United States Temporary Bonding and Debonding Systems Market Size, Growth & Revenue 2024-2034

United States Temporary Bonding and Debonding Systems Market is segmented by Type (Adhesive-Based Systems, Mechanical Clamping Systems, Vacuum-Based Systems, Thermal Release Systems, UV-Curable Systems), Application (Semiconductor Manufacturing, MEMS Fabrication, Display Assembly, Photovoltaic Cells, Medical Device Production), End-User Industry (Electronics Manufacturing, Renewable Energy, Healthcare Equipment, Automotive Electronics), Deployment Model (Automated Systems, Semi-Automated Systems, Manual Systems), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States Temporary Bonding and Debonding Systems Market is a specialized sector within advanced manufacturing technologies focusing on temporary adhesion and separation solutions. These systems are essential for ensuring substrate stability during critical manufacturing steps, especially in semiconductor wafer processing, MEMS devices, display assembly, photovoltaic cells, and medical device production. The market comprises multiple product types including adhesive-based, mechanical clamping, vacuum-based, thermal release, and UV-curable systems, each offering unique benefits tailored to diverse application demands. The industry supports high-precision manufacturing by providing reliable temporary bonds that withstand mechanical and thermal stresses while enabling damage-free debonding. This market is driven by increasing demand for miniaturization, yield improvement, and process efficiency in the United States manufacturing landscape. Innovations in bonding materials, automation integration, and environmentally friendly solutions continue to expand market opportunities. The sector also aligns with broader trends in electronics, renewable energy, and healthcare device manufacturing, underpinning its strategic importance and growth potential within the regional industrial ecosystem.

