Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance Market Size, Growth & Revenue 2025-2034

Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance Market is segmented by Product Type (Engine Components, Airframe Components, Avionics, Landing Gear, Auxiliary Power Units), Application (Commercial Aviation, Military Aviation, General Aviation, Cargo Aviation, Business Aviation), Service Type (Manufacturing, Repair, Maintenance, Overhaul), Regional Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

- •The Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance market is a critical segment of the aerospace industry, focusing on the production and upkeep of vital aircraft components such as engine parts, avionics, landing gear, and airframe structures. This market supports diverse aviation sectors including commercial, military, general, cargo, and business aviation, offering extensive value through manufacturing, repair, overhaul, and maintenance services. The region is witnessing robust growth propelled by increasing air travel demand, fleet expansions, and a growing need for modernization of aging aircraft. Key technological advancements like composite materials, predictive maintenance powered by IoT, and automated repair techniques are enhancing operational efficiencies and component longevity. The value chain integrates OEMs, MRO providers, and aftermarket service operators, each playing a vital role in maintaining aircraft safety and compliance with stringent regulatory frameworks. Market dynamics are also influenced by government investments in aerospace infrastructure, regional defense modernization programs, and international collaborations that foster indigenous manufacturing capabilities. The Asia-Pacific region’s strategic emphasis on enhancing aviation safety, reducing downtime, and optimizing lifecycle costs creates significant opportunities for market players. Furthermore, the market caters to an expanding base of airline operators and military agencies actively upgrading fleets to meet evolving performance and environmental standards. As the aerospace ecosystem matures, the market is expected to benefit from increased innovation, enhanced service offerings, and a growing focus on sustainable practices within aircraft parts manufacturing and maintenance.

