Australia Automotive Embedded Non-Volatile Memory Market Size, Growth & Revenue 2025-2034

Australia Automotive Embedded Non-Volatile Memory Market is segmented by Memory Type (NOR Flash Memory, NAND Flash Memory, EEPROM, Ferroelectric RAM (FeRAM), Magnetoresistive RAM (MRAM)), Automotive Application (Engine Control Units (ECUs), Infotainment Systems, Advanced Driver Assistance Systems (ADAS), Body Electronics, Powertrain Control Modules), Deployment Model (OEM Embedded Solutions, Aftermarket Embedded Solutions, Tier 1 Supplier Embedded Solutions), Packaging Type (Chip-On-Board (COB), Plastic Leaded Chip Carrier (PLCC), Ball Grid Array (BGA), Dual In-line Package (DIP)), and Geography (New South Wales, Queensland, TASMANIA, Victoria, Western Australia, South Australia)

Pricing

Report Overview

Executive Summary

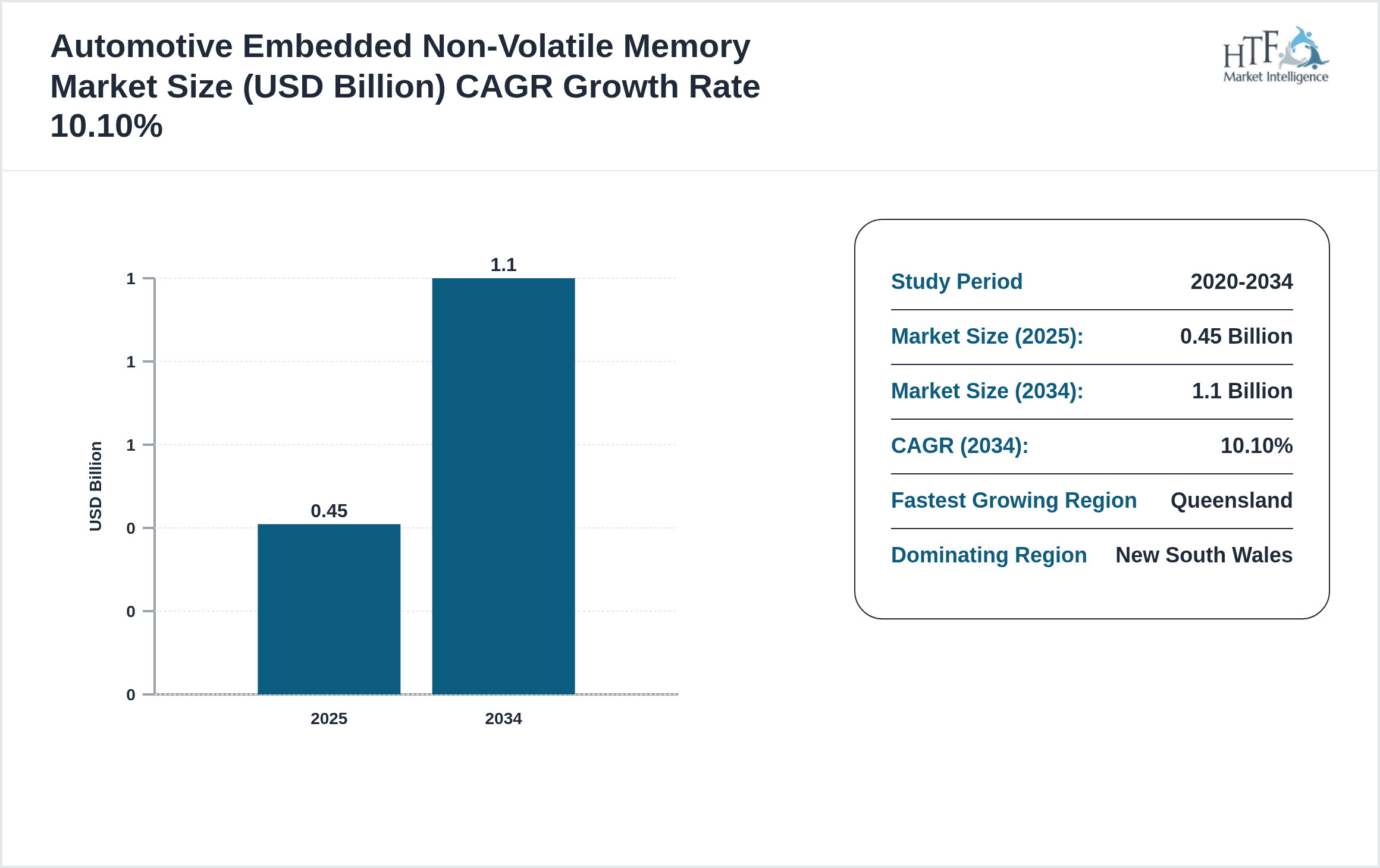

- •The Australia Automotive Embedded Non-Volatile Memory market is focused on memory technologies integrated into automotive electronic systems to provide persistent storage solutions essential for vehicle operation and smart functionalities. This market includes memory types such as NOR Flash, NAND Flash, EEPROM, Ferroelectric RAM, and Magnetoresistive RAM, which serve various roles across applications like engine control units, infotainment, advanced driver assistance systems, body electronics, and powertrain control. Embedded memories support critical automotive needs including data retention under harsh conditions, fast access speeds, reliability, and endurance, crucial for enhancing vehicle safety, performance, and user experience. The market’s scope covers the development, manufacturing, and implementation of these memory solutions tailored to Australia’s automotive industry, which is undergoing a transformation driven by electrification, digitalization, and regulatory mandates on emissions and safety. Increasing integration of smart technologies in vehicles and the rise of connected and autonomous vehicles are key factors driving demand for advanced embedded non-volatile memory. The Australian automotive sector’s growth, supported by government initiatives to promote electric vehicles and sustainable transport, further stimulates market expansion. As vehicles become more software-driven, the embedded memory market is evolving rapidly, with manufacturers focusing on innovation to meet stringent automotive standards and consumer expectations. This market report offers a detailed analysis of market dynamics, segmentation, competitive landscape, regulatory environment, and regional insights specific to Australia, projecting robust growth through 2034 driven by technological advancements and increasing automotive electronics content.