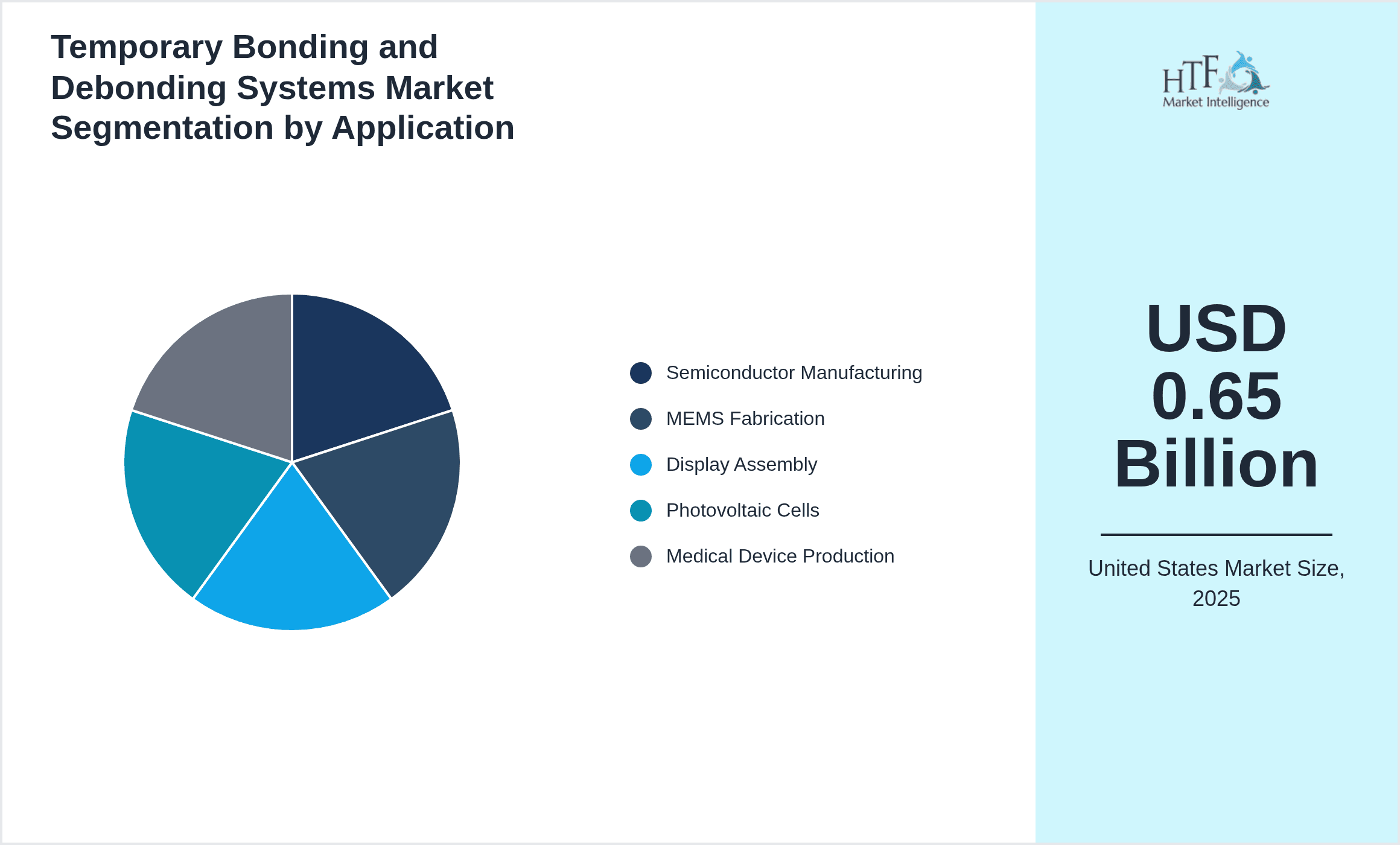

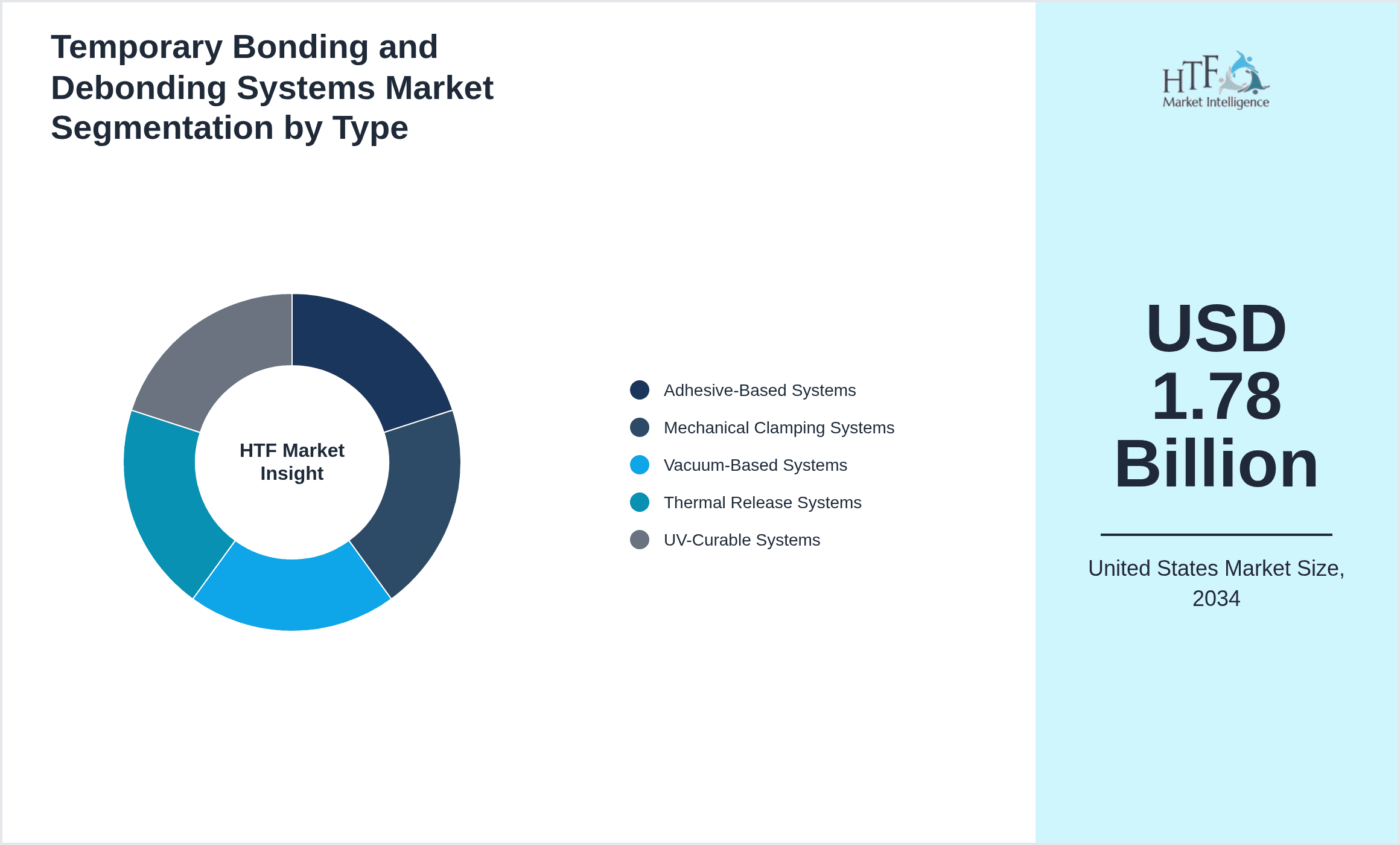

- •Key market highlights include a projected CAGR of 11.2% from 2024 to 2034, with the market size expected to grow from USD 0.65 Billion in 2024 to USD 1.78 Billion by 2034. The West Coast region dominates the market with a 32% share, supported by a mature semiconductor and electronics manufacturing ecosystem, while the Southeast region is the fastest growing at a CAGR of 13.5%, fueled by expanding medical device production and renewable energy sectors. Adhesive-based systems lead product categories due to their versatility and ease of integration, whereas thermal release systems represent the fastest-growing product segment driven by demand for efficient process cycles. Semiconductor manufacturing remains the leading application, with burgeoning opportunities in photovoltaic and medical device assembly. The market’s growth is underpinned by technological advancements, increasing automation, and stringent quality requirements in manufacturing processes.

- •The market offers substantial value to manufacturers by enhancing process yields, reducing substrate damage, and enabling complex device architectures. Strategic importance spans semiconductor fabs, MEMS manufacturers, display fabricators, and medical device producers, all requiring precise temporary bonding solutions. Stakeholders benefit from innovations that reduce costs and improve throughput, while suppliers capitalize on rising demand for customized bonding systems. Environmental regulations and sustainability considerations drive development of eco-friendly adhesives and energy-efficient debonding methods. The market’s continued evolution will be shaped by integration with Industry 4.0 technologies, further automation, and collaboration across the supply chain. Overall, the United States Temporary Bonding and Debonding Systems Market represents a critical enabler of advanced manufacturing competitiveness and technological leadership.

Competitive Landscape

The competitive environment in the United States Temporary Bonding and Debonding Systems Market is characterized by a mix of established multinational corporations and specialized regional players. Market dynamics revolve around continuous innovation in bonding materials, system automation, and process integration to meet stringent manufacturing requirements, especially in semiconductor and medical device sectors. Leading companies focus on developing proprietary adhesive chemistries and thermal release technologies, striving for differentiation through enhanced performance and environmental sustainability. Competitive strategies include strategic partnerships with equipment manufacturers, investments in R&D, and expanding service portfolios to offer end-to-end bonding solutions. Pricing strategies vary based on customization levels and technological complexity, with premium pricing for high-precision systems justified by yield improvements. Regional competition is intense in technology hubs such as the West Coast, while emerging manufacturing zones in the Southeast present opportunities for new entrants. Market entry barriers include high capital expenditure, technical expertise requirements, and regulatory compliance. Future trends suggest increasing consolidation through mergers and acquisitions, fostering integrated solutions and expanding geographic presence to secure competitive advantage.

