China Fully Automatic Enzyme Immunoassay Instrument Market - China Size & Outlook 2025-2034

China Fully Automatic Enzyme Immunoassay Instrument Market is segmented by Type (Chemiluminescence Immunoassay Instruments, Enzyme-Linked Immunosorbent Assay (ELISA) Instruments, Fluorescence Immunoassay Instruments, Radioimmunoassay Instruments, Turbidimetric Immunoassay Instruments), Application (Clinical Diagnostics, Pharmaceutical Research, Food Safety Testing, Environmental Monitoring, Veterinary Diagnostics), End-User Facility (Hospitals, Diagnostic Laboratories, Research Institutes, Veterinary Clinics, Food Testing Laboratories), Distribution Channel (Direct Sales, Distributors, Online Sales, After-Sales Service Providers), and Geography (North China, Northeast China, East China, South Central China, Southwest China, Northwest China)

Pricing

Report Overview

Executive Summary

- •The China Fully Automatic Enzyme Immunoassay Instrument market comprises highly automated devices that detect and quantify specific substances through enzyme immunoassay techniques to support diverse applications such as clinical diagnostics, pharmaceutical research, food safety, environmental monitoring, and veterinary diagnostics. The market includes various types of instruments like chemiluminescence immunoassay, ELISA, fluorescence immunoassay, radioimmunoassay, and turbidimetric immunoassay systems that deliver improved sensitivity, throughput, and operational efficiency. These instruments help healthcare providers and researchers rapidly perform complex immunoassays with minimal human intervention, leading to faster and more reliable results. The industry scope extends to hospitals, diagnostic centers, research laboratories, food testing facilities, and veterinary clinics across China. Growing healthcare infrastructure, increasing chronic disease incidence, and government-backed initiatives supporting technological upgrades drive the adoption of fully automatic enzyme immunoassay instruments. Furthermore, innovations in assay chemistry and instrument design are enabling broader application and enhanced market penetration across China's vast and diverse regions.