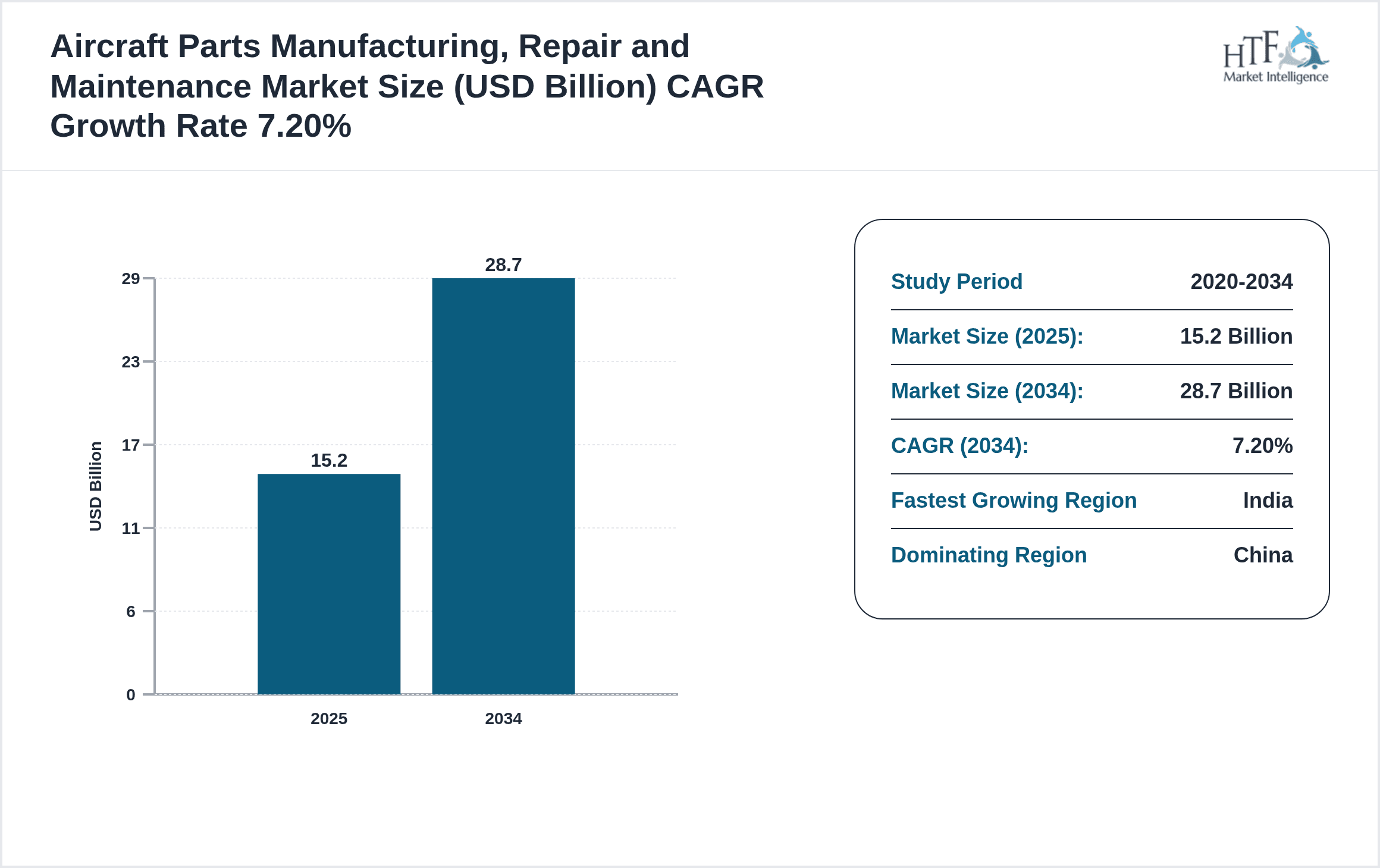

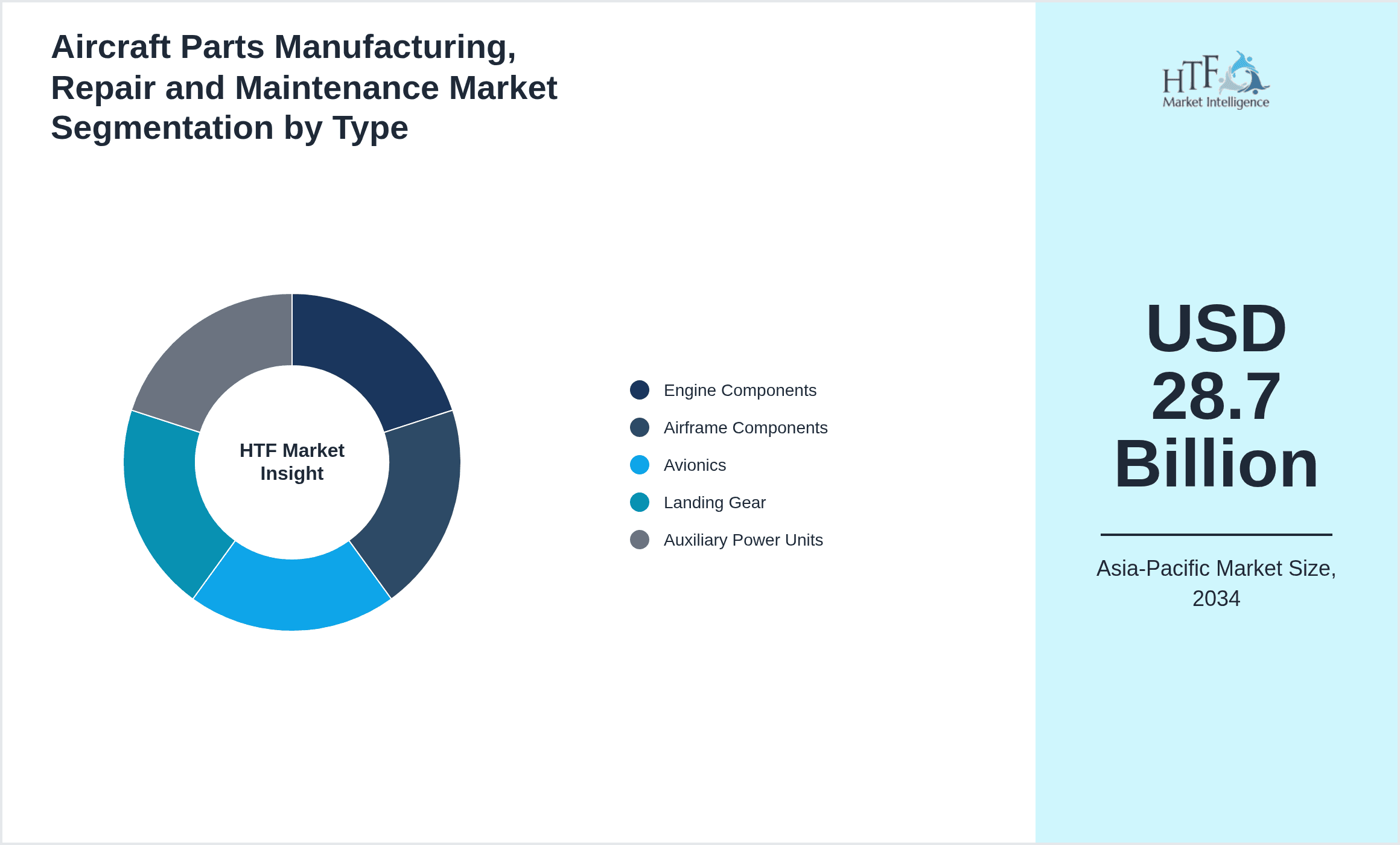

- •Key market highlights include a base market size of USD 15.2 billion in 2025, projected to reach USD 28.7 billion by 2034, representing a CAGR of 7.2%. China dominates the region with a 35% market share, while India emerges as the fastest growing country with a CAGR of 9.5% and an 18% market share. Engine components remain the leading product type due to their critical role in aircraft performance and maintenance schedules, whereas avionics is the fastest growing segment driven by digital transformation and enhanced navigation system requirements. The Asia-Pacific market benefits from expanding commercial aviation fleets, military modernization, and increased demand for cargo and business aviation services, which collectively contribute to sustained growth and diversification of market applications.

- •The Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance market holds strategic importance for aerospace OEMs, MRO providers, airlines, defense agencies, and investors. Its growth is integral to supporting regional aviation safety, operational efficiency, and economic development. The market’s value proposition lies in its ability to deliver high-quality, compliant aircraft components and maintenance services that minimize downtime and extend aircraft lifecycle. Stakeholders benefit from technological advancements, such as predictive maintenance and lightweight material innovations, which reduce costs and environmental impact. Additionally, regional government initiatives aimed at bolstering aerospace manufacturing capabilities and infrastructure development enhance competitiveness. The interplay of rising air traffic, fleet modernization, and evolving regulatory standards creates a dynamic environment fostering innovation and investment. This market report offers critical insights for consultants, investors, and industry leaders to identify growth avenues, mitigate risks, and align strategic initiatives with emerging market trends and regulatory requirements.

