Europe Prefabricated Photovoltaic Substation Market - Europe Size & Outlook 2024-2034

Europe Prefabricated Photovoltaic Substation Market is segmented by Type (Containerized Substation, Modular Substation, Skid-Mounted Substation, Mobile Substation, Hybrid Substation), Application (Residential, Commercial, Utility, Industrial, Agricultural), End User (Energy Utilities, Independent Power Producers, Commercial Enterprises, Agricultural Sector), Technology (Smart Grid Integrated Substations, Conventional Prefabricated Substations, Hybrid Energy Substations), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

The Europe Prefabricated Photovoltaic Substation Market is a specialized segment focused on providing ready-to-install electrical substations optimized for photovoltaic energy systems, facilitating efficient power transformation and distribution from solar installations. These substations are engineered to support a wide range of photovoltaic applications, including residential, commercial, utility-scale, industrial, and agricultural solar projects. The market is defined by a variety of substation types such as containerized, modular, skid-mounted, mobile, and hybrid designs, each offering unique advantages in terms of scalability, installation speed, and adaptability to diverse site conditions. The scope includes integration with smart grid technologies and compliance with stringent European renewable energy standards, underscoring the sector's strategic importance in the regional energy transition. Market growth is driven by increasing solar capacity installation, government incentives, and the need for grid modernization. Europe’s leading economies such as Germany, France, and the United Kingdom dominate the market, supported by robust policy frameworks and technological innovation. The industry's future is shaped by evolving energy policies, technological advancements in prefabrication, and rising demand for decentralized energy solutions, positioning the market for substantial growth through 2034.

Competitive Landscape

The competitive landscape of the Europe Prefabricated Photovoltaic Substation Market is characterized by intense rivalry among global and regional manufacturers striving to enhance their market positioning through innovation and strategic partnerships. Companies are focusing on developing advanced modular and containerized substations that offer superior flexibility, scalability, and integration capabilities with smart grid infrastructure. Innovation is a key differentiator, with leading players investing heavily in R&D to improve substation efficiency, reduce installation times, and comply with evolving environmental regulations. Market participants leverage strategic collaborations and joint ventures to expand their footprint across Europe, especially in high-growth countries like France and Germany. Pricing strategies are influenced by raw material costs and competitive bidding in public renewable energy projects, while product differentiation is achieved through customization and enhanced safety features. Distribution networks are being optimized for timely delivery and service support, ensuring customer retention and satisfaction. Barriers to entry remain moderate due to technological complexity and capital requirements, but emerging players capitalize on niche applications and regional demand. Overall, the competitive dynamics are shaped by technological innovation, regulatory compliance, and expanding renewable energy investments.