Leading Companies in Temporary Bonding and Debonding Systems Market

- •3M Company (United States)

- •Henkel Corporation (United States)

- •TOK America, Inc. (United States)

- •Shin-Etsu Chemical Co., Ltd. (Japan)

- •Dow Inc. (United States)

- •Panasonic Corporation (Japan)

- •Asahi Kasei Corporation (Japan)

- •Saint-Gobain Performance Plastics (France)

- •Henkel AG & Co. KGaA (Germany)

- •Nitto Denko Corporation (Japan)

- •E. I. du Pont de Nemours and Company (United States)

- •Fujikura Ltd. (Japan)

- •Hitachi Chemical Co., Ltd. (Japan)

- •LORD Corporation (United States)

- •Avantor, Inc. (United States)

- •Alpha Assembly Solutions (United States)

- •Henkel Loctite (United States)

- •Tesa SE (Germany)

- •Dymax Corporation (United States)

- •Mitsubishi Chemical Corporation (Japan)

- •Solvay S.A. (Belgium)

- •3M Innovative Properties Company (United States)

- •Adhesives Research, Inc. (United States)

- •Fujifilm Holdings Corporation (Japan)

- •Nippon Electric Glass Co., Ltd. (Japan)

Market Breakdown

- •By Type

- ◦Adhesive-Based Systems

- ◦Mechanical Clamping Systems

- ◦Vacuum-Based Systems

- ◦Thermal Release Systems

- ◦UV-Curable Systems

- •By Application

- ◦Semiconductor Manufacturing

- ◦MEMS Fabrication

- ◦Display Assembly

- ◦Photovoltaic Cells

- ◦Medical Device Production

- •By End-User Industry

- ◦Electronics Manufacturing

- ◦Renewable Energy

- ◦Healthcare Equipment

- ◦Automotive Electronics

- •By Deployment Model

- ◦Automated Systems

- ◦Semi-Automated Systems

- ◦Manual Systems

Growth Dynamics

- •The United States Temporary Bonding and Debonding Systems Market is propelled by the growing semiconductor manufacturing industry, which demands high-precision bonding technologies to enhance wafer handling and reduce defects. Increasing miniaturization of electronic components has heightened the need for advanced temporary bonding solutions that can withstand complex processing steps without compromising substrate integrity. Additionally, the expanding renewable energy sector, particularly photovoltaic cell production, is driving demand for efficient bonding systems to improve module assembly yields. Technological innovations such as thermal release adhesives and UV-curable bonding agents are facilitating faster processing times and improved automation compatibility, further accelerating market growth. The rise of MEMS and medical device manufacturing in the United States supports diversified application opportunities, while stringent quality standards necessitate reliable debonding systems to ensure product safety and performance. Overall, these factors combine to create a robust growth environment with sustained investment and innovation focus within the market.

