GCC Three Piles Offshore Wind Power Jackets Market - GCC Size & Outlook 2025-2034

GCC Three Piles Offshore Wind Power Jackets Market is segmented by Jacket Type (Monopile Jackets, Tripod Jackets, Jacket Structures, Gravity-Based Foundations, Suction Bucket Foundations), Application Area (Fixed Offshore Wind Farms, Floating Offshore Wind Farms, Hybrid Wind Systems, Coastal Protection, Marine Infrastructure), End User (Energy Utilities, Independent Power Producers (IPPs), Engineering, Procurement, and Construction (EPC) Contractors, Government & Regulatory Bodies), Deployment Environment (Shallow Water (<30m), Intermediate Water (30-60m), Deep Water (>60m)), and Geography (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates)

Pricing

Report Overview

Executive Summary

- •The GCC Three Piles Offshore Wind Power Jackets Market is a specialized segment within the renewable energy infrastructure domain focused on offshore wind turbine foundation technologies utilizing three-pile jacket structures. These jackets provide structural stability and support for offshore wind turbines, enabling deployment in challenging marine environments typical of the Gulf region. The market scope covers the entire lifecycle from design, materials sourcing, fabrication, transportation, installation, to operation and maintenance services. Key applications include fixed offshore wind farms, floating offshore wind projects, hybrid systems, coastal protection, and marine infrastructure. This market is driven by GCC countries' strategic priorities to diversify energy portfolios, reduce carbon emissions, and harness abundant offshore wind resources. The industry integrates advanced engineering, steel fabrication technologies, and project management tailored to the unique environmental and regulatory conditions of the GCC. The market's growth is supported by increasing government mandates, private sector investments, and technological innovations enhancing jacket performance and cost-efficiency.

