Quartz Glass for Optical Purposes Market - Europe Size & Outlook 2020-2034

Europe Quartz Glass for Optical Purposes Market is segmented by Quartz Glass Type (Fused Quartz, Fused Silica, Synthetic Quartz, Crystalline Quartz, Amorphous Quartz), Optical Application (Precision Optics, Photolithography, Optical Fiber, Laser Systems, Medical Imaging), Manufacturing Process (Flame Fusion, Electric Fusion, Chemical Vapor Deposition, Sol-Gel Process), End-Use Industry (Semiconductor Manufacturing, Telecommunications, Healthcare & Medical Devices, Defense & Aerospace), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Quartz Glass for Optical Purposes market is defined by the production and application of high-purity quartz glass materials used primarily in optical components and devices. This market includes various types of quartz glass such as fused quartz, fused silica, synthetic quartz, crystalline quartz, and amorphous quartz, each offering unique properties suited for different optical needs. The scope covers applications in precision optics, photolithography, optical fiber communications, laser systems, and medical imaging technologies. The value chain starts from raw quartz extraction and purification, followed by advanced manufacturing processes involving melting, molding, and finishing to produce optical-grade glass. These components are then integrated into diverse end-use industries including telecommunications, semiconductor manufacturing, healthcare, and defense sectors across Europe. The market is propelled by the increasing adoption of quartz glass in high-tech applications due to its superior light transmission, thermal stability, and chemical resistance, which are critical for reliability and performance in optical devices. Europe’s robust semiconductor and telecommunications industries significantly contribute to demand, alongside growing investments in laser and medical imaging technologies. Additionally, technological advancements in synthetic quartz production and expanding use in fiber optics and photolithography drive innovation and market expansion, positioning quartz glass as an essential material in Europe's optical technology ecosystem.