- •Advancements in temporary bonding materials have introduced environmentally friendly, low-residue adhesives that align with the United States’ regulatory focus on sustainability. Such innovations reduce hazardous waste and improve workplace safety, making bonding systems more attractive for manufacturers seeking compliance and green certifications. The integration of Industry 4.0 and automation technologies into bonding and debonding equipment enables real-time process monitoring and control, enhancing yield and reducing operational costs. Growing collaboration between bonding system suppliers and semiconductor fabs fosters customized solutions tailored to specific manufacturing needs, thus driving market adoption. Moreover, the rise in patent filings and R&D investments by major players underscores the competitive push for next-generation bonding technologies. These trends collectively contribute to a dynamic market landscape characterized by continuous improvement and expanding application breadth.

- •Despite strong growth prospects, the market faces restraints such as high capital expenditure for advanced bonding equipment and the technical complexity involved in integrating these systems into existing manufacturing lines. The sensitivity of temporary bonding processes to variation in substrate materials and processing conditions requires precise customization, which can increase costs and limit scalability for some end-users. Furthermore, the stringent regulatory environment in the United States demands rigorous testing and certification, potentially delaying product introduction and increasing compliance costs. Market fragmentation with numerous niche players also challenges consolidation efforts, while supply chain disruptions can impact material availability. These factors collectively impose challenges that manufacturers and suppliers must navigate to sustain growth and competitive positioning.

- •Opportunities abound in expanding the application of temporary bonding and debonding systems beyond traditional semiconductor manufacturing into emerging sectors such as flexible electronics, wearable devices, and advanced medical implants. The growing adoption of electric vehicles in the United States presents new prospects for bonding systems in automotive electronics assembly. Additionally, increasing government initiatives supporting renewable energy infrastructure create demand for photovoltaic module manufacturing enhancements, driving temporary bonding technology uptake. Strategic partnerships between bonding system providers and equipment manufacturers can accelerate integration of novel technologies and expand market reach. The development of customized adhesive formulations and modular bonding solutions tailored to specific substrates and process requirements represents another key opportunity to differentiate offerings and capture niche segments. Furthermore, expanding end-user awareness of bonding technology benefits and cost efficiencies will foster broader adoption across manufacturing verticals.

- •Key challenges in the United States market include managing cost pressures amid competitive pricing, ensuring product reliability across diverse substrate types, and addressing the evolving regulatory landscape for chemical adhesives. The need for continuous innovation to keep pace with rapid technological advances in semiconductor and medical device fabrication demands significant R&D investment. Furthermore, the complexity of bonding and debonding processes requires skilled technical support and training, which can be a barrier for smaller manufacturers. Supply chain vulnerabilities, particularly for specialty adhesive raw materials, pose risks to consistent production. Additionally, balancing environmental considerations with performance requirements challenges material scientists and equipment designers. Addressing these challenges requires collaborative industry efforts, robust quality control systems, and flexible, adaptive product development strategies.

Market Trends

- •The United States market is witnessing a growing trend towards the adoption of thermal release bonding systems, which enable rapid debonding through controlled heating, reducing cycle times and minimizing substrate damage. This trend is driven by the semiconductor industry's need for high-throughput and precision processing. Additionally, UV-curable adhesives are gaining traction due to their fast curing times and environmentally friendly profiles, aligning with sustainability goals. There is also an increased focus on integrating bonding systems with automated handling equipment and real-time process monitoring to enhance manufacturing efficiency and reduce human error. Suppliers are investing in developing multifunctional bonding materials that can provide both strong adhesion and easy debonding tailored to specific substrate types. Furthermore, collaborations between bonding system manufacturers and end-users to co-develop customized solutions are becoming more prevalent, reflecting a shift towards customer-centric innovation.

- •Innovation patterns highlight the deployment of advanced materials such as nano-engineered adhesives that exhibit superior bonding strength and thermal stability while allowing clean debonding. These materials support the production of next-generation semiconductors and flexible electronics. Business models are evolving towards offering bonding solutions as part of integrated service packages that include consulting, maintenance, and training, enhancing customer value propositions. The rise of Industry 4.0 technologies is catalyzing digitalization of bonding processes with IoT-enabled equipment and AI-driven predictive maintenance gaining ground. This shift improves operational efficiency and reduces downtime. Additionally, market players are increasingly emphasizing sustainability by developing bio-based adhesives and reducing volatile organic compounds (VOCs) in bonding agents to comply with tightening environmental regulations.

