Japan Industrial Machine Vision Sensors Market Size, Growth & Revenue 2024-2034

Japan Industrial Machine Vision Sensors Market is segmented by Type (2D Vision Sensors, 3D Vision Sensors, Line Scan Cameras, Area Scan Cameras, Time-of-Flight Sensors), Application (Automotive Inspection, Electronics Manufacturing, Food & Beverage Quality Control, Pharmaceuticals, Packaging), End-User Industry (Automotive OEMs, Electronics OEMs, Food Processing Companies, Pharmaceutical Manufacturers, Packaging Companies), Distribution Channel (Direct Sales, Distributors and Resellers, Online Platforms), and Geography (Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu)

Pricing

Report Overview

Executive Summary

- •The Japan Industrial Machine Vision Sensors market is defined by the integration of sophisticated optical sensing technologies designed to enhance automated inspection and quality control across multiple manufacturing industries. It comprises various sensor types including 2D and 3D vision sensors, line scan and area scan cameras, and time-of-flight sensors, each serving specific industrial requirements. The market scope covers applications in automotive inspection, electronics manufacturing, pharmaceutical quality assurance, food and beverage processing, and packaging. These sensors facilitate high-speed data acquisition and image processing to detect defects, measure dimensions, and improve production accuracy. The industry benefits from Japan’s advanced manufacturing infrastructure and a strong focus on innovation in sensor technology and AI integration. Geographically, the market is segmented into regional zones such as Kanto, Kansai, and Kyushu & Okinawa, reflecting localized industrial activities and adoption rates. Strategic initiatives by key players and government support for automation further stimulate market growth through 2034.