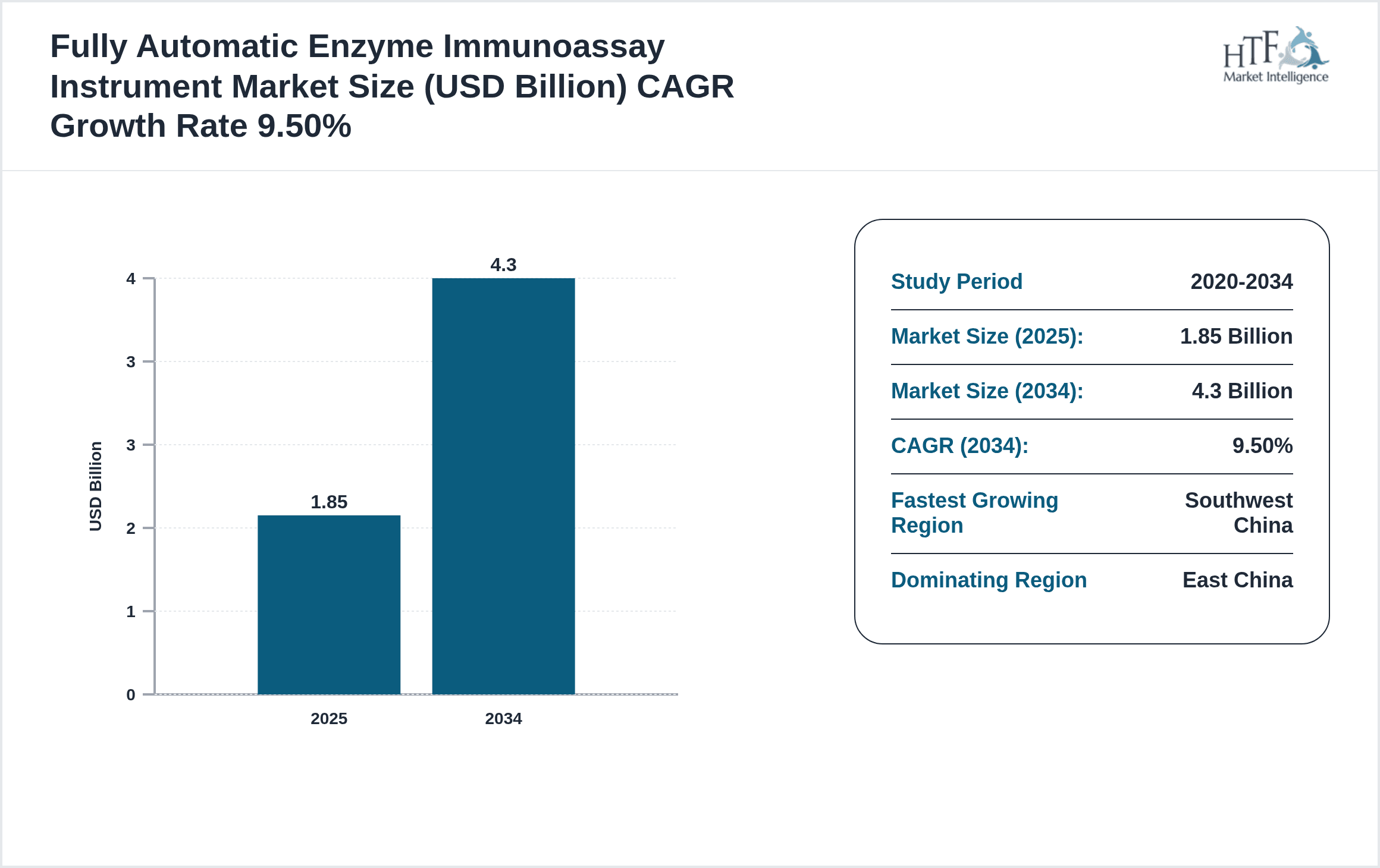

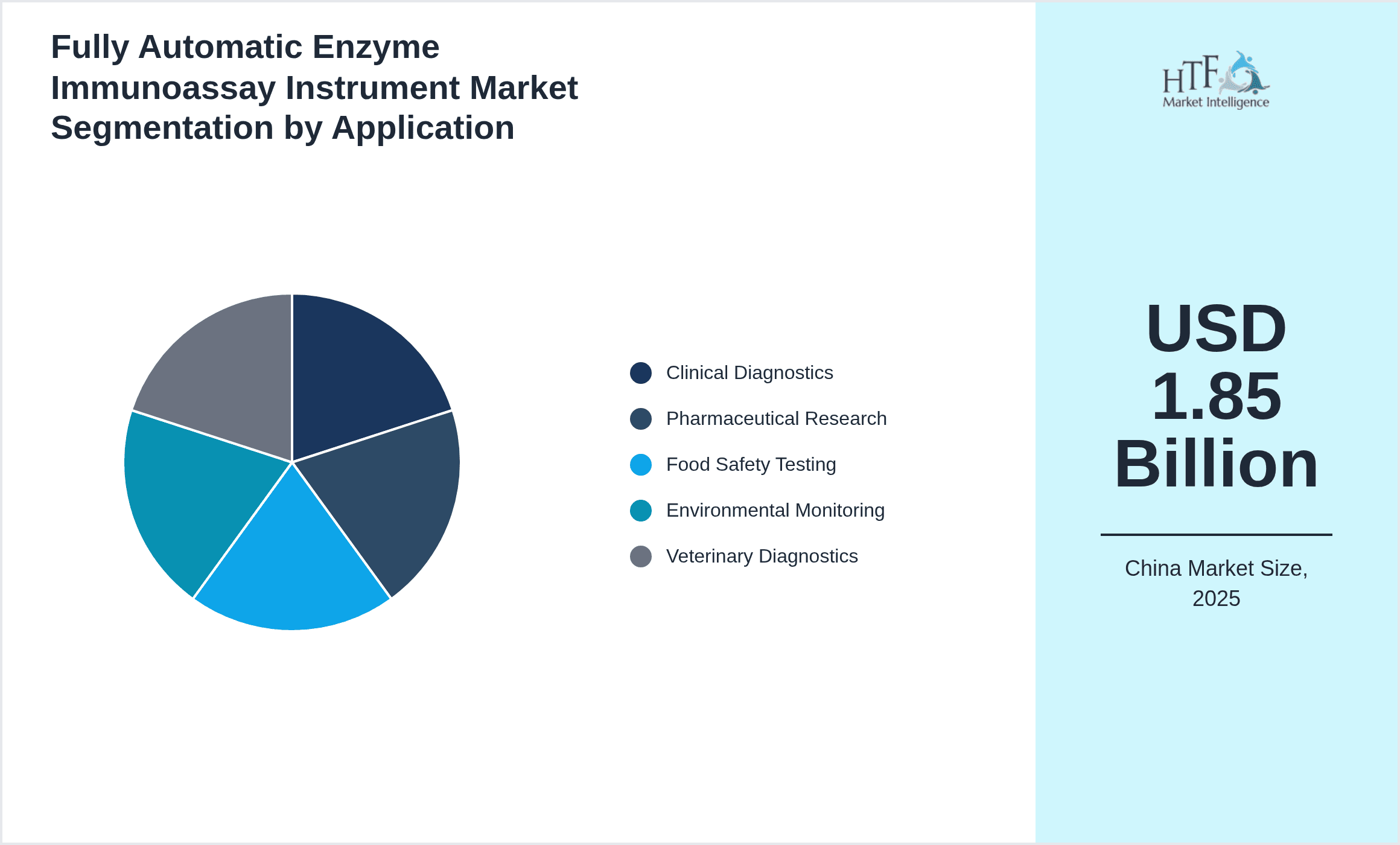

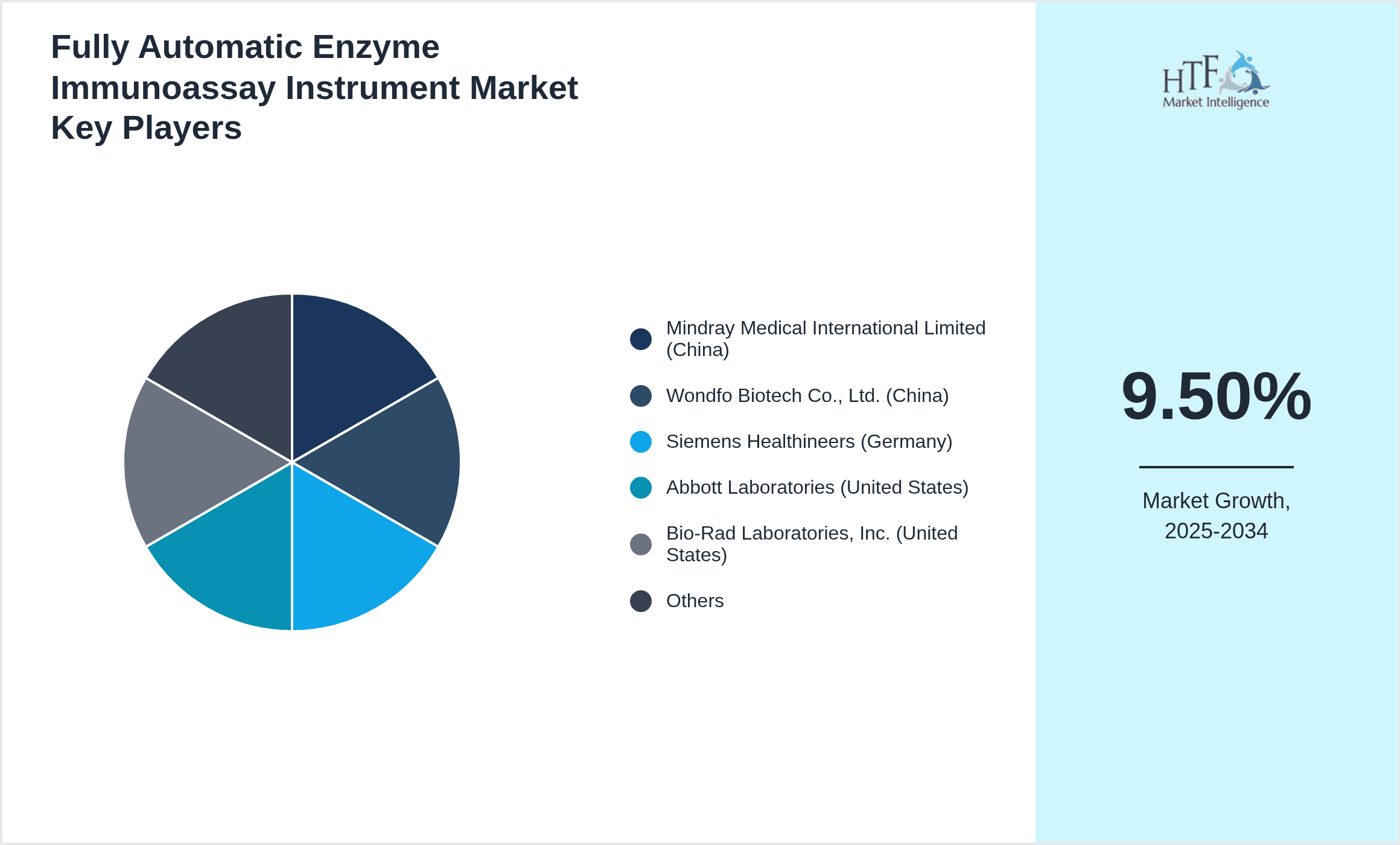

- •Key highlights include a projected CAGR of 9.5% from 2025 to 2034, expanding the market size from USD 1.85 billion in 2025 to USD 4.3 billion by 2034. East China dominates with a 28% market share due to its advanced healthcare infrastructure and concentration of research centers, while Southwest China exhibits the fastest growth at 12.3% CAGR. Chemiluminescence immunoassay instruments lead the product type segment, favored for their high sensitivity and specificity, whereas fluorescence immunoassay instruments are the fastest growing due to technological advancements and expanding application scope. Clinical diagnostics remain the largest application segment, driven by increased demand for rapid and accurate disease detection. The competitive landscape is marked by domestic and international players investing in innovation, strategic partnerships, and regional expansion to capture emerging opportunities within China’s diverse healthcare ecosystem.