Competitive Landscape

The Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance market exhibits a competitive environment characterized by the presence of global aerospace OEMs, regional specialized manufacturers, and a growing number of Maintenance, Repair and Overhaul (MRO) providers. Companies adopt diverse competitive strategies including vertical integration, strategic partnerships, joint ventures, and technology licensing to enhance their market share and operational capabilities. Innovation plays a central role, with players investing heavily in research and development to introduce advanced materials, digital diagnostic tools, and automated repair processes that improve component reliability and reduce maintenance turnaround times. Market positioning is influenced by regional regulatory compliance expertise, cost competitiveness, and the ability to service a wide variety of aircraft types. Mergers and acquisitions are also shaping the competitive landscape by consolidating capabilities and expanding geographic footprints. Pricing strategies often reflect the balance between quality assurance and cost efficiency, with key players leveraging economies of scale and supply chain optimizations. Distribution channels include direct OEM partnerships, authorized service centers, and aftermarket suppliers. Technology adoption includes predictive maintenance, additive manufacturing, and digital twin technologies, providing competitive advantages. Entry barriers remain moderate due to high capital requirements and certification complexities, but government support for domestic aerospace industries fosters new entrants. Regional competition is intensified by emerging aerospace hubs in China, India, Japan, and Southeast Asia. Future competitive trends point toward increasing collaboration between industry and technology firms to accelerate innovation and sustainable manufacturing practices.