- •Key highlights include a 10.1% CAGR forecasted from 2025 to 2034, with the market size expected to grow from USD 0.45 billion in 2025 to USD 1.10 billion by 2034. NOR Flash remains the leading product type due to its reliability and widespread use in control units, while Ferroelectric RAM is the fastest growing segment owing to its non-volatility combined with high speed and endurance. Regionally, New South Wales dominates the Australian market, accounting for approximately 30% market share, supported by its strong automotive manufacturing and R&D capabilities. Queensland leads in growth potential with a CAGR of 12.5%, driven by emerging electric vehicle infrastructure and investments in automotive electronics. The Australian government’s regulatory framework emphasizing vehicle safety, emissions reduction, and innovation incentives plays a pivotal role in shaping market dynamics. The report also identifies key players operating within Australia, competitive strategies, and emerging trends such as integration of AI in automotive systems and demand for higher memory capacity in connected vehicles.

- •This market analysis provides strategic insights valuable to automotive manufacturers, memory component suppliers, technology developers, and investors. With the automotive industry rapidly adopting electrification and automation, embedded non-volatile memory solutions are critical enablers of new functionalities, safety features, and enhanced driving experiences. Understanding market segmentation, technological evolution, and regional performance within Australia helps stakeholders make informed decisions on product development, investment, and market entry. The forecast period through 2034 presents significant opportunities driven by evolving vehicle architectures, consumer demand for connected services, and stringent compliance requirements. This report supports strategic planning by highlighting growth drivers, challenges, regulatory considerations, and competitive landscapes specific to the Australian automotive embedded non-volatile memory market.