- •The China Fully Automatic Enzyme Immunoassay Instrument market plays a strategic role in advancing healthcare quality and research capabilities across the country. Its ability to deliver precise, automated testing solutions supports early disease detection, monitoring, and drug development efforts, thereby benefiting patients, clinicians, and pharmaceutical companies alike. The market’s growth is underpinned by government policies promoting healthcare modernization, increasing awareness of enzyme immunoassay benefits, and rising investments in biotechnology. Stakeholders including instrument manufacturers, healthcare providers, and regulatory bodies must navigate evolving technological trends and regulatory frameworks to capitalize on expanding market potential. The integration of automation and digital connectivity further enhances the value proposition by enabling scalable, efficient, and cost-effective diagnostic workflows that address China’s growing healthcare demands and stringent quality standards.

Competitive Landscape

The China Fully Automatic Enzyme Immunoassay Instrument market is characterized by intense competition among both multinational corporations and domestic manufacturers striving for technological leadership and market share. Companies focus heavily on innovation, developing instruments that offer enhanced automation, improved sensitivity, and user-friendly interfaces to differentiate their offerings. Strategic partnerships with healthcare institutions and research organizations facilitate product validation and adoption, while aggressive pricing strategies aim to penetrate tier 2 and tier 3 cities in China. The rivalry also extends to expanding service networks and after-sales support to maintain customer loyalty. Mergers and acquisitions have emerged as a key competitive strategy to consolidate capabilities and broaden product portfolios. Furthermore, regional competition within China’s diverse geographical zones compels companies to tailor their go-to-market approaches, balancing urban sophistication with rural accessibility. The trend towards digitization and integration with laboratory information systems is reshaping competitive dynamics, with firms investing in software capabilities and data analytics to deliver comprehensive immunoassay solutions.

