EMEA E Beam Liner Market Size, Growth & Revenue 2024-2034

EMEA E Beam Liner Market is segmented by E Beam Liner Type (Standard E Beam Liners, High-Performance E Beam Liners, Customized E Beam Liners, Flexible E Beam Liners, Reinforced E Beam Liners), Application Sector (Automotive, Aerospace, Electronics, Medical Devices, Industrial Manufacturing), Material Composition (Metal-Based Liners, Composite Liners, Polymer-Based Liners, Ceramic-Enhanced Liners), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA)

Pricing

Report Overview

Executive Summary

- •The EMEA E Beam Liner Market comprises advanced electron beam liner technologies used across automotive, aerospace, electronics, medical, and industrial manufacturing sectors. The market scope involves various liner types including standard, high-performance, customized, flexible, and reinforced models designed to enhance surface properties like hardness, corrosion resistance, and wear protection. These liners are critical in extending the lifecycle and performance of components exposed to harsh operational environments. The market is driven by technological innovations, increasing industrial automation, and stringent quality standards within EMEA regions, especially in Germany, France, and the United Kingdom. Growing demand for lightweight, durable materials in aerospace and automotive sectors further propels market expansion. Regulatory frameworks focusing on environmental compliance and safety standards also shape production and application trends. The region's focus on sustainability and material efficiency underpins strategic investments and R&D activities in the E Beam liner market.