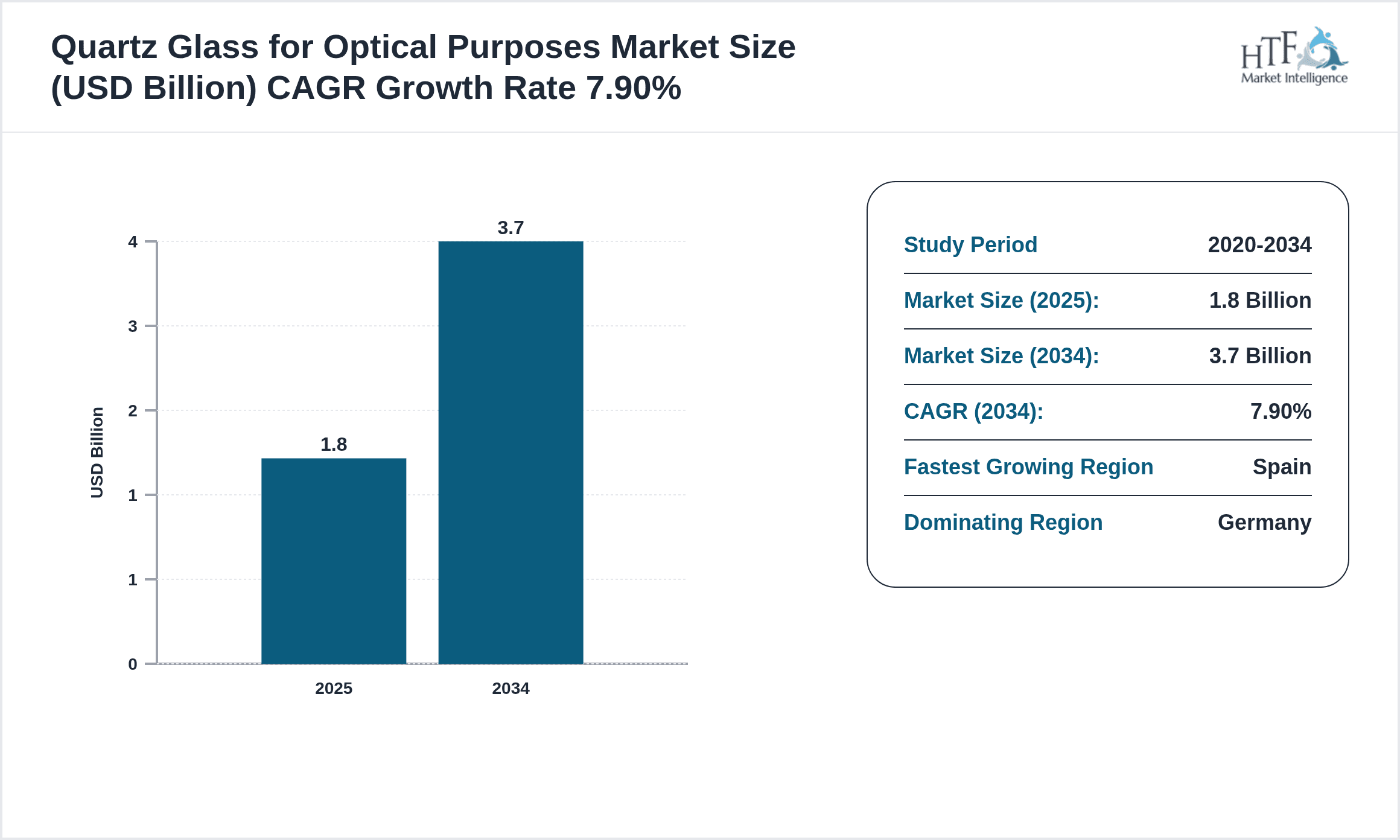

- •Key market highlights include a base year market size of USD 1.8 Billion in 2025, growing to an anticipated USD 3.7 Billion by 2034, reflecting a CAGR of 7.9%. Germany leads as the dominating regional market with a 28% share, attributed to its advanced manufacturing infrastructure and strong semiconductor sector. Spain is identified as the fastest-growing country within Europe, with a CAGR of 10.2%, driven by rising investments in telecommunications and medical device manufacturing. Among product types, fused silica remains dominant due to its widespread application in precision optics, while synthetic quartz is the fastest-growing segment, benefiting from innovations that improve purity and manufacturability. Applications such as photolithography and optical fibers continue to expand, fueled by demand for smaller, faster semiconductor devices and robust communication networks. Market dynamics are shaped by technological innovation, regulatory compliance, and growing environmental sustainability considerations.

- •The market offers significant value propositions to diverse industries by enabling production of high-performance optical components essential for cutting-edge devices. Quartz glass’s superior optical clarity, durability, and thermal resistance ensure enhanced device efficiency, longevity, and accuracy in applications ranging from semiconductor fabrication to medical imaging. This strategic importance attracts stakeholders including raw material suppliers, manufacturers, equipment providers, and end users in telecommunications, healthcare, and industrial sectors. The evolving technology landscape and growing demand for miniaturized, high-precision optical components underscore the market's critical role in Europe's industrial and technological advancement.

Competitive Landscape

The Europe Quartz Glass for Optical Purposes market is characterized by a highly competitive environment with established multinational corporations and specialized regional manufacturers vying for market share. Competitive strategies revolve around technological innovation, process optimization, and product differentiation to meet stringent optical quality and purity standards required by end-use industries. Companies emphasize R&D investments to improve synthetic quartz production methods and enhance material properties such as transmission efficiency and thermal stability. Strategic partnerships and collaborations with semiconductor and optical equipment manufacturers enable integration of quartz glass components into advanced device architectures. Mergers and acquisitions, although limited recently, play a role in consolidating technological expertise and expanding geographic footprint. Pricing strategies are influenced by raw material costs and production complexities, with premium pricing justified by superior product performance. Distribution channels include direct supply agreements with industrial clients and collaborations with optical component assemblers. Regional competition is intense between Western European manufacturing hubs and emerging players in Central and Eastern Europe. Future trends indicate increasing adoption of sustainable manufacturing processes and digitalization in quality control to maintain competitive advantage.