Leading Companies in Fully Automatic Enzyme Immunoassay Instrument Market

- •Mindray Medical International Limited (China)

- •Wondfo Biotech Co., Ltd. (China)

- •Siemens Healthineers (Germany)

- •Abbott Laboratories (United States)

- •Bio-Rad Laboratories, Inc. (United States)

- •Roche Diagnostics (Switzerland)

- •Beckman Coulter, Inc. (United States)

- •Shenzhen New Industries Biomedical Engineering Co., Ltd. (China)

- •Hangzhou Testsea Biotechnology Co., Ltd. (China)

- •Ortho Clinical Diagnostics (United States)

- •Thermo Fisher Scientific Inc. (United States)

- •PerkinElmer, Inc. (United States)

- •Bio-Techne Corporation (United States)

- •Diasorin S.p.A. (Italy)

- •Hycor Biomedical (United States)

- •Nova Biomedical (United States)

- •Tianjin Ringpu Bio-technology Co., Ltd. (China)

- •Zhejiang Orient Gene Biotech Co., Ltd. (China)

- •BioSino Bio-Technology & Science Inc. (China)

- •Antu Bioengineering Co., Ltd. (China)

- •DiaSorin (Italy)

- •Hoffmann-La Roche AG (Switzerland)

- •Tecan Group Ltd. (Switzerland)

- •Sysmex Corporation (Japan)

- •Bioscientia GmbH (Germany)

Market Breakdown

- •By Type

- ◦Chemiluminescence Immunoassay Instruments

- ◦Enzyme-Linked Immunosorbent Assay (ELISA) Instruments

- ◦Fluorescence Immunoassay Instruments

- ◦Radioimmunoassay Instruments

- ◦Turbidimetric Immunoassay Instruments

- •By Application

- ◦Clinical Diagnostics

- ◦Pharmaceutical Research

- ◦Food Safety Testing

- ◦Environmental Monitoring

- ◦Veterinary Diagnostics

- •By End-User Facility

- ◦Hospitals

- ◦Diagnostic Laboratories

- ◦Research Institutes

- ◦Veterinary Clinics

- ◦Food Testing Laboratories

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

- ◦After-Sales Service Providers

Growth Dynamics

- •Rising prevalence of chronic diseases such as cancer and infectious diseases in China has amplified demand for accurate and high-throughput diagnostic instruments, fueling market growth for fully automatic enzyme immunoassay systems. Hospitals and diagnostic centers increasingly adopt automation to improve workflow efficiency and patient outcomes.

- •Government initiatives focusing on healthcare infrastructure modernization and biotechnology innovation, including subsidies for laboratory automation and precision medicine projects, significantly drive market expansion by encouraging adoption of advanced immunoassay instruments.

- •Advancements in chemiluminescence and fluorescence immunoassay technologies have enhanced assay sensitivity and specificity, attracting pharmaceutical companies and research institutions to invest in these sophisticated instruments for drug discovery and development.

- •The shift towards integrated laboratory information management systems (LIMS) and digital connectivity facilitates seamless data management and remote diagnostics, further incentivizing healthcare providers to upgrade to fully automated enzyme immunoassay instruments.

- •Increasing consumer awareness regarding food safety and environmental health boosts demand for rapid, automated immunoassay testing in food and environmental laboratories, thereby expanding market opportunities beyond traditional clinical applications.

- •Strategic collaborations between instrument manufacturers and local distributors enhance market penetration in tier 2 and tier 3 cities, addressing regional healthcare disparities and accelerating market adoption across China’s vast geography.

- •Investment in R&D by both domestic and international companies to develop compact, user-friendly, and cost-effective immunoassay instruments is expected to sustain growth momentum by catering to small clinics and remote testing locations.