Leading Companies in Prefabricated Photovoltaic Substation Market

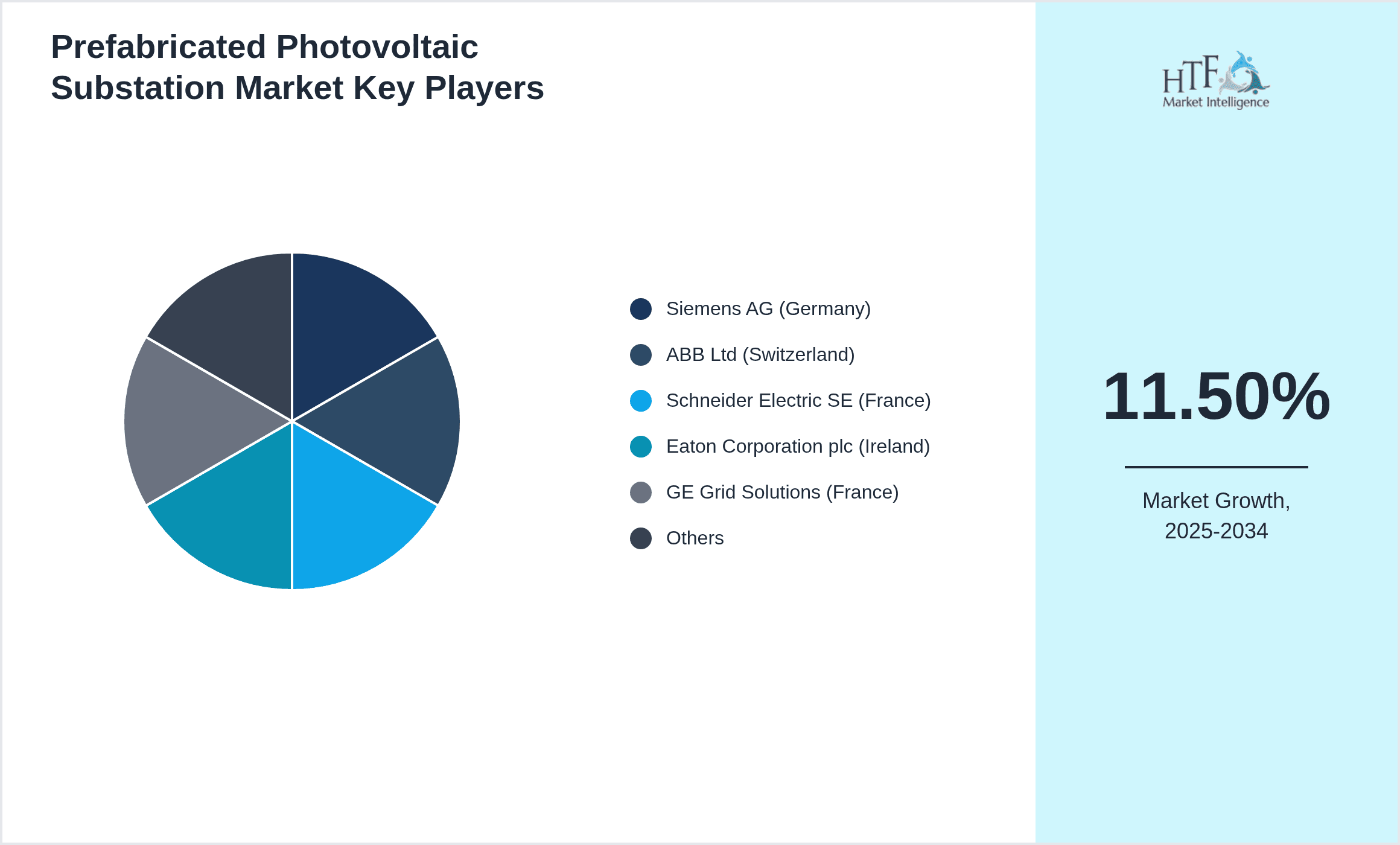

- •Siemens AG (Germany)

- •ABB Ltd (Switzerland)

- •Schneider Electric SE (France)

- •Eaton Corporation plc (Ireland)

- •GE Grid Solutions (France)

- •Hitachi Energy (Switzerland)

- •Mitsubishi Electric Europe (Germany)

- •SGB-SMIT Group (Germany)

- •Toshiba Transmission & Distribution Systems (UK)

- •Nexans S.A. (France)

- •Rittal GmbH & Co. KG (Germany)

- •Crompton Greaves Consumer Electricals Limited (Spain)

- •Alfen N.V. (Netherlands)

- •Powertis (Spain)

- •Solar Substation Solutions GmbH (Germany)

- •Schaltbau Holding AG (Germany)

- •S&C Electric Company (UK)

- •Vinci Energies (France)

- •Efacec Power Solutions (Portugal)

- •ZIV Group (Spain)

- •DFM Solar (Germany)

- •Enerparc AG (Germany)

- •Prysmian Group (Italy)

- •NKT A/S (Denmark)

- •Elia Group (Belgium)