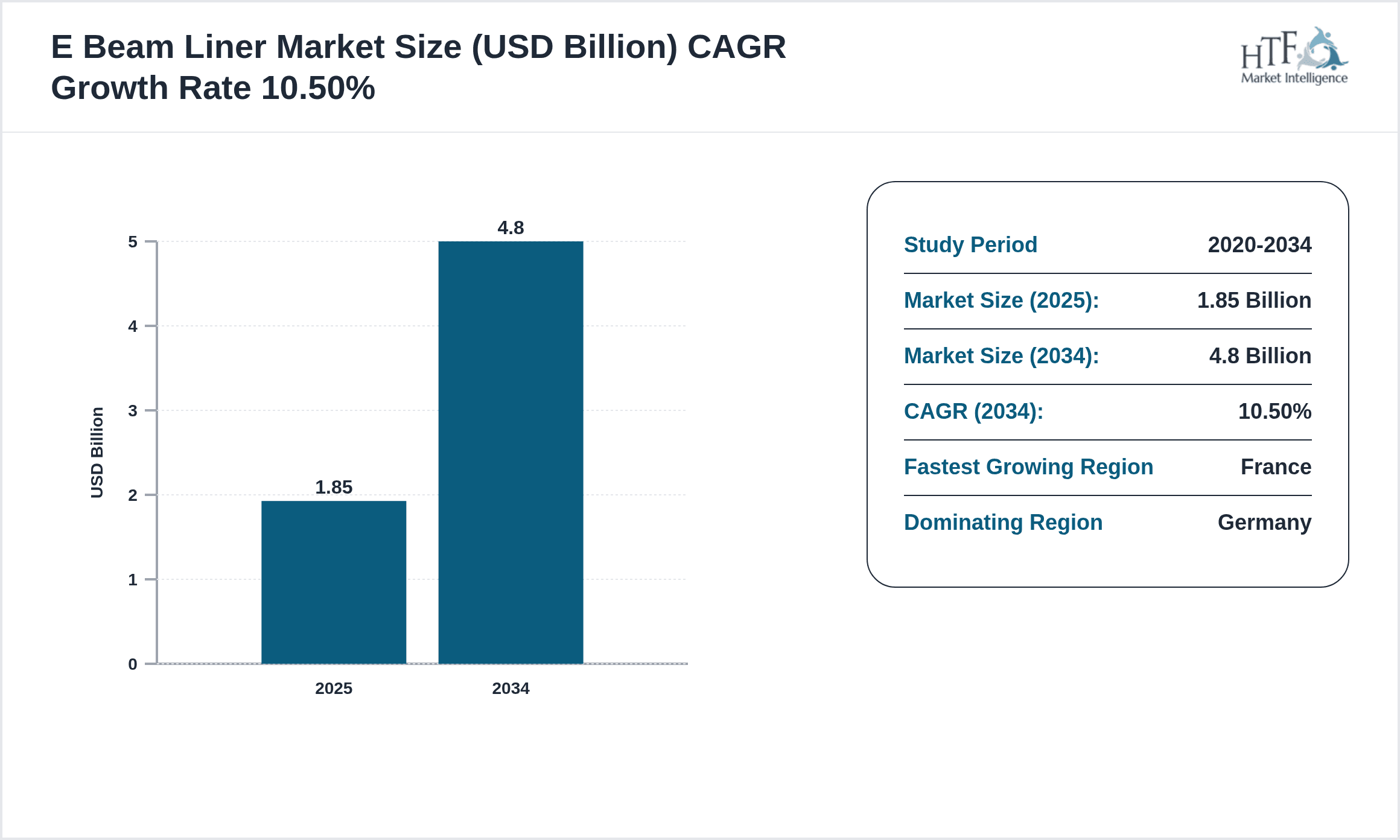

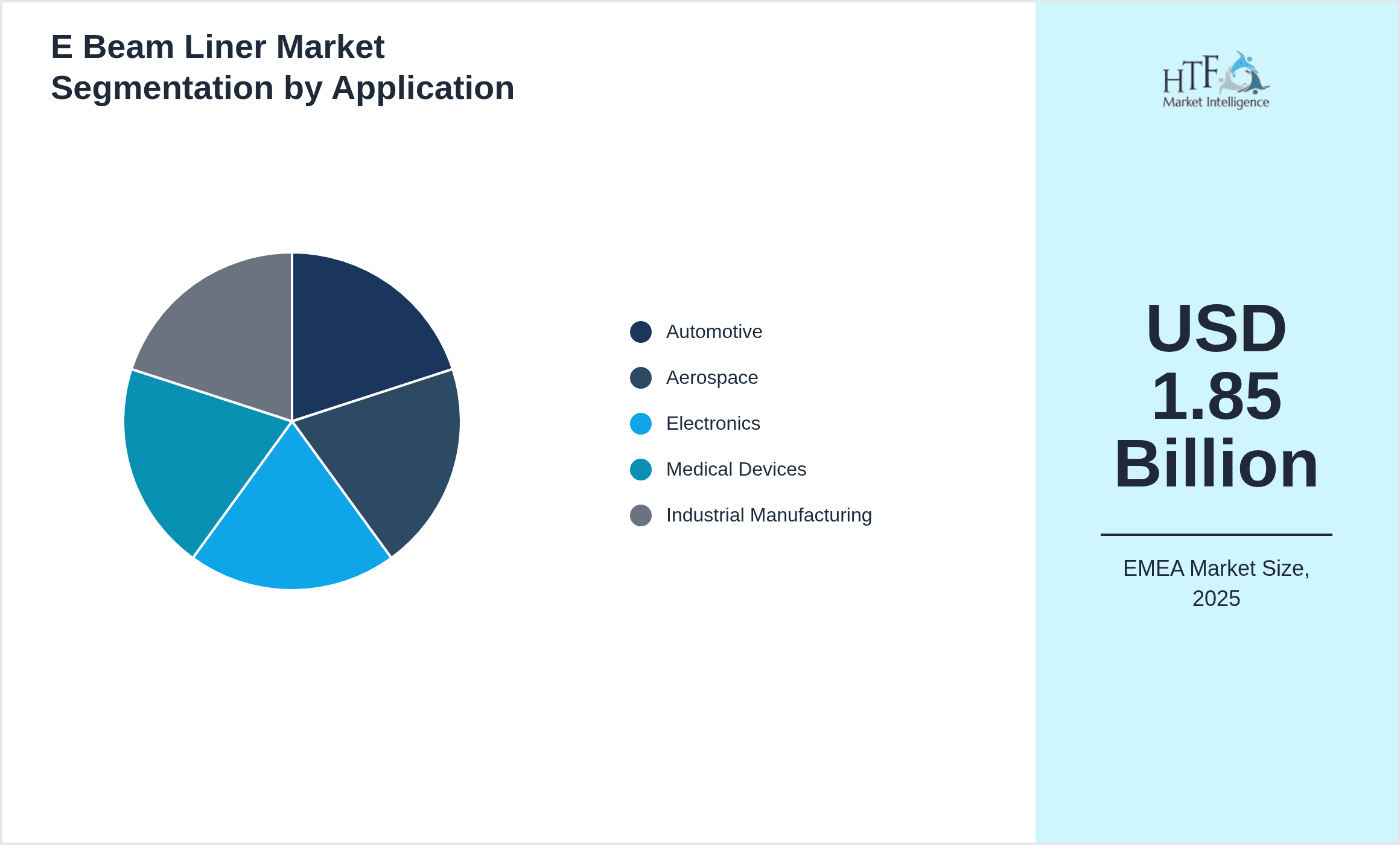

- •Key highlights include a base market size of USD 1.85 Billion in 2024, with forecasts indicating growth to USD 4.8 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 10.5%. Germany dominates the market with a 28% share, while France is the fastest-growing country at a CAGR of 13.2%. High-performance E Beam liners lead the product segment, and flexible E Beam liners exhibit the highest growth potential due to increasing customization needs across industries. The automotive application remains dominant, followed closely by aerospace, supported by rising demand for lightweight and high-strength materials. Year-over-year growth is stable at approximately 10%, showcasing robust market dynamics despite geopolitical and supply chain challenges.

- •The EMEA E Beam Liner Market offers significant value propositions to stakeholders through enhanced product durability, improved operational efficiencies, and compliance with evolving environmental regulations. Manufacturers benefit from innovations in liner materials and customization, enabling penetration into niche industrial applications. The market's strategic importance is underscored by its role in supporting key industries such as automotive and aerospace, which are pivotal for regional economic growth. Continuous investments in R&D, coupled with increasing adoption of electron beam technologies, position the market for sustained expansion, offering lucrative opportunities for equipment providers, material suppliers, and end-users across the EMEA region.