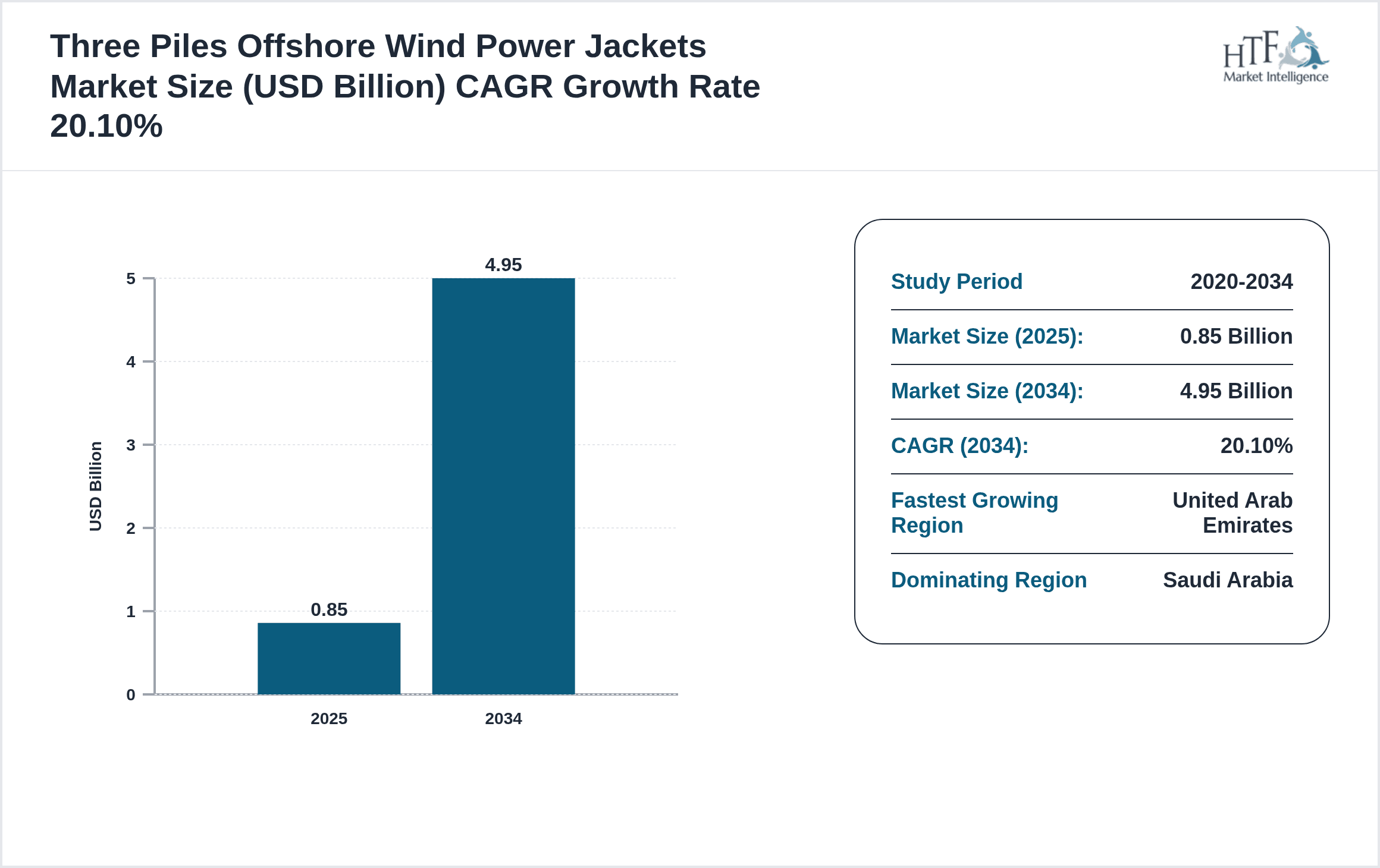

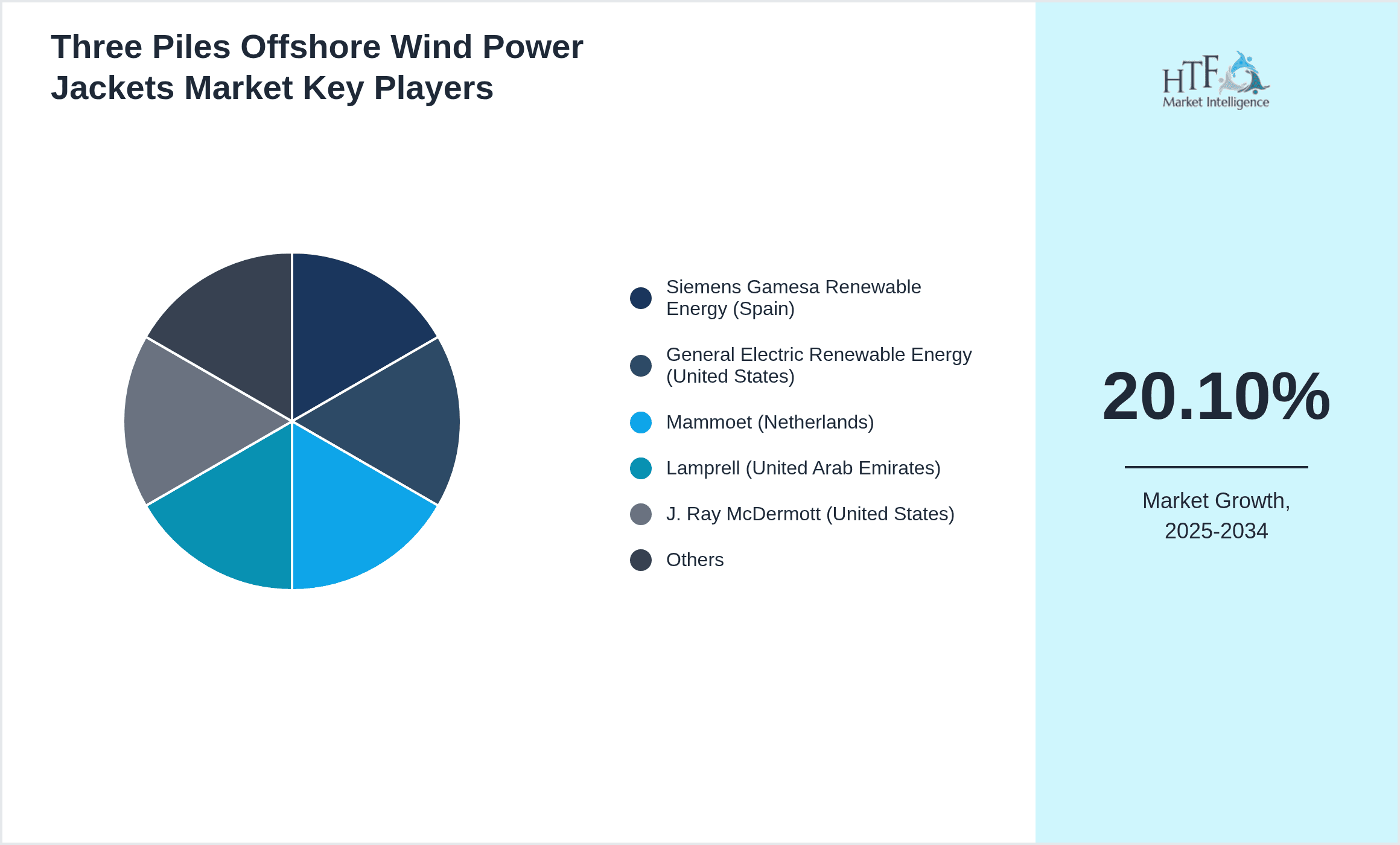

- •Key market highlights include a projected CAGR of 20.1% from 2025 to 2034, with the GCC offshore wind power jackets market expected to grow from USD 0.85 Billion in 2025 to USD 4.95 Billion by 2034. Saudi Arabia leads the regional market share at 38%, followed by the UAE at 26%, which is also the fastest growing country with a CAGR of 24.3%. Monopile jackets dominate the product type segment, driven by ease of installation and cost-effectiveness, while tripod jackets exhibit the fastest growth due to adaptation in deeper waters. Fixed offshore wind farms remain the primary application, complemented by rising deployments in floating and hybrid offshore systems. These data points underscore strong regional momentum fueled by ambitious renewable energy policies and increasing offshore wind capacity installations across the GCC.

- •The GCC Three Piles Offshore Wind Power Jackets Market holds strategic importance for regional energy diversification and sustainability goals. By facilitating robust offshore wind infrastructure, these jackets enable GCC countries to tap into their vast offshore wind potential, reduce reliance on fossil fuels, and comply with international climate commitments. The market offers significant value propositions including technological innovation, local industrial development, and creation of skilled employment opportunities. For investors, manufacturers, and policymakers, understanding this market’s dynamics is critical to unlocking long-term growth, achieving cost efficiencies, and fostering regional cooperation in renewable energy deployment. The market’s expansion also contributes to enhanced energy security and environmental stewardship in the Gulf region.

Competitive Landscape