Market Breakdown

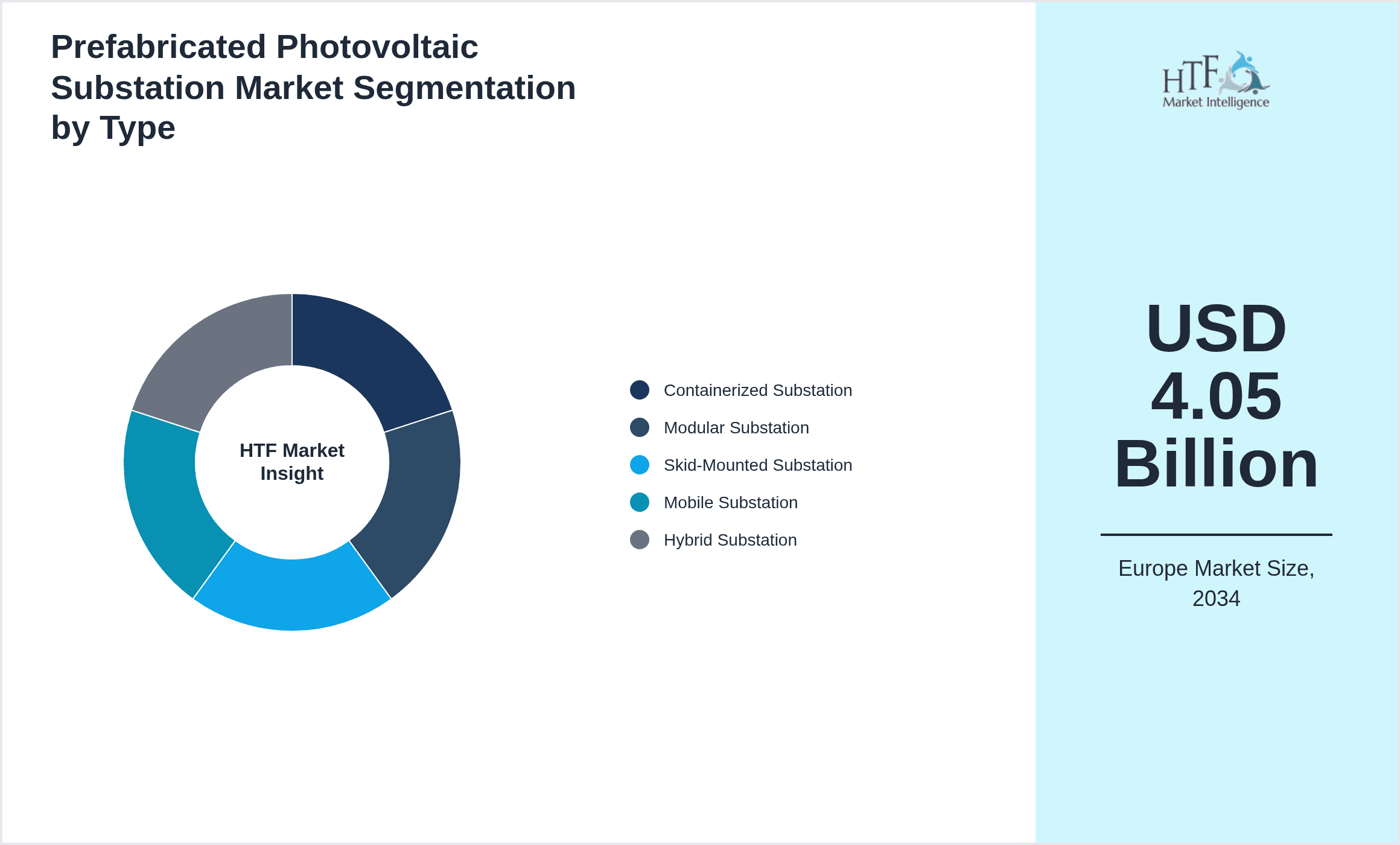

- •By Type

- ◦Containerized Substation

- ◦Modular Substation

- ◦Skid-Mounted Substation

- ◦Mobile Substation

- ◦Hybrid Substation

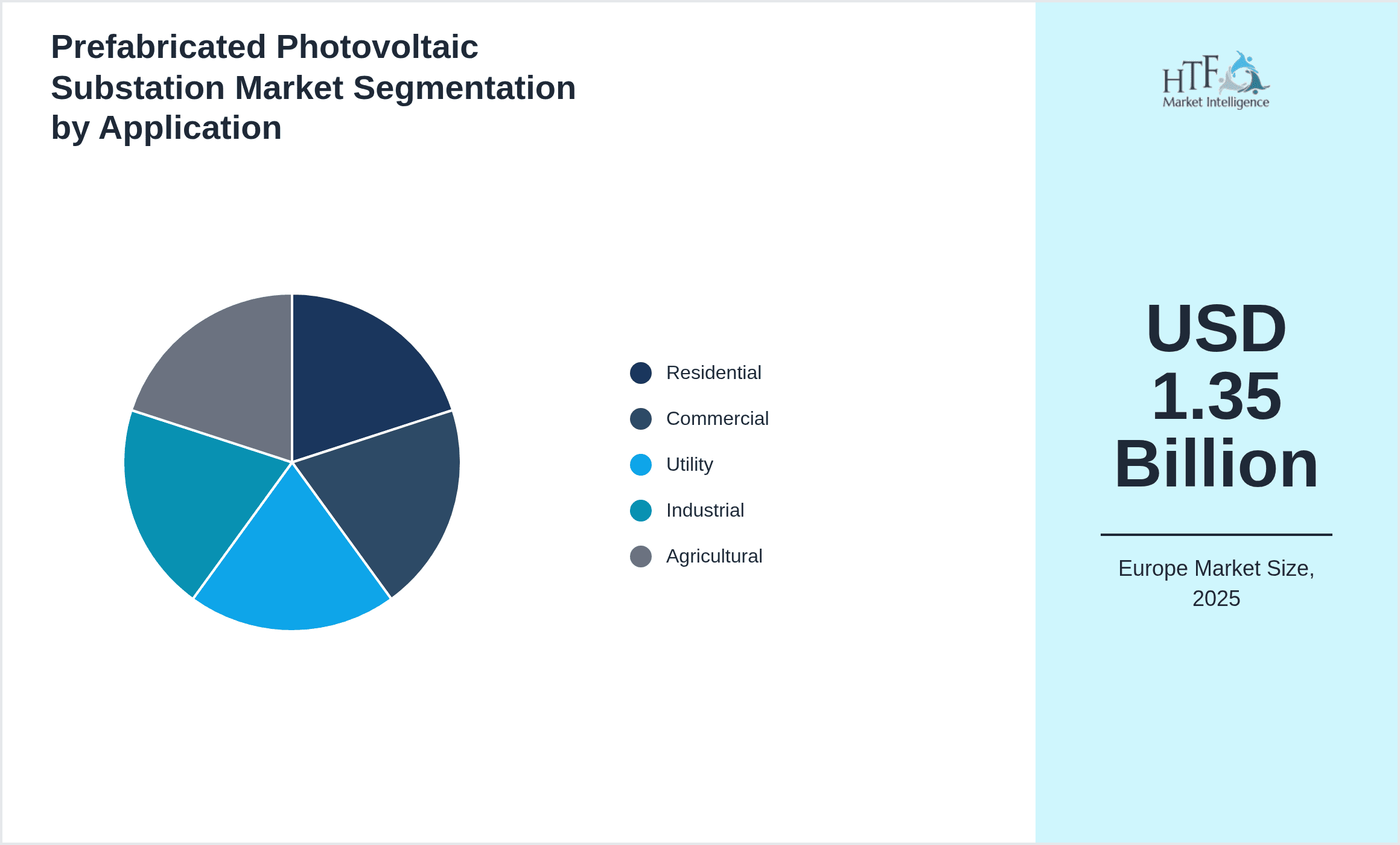

- •By Application

- ◦Residential

- ◦Commercial

- ◦Utility

- ◦Industrial

- ◦Agricultural

- •By End User

- ◦Energy Utilities

- ◦Independent Power Producers

- ◦Commercial Enterprises

- ◦Agricultural Sector

- •By Technology

- ◦Smart Grid Integrated Substations

- ◦Conventional Prefabricated Substations

- ◦Hybrid Energy Substations

Growth Dynamics

- •The Europe Prefabricated Photovoltaic Substation Market is propelled by strong governmental policies aimed at increasing renewable energy capacities, particularly solar power. Incentives such as feed-in tariffs and subsidies encourage investments in prefabricated substations that reduce installation time and costs. Additionally, the demand for grid modernization and integration of distributed energy resources fosters adoption of modular and containerized substations, which offer flexibility and scalability. Technological advancements in prefabrication and automation also contribute to improved efficiency and reliability, meeting stringent European grid codes. Furthermore, growing environmental awareness among consumers and industries stimulates demand across residential and commercial applications.

- •Rising solar installations across Europe, notably in Germany and France, create a burgeoning need for efficient power transformation infrastructure. Prefabricated substations enable rapid deployment in solar farms and rooftop installations, addressing spatial constraints and reducing on-site construction complexities. The increasing electrification of industries and agriculture further drives demand for customized prefabricated solutions. Market players benefit from strategic collaborations with renewable energy developers, amplifying growth prospects. The integration of smart grid technologies enhances substation functionalities, attracting investments from utilities and independent power producers.

- •The trend towards modular and containerized prefabricated substations is gaining momentum due to their ease of transport, installation, and adaptability to various site conditions. European manufacturers are emphasizing eco-friendly materials and designs aligned with sustainability goals. The shift toward hybrid substations that integrate energy storage and multiple renewable sources reflects evolving market demands. Digitalization and remote monitoring capabilities are also transforming the market, enabling predictive maintenance and operational excellence. These trends collectively enhance the market’s attractiveness for investors and end users.