Competitive Landscape

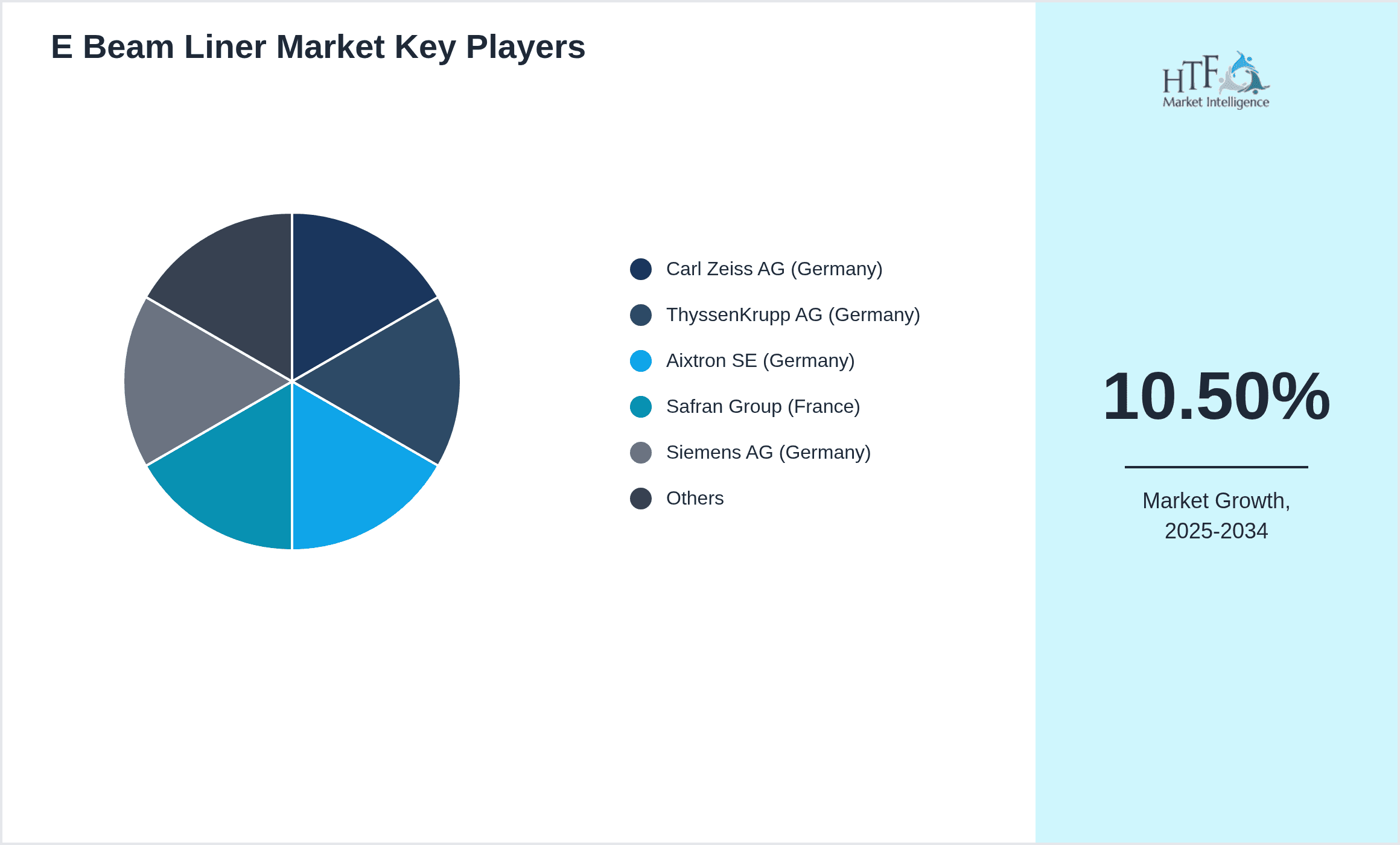

The competitive environment in the EMEA E Beam Liner Market is marked by intense rivalry among established multinational corporations and specialized regional manufacturers. Companies compete on innovation, product quality, and customization capabilities to meet stringent industry standards and diverse application requirements. Strategic partnerships, technology licensing, and collaborative R&D initiatives are common approaches to maintain competitive advantage and expand market shares. Pricing strategies are influenced by raw material costs and technological complexity, while companies invest heavily in product differentiation through advanced coating technologies and sustainable materials. Market entry barriers include high capital investments, regulatory compliance, and the need for technical expertise, which favor incumbents with strong operational capabilities. Regional competition is driven by Germany's industrial base and France's rapid adoption of flexible E Beam liners, while emerging players in Italy and Spain focus on niche applications. Future trends suggest consolidation and strategic alliances will intensify to address evolving market demands and global supply chain challenges.