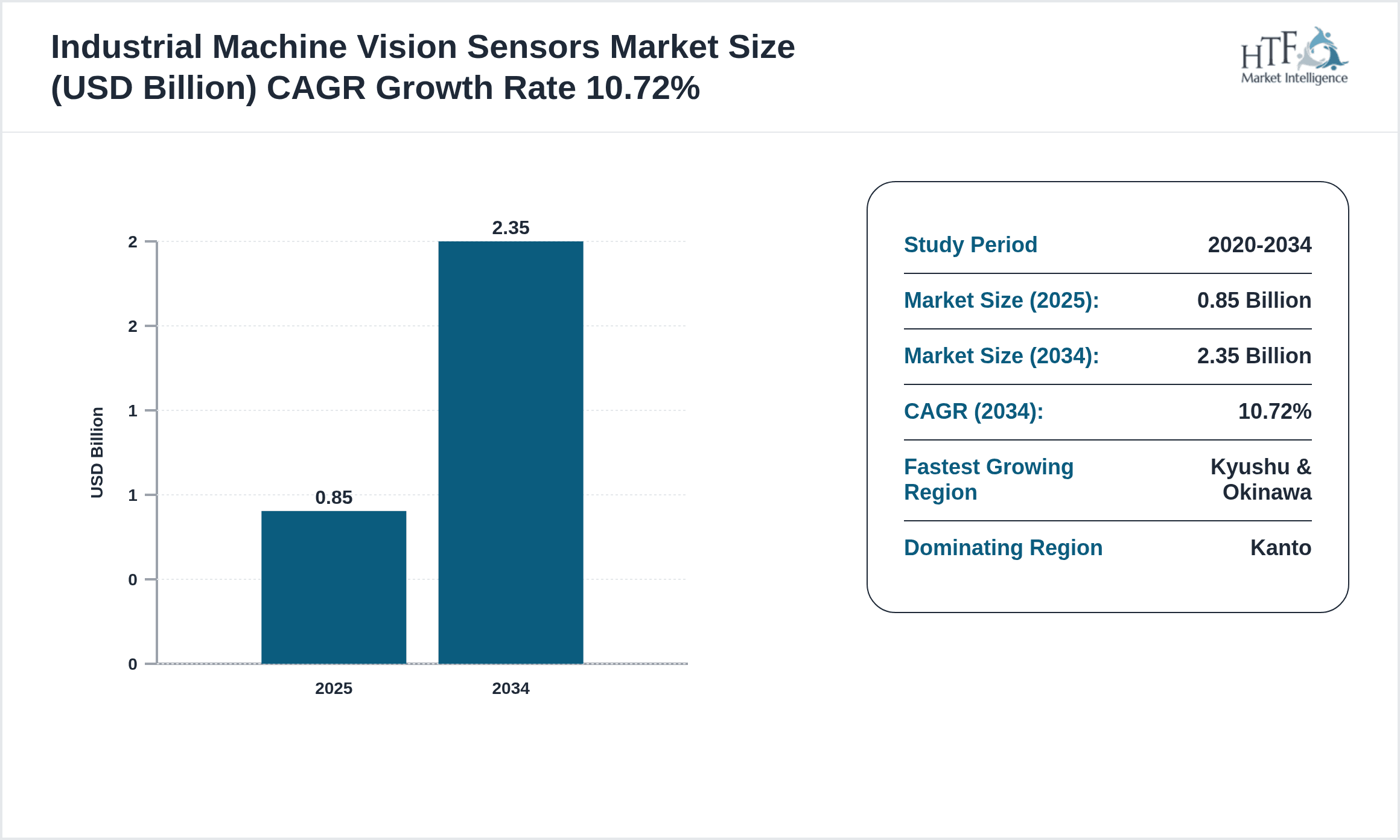

- •Key market highlights include a base market size of USD 0.85 billion in 2024 with projected growth to USD 2.35 billion by 2034, reflecting a robust CAGR of 10.72%. The 2D vision sensors currently dominate the market due to their widespread use in traditional inspection tasks, while 3D vision sensors represent the fastest growing segment owing to increasing demand for precise depth and volume measurements. The Kanto region leads with 35% market share, driven by its concentration of automotive and electronics manufacturing hubs. Kyushu & Okinawa is the fastest growing regional zone, exhibiting a CAGR of 14.5% attributed to rising investments in industrial modernization. Emerging trends include AI-powered image analysis, integration with Industry 4.0 systems, and the adoption of time-of-flight sensors for complex applications.

- •The market offers significant value propositions by enhancing manufacturing efficiency, reducing defect rates, and enabling real-time quality monitoring. These improvements translate into cost savings and higher product standards, critical for Japan’s competitive export-driven industries. The strategic importance of this market spans automotive OEMs, electronics manufacturers, pharmaceutical companies, and food processors who rely on precision and compliance with stringent quality norms. Stakeholders including sensor manufacturers, system integrators, and end-users are collaborating to drive innovation and expand deployment. Continuous advancements in sensor miniaturization, AI integration, and data analytics are expected to reshape production lines, fostering smart factories and sustainable industrial growth across Japan’s diverse regional zones.

Competitive Landscape

The competitive environment within the Japan Industrial Machine Vision Sensors market is marked by intense rivalry among global leaders and domestic innovators striving to deliver cutting-edge sensor technologies and integrated solutions. Companies differentiate themselves through continuous investment in research and development, focusing on enhancing sensor accuracy, speed, and AI-enabled analytics. Strategic partnerships and collaborations with system integrators and manufacturing enterprises are common to expand market reach and tailor solutions to specific industry needs. Pricing strategies and product customization also play a crucial role in gaining competitive advantage. The market features a mix of established multinational corporations and agile Japanese firms leveraging local expertise and strong customer relationships. Mergers and acquisitions have become a key strategy to consolidate technology portfolios and enhance scale. Additionally, regulatory compliance and adherence to quality standards present barriers to entry, reinforcing the competitive positioning of established players. Innovation cycles and technology adoption rates drive future competition dynamics and market leadership.

Prominent Players in Japan Industrial Machine Vision Sensors Market

- •Keyence Corporation (Japan)

- •Omron Corporation (Japan)

- •Panasonic Corporation (Japan)

- •Sony Corporation (Japan)

- •Cognex Corporation (United States)

- •Basler AG (Germany)

- •Teledyne Technologies Incorporated (United States)

- •Datalogic S.p.A. (Italy)

- •JAI A/S (Denmark)

- •Sick AG (Germany)

- •Hitachi, Ltd. (Japan)

- •Toshiba Corporation (Japan)

- •Fujifilm Corporation (Japan)