- •Despite robust growth, the market faces challenges from fluctuating raw material costs and supply chain disruptions, which can delay project timelines and increase expenses. Regulatory compliance complexity across different European countries necessitates tailored solutions, raising engineering and certification costs. The high initial capital investment for advanced prefabricated substation technologies may also restrain small-scale developers. Furthermore, competition from traditional on-site constructed substations persists in certain segments, limiting immediate market penetration. Lastly, skilled labor shortages in specialized prefabrication processes impact production scalability.

- •Opportunities abound in expanding prefabricated photovoltaic substation applications to emerging European markets with untapped solar potential, such as Eastern Europe and the Mediterranean region. The growing emphasis on decentralized energy generation opens new avenues for mobile and hybrid substation deployment. Innovation in integrating energy storage and grid management technologies creates value-added solutions. Additionally, public-private partnerships and green financing schemes present capital infusion opportunities. Manufacturers can leverage digital twin technologies and IoT-enabled monitoring systems to offer differentiated services, fostering long-term customer relationships and market expansion.

Market Trends

- •The Europe Prefabricated Photovoltaic Substation Market is witnessing a significant shift towards modular and containerized designs due to their rapid deployability and ease of scalability, especially in utility-scale solar projects. This trend aligns with the increasing complexity of renewable energy grids requiring adaptable infrastructure. Manufacturers are also integrating digital monitoring systems to enhance operational efficiency. The rising adoption of hybrid substations combining photovoltaic generation with energy storage and other renewable sources reflects an industry-wide push for flexible energy solutions. Environmental sustainability considerations are driving the use of eco-friendly materials and low-carbon manufacturing processes. These trends collectively support the ongoing energy transition and grid modernization efforts across Europe.

- •Smart grid integration is increasingly becoming a standard feature in new prefabricated photovoltaic substations, enabling real-time data analytics and predictive maintenance. This trend is supported by advancements in IoT and communication technologies. Furthermore, the adoption of decentralized energy systems, including microgrids, is shaping demand for mobile and skid-mounted substations that facilitate quick deployment in remote or off-grid locations. Energy policy frameworks emphasizing carbon neutrality by 2050 are accelerating investments in innovative substation technologies. Collaborations between technology providers and utilities are fostering integrated solutions to improve grid stability and renewable power integration.

- •Europe’s focus on reducing greenhouse gas emissions has prompted stricter regulatory standards for photovoltaic infrastructure, influencing substation design and construction. This has resulted in the development of substations with enhanced safety, electromagnetic compatibility, and noise reduction features. The rising trend of electrification in agriculture and industrial sectors is expanding the application base for prefabricated substations. Additionally, digital twin technology adoption enables virtual simulation and optimization of substation performance before deployment, reducing costs and risks. The market is also witnessing increased demand for customized solutions tailored to specific climatic and geographical conditions.

- •The COVID-19 pandemic accelerated digital transformation in the energy sector, leading to increased investments in automated and remotely operable prefabricated substations. Supply chain resilience has become a priority, with manufacturers localizing component sourcing and enhancing modular designs to reduce dependencies. There is also a growing trend of integrating cybersecurity features into prefabricated substations to protect critical energy infrastructure. Public awareness campaigns and sustainability certifications are influencing procurement decisions, favoring vendors with green credentials. These evolving trends are shaping the competitive landscape and innovation focus within the European market.

- •Collaborative innovation through partnerships between equipment manufacturers, renewable energy developers, and research institutions is driving accelerated product development cycles. European Union funding programs support pilot projects aimed at integrating advanced energy storage and grid management within prefabricated substations. Market participants are adopting lifecycle cost analysis to demonstrate long-term value to customers, encouraging wider acceptance. Additionally, emerging technologies such as solid-state transformers and advanced power electronics are beginning to influence substation design. These strategic and technological trends underscore a dynamic market environment focused on sustainability, efficiency, and adaptability.

Market Opportunities

- •Expanding solar capacity in emerging European economies presents significant growth opportunities for prefabricated photovoltaic substations, particularly in Eastern Europe and the Balkans. These regions are experiencing increased investments in renewable energy infrastructure with supportive policy frameworks. Prefabricated substations offer a cost-effective and rapid deployment solution to meet urgent grid integration needs. Additionally, the rise of decentralized energy systems and microgrids across rural and industrial areas creates demand for mobile and skid-mounted substations. Opportunities also exist in retrofitting aging grid infrastructure with advanced prefabricated solutions that incorporate smart grid technologies, enhancing grid resilience and efficiency.