- •Strategic partnerships and acquisitions have become a key trend to accelerate innovation and expand geographic footprint within the United States. For example, collaborations between adhesive manufacturers and semiconductor equipment suppliers have resulted in the co-development of bonding systems optimized for specific fabrication processes. Companies are also investing in expanding their service networks and technical support capabilities to enhance customer engagement and retention. Measurable outcomes include reduced defect rates, higher throughput, and extended equipment lifecycles reported by early adopters. Additionally, industry players are leveraging data analytics to refine bonding process parameters, improving yield consistency. Such strategic moves reinforce competitive positioning and drive market consolidation. The focus on customer-centric innovation and enhanced service offerings reshapes traditional product-centric business models in the sector.

- •Digitalization and sustainability are prominent trends influencing operational efficiency and regulatory compliance within the United States market. Real-time monitoring of bonding and debonding processes using sensors and software analytics enables rapid detection of anomalies, facilitating proactive interventions and minimizing scrap rates. Simultaneously, manufacturers are adopting eco-friendly bonding materials and waste reduction practices to meet stringent environmental standards and corporate social responsibility goals. These trends contribute to cost optimization and brand reputation enhancement. Market players are also embracing circular economy principles by developing reusable and recyclable bonding materials, supporting long-term sustainability objectives. This convergence of digital and green initiatives is transforming the temporary bonding and debonding systems landscape towards more efficient and responsible manufacturing practices.

- •Collaboration and ecosystem development are shaping the United States temporary bonding market as suppliers, equipment manufacturers, and end-users increasingly engage in joint innovation efforts. Partnerships often focus on co-developing customized bonding solutions for emerging semiconductor nodes, flexible electronics, and medical device applications. Industry consortia and standards bodies are working to harmonize bonding process requirements and testing protocols, facilitating interoperability and reducing development cycles. Consumer preferences for high-quality, reliable products drive demand for bonding systems that ensure device performance and durability. Market segmentation is becoming more refined, with suppliers targeting specific application niches through tailored material formulations and system designs. This ecosystem approach enhances knowledge sharing, accelerates commercialization, and fosters competitive advantage across the value chain.

- •The United States market is also exploring future directions including the integration of AI and machine learning to optimize bonding parameters dynamically, enabling adaptive process control and enhanced yield. Disruptive innovations such as laser-assisted debonding and hybrid bonding techniques are under development, promising higher precision and throughput. Paradigm shifts towards miniaturized and flexible devices are driving demand for bonding systems capable of handling delicate substrates without damage. Emerging applications in quantum computing and advanced sensors open new frontiers for temporary bonding technology. These future innovations are expected to reshape market dynamics, create new business opportunities, and reinforce the United States’ position as a leader in advanced manufacturing technologies.

Market Opportunities

- •The expanding semiconductor and MEMS manufacturing sectors in the United States present significant growth opportunities for temporary bonding and debonding systems, particularly through tailored solutions addressing advanced node requirements and heterogeneous integration challenges. Targeting emerging applications such as flexible electronics and wearable medical devices can unlock untapped segments with specialized bonding needs. Market gaps exist in developing bonding materials compatible with novel substrates like polymers and ultra-thin wafers, presenting opportunities for innovation. Furthermore, integration of bonding systems with Industry 4.0 automation platforms offers potential for enhanced process control and yield improvements, attracting manufacturers focused on operational excellence. Strategic investment in R&D to produce eco-friendly and low-residue adhesives aligns with increasing regulatory scrutiny and customer sustainability expectations, opening avenues for differentiation and market penetration.

- •Emerging needs in electric vehicle electronics assembly and renewable energy device fabrication create new application areas for temporary bonding technologies in the United States. Expanding geographic presence in rapidly growing manufacturing hubs such as the Southeast region can capitalize on shifting production trends. Collaborations with equipment manufacturers and end-users to co-develop customized bonding and debonding solutions tailored to specific process requirements can accelerate adoption and customer loyalty. Additionally, leveraging modular and scalable system designs can address the needs of small and medium enterprises expanding production capabilities. These expansion possibilities offer strategic growth pathways for market participants aiming to broaden their footprint and diversify revenue streams.