The GCC Three Piles Offshore Wind Power Jackets Market is characterized by intense competition among global and regional players focusing on innovation, quality, and project execution capabilities. Market leaders emphasize advanced engineering designs that optimize structural integrity and installation efficiency suitable for the unique marine conditions in the Gulf. Companies invest heavily in R&D to develop jackets that reduce material use while enhancing durability against corrosive seawater and high winds. Strategic partnerships and joint ventures between international manufacturers and local firms are common to leverage regional expertise and comply with local content regulations. Competitive differentiation is also achieved through comprehensive service offerings including fabrication, logistics, installation, and after-sales maintenance. Pricing strategies are aligned with project scales and client requirements, with a growing focus on sustainable and cost-effective solutions. Market entry barriers include high capital intensity, stringent regulatory compliance, and the need for specialized technical expertise. The competitive environment is expected to intensify as offshore wind adoption accelerates, driving continuous innovation and consolidation trends.

Leading Companies in GCC Three Piles Offshore Wind Power Jackets Market

- •Siemens Gamesa Renewable Energy (Spain)

- •General Electric Renewable Energy (United States)

- •Mammoet (Netherlands)

- •Lamprell (United Arab Emirates)

- •J. Ray McDermott (United States)

- •Sif Group (Netherlands)

- •TechnipFMC (France)

- •Boskalis Westminster (Netherlands)

- •Jan De Nul Group (Belgium)

- •Saipem (Italy)

- •Navantia (Spain)

- •Van Oord (Netherlands)

- •Hyundai Heavy Industries (South Korea)

- •China Communications Construction Company (China)

- •Petrofac (United Kingdom)

- •Keppel Corporation (Singapore)

- •Doosan Heavy Industries & Construction (South Korea)

- •Lamprell Energy (United Arab Emirates)

- •Vestas Wind Systems (Denmark)