- •The integration of energy storage systems into photovoltaic substations opens new avenues for innovation and market penetration. Hybrid substations combining battery storage with solar generation facilitate grid balancing and peak load management, addressing intermittency challenges. Manufacturers can capitalize on this trend by developing modular, scalable storage-integrated substations tailored for diverse applications. Furthermore, the increasing adoption of electric vehicles and associated charging infrastructure in Europe creates ancillary demand for prefabricated substations capable of managing load fluctuations. Strategic partnerships with EV infrastructure providers offer additional growth channels. Investment incentives and green financing mechanisms further enhance market accessibility.

- •Advancements in digital technologies such as IoT, AI, and digital twins provide opportunities to deliver value-added services through prefabricated photovoltaic substations. Real-time monitoring, predictive maintenance, and remote operation capabilities improve asset management and reduce operational costs. Providers offering integrated digital solutions alongside hardware can differentiate themselves in the competitive landscape. The growing emphasis on sustainability also opens opportunities for eco-friendly materials and manufacturing practices, appealing to environmentally conscious customers and aligning with European Union climate targets. Expanding into adjacent renewable sectors such as wind and hybrid energy systems presents diversification potential for substation manufacturers.

- •Collaboration with energy utilities and government agencies for smart grid modernization projects represents a strategic opportunity. Prefabricated substations designed for seamless integration with digital grid management systems are increasingly sought after. Participating in public-private partnerships and pilot projects allows companies to showcase technological capabilities and gain market credibility. Additionally, expanding service offerings to include installation, maintenance, and lifecycle management can generate recurring revenue streams and strengthen customer relationships. Geographic expansion into underserved markets within Europe, supported by localized manufacturing and supply chains, offers further growth prospects.

- •There is growing potential to develop customized prefabricated photovoltaic substations designed for extreme weather and geographically challenging environments common in parts of Europe. Solutions tailored to cold climates, high humidity, or seismic zones enhance market appeal. The adoption of standardized modular components facilitates faster certification and deployment across multiple countries, reducing time-to-market. Furthermore, increasing consumer demand for green buildings and energy self-sufficiency fuels interest in residential and commercial prefabricated substations. Capitalizing on these niche segments with innovative, flexible products can drive incremental market growth.

Market Challenges

- •One of the primary challenges in the Europe Prefabricated Photovoltaic Substation Market is the complexity of navigating diverse regulatory environments across multiple countries. Different certification standards, grid codes, and environmental requirements necessitate customized engineering and compliance efforts, increasing project timelines and costs. This regulatory fragmentation limits scalability and complicates cross-border deployment. Additionally, varying incentive structures and policy uncertainties in some European nations affect market predictability and investor confidence, posing risks for manufacturers and developers.

- •Supply chain disruptions and escalating raw material prices, particularly for electrical components and metals, pose significant challenges to cost management and timely delivery of prefabricated substations. Global logistics constraints and geopolitical tensions have exacerbated these issues, leading to project delays and margin pressures. Smaller manufacturers face difficulties competing with larger players who have more robust procurement networks, impacting market diversity. Furthermore, limited availability of skilled workforce specialized in prefabrication and renewable energy infrastructure construction constrains capacity expansion and quality assurance.

- •High upfront capital expenditure associated with advanced prefabricated substations, especially those incorporating smart grid and energy storage technologies, restricts adoption among smaller developers and residential customers. Financing complexities and longer payback periods may hinder widespread market penetration. The competition from traditional on-site constructed substations, which may offer lower initial costs despite longer installation times, remains a barrier. Additionally, integration challenges with existing grid infrastructure, especially in older urban areas, require bespoke solutions that can increase complexity and costs.

- •Technological obsolescence risk is a concern, as rapid advancements in power electronics, digital control systems, and energy storage solutions can render existing prefabricated substation designs outdated. Manufacturers must continuously invest in R&D to keep pace with innovation, which may strain resources. Cybersecurity threats targeting digitally integrated substations also present operational risks, necessitating enhanced protective measures. Market fragmentation due to numerous small-scale players offering niche products can dilute brand recognition and complicate standardization efforts.

- •Environmental and social acceptance challenges, such as aesthetic concerns and land use conflicts, can impede project approvals and community support for new photovoltaic substation installations. Noise and electromagnetic interference from substations may trigger regulatory scrutiny and require mitigation measures. Navigating public perception and ensuring transparent stakeholder engagement are essential but resource-intensive tasks. These non-technical barriers can delay project execution and add to overall costs, impacting market growth trajectories.