- •Mitsubishi Electric Corporation (Japan)

- •Sony Semiconductor Solutions Corporation (Japan)

- •Hamamatsu Photonics K.K. (Japan)

- •National Instruments Corporation (United States)

- •IDS Imaging Development Systems GmbH (Germany)

- •LUCID Vision Labs Inc. (Canada)

- •Baumer Group (Switzerland)

- •FLIR Systems, Inc. (United States)

- •Allied Vision Technologies GmbH (Germany)

- •Omnivision Technologies, Inc. (United States)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Canon Inc. (Japan)

Market Breakdown

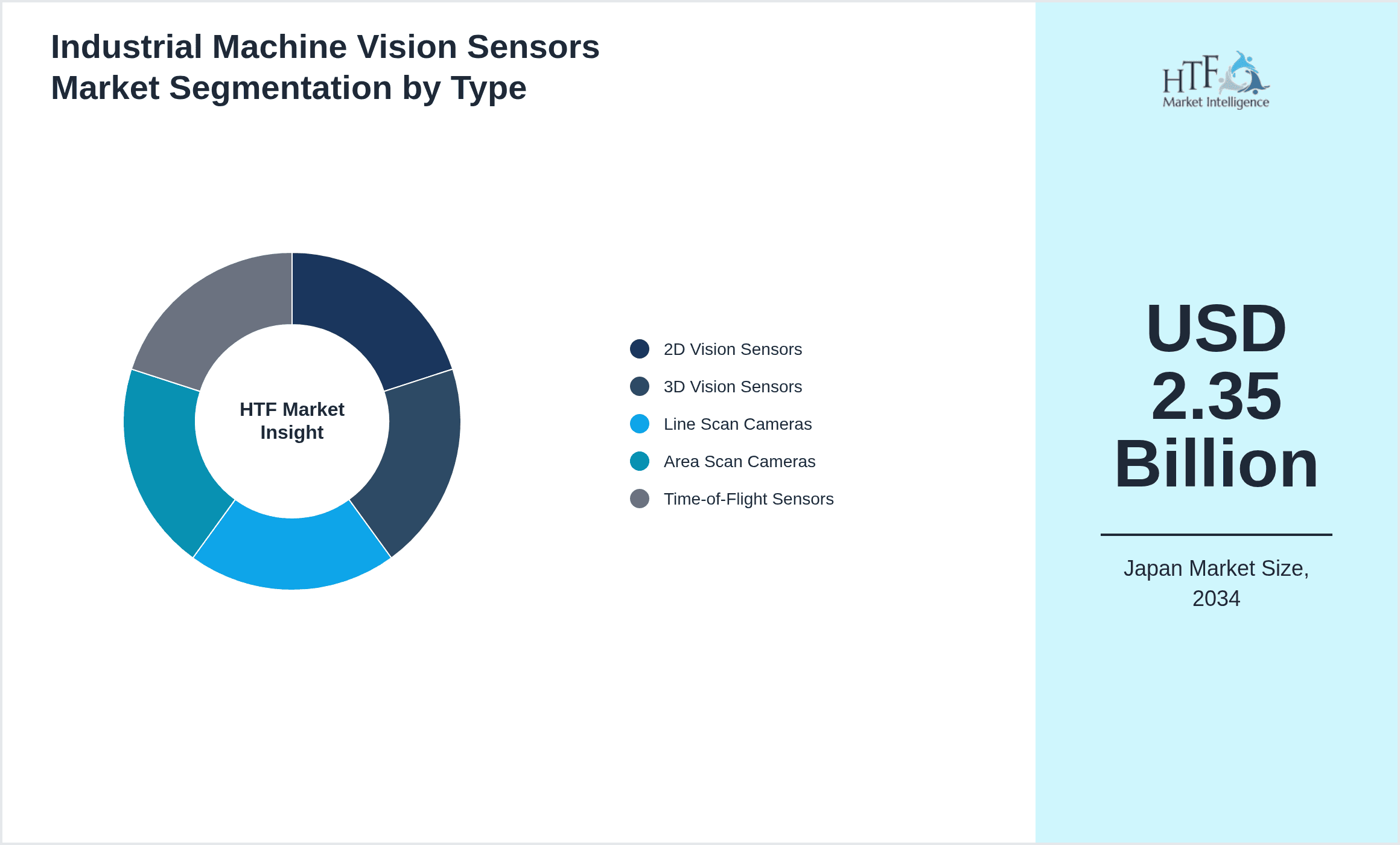

- •By Type

- ◦2D Vision Sensors

- ◦3D Vision Sensors

- ◦Line Scan Cameras

- ◦Area Scan Cameras

- ◦Time-of-Flight Sensors

- •By Application

- ◦Automotive Inspection

- ◦Electronics Manufacturing

- ◦Food & Beverage Quality Control

- ◦Pharmaceuticals

- ◦Packaging

- •By End-User Industry

- ◦Automotive OEMs

- ◦Electronics OEMs

- ◦Food Processing Companies

- ◦Pharmaceutical Manufacturers

- ◦Packaging Companies

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Resellers

- ◦Online Platforms

Growth Dynamics

The Japan Industrial Machine Vision Sensors market is propelled by increasing automation across manufacturing sectors, particularly in automotive and electronics industries. The demand for higher precision and faster inspection processes accelerates adoption of advanced vision sensors, enhancing quality control and reducing production costs. Government initiatives promoting Industry 4.0 and smart factories further stimulate investments in machine vision technologies. Additionally, technological advancements such as AI integration and 3D sensing capabilities expand application possibilities, driving market growth. Companies are also focusing on miniaturization and multi-functionality to meet compact manufacturing needs. The rising trend of predictive maintenance using vision sensors contributes to operational efficiency, while growing exports from Japan’s manufacturing hubs create international demand. Collectively, these factors sustain a strong growth trajectory projected through 2034.

Market Trends