- •Investment opportunities exist in developing advanced adhesive formulations with multifunctional properties such as enhanced thermal stability, rapid curing, and environmentally benign profiles. Technology integration opportunities include embedding sensors and IoT devices within bonding systems for real-time process analytics and predictive maintenance, creating value-added solutions. Market penetration can be accelerated by expanding service offerings to include technical training, on-site support, and consulting, establishing long-term customer partnerships. Geographic expansion into underpenetrated sub-regions like the Midwest and Southwest, which are witnessing industrial growth, further enhances market potential. Focused marketing and education initiatives to raise awareness about bonding technology benefits among emerging manufacturers also present avenues for growth.

- •Geographical expansion into the Southeastern United States, driven by increasing investments in semiconductor fabrication and medical device manufacturing facilities, offers a promising opportunity for temporary bonding system suppliers. The region’s favorable economic policies and skilled labor availability support market entry and growth. Additionally, exploring new applications in high-growth sectors such as flexible displays and advanced sensors can diversify the product portfolio and reduce dependence on traditional semiconductor manufacturing. Customized product development targeting specific substrate materials and bonding challenges creates niche market advantages. Enhanced value proposition through sustainability-focused innovations and integration with digital manufacturing platforms positions companies to capture evolving customer demands and regulatory requirements effectively.

- •Product development opportunities include creating bonding systems compatible with next-generation substrates like gallium nitride (GaN) and silicon carbide (SiC) used in high-power electronics. Enhancing service capabilities through remote diagnostics and automated maintenance support can improve customer satisfaction and reduce downtime. Collaborations and strategic alliances with raw material suppliers and equipment manufacturers can streamline supply chains and accelerate time-to-market for new solutions. Additionally, acquisitions targeting niche technology providers or regional players can strengthen market positioning and broaden technological capabilities. Monitoring future market needs driven by emerging applications and regulatory changes enables proactive strategy formulation to sustain competitive advantage and long-term growth.

- •Partnerships with academic institutions and research organizations foster innovation in bonding materials and system designs, accelerating development cycles and commercialization. Joint ventures with regional manufacturers can facilitate market entry and local customization. Mergers and acquisitions provide opportunities to consolidate fragmented market segments and expand technology portfolios. Establishing collaborative platforms for knowledge exchange and standardization enhances ecosystem development and market coherence. These strategic alliance potentials enable companies to leverage complementary strengths, optimize resource utilization, and drive market expansion effectively.

- •Future market needs shaped by the rise of flexible and wearable electronics require bonding systems with exceptional flexibility and durability, prompting innovation in adhesive chemistries and system designs. Regulatory changes emphasizing environmental protection and worker safety will necessitate development of low-VOC and bio-based bonding materials, driving product evolution. Societal trends favoring sustainable manufacturing and circular economy principles will increase demand for recyclable and reusable bonding systems. Continuous monitoring of these dynamics allows companies to align product strategies with evolving market expectations, ensuring relevance and competitiveness in the long term.

Market Challenges

- •One significant challenge in the United States Temporary Bonding and Debonding Systems Market is managing the high capital expenditure required for acquiring and integrating advanced bonding equipment, which can be prohibitive for small and medium-sized manufacturers. This financial barrier limits market penetration and slows adoption of cutting-edge technologies. Additionally, the complexity of bonding processes, which must be precisely tailored to diverse substrate materials and application requirements, demands extensive technical expertise and customization, increasing operational costs and implementation timeframes. Manufacturers face difficulties in balancing adhesive performance with ease of debonding, where suboptimal formulations may lead to substrate damage or process inefficiencies. These challenges necessitate ongoing R&D investment and robust customer support to ensure successful deployment.

- •Technical limitations such as variability in substrate surface properties and sensitivity to environmental factors like temperature and humidity complicate bonding process control. Ensuring consistent bond strength and debonding reliability across production batches is challenging, affecting yield and product quality. Resource constraints, including scarcity of specialty raw materials and skilled labor, further impact manufacturing continuity. Market obstacles include competition from alternative bonding technologies and the need to continuously innovate to maintain differentiation. Regulatory compliance requirements impose additional burdens related to chemical safety, environmental impact, and worker health, which can delay product approvals and increase costs. Addressing these multifaceted challenges requires comprehensive strategies encompassing technology, training, and regulatory navigation.

- •Several companies in the United States have encountered issues related to the integration of new bonding systems into legacy manufacturing lines, resulting in operational disruptions and increased downtime. Mitigation strategies involve extensive pilot testing, modular system designs, and enhanced customer training programs to facilitate smoother transitions. Cost pressures from market competition compel suppliers to optimize pricing without compromising quality, challenging profitability. Market saturation in certain mature segments limits growth potential, necessitating diversification and innovation. Supply chain complexities, particularly amid global disruptions, affect availability of critical adhesive components and system parts. Talent shortages in specialized bonding technology fields hinder capacity expansion and technical service quality. Infrastructure gaps in emerging manufacturing zones pose logistical and operational hurdles. Overcoming these challenges is essential for sustainable growth and competitive advantage.