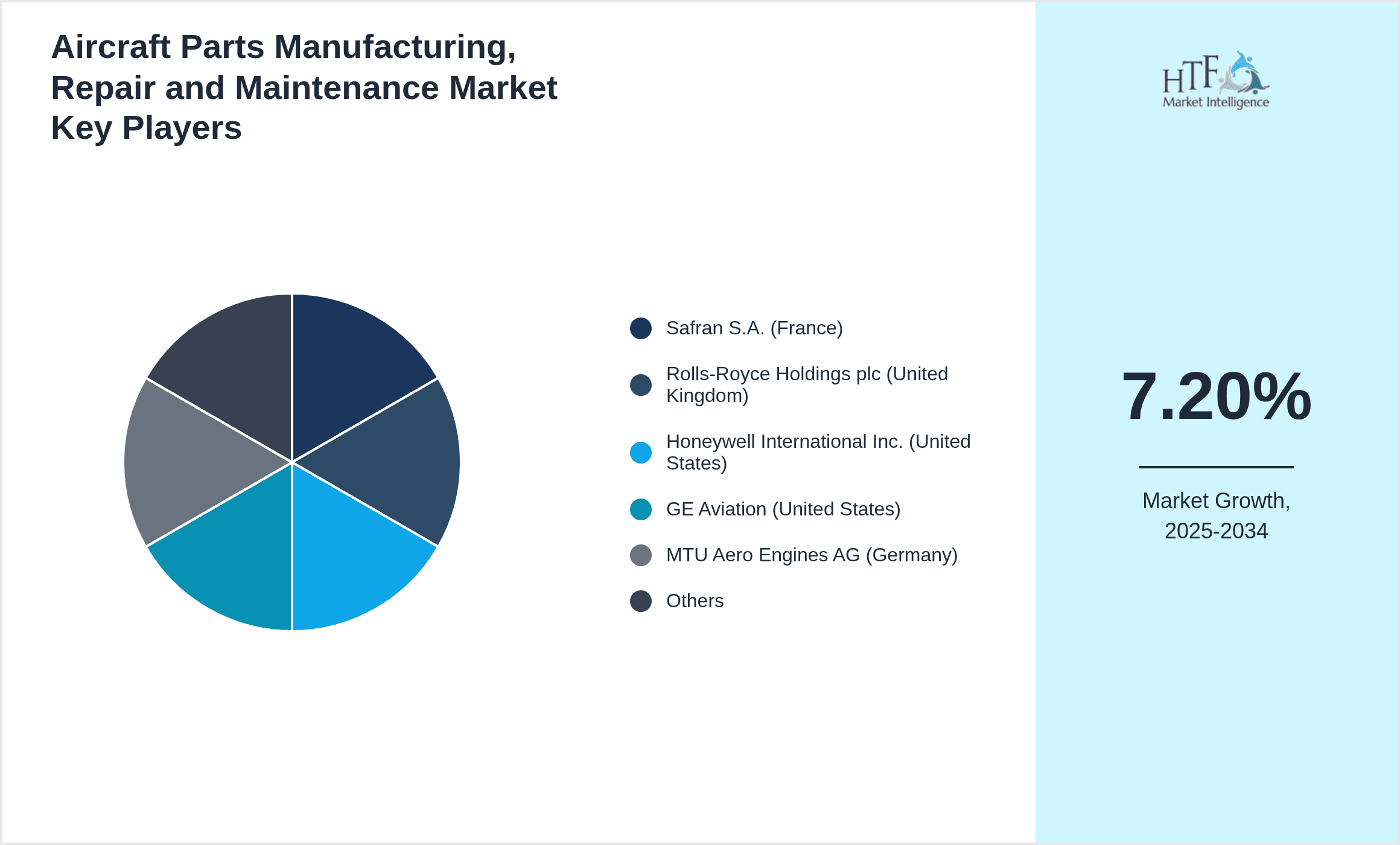

Leading Companies in Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance Market

- •Safran S.A. (France)

- •Rolls-Royce Holdings plc (United Kingdom)

- •Honeywell International Inc. (United States)

- •GE Aviation (United States)

- •MTU Aero Engines AG (Germany)

- •ST Engineering Aerospace Ltd (Singapore)

- •Korean Air Aerospace Division (South Korea)

- •Tata Advanced Systems Limited (India)

- •Mitsubishi Heavy Industries, Ltd. (Japan)

- •China Aviation Industry Corporation (China)

- •AVIC International Holdings Limited (China)

- •SIA Engineering Company Limited (Singapore)

- •Hindustan Aeronautics Limited (India)

- •Boeing India Private Limited (India)

- •Airbus Operations (India) Private Limited (India)

- •Fuji Heavy Industries Ltd. (Japan)

- •China Southern Airlines Co., Ltd. (China)

- •China Eastern Airlines Corporation Limited (China)

- •Singapore Technologies Engineering Ltd (Singapore)

- •Sumitomo Precision Products Co., Ltd. (Japan)

- •Hafei Aviation Industry Co., Ltd. (China)

- •Bharat Electronics Limited (India)

- •Kawasaki Heavy Industries, Ltd. (Japan)

- •Bombardier Aerospace (Canada)

- •ATR Aircraft Manufacturing S.A. (France)