Recent trends in the Japan Industrial Machine Vision Sensors market include the increasing adoption of AI-powered image analysis to enhance defect detection accuracy and reduce false positives. Manufacturers are integrating machine learning algorithms with sensor data to enable predictive quality control. The rise of 3D vision sensors is notable, as they provide detailed spatial information critical for complex assembly processes. There is also a shift towards compact and energy-efficient sensor designs suitable for space-constrained production lines. Furthermore, collaborations between sensor manufacturers and system integrators are becoming common to offer end-to-end vision solutions. Sustainability and digital twin technologies are influencing sensor development to support eco-friendly and virtual manufacturing environments.

Market Opportunities

The Japan market presents significant opportunities for expansion of 3D vision sensors in emerging industries such as robotics and medical device manufacturing. Untapped segments like food safety inspection and pharmaceutical packaging offer potential for customized sensor solutions. Integration of vision sensors with IoT and cloud platforms can unlock new service models including remote monitoring and analytics. Additionally, regional zones like Kyushu & Okinawa show high growth potential due to increasing industrial investments and government support. Strategic partnerships aimed at developing AI-enabled vision systems and tailored solutions for automotive and electronics sectors can enhance market penetration. Innovation in low-cost, high-performance sensors targeting small and medium enterprises represents another growth avenue. Furthermore, increased demand for real-time quality control in high-value exports drives continuous market expansion.

Market Challenges

Despite strong growth prospects, the Japan Industrial Machine Vision Sensors market faces challenges including high initial investment costs which can deter small manufacturers from adoption. Technical complexity in integrating sensors with existing production lines and legacy systems poses barriers requiring specialized expertise. Additionally, evolving industry standards and regulatory compliance necessitate continuous updates to sensor technology, increasing development costs. Supply chain disruptions, particularly for semiconductor components, can impact sensor availability and pricing. The need for skilled workforce capable of managing advanced sensor systems remains a concern. Furthermore, competition from low-cost imports challenges domestic manufacturers’ market share. Data security and privacy issues related to image data collection and processing also require attention to maintain trust and regulatory adherence.