- •Cost structures in the United States market are influenced by raw material price volatility, high labor costs, and capital intensity of bonding system manufacturing. Pricing pressure from global competitors and substitute technologies requires efficiency improvements and value-added services to maintain margins. Profitability concerns arise from the need for continuous innovation and regulatory compliance investments. Balancing investment in advanced technologies with customer affordability is complex, especially for smaller manufacturers. These financial and operational challenges necessitate strategic planning, cost management, and collaborative innovation to sustain market viability.

- •Regulatory compliance constitutes a significant challenge, as bonding system manufacturers must adhere to stringent safety and environmental standards enforced by U.S. agencies. Navigating complex certification processes and ensuring product formulations meet volatile organic compound (VOC) limits increase development timelines and costs. Market players also face standardization issues due to diverse application requirements and lack of uniform testing protocols, complicating product validation. Policy uncertainties related to chemical regulations and trade restrictions add risk to supply chain and market access. These regulatory challenges require proactive engagement with authorities, robust compliance frameworks, and agile product development to mitigate risks and maintain market access.

- •The United States Temporary Bonding and Debonding Systems Market experiences intense competition from numerous domestic and international players, leading to market saturation in key segments. Differentiating products on performance, sustainability, and service quality is challenging amid similar technology offerings. Market saturation also limits growth prospects for established players, prompting the need for innovation and diversification. Supply chain disruptions, including raw material shortages and logistics delays, affect timely delivery and production schedules. Talent shortages in specialized technical roles constrain capacity expansion and service delivery. Infrastructure gaps in emerging manufacturing regions hinder rapid market expansion and customer support. Addressing these competitive and operational challenges requires strategic investments in innovation, partnerships, and workforce development to sustain market leadership.

- •Supply chain complexities arise from dependence on specialized raw materials sourced globally, exposing manufacturers to geopolitical and logistical risks. Talent shortages in adhesive chemistry, equipment engineering, and process integration limit the ability to scale operations and provide technical support. Infrastructure gaps, particularly in emerging manufacturing hubs, affect installation, maintenance, and customer service capabilities. These challenges impact production efficiency, customer satisfaction, and overall market growth. Strategic planning, diversification of suppliers, investment in workforce development, and infrastructure enhancement are necessary to mitigate these risks and support sustainable market development.

Regulatory Framework

- •From 2019 to 2024, the United States Environmental Protection Agency (EPA) has implemented stricter regulations limiting volatile organic compound (VOC) emissions from adhesive and bonding materials, requiring manufacturers to reformulate products to reduce environmental impact while maintaining performance. Compliance with the Toxic Substances Control Act (TSCA) mandates thorough chemical risk assessments and reporting, influencing product development timelines and costs. The Occupational Safety and Health Administration (OSHA) has enhanced workplace safety standards specifically targeting exposure to bonding agents’ chemical components, necessitating improved handling procedures and protective equipment. Additionally, California’s Proposition 65 requires clear labeling of products containing chemicals known to cause cancer or reproductive harm, impacting packaging and marketing practices. These regulatory measures collectively drive innovation toward low-VOC, non-toxic adhesives and reinforce sustainable manufacturing practices within the United States market.

- •Enforcement mechanisms include routine inspections, mandatory reporting, and potential penalties for non-compliance, compelling manufacturers to maintain rigorous quality control and documentation. Stakeholders across the supply chain are required to adapt to evolving standards, fostering collaboration to ensure regulatory adherence. The Food and Drug Administration (FDA) regulations influence bonding materials used in medical device production, mandating biocompatibility and sterilization compatibility. State-level environmental mandates further complicate compliance landscapes, with some states imposing additional restrictions beyond federal requirements. Industry associations actively engage in advocacy and standard-setting to harmonize regulations and promote best practices. Overall, the regulatory framework shapes product innovation, safety profiles, and market access strategies for bonding system providers in the United States.

- •Safety standards such as ANSI and ASTM guidelines provide operational protocols for bonding and debonding equipment, ensuring consistent performance and worker protection. Environmental norms increasingly emphasize lifecycle impacts, encouraging development of recyclable and bio-based adhesives. Operational guidelines for bonding process validation and quality assurance are evolving to accommodate complex substrate materials and manufacturing environments. These standards support industry-wide consistency and facilitate customer confidence in bonding system reliability.

- •State-specific mandates, notably in California, New York, and Washington, include timelines for VOC reductions and restrictions on hazardous air pollutants, requiring phased implementation plans by manufacturers. These regulations influence regional market dynamics and encourage early adoption of compliant technologies. Timelines for compliance vary, with some measures extending into the late 2020s, providing clear regulatory roadmaps for industry planning.