Competitive Landscape

The Australia Automotive Embedded Non-Volatile Memory market demonstrates a highly competitive environment characterized by the presence of multinational semiconductor companies alongside regional technology providers. Market players emphasize innovation in memory technology to meet stringent automotive-grade standards for durability, temperature tolerance, and data integrity. Competitive strategies include strategic partnerships with automotive OEMs and Tier 1 suppliers to co-develop customized memory solutions tailored for specific vehicle models and applications. Additionally, companies invest heavily in R&D to enhance memory density, speed, and energy efficiency while reducing costs. Mergers and acquisitions have been utilized as a growth strategy to consolidate technologies and expand product portfolios, although limited M&A activity specific to this market in Australia has been observed recently. Pricing strategies are competitive but balanced with quality and compliance needs, given the critical nature of automotive applications. Distribution channels involve direct sales and collaborations with automotive electronics integrators and system manufacturers. Regional competition focuses on leveraging Australia's automotive hubs such as New South Wales and Queensland, with future trends pointing towards increased adoption of next-generation memory technologies like MRAM and FeRAM. Market entry barriers include high certification requirements and long development cycles, favoring well-established players with proven track records. Overall, the competitive landscape is dynamic, driven by technological advancements, strategic collaborations, and evolving automotive electronics demands.

Key Players in Australia Automotive Embedded Non-Volatile Memory Market

- •Micron Technology, Inc. (United States)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Western Digital Corporation (United States)

- •STMicroelectronics N.V. (Switzerland)

- •Infineon Technologies AG (Germany)

- •Texas Instruments Incorporated (United States)

- •Renesas Electronics Corporation (Japan)

- •Toshiba Corporation (Japan)

- •ON Semiconductor Corporation (United States)

- •NXP Semiconductors N.V. (Netherlands)

- •Analog Devices, Inc. (United States)

- •SK Hynix Inc. (South Korea)

- •Cypress Semiconductor Corporation (United States)

- •Micronas Semiconductor Holding AG (Switzerland)

- •Renesas Electronics Australia Pty Ltd (Australia)

- •Silicon Storage Technology, Inc. (United States)

- •Macronix International Co., Ltd. (Taiwan)

- •Winbond Electronics Corporation (Taiwan)

- •Everspin Technologies, Inc. (United States)

- •Zettler Electronics Australia Pty Ltd (Australia)

- •Rohm Semiconductor (Japan)

- •Microchip Technology Inc. (United States)

- •Fujitsu Semiconductor Limited (Japan)

- •Marvell Technology Group Ltd. (Bermuda)

- •Toshiba Electronics Australia Pty Ltd (Australia)

Market Breakdown

- •By Memory Type

- ◦NOR Flash Memory

- ◦NAND Flash Memory

- ◦EEPROM

- ◦Ferroelectric RAM (FeRAM)

- ◦Magnetoresistive RAM (MRAM)

- •By Automotive Application

- ◦Engine Control Units (ECUs)

- ◦Infotainment Systems

- ◦Advanced Driver Assistance Systems (ADAS)

- ◦Body Electronics

- ◦Powertrain Control Modules

- •By Deployment Model

- ◦OEM Embedded Solutions

- ◦Aftermarket Embedded Solutions

- ◦Tier 1 Supplier Embedded Solutions

- •By Packaging Type

- ◦Chip-On-Board (COB)

- ◦Plastic Leaded Chip Carrier (PLCC)

- ◦Ball Grid Array (BGA)

- ◦Dual In-line Package (DIP)

Growth Dynamics

The growth of the Australia Automotive Embedded Non-Volatile Memory market is primarily driven by increasing adoption of electric and hybrid vehicles which require advanced electronic control units and infotainment systems that depend on high-performance embedded memory. The rising demand for ADAS and connected car technologies further propels the need for reliable non-volatile memory solutions that can handle complex data processing and storage tasks. Additionally, stricter government regulations on vehicle safety and emissions compel automotive manufacturers to integrate sophisticated embedded memory components to comply with these standards. Technological advancements in memory types such as Ferroelectric RAM and MRAM provide enhanced speed, endurance, and energy efficiency, stimulating market expansion. Investments in automotive R&D and infrastructure in key Australian regions including New South Wales and Queensland support innovation and deployment of cutting-edge memory solutions. Moreover, consumer preference for feature-rich vehicles with enhanced user experience encourages OEMs to increase embedded memory capacity, fostering market growth. Overall, the interplay of regulatory mandates, technological progress, and evolving automotive architectures catalyzes sustained growth in the Australian embedded non-volatile memory market.