Market Trends

- •Increased adoption of multiplex immunoassay platforms capable of detecting multiple analytes simultaneously is gaining traction in China, enabling more comprehensive disease profiling and faster diagnostics in clinical and research settings.

- •The rise of point-of-care testing (POCT) combined with automation is creating new market opportunities by delivering rapid, onsite immunoassay results, particularly in rural and underserved regions of China.

- •Integration of artificial intelligence (AI) and machine learning algorithms with immunoassay instruments is enhancing data interpretation accuracy and predictive diagnostics, driving innovation and differentiation among market players.

- •Sustainability considerations are influencing instrument design, with manufacturers focusing on energy-efficient models and reduction of reagent consumption to meet environmental regulations and customer preferences.

- •Collaborative ecosystems involving instrument vendors, reagent suppliers, and software developers are emerging to offer end-to-end immunoassay solutions that streamline laboratory workflows and improve operational efficiency.

- •Growing demand for personalized medicine in China is encouraging development of immunoassay instruments tailored for biomarker detection, facilitating targeted therapies and improved patient management.

- •The COVID-19 pandemic has accelerated adoption of automated immunoassay platforms for serological testing, establishing a foundation for sustained growth and innovation in infectious disease diagnostics.

Market Opportunities

- •Expansion into underserved regions such as Southwest and Northwest China presents significant growth potential by addressing unmet diagnostic needs through affordable and portable fully automatic enzyme immunoassay instruments.

- •Development of multi-functional immunoassay platforms that combine different detection technologies can unlock new applications in pharmaceutical research and environmental testing, broadening market reach.

- •Investment in localized manufacturing and reagent development can reduce costs and improve supply chain resilience, enhancing competitiveness of domestic players in the Chinese market.

- •Collaboration with government health programs for large-scale screening initiatives offers opportunities to deploy automated immunoassay instruments in public health campaigns targeting infectious and chronic diseases.

- •Leveraging digital health trends by integrating cloud-based data analytics and remote monitoring capabilities can provide value-added services and foster customer loyalty.

- •Rising consumer demand for food safety and environmental quality monitoring creates avenues for specialized immunoassay instruments tailored for these sectors, expanding the market beyond clinical diagnostics.

- •Strategic alliances with international technology leaders enable transfer of advanced immunoassay technologies and accelerate innovation pipelines in China.

Market Challenges

- •High initial investment costs for fully automatic enzyme immunoassay instruments limit adoption by smaller hospitals and clinics, restricting market penetration in lower-tier cities and rural areas.

- •Complex regulatory approval processes and stringent quality standards in China can delay product launches and increase compliance costs for manufacturers, especially new entrants.

- •Dependence on imported reagents and components exposes the market to supply chain disruptions and currency fluctuations, impacting pricing and availability.

- •Limited skilled technical personnel to operate and maintain sophisticated immunoassay instruments hinders efficient utilization, particularly in less developed regions.

- •Intense competition from low-cost domestic manufacturers challenges profitability and compels multinational companies to innovate continuously to maintain market share.

- •Data security and privacy concerns related to integration of immunoassay instruments with digital health platforms pose regulatory and trust challenges.

- •Rapid technological obsolescence requires ongoing R&D investments, which can strain resources for small and mid-sized companies operating in the China market.

Regulatory Framework

- •Between 2020 and 2025, China’s National Medical Products Administration (NMPA) implemented stricter classification and registration requirements for in vitro diagnostic devices, including enzyme immunoassay instruments, mandating comprehensive safety and performance evaluations prior to market entry.

- •New guidelines introduced in 2023 require manufacturers to enhance traceability and quality control of reagents used in immunoassay instruments, elevating standards for product consistency and reliability across the supply chain.

- •Environmental regulations enacted in 2024 impose restrictions on hazardous waste disposal generated from immunoassay testing processes, compelling companies to adopt eco-friendly manufacturing and waste management practices.