Prominent Players in Quartz Glass for Optical Purposes Market

- •Schott AG (Germany)

- •Heraeus Quarzglas GmbH & Co. KG (Germany)

- •Momentive Performance Materials Inc. (USA)

- •Mitsubishi Chemical Corporation (Japan)

- •Ohara Corporation (Japan)

- •Asahi Glass Co., Ltd. (AGC) (Japan)

- •Corning Incorporated (USA)

- •Kopp Glass, Inc. (Germany)

- •Lattice Materials GmbH (Germany)

- •Tosoh Corporation (Japan)

- •Nippon Electric Glass Co., Ltd. (Japan)

- •Advanced Glass Technologies Ltd. (UK)

- •Saint-Gobain Quartz (France)

- •Glassworks Ltd. (UK)

- •SiCrystal AG (Germany)

- •Heraeus Noblelight GmbH (Germany)

- •Toshiba Materials Co., Ltd. (Japan)

- •Mersen Group (France)

- •Plan Optik AG (Germany)

- •Sicnova Laser SL (Spain)

- •Optoelectronics GmbH (Germany)

- •SCHOTT Lithotec GmbH (Germany)

- •LiqTech International, Inc. (Denmark)

- •Nippon Quartz Co., Ltd. (Japan)

- •Euroquartz Ltd. (UK)

Market Breakdown

- •By Quartz Glass Type

- ◦Fused Quartz

- ◦Fused Silica

- ◦Synthetic Quartz

- ◦Crystalline Quartz

- ◦Amorphous Quartz

- •By Optical Application

- ◦Precision Optics

- ◦Photolithography

- ◦Optical Fiber

- ◦Laser Systems

- ◦Medical Imaging

- •By Manufacturing Process

- ◦Flame Fusion

- ◦Electric Fusion

- ◦Chemical Vapor Deposition

- ◦Sol-Gel Process

- •By End-Use Industry

- ◦Semiconductor Manufacturing

- ◦Telecommunications

- ◦Healthcare & Medical Devices

- ◦Defense & Aerospace

Growth Dynamics

- •Rising demand for high-purity quartz glass in semiconductor photolithography drives growth, as smaller node fabrication requires materials with exceptional optical clarity and thermal stability. Leading European semiconductor hubs such as Germany and France bolster this trend with expanding chip manufacturing capacities.

- •Increased deployment of fiber optic networks across Europe to support 5G and broadband expansion fuels demand for quartz glass optical fibers, promoting market expansion particularly in countries like Spain and Italy with growing telecommunications infrastructure investments.

- •Advancements in laser system technologies for industrial and medical applications require quartz glass components with high damage thresholds and precision shaping, encouraging manufacturers to innovate synthetic quartz production methods for enhanced performance.

- •Environmental regulations promoting sustainable and energy-efficient manufacturing processes encourage adoption of cleaner quartz glass production technologies, positively influencing market growth by aligning with European Union’s green directive goals.

- •Growing healthcare sector demand for advanced medical imaging technologies such as endoscopy and optical coherence tomography drives applications of quartz glass, particularly in Western Europe, highlighting the material’s biocompatibility and optical advantages.

- •Rising investments by European governments and private sectors in R&D for photonics and optical material innovations stimulate market growth by enabling next-generation quartz glass products with superior properties and new application potential.

- •Increasing consumer electronics miniaturization trends require smaller, more precise optical components made from quartz glass, incentivizing companies to enhance manufacturing precision and material quality to meet evolving industry needs.

Market Trends

- •Integration of synthetic quartz with nanostructured coatings enhances optical performance and durability, exemplified by recent product launches from leading European quartz glass manufacturers targeting photonics and laser markets.

- •Shift towards digitalization and automation in quartz glass manufacturing improves consistency, reduces defects, and shortens lead times, enabling suppliers to meet increasing demand for precision optics in Europe’s semiconductor sector.

- •Emergence of eco-friendly quartz glass production methods, such as sol-gel processes, aligns with Europe’s sustainability commitments and attracts customers seeking greener optical materials without compromising quality.

- •Collaborations between quartz glass producers and optical device manufacturers foster innovation in custom optical components tailored for aerospace and defense applications, driving market differentiation and growth.