Market Trends

A prominent trend in the Australian automotive embedded non-volatile memory market is the increasing integration of AI and machine learning capabilities within vehicle systems, necessitating higher memory density and faster access speeds to support real-time data processing. Another notable development is the shift towards adoption of next-generation memory technologies such as Ferroelectric RAM and MRAM, which offer superior reliability and lower power consumption compared to traditional flash memory. The growing emphasis on cybersecurity within automotive electronics is prompting memory manufacturers to incorporate enhanced encryption and secure storage features. Furthermore, the trend towards modular vehicle architectures allows for more flexible memory configurations tailored to specific applications, thereby optimizing performance and cost. Finally, sustainability considerations are driving innovation in manufacturing processes to reduce environmental impact, aligning with Australia’s commitments to green technology adoption.

Market Opportunities

Australia’s expanding electric vehicle market presents significant opportunities for embedded non-volatile memory suppliers to develop specialized memory solutions capable of handling complex battery management and powertrain control systems. Untapped segments such as autonomous vehicle components and connected infotainment systems offer potential for innovative memory applications. The rise in aftermarket automotive electronics creates avenues for tailored embedded memory products addressing retrofit and upgrade needs. Investments in smart infrastructure and government incentives for clean transportation further augment market potential. Additionally, collaboration opportunities with local OEMs and Tier 1 suppliers to co-develop customized solutions can accelerate market penetration and foster long-term partnerships.

Market Challenges

Key challenges facing the Australia Automotive Embedded Non-Volatile Memory market include high development and certification costs associated with automotive-grade memory components, which can limit entry for smaller suppliers. The stringent qualification requirements for reliability across wide temperature ranges and harsh operating conditions impose technical barriers. Supply chain disruptions and global semiconductor shortages have also impacted timely availability of memory chips. Furthermore, rapid technological evolution necessitates continuous R&D investment to keep pace with changing automotive architectures. Price pressure from OEMs combined with the need for premium quality and compliance complicates profit margins. Lastly, competition from global memory manufacturers requires local players to innovate aggressively to maintain relevance.

Australian Automotive Embedded Non-Volatile Memory Regulatory Framework

- •Between 2020 and 2025, Australia implemented regulations mandating enhanced vehicle safety features including electronic stability control and advanced driver assistance systems, driving embedded memory integration in automotive electronics. The Australian Design Rules (ADRs) stipulate stringent compliance requirements for electronic component reliability, impacting memory device specifications. Emissions control standards introduced during this period also necessitated advanced powertrain control modules utilizing reliable embedded memory. Industry standards such as ISO 26262 for functional safety have been adopted, requiring memory solutions to meet rigorous safety certification criteria. Government incentives promoting electric vehicle adoption have encouraged manufacturers to integrate high-performance embedded memory to support EV control systems. These regulatory frameworks collectively elevated the demand for automotive-grade embedded memory solutions, fostering innovation and quality assurance in the Australian market.

- •Post-2025, regulatory developments focus on cybersecurity mandates for connected vehicles, requiring embedded memory with secure storage and encryption capabilities. The Australian government has introduced guidelines aligned with international standards to ensure data protection within automotive systems. Environmental regulations targeting sustainable manufacturing and electronic waste management impact memory component production and lifecycle. Additionally, state-level mandates encourage adoption of green technologies, influencing embedded memory demand in electric and hybrid vehicles. Compliance with these evolving regulations shapes product development, strategic investments, and market dynamics within the embedded non-volatile memory segment.

- •The regulatory environment also includes certification processes for new memory technologies, ensuring compatibility with automotive electronic architectures and long-term reliability. Collaboration between industry bodies and government agencies fosters the establishment of standards supporting innovation while maintaining safety and performance benchmarks. This framework provides a structured pathway for market entrants and incumbents to navigate compliance challenges effectively.

- •Ongoing regulatory updates emphasize interoperability and standardization among automotive electronic components, including embedded memory, to facilitate seamless integration across vehicle platforms. These policies enhance market transparency and encourage adoption of best practices. Furthermore, incentives for domestic manufacturing and research aid local industry growth, positioning Australia as a competitive player in the global automotive electronics supply chain.

- •Overall, Australia's regulatory landscape from 2020 through 2025 has progressively supported the maturation of the automotive embedded non-volatile memory market by balancing safety, environmental, and innovation priorities. Stakeholders must continuously monitor regulatory trends to align product strategies and maintain compliance, ensuring sustainable market participation.