- •CNIM Group (France)

- •ZPMC Offshore (China)

- •Wartsila Corporation (Finland)

- •Baker Hughes (United States)

- •Hyundai Engineering & Construction (South Korea)

- •Al Jaber Energy Services (United Arab Emirates)

Market Breakdown

- •By Jacket Type

- ◦Monopile Jackets

- ◦Tripod Jackets

- ◦Jacket Structures

- ◦Gravity-Based Foundations

- ◦Suction Bucket Foundations

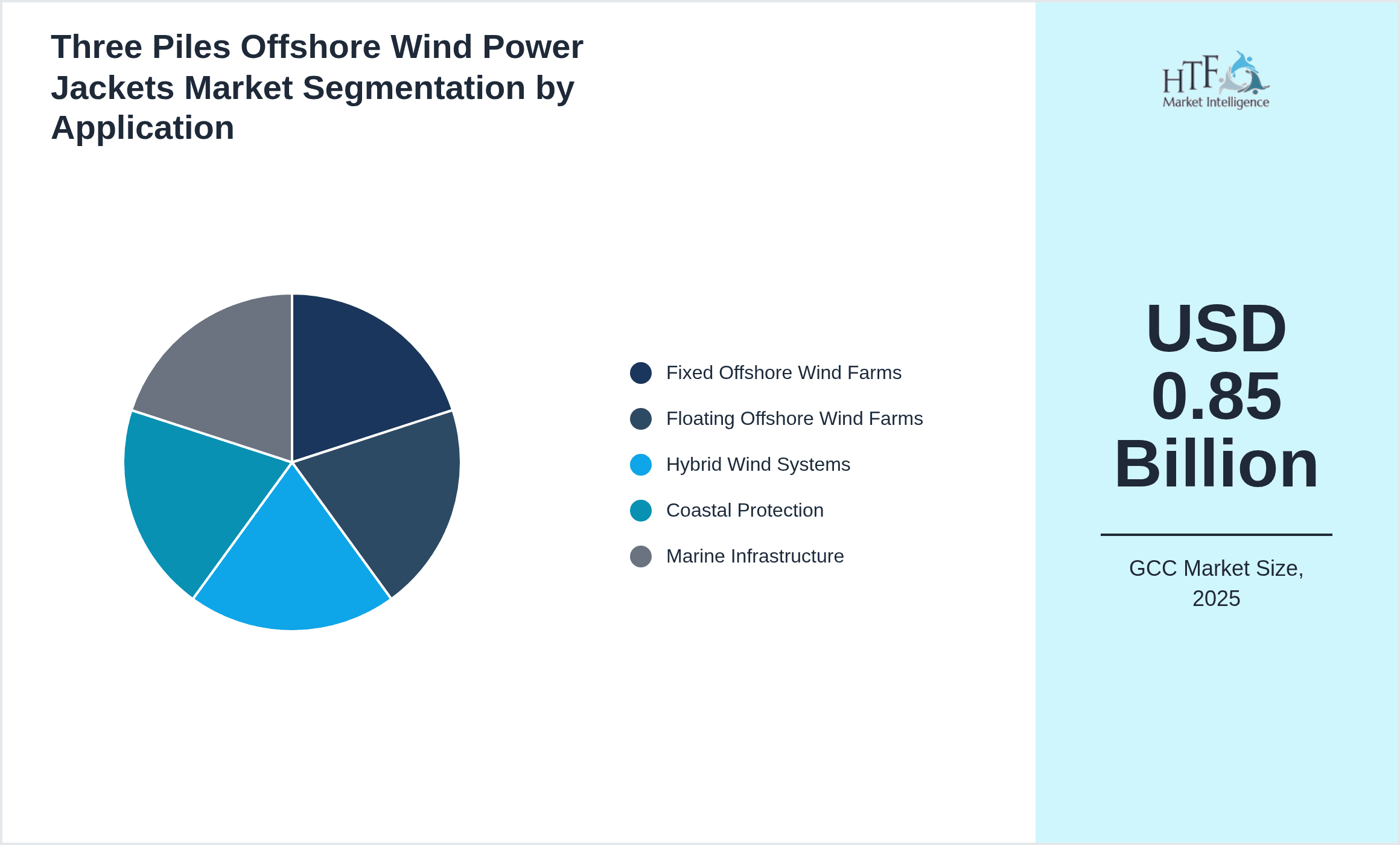

- •By Application Area

- ◦Fixed Offshore Wind Farms

- ◦Floating Offshore Wind Farms

- ◦Hybrid Wind Systems

- ◦Coastal Protection

- ◦Marine Infrastructure

- •By End User

- ◦Energy Utilities

- ◦Independent Power Producers (IPPs)