Regulatory Framework

- •Between 2019 and 2024, Europe has seen the implementation of the EU Renewable Energy Directive (RED II), which mandates increased renewable energy targets and encourages the adoption of prefabricated photovoltaic substations to accelerate solar power integration. Compliance with the Low Voltage Directive and Medium Voltage Directive has become stricter, requiring enhanced safety and electromagnetic compatibility standards for substation equipment. The European Network of Transmission System Operators (ENTSO-E) has updated grid codes to support distributed generation and smart grid technologies, influencing substation design and interoperability. Additionally, the EU’s Green Deal has introduced incentives and funding mechanisms to promote clean energy infrastructure investments. National regulations in Germany, France, and the UK complement these frameworks with specific certification and environmental impact assessment requirements, ensuring robust market governance and facilitating technology adoption across the region.

- •The enforcement of the Machinery Directive and EMC Directive across Europe ensures that prefabricated substations meet rigorous operational safety and electromagnetic interference standards, protecting consumers and grid stability. Compliance monitoring mechanisms have been strengthened, with increased reliance on third-party certification bodies and harmonized testing protocols. These regulations compel manufacturers to innovate in design and quality control, fostering higher product reliability and market confidence. Additionally, regulations addressing waste electrical and electronic equipment (WEEE) and the restriction of hazardous substances (RoHS) impact the selection of materials and end-of-life management of substations, promoting sustainability.

- •Environmental regulations such as the EU’s Noise Directive require prefabricated substations to incorporate noise reduction features, particularly in residential and sensitive areas. Local authorities across Europe enforce land use permits and environmental impact assessments tailored to photovoltaic infrastructure projects, influencing siting and design decisions. The EU’s energy labeling and eco-design regulations incentivize energy-efficient substation components, driving adoption of next-generation technologies. Furthermore, data protection regulations like GDPR shape the deployment of digital monitoring and control systems within substations, ensuring secure handling of operational data.

- •Country-specific mandates in Germany, including the Energiewende policy framework, promote the use of standardized prefabricated substations to meet ambitious solar capacity goals. France’s multi-annual energy plan supports smart grid integration, encouraging the deployment of digitalized substation solutions. The UK’s Net Zero Strategy mandates grid modernization and renewable energy expansion, creating a favorable market environment for prefabricated photovoltaic substations. These national policies include funding support, tax incentives, and streamlined permitting processes, accelerating project development timelines. Compliance with these evolving regulatory landscapes requires manufacturers to maintain adaptive engineering and certification capabilities.

- •Government initiatives such as the European Investment Bank’s green financing programs provide critical capital to renewable energy projects incorporating prefabricated photovoltaic substations. Public-private partnerships foster research collaborations and pilot deployments of innovative substation technologies. The EU’s Horizon Europe program funds projects focused on energy system integration and digitalization, directly influencing product development and market expansion. These policy frameworks collectively support the transition towards a low-carbon energy infrastructure, positioning the prefabricated photovoltaic substation market for sustainable growth across Europe.

Market Intelligence

- •12th March 2025, Siemens AG announced the launch of its latest modular prefabricated photovoltaic substation designed to enhance grid integration for utility-scale solar projects in Europe. The new product features advanced digital control systems enabling real-time monitoring and predictive maintenance, significantly reducing operational downtime. Siemens aims to target high-growth markets in Germany and France, where rapid solar capacity expansion is underway. This launch is aligned with the company’s strategic focus on smart grid solutions and renewable energy infrastructure modernization. The product’s modular design facilitates scalable deployment, catering to diverse customer needs across residential, commercial, and utility applications. Siemens expects this innovation to strengthen its competitive positioning in the European market and accelerate the adoption of prefabricated substations.

- •18th January 2025, Schneider Electric SE unveiled a hybrid prefabricated photovoltaic substation integrating battery energy storage systems for enhanced grid stability and peak load management. The solution targets the growing demand for flexible renewable energy infrastructure in the commercial and industrial sectors across Europe. Schneider Electric emphasized the substation’s compliance with stringent European grid codes and its compatibility with smart grid platforms. The company has initiated pilot projects in France and Italy to demonstrate the system’s operational efficiency and scalability. This strategic innovation underscores Schneider Electric’s commitment to advancing sustainable energy solutions and supports its expansion in the prefabricated substation market segment.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