- •Government initiatives such as the U.S. Department of Energy’s support for clean manufacturing and advanced materials R&D provide incentives that indirectly benefit temporary bonding system development by fostering innovation and adoption of sustainable technologies. Programs promoting domestic semiconductor manufacturing and medical device production also create conducive environments for market growth. Industry collaboration with regulatory bodies ensures alignment of technological capabilities with policy objectives, facilitating smoother market entry and expansion.

Market Intelligence

- •15th January 2025, 3M Company launched an advanced thermal release bonding system designed for high-volume semiconductor wafer processing. The new system features proprietary adhesive formulations enabling rapid debonding at precisely controlled temperatures, reducing cycle times by 20% and minimizing substrate damage. Targeted at leading semiconductor fabs in the United States, this solution integrates seamlessly with automated handling equipment and supports wafers down to 3 nm nodes. 3M’s innovation aims to address increasing manufacturing complexities and yield improvement demands, reinforcing its market leadership. The launch is supported by comprehensive technical support and training programs to accelerate customer adoption and optimize process integration. Source: 3M official press release.

- •10th March 2025, Henkel Corporation introduced a new UV-curable adhesive tailored for flexible electronics and medical device assembly applications. The adhesive exhibits rapid curing under low-intensity UV light, enabling delicate substrate bonding with minimal thermal exposure, thereby preserving material integrity. Its bio-based formulation aligns with stringent environmental regulations and corporate sustainability goals. Henkel’s product expansion reflects growing demand in emerging sectors and responds to customer calls for eco-friendly, high-performance bonding solutions. The launch includes collaborative pilot projects with key industry players to customize adhesive properties for specific applications. This development positions Henkel to capitalize on expanding market segments and regulatory trends. Source: Henkel Corporation news update.

- •8th July 2024, Dow Inc. announced a strategic partnership with a leading semiconductor equipment manufacturer to co-develop integrated temporary bonding and debonding systems. The collaboration aims to combine Dow’s advanced adhesive technologies with sophisticated automation equipment to improve process throughput and yield in wafer fabrication. The initiative includes joint R&D efforts, pilot testing in United States fabs, and coordinated marketing strategies. Expected outcomes include enhanced process reliability, reduced operational costs, and accelerated adoption of next-generation bonding solutions. This partnership exemplifies industry trends toward integrated solution offerings and cross-sector collaboration to address complex manufacturing challenges. Source: Dow Inc. corporate announcement.

- •25th November 2024, Avantor, Inc. completed the acquisition of a specialized adhesive materials startup focused on thermal release systems for medical device applications. The acquisition strengthens Avantor’s product portfolio by adding innovative bonding technologies critical for precision assembly and sterilization compatibility. The startup’s proprietary chemistries complement Avantor’s existing offerings, enabling expanded market reach and enhanced R&D capabilities. This strategic move supports Avantor’s growth objectives in the healthcare manufacturing segment and reflects ongoing consolidation trends within the temporary bonding market. Integration plans include scaling manufacturing capacity and leveraging Avantor’s extensive distribution network across the United States. Source: Avantor official press release.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.65 Billion |

| Forecast Year Market Size | USD 1.78 Billion |

| CAGR | 11.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.2% |

| Scope of Report | Market is segmented by Type (Adhesive-Based Systems, Mechanical Clamping Systems, Vacuum-Based Systems, Thermal Release Systems, UV-Curable Systems), Application (Semiconductor Manufacturing, MEMS Fabrication, Display Assembly, Photovoltaic Cells, Medical Device Production), End-User Industry (Electronics Manufacturing, Renewable Energy, Healthcare Equipment, Automotive Electronics), Deployment Model (Automated Systems, Semi-Automated Systems, Manual Systems) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | 3M Company (United States), Henkel Corporation (United States), TOK America, Inc. (United States), Shin-Etsu Chemical Co., Ltd. (Japan), Dow Inc. (United States), Panasonic Corporation (Japan), Asahi Kasei Corporation (Japan), Saint-Gobain Performance Plastics (France), Henkel AG & Co. KGaA (Germany), Nitto Denko Corporation (Japan), E. I. du Pont de Nemours and Company (United States), Fujikura Ltd. (Japan), Hitachi Chemical Co., Ltd. (Japan), LORD Corporation (United States), Avantor, Inc. (United States), Alpha Assembly Solutions (United States), Henkel Loctite (United States), Tesa SE (Germany), Dymax Corporation (United States), Mitsubishi Chemical Corporation (Japan), Solvay S.A. (Belgium), 3M Innovative Properties Company (United States), Adhesives Research, Inc. (United States), Fujifilm Holdings Corporation (Japan), Nippon Electric Glass Co., Ltd. (Japan) |

United States Temporary Bonding and Debonding Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.