- ◦Engineering, Procurement, and Construction (EPC) Contractors

- ◦Government & Regulatory Bodies

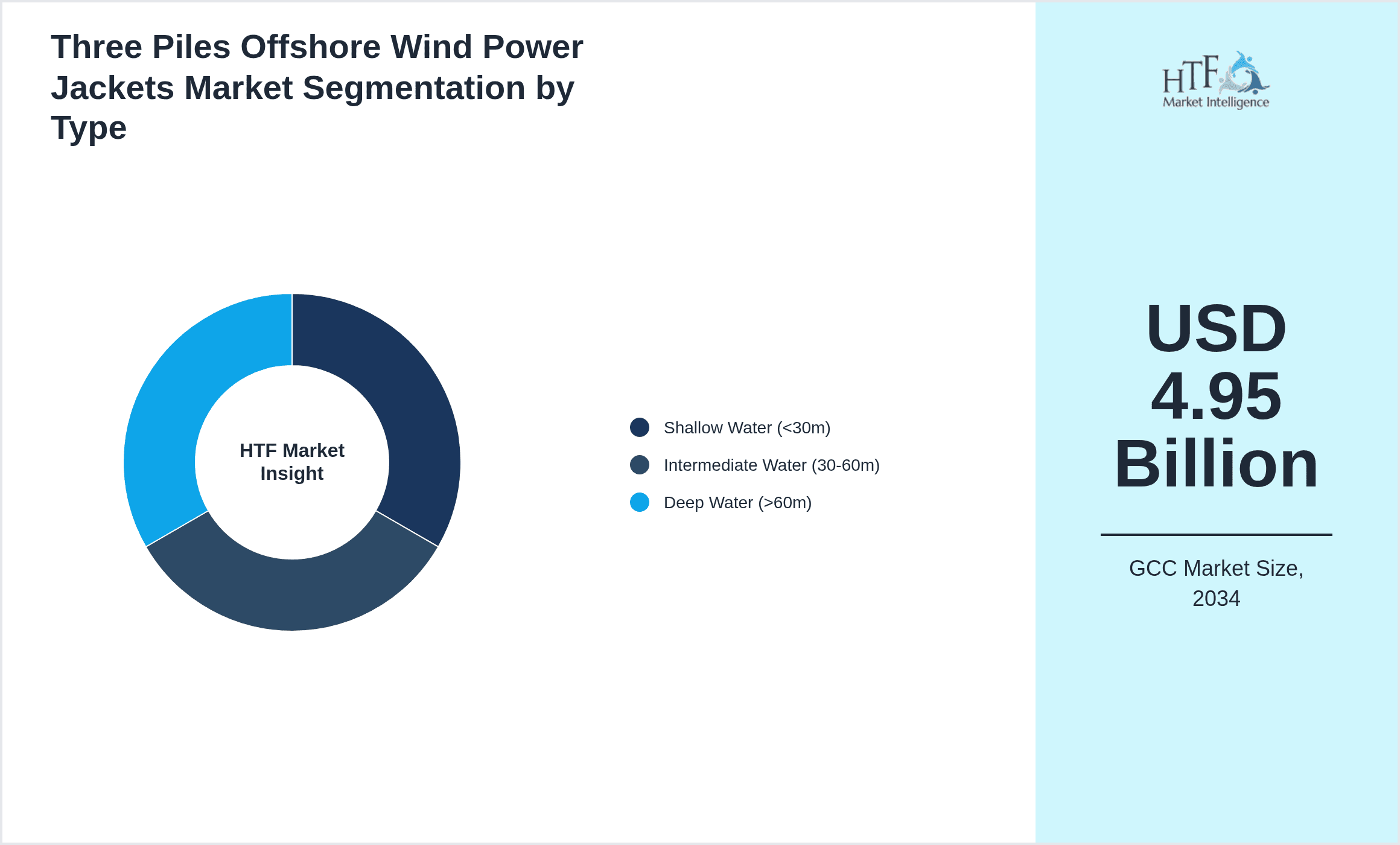

- •By Deployment Environment

- ◦Shallow Water (<30m)