Leading Companies in E Beam Liner Market

- •Carl Zeiss AG (Germany)

- •ThyssenKrupp AG (Germany)

- •Aixtron SE (Germany)

- •Safran Group (France)

- •Siemens AG (Germany)

- •Rolls-Royce Holdings plc (United Kingdom)

- •Bosch Group (Germany)

- •Valeo SA (France)

- •Alstom SA (France)

- •Renishaw plc (United Kingdom)

- •MTU Aero Engines AG (Germany)

- •ABB Ltd (Switzerland)

- •Fives Group (France)

- •GKN plc (United Kingdom)

- •Schneider Electric SE (France)

- •Eaton Corporation plc (United Kingdom)

- •Thales Group (France)

- •Schott AG (Germany)

- •Danaher Corporation (United Kingdom)

- •Atlas Copco AB (Sweden)

- •Nexans S.A. (France)

- •SKF AB (Sweden)

- •Henkel AG & Co. KGaA (Germany)

- •Leoni AG (Germany)

- •Prysmian Group (Italy)

Market Breakdown

- •By E Beam Liner Type

- ◦Standard E Beam Liners

- ◦High-Performance E Beam Liners

- ◦Customized E Beam Liners

- ◦Flexible E Beam Liners

- ◦Reinforced E Beam Liners

- •By Application Sector

- ◦Automotive

- ◦Aerospace

- ◦Electronics

- ◦Medical Devices

- ◦Industrial Manufacturing

- •By Material Composition

- ◦Metal-Based Liners

- ◦Composite Liners

- ◦Polymer-Based Liners

- ◦Ceramic-Enhanced Liners

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •Increasing industrial automation across EMEA drives demand for advanced E Beam liners that enhance component durability and operational efficiency. For example, automotive manufacturers in Germany invest heavily in high-performance liners to ensure vehicle safety and longevity under rigorous conditions.

- •Technological advancements such as flexible and customized E Beam liners enable tailored solutions for aerospace and electronics sectors, expanding application scopes and addressing complex engineering challenges unique to these industries.

- •Stringent environmental regulations in the European Union promote sustainable manufacturing practices, compelling companies to adopt eco-friendly liner materials and processes that reduce waste and energy consumption.

- •Growing emphasis on lightweight materials in aerospace and automotive applications fuels demand for reinforced and polymer-based E Beam liners, balancing strength with weight reduction to meet performance and emission targets.

- •Rising investments in R&D by key players across France and the United Kingdom spur innovation in liner coatings and electron beam technologies, fostering market growth through improved product offerings and enhanced application versatility.

Market Trends

- •The shift toward flexible E Beam liners reflects a trend in customization and adaptability, enabling manufacturers to meet specific design and operational requirements across diverse industrial applications.

- •Integration of digital monitoring and quality control systems within liner production enhances precision and reduces defects, aligning with Industry 4.0 initiatives prevalent in Germany and other leading EMEA countries.

- •Sustainability continues to shape material choices, with an uptick in the use of composite and polymer-based liners that offer environmental benefits without compromising performance.

- •Collaborations between liner manufacturers and end-user industries such as aerospace drive product innovation and faster adoption of advanced electron beam technologies.

- •Market players increasingly focus on expanding distribution channels through digital platforms, enhancing accessibility and customer engagement in less penetrated EMEA regions.

Market Opportunities

- •The growing aerospace industry in countries like France and the UK presents significant opportunities for customized E Beam liners designed for high-stress and lightweight applications, enabling market expansion.

- •Emerging industrial hubs in Eastern Europe offer untapped markets for standard and reinforced E Beam liners, with potential for strategic partnerships and localized manufacturing facilities.

- •Advancements in polymer and composite liner technologies open avenues for new product development focused on sustainability and performance, appealing to environmentally conscious manufacturers.

- •Increasing adoption of online sales channels and digital marketing facilitates broader customer reach across diverse EMEA territories, creating growth prospects for liner suppliers.

- •Government incentives promoting green manufacturing and innovation in materials science in Germany and France support investment in next-generation E Beam liners, fostering competitive advantage.

Market Challenges

- •High initial capital expenditure for electron beam equipment and liner production limits entry for smaller manufacturers, constraining market competitiveness and innovation diversity.

- •Supply chain disruptions, especially in raw materials like specialized metals and composites, affect timely production and delivery, impacting customer satisfaction and market growth.

- •Complex regulatory compliance across multiple EMEA countries increases operational costs and requires continuous adaptation, posing challenges for manufacturers operating region-wide.

