & Co. KG (Germany)

- •Pilz GmbH & Co. KG (Germany)

- •Festo AG & Co. KG (Germany)

- •Lenze SE (Germany)

- •Delta Electronics, Inc. (Taiwan)

Market Breakdown

- •By Rotary Indexing Assembly Machine Type

- ◦Mechanical Rotary Indexing Assembly Machines

- ◦Pneumatic Rotary Indexing Assembly Machines

- ◦Servo Motor Driven Rotary Indexing Machines

- ◦Hydraulic Rotary Indexing Assembly Machines

- ◦Electric Rotary Indexing Assembly Machines

- •By Application in Manufacturing

- ◦Automotive Component Assembly

- ◦Electronics Manufacturing Assembly

- ◦Medical Device Assembly

- ◦Consumer Goods Assembly

- ◦Industrial Machinery Assembly

- •By Service Type

- ◦Installation and Commissioning Services

- ◦Maintenance and Repair Services

- ◦Upgrades and Retrofits

- ◦After-Sales Technical Support

- •By Deployment Model

- ◦On-Premise Deployment

- ◦Cloud-Enabled Monitoring Integration

- ◦Hybrid Automated Assembly Systems

Growth Dynamics

- •Rising industrial automation adoption across GCC countries is a primary growth driver, with manufacturers seeking to improve production precision and throughput while reducing labor costs. For example, Saudi Arabia's Vision 2030 initiative emphasizes industrial diversification, accelerating investments in advanced assembly machinery.

- •Expanding automotive and electronics manufacturing sectors in the UAE and Qatar are driving demand for rotary indexing machines capable of handling complex assembly tasks with high repeatability and speed, fostering regional market expansion.

- •Technological advancements, including the integration of servo motor and electric rotary indexing systems with IoT-enabled monitoring, are enhancing machine efficiency and predictive maintenance capabilities, attracting investment from regional manufacturers.

- •Government incentives and subsidies across GCC nations aimed at promoting smart factory implementations and local manufacturing have stimulated market growth by lowering entry barriers and encouraging adoption of automated assembly technologies.

- •Increasing consumer demand for high-quality, customized products is pushing manufacturers to adopt flexible rotary indexing assembly machines that support rapid changeovers and multi-product assembly lines.

- •Rising foreign direct investment (FDI) and joint ventures between global rotary indexing machine manufacturers and GCC-based enterprises are facilitating technology transfer and expanding market reach within the region.

- •The growing emphasis on energy-efficient and environmentally sustainable manufacturing processes is driving demand for electric rotary indexing machines that reduce energy consumption and operational costs.

Market Trends

- •Increasing integration of Industry 4.0 technologies such as IoT sensors and AI analytics into rotary indexing assembly machines is improving real-time monitoring and predictive maintenance, enhancing operational uptime and reducing downtime.

- •Adoption of modular and flexible rotary indexing systems is rising, enabling manufacturers in the GCC to swiftly adapt production lines to changing product designs and shorter product life cycles.

- •Collaborations between local GCC manufacturers and global automation technology providers are growing, facilitating knowledge exchange and localized solutions tailored to regional production requirements.

- •Sustainability trends are influencing design priorities, with manufacturers increasingly selecting machines that offer reduced energy consumption and lower carbon footprints in line with GCC environmental regulations.

- •Digital twin simulations for rotary indexing assembly processes are gaining traction, allowing manufacturers to optimize machine performance and troubleshoot virtually before physical deployment.

- •The rise of smart factories in the GCC is accelerating adoption of cloud-enabled monitoring and control systems for rotary indexing machines, improving data-driven decision-making and operational transparency.

- •Manufacturers are increasingly investing in after-sales service capabilities, including remote diagnostics and software updates, to enhance machine lifecycle management and customer satisfaction.

Market Opportunities

- •Significant potential exists in expanding rotary indexing assembly machine applications into emerging GCC industries such as renewable energy equipment manufacturing and aerospace component assembly, sectors currently underpenetrated by automation.

- •Growing demand for customized and small-batch production creates opportunities for manufacturers offering flexible and modular rotary indexing machines capable of rapid changeovers and multi-product handling.

- •Investment in localized manufacturing and regional supply chains under GCC economic diversification plans opens avenues for establishing rotary indexing machine production and assembly facilities within the region.

- •Integration of advanced digital technologies, including AI-driven process optimization and predictive maintenance, provides opportunities to develop next-generation rotary indexing machines tailored to GCC market needs.

- •Aftermarket services such as maintenance contracts, retrofits, and upgrades represent a growing revenue stream as installed base of rotary indexing machines increases across GCC manufacturing facilities.

- •Strategic partnerships and joint ventures between local firms and global rotary indexing machine manufacturers can unlock market access and accelerate technology transfer throughout the GCC.

- •Government-backed smart manufacturing initiatives present funding and incentive opportunities for companies investing in innovative rotary indexing assembly solutions attuned to regional industrial policies.

Market Challenges

- •High initial capital expenditure for acquiring advanced rotary indexing assembly machines limits adoption among small and medium-sized enterprises in the GCC, slowing market penetration outside large industrial players.

- •Technical complexity and the requirement for skilled operators and maintenance personnel create barriers, necessitating investment in workforce training and technical support infrastructure.

- •Supply chain disruptions and dependency on imported components can delay machine delivery and increase costs, impacting project timelines and customer satisfaction within the GCC market.