- •Pilot programs initiated in 2022 promote accelerated approval pathways for innovative diagnostic technologies under the China Drug Administration Law, encouraging local innovation while ensuring patient safety.

- •Government incentives supporting domestic production of key reagents and diagnostic equipment have been expanded in 2023 to reduce import dependence and foster self-reliance within the enzyme immunoassay market.

Market Intelligence

- •15th January 2025, Mindray Medical International Limited launched a next-generation chemiluminescence immunoassay analyzer featuring enhanced throughput and AI-powered result interpretation, targeting large hospitals and diagnostic labs across East and South China. The instrument integrates seamlessly with hospital information systems, reducing manual errors and accelerating diagnostic workflows. This launch aims to consolidate Mindray’s leadership in China’s clinical diagnostics segment by offering superior accuracy and operational efficiency. Source: Mindray Official Press Release

- •22nd March 2025, Wondfo Biotech Co., Ltd. introduced a portable fluorescence immunoassay instrument designed for point-of-care testing in remote and rural regions of China. The device supports rapid detection of infectious diseases with minimal sample preparation and connectivity for cloud-based data management. This innovation responds to growing demand for decentralized diagnostics and aligns with government rural healthcare initiatives. Source: Wondfo Corporate Website

- •10th June 2024, Siemens Healthineers expanded its footprint in China by establishing a regional research and development center focused on immunoassay technology enhancements, including multiplexing and digital integration. This strategic move is expected to accelerate product innovation tailored to local market needs and strengthen collaborations with Chinese academic institutions. Source: Siemens Press Release

- •5th November 2024, Roche Diagnostics announced a partnership with a leading Chinese pharmaceutical company to co-develop immunoassay reagents optimized for prevalent diseases in China such as hepatitis and diabetes. This collaboration aims to improve assay sensitivity and reduce costs, enhancing accessibility across Chinese healthcare settings. Source: Roche Official News

Regional Outlook

The East China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southwest China is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North China

- Northeast China

- East China

- South Central China

- Southwest China

- Northwest China

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 4.3 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Scope of Report | Market is segmented by Type (Chemiluminescence Immunoassay Instruments, Enzyme-Linked Immunosorbent Assay (ELISA) Instruments, Fluorescence Immunoassay Instruments, Radioimmunoassay Instruments, Turbidimetric Immunoassay Instruments), Application (Clinical Diagnostics, Pharmaceutical Research, Food Safety Testing, Environmental Monitoring, Veterinary Diagnostics), End-User Facility (Hospitals, Diagnostic Laboratories, Research Institutes, Veterinary Clinics, Food Testing Laboratories), Distribution Channel (Direct Sales, Distributors, Online Sales, After-Sales Service Providers) |

| Regions Covered | North China, Northeast China, East China, South Central China, Southwest China, Northwest China |

| Key Companies | Mindray Medical International Limited (China), Wondfo Biotech Co., Ltd. (China), Siemens Healthineers (Germany), Abbott Laboratories (United States), Bio-Rad Laboratories, Inc. (United States), Roche Diagnostics (Switzerland), Beckman Coulter, Inc. (United States), Shenzhen New Industries Biomedical Engineering Co., Ltd. (China), Hangzhou Testsea Biotechnology Co., Ltd. (China), Ortho Clinical Diagnostics (United States), Thermo Fisher Scientific Inc. (United States), PerkinElmer, Inc. (United States), Bio-Techne Corporation (United States), Diasorin S.p.A. (Italy), Hycor Biomedical (United States), Nova Biomedical (United States), Tianjin Ringpu Bio-technology Co., Ltd. (China), Zhejiang Orient Gene Biotech Co., Ltd. (China), BioSino Bio-Technology & Science Inc. (China), Antu Bioengineering Co., Ltd. (China), DiaSorin (Italy), Hoffmann-La Roche AG (Switzerland), Tecan Group Ltd. (Switzerland), Sysmex Corporation (Japan), Bioscientia GmbH (Germany) |

China Fully Automatic Enzyme Immunoassay Instrument Market - China Size & Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.