- •Expansion of laser-based additive manufacturing technologies utilizes quartz glass components with unique thermal and optical properties, broadening application scopes and creating new market segments in Europe.

- •Increasing adoption of quartz glass in medical imaging devices supports high-resolution diagnostics, with European healthcare providers investing in optical technologies for enhanced patient outcomes.

- •Development of integrated photonics platforms incorporating quartz glass substrates accelerates as European research institutions and companies pursue miniaturized, high-performance optical circuits for telecommunications and computing.

Market Opportunities

- •Expanding semiconductor manufacturing in Eastern Europe offers untapped markets for quartz glass suppliers, presenting growth potential through localized production and tailored product offerings.

- •Rising demand for high-power laser systems in industrial manufacturing creates opportunities to develop specialized synthetic quartz products with enhanced thermal and mechanical properties.

- •Integration of quartz glass in next-generation medical diagnostic devices opens avenues for innovation in biocompatible optical materials, catering to Europe’s aging population and healthcare modernization.

- •Collaboration with photonics startups and research centers enables development of advanced quartz glass components for emerging applications such as quantum computing and LiDAR technologies.

- •Growing optical fiber deployments for smart city infrastructure in Southern Europe provide new markets for quartz glass fiber preforms and related materials, supporting urban digital transformation.

- •Government incentives for green manufacturing encourage investment in sustainable quartz glass production lines, enhancing competitiveness and market access within Europe’s eco-conscious customer base.

- •Customization services for precision optics allow quartz glass manufacturers to cater to niche markets requiring high-quality, application-specific components, strengthening client relationships and revenue streams.

Market Challenges

- •High production costs associated with ultra-pure quartz glass manufacturing limit price competitiveness, particularly against lower-cost imports from Asia, challenging European manufacturers to optimize operations.

- •Raw material supply chain fluctuations and scarcity of natural quartz deposits in Europe create vulnerabilities in consistent production and pricing stability for quartz glass producers.

- •Stringent regulatory requirements for optical materials and chemical handling increase compliance burden and operational costs, impacting smaller manufacturers disproportionately.

- •Technological complexity in producing defect-free large-size quartz glass components restricts scalability and limits adoption in some high-volume applications.

- •Competition from alternative materials such as specialty plastics and ceramics for certain optical applications pressures quartz glass market share and necessitates continuous innovation.

- •Limited skilled workforce availability in advanced manufacturing techniques hinders capacity expansion and technology adoption within Europe’s quartz glass industry.

- •Economic uncertainties including fluctuating demand in end-use sectors like automotive and aerospace reduce investment appetite and market predictability for quartz glass suppliers.

Regulatory Framework

- •The European Union’s REACH regulation, implemented before 2020, mandates rigorous chemical safety and environmental compliance for quartz glass manufacturers, impacting raw material sourcing and production processes significantly. Companies must ensure all substances used meet safety standards to continue market access.

- •Directive 2011/65/EU (RoHS) limits hazardous substances in electronic and optical components, requiring quartz glass producers supplying semiconductor and telecommunications sectors to comply with strict material composition guidelines, influencing product design and material selection.

- •EU Eco-Design Directive enforces energy efficiency in manufacturing processes, prompting quartz glass producers to adopt cleaner, energy-saving technologies and reduce carbon footprint, aligning with Europe’s Green Deal objectives and enhancing sustainability credentials.

- •The European Chemicals Agency (ECHA) periodically updates guidelines on the handling and disposal of silica dust and quartz particles to protect worker health, necessitating enhanced workplace safety measures and compliance protocols in production facilities.

- •Country-specific regulations such as Germany’s Federal Immission Control Act impose additional environmental and emission standards on quartz glass manufacturing plants, requiring continuous monitoring and investment in pollution control technologies to meet local compliance.