- •Fragmented regional regulatory requirements and standards pose compliance challenges for manufacturers and suppliers seeking to operate uniformly across multiple GCC countries.

- •Competitive pressure from low-cost rotary indexing machines imported from Asia places pricing constraints on regional suppliers, affecting profitability and market share retention.

- •Limited awareness and conservative investment approaches among traditional manufacturers hinder adoption of cutting-edge rotary indexing technologies in some GCC sectors.

- •Integration challenges with existing legacy production lines and systems can lead to operational disruptions and require additional customization and engineering efforts.

Regulatory Framework

- •The GCC countries have implemented manufacturing and safety regulations during 2020-2025 aimed at ensuring operational safety and environmental compliance for industrial assembly machinery. These include standards for electrical safety, machine guarding, and emissions control, which rotary indexing assembly machines must adhere to for market entry.

- •Saudi Arabia's Saudi Standards, Metrology and Quality Organization (SASO) mandates certification for industrial machinery, requiring conformity to quality and safety standards that impact rotary indexing machine manufacturers and importers.

- •The United Arab Emirates enforces regulations through the Emirates Authority for Standardization and Metrology (ESMA), focusing on energy efficiency and sustainability compliance for manufacturing equipment, driving innovations in energy-saving rotary indexing technologies.

- •Regional trade agreements within the GCC facilitate harmonized customs procedures and standards, simplifying cross-border machinery movement but requiring adherence to collective technical regulations and conformity assessments.

- •Government initiatives promoting industrial automation and smart manufacturing also include regulatory support such as incentives and subsidies for adopting compliant advanced machinery, accelerating rotary indexing machine uptake in line with national industrial strategies.

Market Intelligence

- •15th January 2025, Bosch Rexroth AG announced the launch of its latest servo motor driven rotary indexing assembly machine model tailored for the GCC market, featuring enhanced energy efficiency and IoT-enabled predictive maintenance capabilities. The new model aims to support automotive and electronics manufacturers in Saudi Arabia and UAE by reducing downtime and improving assembly precision, aligning with regional industrial modernization goals. Bosch's initiative includes localized after-sales service centers to ensure rapid technical support. Source: Bosch Rexroth Official Press Release

- •22nd March 2025, FANUC Corporation introduced an AI-integrated electric rotary indexing assembly machine designed to optimize production line flexibility for GCC-based manufacturers. This innovation enables real-time monitoring and adaptive control, allowing rapid product changeovers and minimizing waste. FANUC’s deployment strategy focuses on UAE and Qatar, where demand for smart factory solutions is rising. The company partnered with regional distributors to expand service networks. Source: FANUC Corporate Communications

- •10th July 2025, Siemens AG announced a strategic partnership with a leading UAE-based industrial automation firm to co-develop customized rotary indexing assembly machines. This collaboration aims to accelerate the adoption of Industry 4.0 solutions in GCC manufacturing, offering integrated hardware and software platforms that enhance operational efficiency and data analytics capabilities. The initiative is expected to generate significant market traction in Saudi Arabia and Kuwait. Source: Siemens Newsroom

- •5th October 2025, Schneider Electric SE completed the acquisition of a regional automation solutions provider specializing in rotary indexing assembly equipment in the GCC. This move strengthens Schneider’s market position by expanding its local manufacturing and service footprint, enabling faster delivery and tailored solutions for GCC manufacturers. The acquisition supports Schneider’s broader strategy to lead digital transformation in Middle Eastern industrial sectors. Source: Schneider Electric Investor Relations

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 145.8 Million |

| Forecast Year Market Size | USD 312.4 Million |

| CAGR | 8.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Rotary Indexing Assembly Machine Type (Mechanical Rotary Indexing Assembly Machines, Pneumatic Rotary Indexing Assembly Machines, Servo Motor Driven Rotary Indexing Machines, Hydraulic Rotary Indexing Assembly Machines, Electric Rotary Indexing Assembly Machines), Application in Manufacturing (Automotive Component Assembly, Electronics Manufacturing Assembly, Medical Device Assembly, Consumer Goods Assembly, Industrial Machinery Assembly), Service Type (Installation and Commissioning Services, Maintenance and Repair Services, Upgrades and Retrofits, After-Sales Technical Support), Deployment Model (On-Premise Deployment, Cloud-Enabled Monitoring Integration, Hybrid Automated Assembly Systems) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Bosch Rexroth AG (Germany), FANUC Corporation (Japan), Schneider Electric SE (France), Siemens AG (Germany), Yamaha Motor Co., Ltd. (Japan), KUKA AG (Germany), Rockwell Automation, Inc. (United States), Mitsubishi Electric Corporation (Japan), ABB Ltd. (Switzerland), SMC Corporation (Japan), Parker Hannifin Corporation (United States), JTEKT Corporation (Japan), Dürr AG (Germany), Haas Automation, Inc. (United States), Camozzi Automation S.p.A. (Italy), Kawasaki Heavy Industries, Ltd. (Japan), Emerson Electric Co. (United States), Nord Drivesystems Group (Germany), Omron Corporation (Japan), B&R Industrial Automation GmbH (Austria), Schunk GmbH & Co. KG (Germany), Pilz GmbH & Co. KG (Germany), Festo AG & Co. KG (Germany), Lenze SE (Germany), Delta Electronics, Inc. (Taiwan) |

GCC Rotary Indexing Assembly Machine Market - Middle East Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.