Market Breakdown

- •By Product Type

- ◦Engine Components

- ◦Airframe Components

- ◦Avionics

- ◦Landing Gear

- ◦Auxiliary Power Units

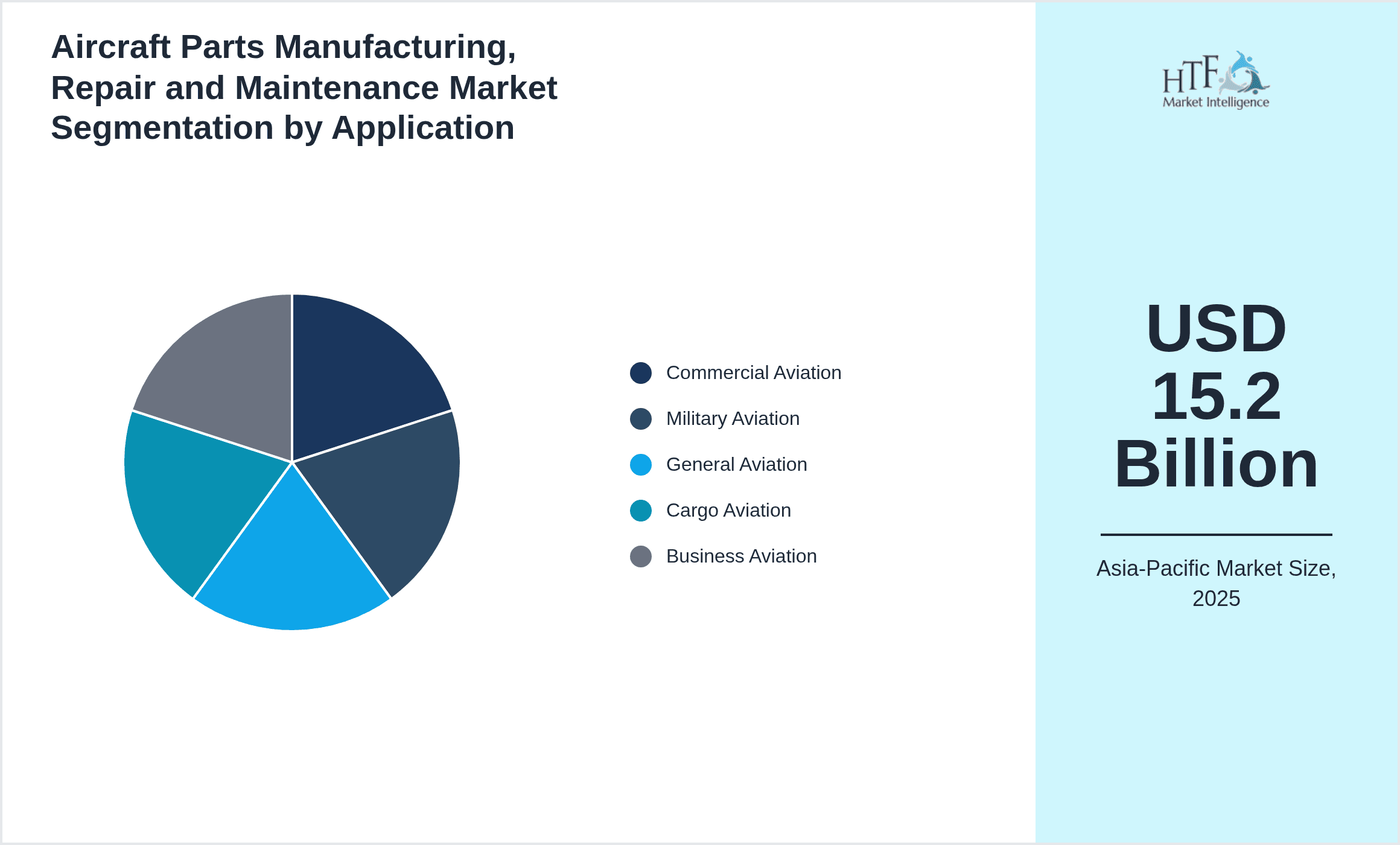

- •By Application

- ◦Commercial Aviation

- ◦Military Aviation

- ◦General Aviation

- ◦Cargo Aviation

- ◦Business Aviation

- •By Service Type

- ◦Manufacturing

- ◦Repair

- ◦Maintenance

- ◦Overhaul

- •By Regional Geography

- ◦Japan

- ◦China

- ◦Southeast Asia

- ◦India

- ◦Australia

- ◦South Korea

- ◦Others

Growth Dynamics

- •The growth of the Asia-Pacific aircraft parts manufacturing, repair, and maintenance market is driven by the rapid expansion of commercial aviation fleets, particularly in China and India, which are investing heavily in new aircraft and replacing aging fleets. This expansion increases demand for high-quality parts and maintenance services to ensure fleet reliability and safety.

- •Increasing defense expenditure and modernization programs across Asia-Pacific countries such as India, Japan, and South Korea are fueling demand for military aircraft parts manufacturing and advanced repair capabilities, creating robust growth opportunities in the military aviation segment.

- •Technological advancements such as the adoption of digital twin technology, predictive maintenance using IoT sensors, and the use of lightweight composite materials are improving operational efficiencies and component lifespan, thereby driving market growth and reducing lifecycle costs.

- •Government initiatives and policies aimed at expanding aerospace manufacturing capacities, including ‘Make in India’ and China’s aerospace industrial strategies, support domestic production capabilities and attract foreign investments, amplifying market growth potential.