- ◦Intermediate Water (30-60m)

- ◦Deep Water (>60m)

Growth Dynamics

- •Government initiatives to diversify energy sources and reduce carbon emissions are accelerating investment in offshore wind projects across the GCC, driving demand for advanced three-pile offshore wind power jackets. These policies include renewable energy targets, subsidies, and regulatory frameworks favoring clean power infrastructure development.

- •Technological advancements in jacket design and fabrication techniques have enhanced structural resilience, installation efficiency, and cost-effectiveness, encouraging broader adoption of three-pile jackets in offshore wind farms within the region. Innovations such as corrosion-resistant coatings and modular construction contribute significantly to market growth.

- •Rising offshore wind capacity installations in Saudi Arabia and UAE, fueled by abundant wind resources and falling technology costs, are expanding the market for three-pile jackets. Major infrastructure projects and strategic partnerships with global manufacturers further bolster growth prospects.

- •The expansion of local manufacturing capabilities and supply chains within the GCC is reducing reliance on imports, shortening project lead times, and improving cost competitiveness in offshore wind jacket fabrication.

- •Increasing awareness about environmental sustainability and energy security among GCC stakeholders is driving preference for offshore wind solutions, which require robust foundational jackets to ensure reliable long-term operations under harsh marine conditions.

Market Trends

- •The GCC market is witnessing a shift towards hybrid offshore wind systems integrating floating and fixed foundations to optimize energy capture in varying water depths and wind conditions, expanding the application of three-pile offshore wind power jackets beyond traditional fixed farms.

- •Collaborative ventures between international offshore wind technology providers and GCC-based engineering firms are increasing, enhancing knowledge transfer and accelerating localization of jacket manufacturing and installation services.

- •Sustainability-driven innovation is trending, with companies developing eco-friendly materials and designs that minimize seabed disturbance and support marine biodiversity alongside offshore wind infrastructure deployment.

- •Digitalization and use of data analytics in jacket design, monitoring, and predictive maintenance are gaining traction in the GCC, improving operational efficiency and reducing downtime in offshore wind projects.

- •The market is adapting to stricter regulatory standards for offshore construction and environmental protection, driving adoption of higher quality control and certification processes for three-pile jackets.

Market Opportunities

- •Emerging offshore wind projects planned in Oman and Kuwait present untapped opportunities for expanding three-pile jacket deployments, supported by government incentives and growing private sector interest.

- •Advancements in floating foundation technologies compatible with three-pile jacket configurations provide avenues for growth in deeper offshore zones beyond traditional fixed foundation depths in the GCC.

- •Expanding regional manufacturing hubs and supply chain ecosystems offer opportunities for cost optimization, faster project delivery, and increased local employment in the offshore wind jackets sector.

- •Collaborations with global technology leaders for joint development and transfer of advanced jacket fabrication techniques can enhance GCC companies’ competitiveness and innovation capabilities.

- •Growing demand for marine infrastructure supporting offshore wind farms, such as ports and logistics facilities, opens adjacent markets for companies specializing in three-pile jacket fabrication and installation.

Market Challenges

- •High capital expenditure and long project development cycles pose significant barriers to entry and expansion for new players in the GCC three-pile offshore wind power jackets market.

- •Technical complexities related to jacket design and installation in harsh marine environments with extreme temperatures and salinity levels increase operational risks and costs.

- •Scarcity of skilled labor and specialized engineering expertise in the GCC limits rapid scaling of local manufacturing and installation capabilities.

- •Supply chain disruptions and dependency on imported raw materials and components can delay project timelines and impact cost structures.

- •Regulatory uncertainties and evolving environmental standards require continuous adaptation by manufacturers and project developers, complicating compliance efforts.

Regulatory Framework

- •Between 2022 and 2025, GCC countries have introduced comprehensive renewable energy policies mandating offshore wind capacity targets, with specific guidelines on environmental impact assessments and marine spatial planning to ensure sustainable development of offshore infrastructure.