Regulatory Framework

From 2019 to 2024, Japan has implemented several regulations impacting the Industrial Machine Vision Sensors market, focusing on product safety, electromagnetic compatibility, and environmental standards. The Electrical Appliance and Material Safety Law mandates stringent testing and certification for electronic components, including vision sensors, ensuring reliability and user safety. The Act on the Rational Use of Energy promotes energy-efficient sensor designs, encouraging manufacturers to innovate for lower power consumption. Additionally, Japan’s Ministry of Economy, Trade and Industry (METI) has introduced guidelines supporting Industry 4.0 adoption, which include standards for interoperability and data security in sensor integration. Compliance with international standards such as ISO 13849 for functional safety is also enforced, impacting sensor development cycles. These regulatory frameworks drive technological advancements while safeguarding industrial and consumer interests, shaping market growth trajectories.

Market Intelligence

- •15th March 2024, Keyence Corporation launched its latest 3D vision sensor system designed to enhance automotive assembly line inspections with improved depth accuracy and faster processing speeds. The system integrates AI-based defect recognition and offers seamless compatibility with existing factory automation platforms, aiming to reduce downtime and enhance quality assurance. This product targets Japan’s growing automotive manufacturing sector, emphasizing scalability and ease of integration. With this launch, Keyence strengthens its leadership position in the Japan Industrial Machine Vision Sensors market and supports smart factory initiatives. Source: Official Keyence press release

- •10th November 2023, Omron Corporation introduced an innovative line scan camera featuring ultra-high-speed imaging and advanced noise reduction technology tailored for electronics manufacturing inspections. The camera enhances detection of microscopic defects and supports real-time data analytics through cloud connectivity. Omron’s strategic focus on integrating AI algorithms with vision sensors aligns with Japan’s Industry 4.0 roadmap, facilitating smarter production lines and quality control. This launch reflects growing demand for precise and efficient vision solutions in compact electronics manufacturing environments. Source: Omron corporate announcement

- •20th July 2023, Panasonic Corporation announced a strategic partnership with a leading AI software provider to co-develop intelligent vision sensor platforms. The collaboration aims to combine Panasonic’s hardware expertise with advanced AI capabilities to accelerate adoption of automated inspection systems in food and pharmaceutical sectors. This initiative supports product traceability, compliance with safety standards, and operational efficiency improvements across Japan’s manufacturing landscape. The partnership underscores the importance of cross-industry collaboration to foster innovation and market growth. Source: Panasonic official news

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Kanto currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Kyushu & Okinawa is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Hokkaido

- Tohoku

- Kanto

- Chubu

- Kansai

- Chugoku

- Shikoku

- Kyushu

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.85 Billion |

| Forecast Year Market Size | USD 2.35 Billion |

| CAGR | 10.72% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.23% |

| Scope of Report | Market is segmented by Type (2D Vision Sensors, 3D Vision Sensors, Line Scan Cameras, Area Scan Cameras, Time-of-Flight Sensors), Application (Automotive Inspection, Electronics Manufacturing, Food & Beverage Quality Control, Pharmaceuticals, Packaging), End-User Industry (Automotive OEMs, Electronics OEMs, Food Processing Companies, Pharmaceutical Manufacturers, Packaging Companies), Distribution Channel (Direct Sales, Distributors and Resellers, Online Platforms) |

| Regions Covered | Hokkaido, Tohoku, Kanto, Chubu, Kansai, Chugoku, Shikoku, Kyushu |

| Key Companies | Keyence Corporation (Japan), Omron Corporation (Japan), Panasonic Corporation (Japan), Sony Corporation (Japan), Cognex Corporation (United States), Basler AG (Germany), Teledyne Technologies Incorporated (United States), Datalogic S.p.A. (Italy), JAI A/S (Denmark), Sick AG (Germany), Hitachi, Ltd. (Japan), Toshiba Corporation (Japan), Fujifilm Corporation (Japan), Mitsubishi Electric Corporation (Japan), Sony Semiconductor Solutions Corporation (Japan), Hamamatsu Photonics K.K. (Japan), National Instruments Corporation (United States), IDS Imaging Development Systems GmbH (Germany), LUCID Vision Labs Inc. (Canada), Baumer Group (Switzerland), FLIR Systems, Inc. (United States), Allied Vision Technologies GmbH (Germany), Omnivision Technologies, Inc. (United States), Samsung Electronics Co., Ltd. (South Korea), Canon Inc. (Japan) |

Japan Industrial Machine Vision Sensors Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.