- •Rising demand for cargo and business aviation sectors due to e-commerce growth and increasing regional business travel is stimulating demand for customized parts and specialized maintenance services, contributing to market expansion.

- •The regional emphasis on environmental sustainability is promoting the development of eco-friendly manufacturing processes and green maintenance technologies, encouraging innovation and market differentiation among players.

- •Collaborations between aerospace companies and technology firms are accelerating innovation in repair techniques and manufacturing automation, further enhancing the market’s growth trajectory.

Market Trends

- •There is a significant shift towards digitalization in aircraft parts manufacturing and maintenance, with increased adoption of Industry 4.0 technologies such as AI-driven predictive analytics, 3D printing, and robotics to enhance precision and reduce turnaround times.

- •The market is witnessing increasing integration of lightweight composite materials in manufacturing, which improves fuel efficiency and reduces aircraft weight, driving demand for advanced repair methodologies adapted to these new materials.

- •Regional aerospace hubs in China, India, and Southeast Asia are expanding their capabilities through public-private partnerships and government support, positioning Asia-Pacific as a global center for aircraft parts production and MRO services.

- •The rise in outsourcing of MRO services to third-party providers in Asia-Pacific is creating competitive advantages through cost savings and expertise specialization, particularly in countries like Singapore and Malaysia.

- •Sustainability trends are influencing market practices, with players adopting energy-efficient manufacturing processes and prioritizing the recycling of aircraft parts to comply with evolving environmental regulations.

- •Emerging trends include the increased use of augmented reality (AR) and virtual reality (VR) technologies for training maintenance personnel and facilitating complex repair operations, improving service quality and safety.

- •The development of electric and hybrid aircraft is prompting innovation in parts manufacturing and maintenance, creating new sub-segments and altering traditional supply chains.

Market Opportunities

- •Expansion of indigenous aerospace manufacturing capabilities in emerging economies like India and Indonesia offers significant growth opportunities by reducing dependency on imports and supporting local supply chains.

- •Advancements in additive manufacturing (3D printing) present opportunities for cost-effective production of complex aircraft parts, enabling rapid prototyping and on-demand repairs, thus reducing inventory costs.

- •Growing demand for MRO services due to increasing aircraft fleet sizes and aging aircraft in the region creates opportunities for service providers to expand their offerings and geographic presence.

- •Strategic partnerships between aerospace manufacturers and technology companies to co-develop smart maintenance solutions and digital platforms can unlock new revenue streams and improve operational efficiencies.

- •Government incentives and funding programs designed to foster aerospace innovation and infrastructure development provide a conducive environment for investment and capacity building.

- •The rise of regional cargo and logistics sectors driven by e-commerce growth opens new application segments for specialized aircraft parts and maintenance services tailored for cargo aircraft fleets.

- •Sustainability-focused product development, including eco-friendly materials and energy-efficient parts, presents opportunities for differentiation and compliance with tightening environmental regulations.

Market Challenges

- •The high capital investment and stringent certification requirements for manufacturing aircraft parts pose significant barriers for new entrants and smaller players, limiting market competition.

- •Complexity in supply chain management caused by reliance on multiple suppliers and global logistics challenges can lead to delays and increased costs in parts availability and maintenance schedules.

- •Skilled labor shortages, particularly in advanced manufacturing and specialized maintenance skills, hinder operational efficiency and growth potential across the region.

- •Regulatory compliance across diverse countries within Asia-Pacific, each with distinct aviation authorities and standards, creates challenges for uniform market operations and increases administrative burdens.

- •Fluctuations in raw material prices, especially for aerospace-grade metals and composites, impact manufacturing costs and profitability, affecting pricing strategies for parts and services.

- •Geopolitical tensions and trade restrictions may disrupt cross-border collaborations and supply chains, posing risks to market stability and expansion plans.

- •Rapid technological changes require continuous investment in R&D and workforce training, which could strain financial resources, particularly for mid-sized companies.