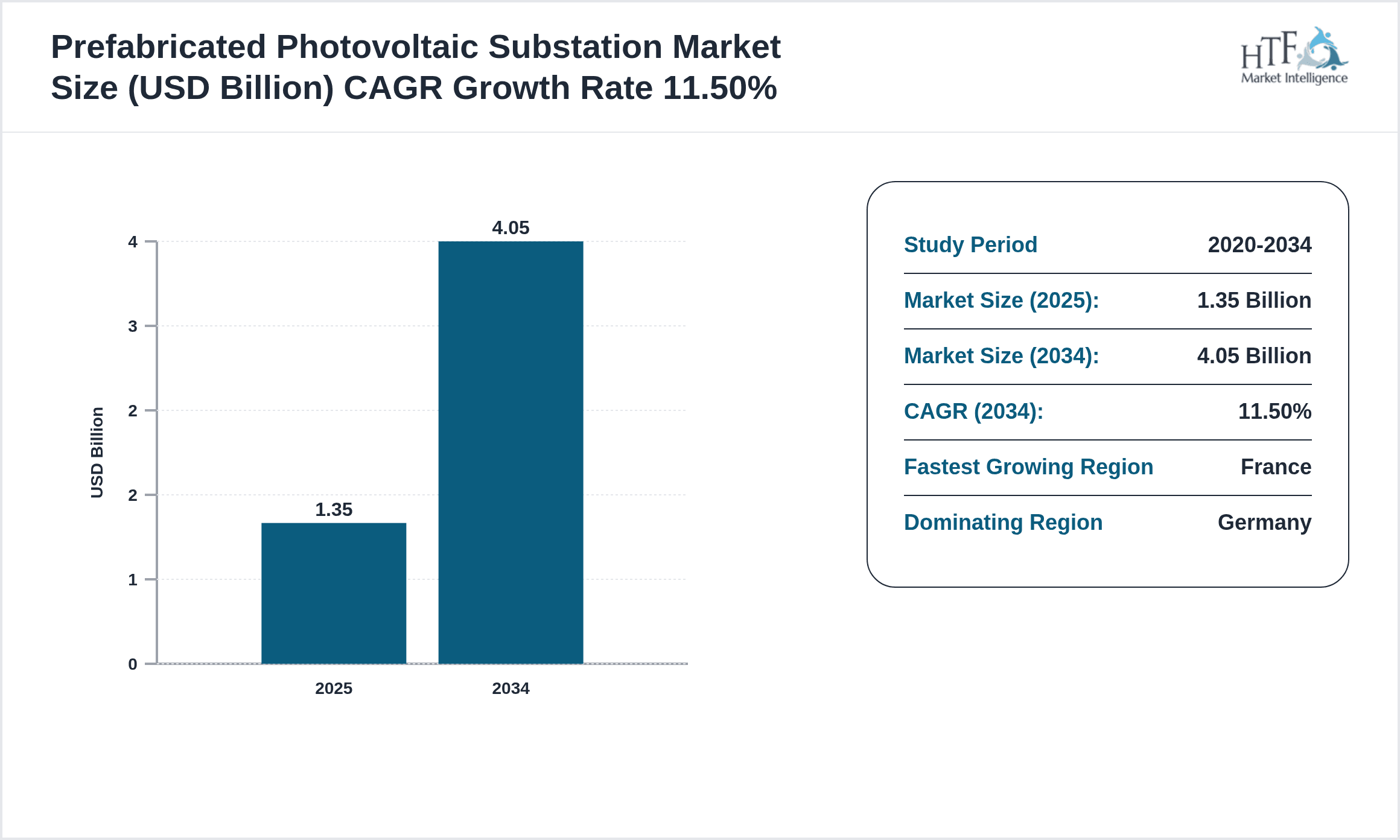

| Base Year Market Size | USD 1.35 Billion |

| Forecast Year Market Size | USD 4.05 Billion |

| CAGR | 11.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Type (Containerized Substation, Modular Substation, Skid-Mounted Substation, Mobile Substation, Hybrid Substation), Application (Residential, Commercial, Utility, Industrial, Agricultural), End User (Energy Utilities, Independent Power Producers, Commercial Enterprises, Agricultural Sector), Technology (Smart Grid Integrated Substations, Conventional Prefabricated Substations, Hybrid Energy Substations) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | Siemens AG (Germany), ABB Ltd (Switzerland), Schneider Electric SE (France), Eaton Corporation plc (Ireland), GE Grid Solutions (France) |

Europe Prefabricated Photovoltaic Substation Market - Europe Size & Outlook 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.