- •Saudi Arabia’s Renewable Energy Project Development Office (REPDO) enforced stricter technical standards in 2023 for offshore wind foundation design, focusing on structural integrity, corrosion resistance, and load-bearing capacity, impacting jacket manufacturing requirements.

- •The UAE updated its maritime construction regulations in 2024 to include mandatory certification and quality assurance protocols for offshore wind power jackets, enhancing safety and performance benchmarks in the sector.

- •Qatar’s environmental agency introduced new regulations in 2023 requiring detailed monitoring and reporting of marine ecological impacts during offshore wind farm installation, influencing project planning and operational compliance.

- •GCC-wide initiatives promote local content requirements and incentivize domestic manufacturing of offshore wind components, including jackets, supporting regional economic diversification and technology transfer objectives.

Market Intelligence

- •15th February 2025, Siemens Gamesa Renewable Energy announced the launch of a new advanced monopile jacket design tailored for deep-water offshore wind projects in the GCC. The design incorporates enhanced corrosion-resistant coatings and modular elements to reduce installation time and costs, targeting Saudi Arabia and UAE markets specifically. This innovation is expected to support the region’s growing offshore wind capacity with improved durability and efficiency. Source: Siemens Gamesa official release.

- •10th May 2025, Lamprell (UAE) unveiled its state-of-the-art fabrication facility expansion dedicated to offshore wind power jackets. The facility employs automated welding and quality control technologies to increase production capacity by 40%, supporting regional demand surge. This strategic move positions Lamprell as a key local player capable of meeting GCC offshore wind infrastructure needs. Source: Lamprell corporate announcement.

- •30th March 2025, General Electric Renewable Energy entered into a strategic partnership with Al Jaber Energy Services to co-develop jacket foundation solutions optimized for the Gulf’s marine conditions. The collaboration aims to integrate advanced design software and local manufacturing expertise, accelerating project delivery timelines and enhancing cost competitiveness. This alliance strengthens the offshore wind supply chain within the GCC. Source: GE Renewable Energy press statement.

- •22nd January 2025, Mammoet secured a contract to provide heavy lifting and transport services for multiple offshore wind jacket installation projects in Saudi Arabia’s Red Sea coast. The contract includes specialized lifting equipment and logistical planning to address challenging offshore environments, underscoring Mammoet’s critical role in GCC offshore wind infrastructure execution. Source: Mammoet official news.

Regional Outlook

The Saudi Arabia currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, United Arab Emirates is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Bahrain

- Kuwait

- Oman

- Qatar

- Saudi Arabia

- United Arab Emirates

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 4.95 Billion |

| CAGR | 20.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 18.6% |

| Scope of Report | Market is segmented by Jacket Type (Monopile Jackets, Tripod Jackets, Jacket Structures, Gravity-Based Foundations, Suction Bucket Foundations), Application Area (Fixed Offshore Wind Farms, Floating Offshore Wind Farms, Hybrid Wind Systems, Coastal Protection, Marine Infrastructure), End User (Energy Utilities, Independent Power Producers (IPPs), Engineering, Procurement, and Construction (EPC) Contractors, Government & Regulatory Bodies), Deployment Environment (Shallow Water (<30m), Intermediate Water (30-60m), Deep Water (>60m)) |

| Regions Covered | Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates |

| Key Companies | Siemens Gamesa Renewable Energy (Spain), General Electric Renewable Energy (United States), Mammoet (Netherlands), Lamprell (United Arab Emirates), J. Ray McDermott (United States), Sif Group (Netherlands), TechnipFMC (France), Boskalis Westminster (Netherlands), Jan De Nul Group (Belgium), Saipem (Italy), Navantia (Spain), Van Oord (Netherlands), Hyundai Heavy Industries (South Korea), China Communications Construction Company (China), Petrofac (United Kingdom), Keppel Corporation (Singapore), Doosan Heavy Industries & Construction (South Korea), Lamprell Energy (United Arab Emirates), Vestas Wind Systems (Denmark), CNIM Group (France), ZPMC Offshore (China), Wartsila Corporation (Finland), Baker Hughes (United States), Hyundai Engineering & Construction (South Korea), Al Jaber Energy Services (United Arab Emirates) |

GCC Three Piles Offshore Wind Power Jackets Market - GCC Size & Outlook 2025-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.