Regulatory Framework

- •From 2020 to 2025, the Asia-Pacific aircraft parts market has been influenced by the implementation of the Regional Aviation Safety Group (RASG) initiatives which emphasize enhanced safety management systems and harmonization of maintenance standards across member countries, facilitating more consistent regulatory compliance.

- •China’s Civil Aviation Administration (CAAC) updated its Airworthiness Certification regulations in 2022, imposing stricter certification procedures for aircraft components and mandating periodic audits of manufacturing and MRO facilities, thereby elevating product quality and safety benchmarks.

- •India’s Directorate General of Civil Aviation (DGCA) enacted new guidelines in 2023 mandating the adoption of digital recordkeeping and traceability for aircraft parts and maintenance activities, improving transparency and regulatory oversight.

- •Japan’s Ministry of Land, Infrastructure, Transport and Tourism (MLIT) introduced environmental compliance standards in 2024 requiring aerospace manufacturers to implement sustainable production processes and reduce hazardous waste, aligning with global environmental norms.

- •Across Southeast Asia, the ASEAN Aviation Safety and Security Network (AASSN) has strengthened cross-border collaboration efforts since 2021, promoting mutual recognition of certifications and facilitating smoother parts and maintenance service trade within member countries.

Market Intelligence

- •15th February 2025, ST Engineering Aerospace Ltd announced the launch of a new digitally integrated maintenance platform designed to leverage AI and IoT technologies for predictive aircraft parts diagnostics and real-time maintenance scheduling. This initiative aims to reduce downtime and enhance operational efficiency across commercial and military aviation clients in Asia-Pacific. The platform integrates advanced data analytics to optimize parts lifecycle management and supports compliance with evolving aviation safety regulations, positioning ST Engineering as a technology leader in the regional MRO market. Source: Official ST Engineering Press Release

- •10th April 2025, Tata Advanced Systems Limited unveiled its new state-of-the-art aircraft parts manufacturing facility in Hyderabad, India, dedicated to producing advanced avionics and engine components. This expansion is part of India’s ‘Make in India’ aerospace initiative to boost indigenous production capabilities and reduce reliance on imports. Equipped with additive manufacturing technologies and precision machining centers, the facility is expected to increase production capacity by 40% and support domestic and export markets. Source: Tata Advanced Systems Corporate News

- •22nd June 2024, Mitsubishi Heavy Industries completed a strategic partnership with a Japanese AI technology company to develop automated inspection systems for aircraft landing gear components. This collaboration aims to enhance defect detection accuracy and reduce manual inspection times, improving safety and maintenance turnaround. The initiative supports Japan’s aerospace sector’s move toward Industry 4.0 integration and will be piloted in commercial aviation maintenance centers across Asia-Pacific. Source: Mitsubishi Heavy Industries Annual Report 2024

- •5th September 2024, China Aviation Industry Corporation (AVIC) announced its acquisition of a Singapore-based MRO provider specialized in engine overhaul services. This acquisition strengthens AVIC’s service network in Southeast Asia and expands its capabilities in advanced engine maintenance and repair, catering to growing demand from regional commercial airlines. The consolidation is expected to improve AVIC’s competitive position and accelerate its growth in the Asia-Pacific aircraft parts aftermarket sector. Source: AVIC Official Press Release

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 15.2 Billion |

| Forecast Year Market Size | USD 28.7 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (Engine Components, Airframe Components, Avionics, Landing Gear, Auxiliary Power Units), Application (Commercial Aviation, Military Aviation, General Aviation, Cargo Aviation, Business Aviation), Service Type (Manufacturing, Repair, Maintenance, Overhaul), Regional Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others) |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | Safran S.A. (France), Rolls-Royce Holdings plc (United Kingdom), Honeywell International Inc. (United States), GE Aviation (United States), MTU Aero Engines AG (Germany) |

Asia-Pacific Aircraft Parts Manufacturing, Repair and Maintenance Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.