- •Technological complexity and need for skilled workforce hinder rapid adoption of advanced E Beam liner technologies in emerging EMEA markets.

- •Price sensitivity among end-users, particularly in industrial manufacturing sectors, limits willingness to adopt premium liner products despite their long-term benefits.

Regulatory Framework

- •Between 2019 and 2024, the European Union implemented the REACH regulation updates, mandating stricter registration and evaluation of chemical substances used in E Beam liner manufacturing, ensuring safer products and environmental protection.

- •CE marking requirements for electron beam equipment have been reinforced, necessitating compliance with updated safety and performance standards across EMEA countries, impacting production design and quality assurance.

- •Environmental directives focusing on emissions and waste management, such as the Waste Framework Directive, have led to adoption of greener liner materials and production processes within the region.

- •Country-specific mandates in Germany and France include energy efficiency standards for manufacturing facilities, promoting sustainable operations and influencing capital investments in the E Beam liner sector.

- •Government initiatives across EMEA support innovation through grants and subsidies targeting advanced materials and electron beam technologies, encouraging R&D and faster market adoption.

Market Intelligence

- •15th February 2025, Carl Zeiss AG announced the launch of its new high-flexibility E Beam liner designed for aerospace applications, featuring enhanced thermal resistance and customized fit capabilities. This product addresses increasing demand for lightweight, durable coatings in the aviation sector and is expected to strengthen the company’s position in the EMEA market. The launch includes integration with digital monitoring tools to ensure quality and performance during installation, representing a significant technological advancement. The initiative aligns with growing sustainability trends and regulatory requirements across Europe.

- •10th April 2025, Safran Group expanded its manufacturing capacity for reinforced E Beam liners at its France facility, investing USD 50 million to meet rising demand from automotive and aerospace clients. The expansion aims to enhance production efficiency, reduce lead times, and incorporate eco-friendly materials compliant with EU regulations. This strategic move is expected to increase Safran’s market share and accelerate adoption of high-performance liners in key EMEA markets. The company also announced partnerships with regional distributors to strengthen supply chain resilience.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- Italy

- United Kingdom

- Nordics

- Rest of Europe

- South Africa

- Egypt

- Turkey

- United Arab Emirates

- Israel

- Saudi Arabia

- Rest of EMEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 4.8 Billion |

| CAGR | 10.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10% |

| Scope of Report | Market is segmented by E Beam Liner Type (Standard E Beam Liners, High-Performance E Beam Liners, Customized E Beam Liners, Flexible E Beam Liners, Reinforced E Beam Liners), Application Sector (Automotive, Aerospace, Electronics, Medical Devices, Industrial Manufacturing), Material Composition (Metal-Based Liners, Composite Liners, Polymer-Based Liners, Ceramic-Enhanced Liners), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | Germany, France, Italy, United Kingdom, Nordics, Rest of Europe, South Africa, Egypt, Turkey, United Arab Emirates, Israel, Saudi Arabia, Rest of EMEA |

| Key Companies | Carl Zeiss AG (Germany), ThyssenKrupp AG (Germany), Aixtron SE (Germany), Safran Group (France), Siemens AG (Germany), Rolls-Royce Holdings plc (United Kingdom), Bosch Group (Germany), Valeo SA (France), Alstom SA (France), Renishaw plc (United Kingdom), MTU Aero Engines AG (Germany), ABB Ltd (Switzerland), Fives Group (France), GKN plc (United Kingdom), Schneider Electric SE (France), Eaton Corporation plc (United Kingdom), Thales Group (France), Schott AG (Germany), Danaher Corporation (United Kingdom), Atlas Copco AB (Sweden), Nexans S.A. (France), SKF AB (Sweden), Henkel AG & Co. KGaA (Germany), Leoni AG (Germany), Prysmian Group (Italy) |

EMEA E Beam Liner Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.