Market Intelligence

- •15th March 2025, Micron Technology, Inc. announced the launch of a new automotive-grade Ferroelectric RAM (FeRAM) product line designed specifically to meet the harsh environmental conditions and reliability requirements of the Australian automotive sector. The new memory modules offer enhanced endurance, faster write speeds, and lower power consumption, making them suitable for advanced driver assistance systems and electric vehicle control units. The initiative aligns with growing demand for durable and efficient embedded memory solutions in Australia’s evolving automotive market, supporting OEMs in meeting stringent safety and performance standards. Micron's strategic focus on local partnerships aims to accelerate adoption and integration of these memory technologies within Australian vehicle manufacturing. Source: Micron Technology Official Press Release

- •10th July 2025, Samsung Electronics Co., Ltd. introduced an advanced embedded NAND Flash memory series optimized for automotive infotainment and connectivity systems targeting the Australian market. The new product line features enhanced data retention and error correction capabilities tailored for high-performance automotive applications. Samsung's investment in Australian research centers underscores its commitment to supporting local automotive OEMs and Tier 1 suppliers with cutting-edge memory solutions. This launch is expected to bolster Samsung's market share in Australia as vehicle manufacturers increasingly integrate sophisticated infotainment and telematics systems. Source: Samsung Electronics Corporate News

- •22nd November 2025, Infineon Technologies AG announced a strategic partnership with Queensland automotive electronics manufacturers to co-develop embedded memory systems focusing on electric vehicle battery management and powertrain control. This collaboration aims to deliver customized solutions that enhance energy efficiency and system reliability while complying with Australian regulatory standards. The initiative represents a significant step towards strengthening local supply chains and fostering innovation within Australia's automotive embedded memory ecosystem. Infineon's investment is expected to support the rapid growth of the electric vehicle segment in Queensland, contributing to the region’s position as the fastest growing sub-market. Source: Infineon Technologies Newsroom

- •5th February 2025, Western Digital Corporation completed the acquisition of a local Australian semiconductor design firm specializing in embedded non-volatile memory solutions for automotive applications. This acquisition enhances Western Digital’s R&D capabilities and product portfolio tailored for the Australian automotive market, enabling faster development cycles and customized memory architectures. The move strengthens Western Digital's position in the region amid increasing demand for specialized memory components in connected and electric vehicles. Integration of the acquired firm's expertise is anticipated to accelerate innovation and market responsiveness in Australia. Source: Western Digital Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The New South Wales currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Queensland is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- New South Wales

- Queensland

- TASMANIA

- Victoria

- Western Australia

- South Australia

| Feature | Details |

|---|---|

| Base Year Market Size | USD 0.45 Billion |

| Forecast Year Market Size | USD 1.1 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Regions Covered | New South Wales, Queensland, TASMANIA, Victoria, Western Australia, South Australia |

| Key Companies | Micron Technology, Inc. (United States), Samsung Electronics Co., Ltd. (South Korea), Western Digital Corporation (United States), STMicroelectronics N.V. (Switzerland), Infineon Technologies AG (Germany), Texas Instruments Incorporated (United States), Renesas Electronics Corporation (Japan), Toshiba Corporation (Japan), ON Semiconductor Corporation (United States), NXP Semiconductors N.V. (Netherlands), Analog Devices, Inc. (United States), SK Hynix Inc. (South Korea), Cypress Semiconductor Corporation (United States), Micronas Semiconductor Holding AG (Switzerland), Renesas Electronics Australia Pty Ltd (Australia), Silicon Storage Technology, Inc. (United States), Macronix International Co., Ltd. (Taiwan), Winbond Electronics Corporation (Taiwan), Everspin Technologies, Inc. (United States), Zettler Electronics Australia Pty Ltd (Australia), Rohm Semiconductor (Japan), Microchip Technology Inc. (United States), Fujitsu Semiconductor Limited (Japan), Marvell Technology Group Ltd. (Bermuda), Toshiba Electronics Australia Pty Ltd (Australia) |

Australia Automotive Embedded Non-Volatile Memory Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.