Market Intelligence

- •15th January 2025, Schott AG announced the launch of an advanced line of synthetic quartz products specifically designed for semiconductor photolithography applications. These products feature enhanced purity levels and improved thermal shock resistance, enabling manufacturers to achieve greater precision in chip fabrication processes. Schott AG aims to capitalize on Europe’s expanding semiconductor market by addressing the demand for superior optical materials that support smaller node sizes and higher throughput. The new product line also incorporates sustainable manufacturing practices aligned with EU environmental regulations, reinforcing the company’s commitment to green innovation. This strategic initiative is expected to strengthen Schott AG’s competitive position and support long-term growth in the quartz glass optical segment across Europe. Source: Schott AG Official Press Release

- •10th March 2025, Heraeus Quarzglas GmbH & Co. KG introduced a novel fused silica optical fiber preform that enhances signal transmission efficiency for telecommunications networks. Developed using proprietary electric fusion technology, the preform demonstrates lower attenuation and higher durability under extreme environmental conditions. This innovation supports the rollout of 5G infrastructure throughout Europe, particularly benefiting markets in Spain and Italy where network expansion is accelerating. Heraeus also emphasized the product’s compatibility with eco-friendly production standards, responding to increasing customer demand for sustainable optical materials. The company’s R&D investment reflects a broader industry trend towards improving optical fiber performance and meeting evolving communication needs. Source: Heraeus Corporate Website

- •22nd May 2025, Mitsubishi Chemical Corporation announced a strategic collaboration with European photonics startup Optoelectronics GmbH to co-develop custom synthetic quartz components tailored for industrial laser systems. This partnership aims to combine Mitsubishi’s material expertise with Optoelectronics’ application-specific design capabilities to address rising demand for high-power laser applications in manufacturing and healthcare. The collaboration includes joint research projects focusing on enhancing quartz glass thermal resistance and optical purity, anticipated to accelerate product development cycles and market entry. The initiative aligns with Europe’s growing industrial laser market and supports both companies’ goals of innovation leadership in optical materials. Source: Mitsubishi Chemical Press Release

- •8th August 2024, Corning Incorporated completed the acquisition of advanced quartz glass producer Lattice Materials GmbH based in Germany. The acquisition strengthens Corning’s European manufacturing footprint and expands its portfolio of high-purity quartz glass products for optical communications and precision optics markets. The deal is expected to yield operational synergies through consolidated R&D and streamlined supply chains, enhancing Corning’s ability to meet rising demand in Europe’s telecommunications and semiconductor sectors. This strategic move reflects ongoing consolidation trends in the quartz glass industry aimed at improving competitiveness and innovation capacity. Source: Corning Incorporated Official Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Spain is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 3.7 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Quartz Glass Type (Fused Quartz, Fused Silica, Synthetic Quartz, Crystalline Quartz, Amorphous Quartz), Optical Application (Precision Optics, Photolithography, Optical Fiber, Laser Systems, Medical Imaging), Manufacturing Process (Flame Fusion, Electric Fusion, Chemical Vapor Deposition, Sol-Gel Process), End-Use Industry (Semiconductor Manufacturing, Telecommunications, Healthcare & Medical Devices, Defense & Aerospace) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Schott AG (Germany), Heraeus Quarzglas GmbH & Co. KG (Germany), Momentive Performance Materials Inc. (USA), Mitsubishi Chemical Corporation (Japan), Ohara Corporation (Japan), Asahi Glass Co., Ltd. (AGC) (Japan), Corning Incorporated (USA), Kopp Glass, Inc. (Germany), Lattice Materials GmbH (Germany), Tosoh Corporation (Japan), Nippon Electric Glass Co., Ltd. (Japan), Advanced Glass Technologies Ltd. (UK), Saint-Gobain Quartz (France), Glassworks Ltd. (UK), SiCrystal AG (Germany), Heraeus Noblelight GmbH (Germany), Toshiba Materials Co., Ltd. (Japan), Mersen Group (France), Plan Optik AG (Germany), Sicnova Laser SL (Spain), Optoelectronics GmbH (Germany), SCHOTT Lithotec GmbH (Germany), LiqTech International, Inc. (Denmark), Nippon Quartz Co., Ltd. (Japan), Euroquartz Ltd. (UK) |

Quartz Glass for Optical Purposes Market - Europe Size & Outlook 2020-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.