Europe Business Data Management Software Market - Outlook 2025-2034

Europe Business Data Management Software Market is segmented by Type (On-Premise Business Data Management Software, Cloud-Based Business Data Management Software, Hybrid Solutions, Open Source Data Management Software, SaaS Platforms), Application (Data Analytics, Data Integration, Master Data Management, Data Governance, Cloud Data Management), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Industry Vertical (Financial Services, Healthcare, Manufacturing, Retail, Telecommunications), and Geography (Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others)

Pricing

Report Overview

Executive Summary

- •The Europe Business Data Management Software Market is a dynamic and rapidly evolving sector focused on delivering comprehensive data handling and analytics solutions tailored to the unique regulatory and operational needs of European enterprises. It covers a broad spectrum of software types, including cloud-based, on-premise, hybrid, open-source, and SaaS platforms, each designed to optimize data governance, integration, and analytics. This market serves multiple applications such as data analytics, master data management, and cloud data management, enabling organizations to harness data as a strategic asset. The market’s growth is propelled by digital transformation trends, increasing regulatory compliance requirements, and the need for enhanced data security and operational efficiency. Key industry players are innovating to offer scalable, secure, and interoperable solutions that address sector-specific challenges. Overall, the market forms a critical backbone for decision-making, competitive differentiation, and regulatory adherence across industries in Europe.

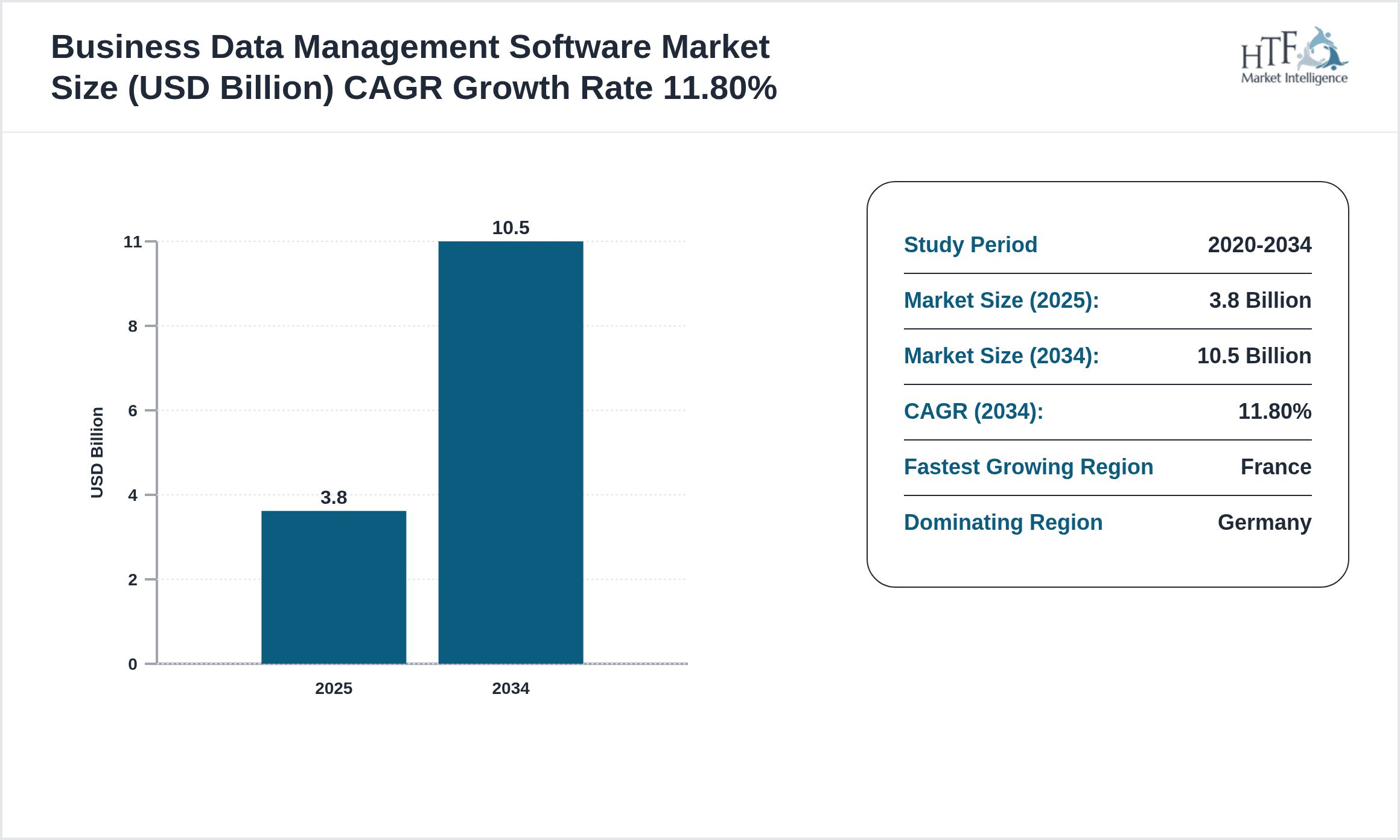

- •Significant highlights include a projected market size expansion from USD 3.8 billion in 2025 to USD 10.5 billion by 2034, reflecting a robust CAGR of 11.8%. Cloud-Based Software currently dominates the market, driven by its scalability and cost-effectiveness, while SaaS Platforms are the fastest-growing product type due to increasing adoption in SMEs. Germany holds the largest market share at 28%, leveraging its strong industrial base and digital infrastructure, whereas France exhibits the highest growth rate with a CAGR of 15.2%. The market is shaped by evolving data privacy regulations, technological innovations, and growing demand for integrated data solutions across finance, healthcare, and manufacturing sectors. Year-over-year growth is steady at approximately 11.4%, indicating sustained investment and adoption momentum across the region.

- •The Europe Business Data Management Software Market offers strategic value to stakeholders by enabling enhanced data-driven decision-making, improved compliance with stringent data protection laws such as GDPR, and operational agility through advanced analytics and cloud integration. Its importance spans IT vendors, enterprise users, regulators, and investors seeking to capitalize on digital transformation trends. The convergence of AI, machine learning, and cloud computing within data management solutions further elevates the market’s relevance. Enterprises benefit from reduced data silos, improved data accuracy, and accelerated insights generation, fostering innovation and competitiveness. As data volumes and complexity grow, the market’s role in ensuring data quality, security, and accessibility becomes increasingly vital for sustainable business growth and regulatory alignment in Europe.

Competitive Landscape

The Europe Business Data Management Software Market is characterized by intense competition and rapid innovation, driven by both established global vendors and emerging regional players. Market participants focus on differentiating through advanced technological capabilities, such as AI-powered analytics, real-time data integration, and enhanced cybersecurity features. Strategic partnerships, acquisitions, and continuous R&D investments are common to expand product portfolios and geographic reach. Pricing strategies vary from subscription-based SaaS models to traditional licensing, catering to diverse customer segments. The market exhibits moderate barriers to entry due to high technological complexity and regulatory compliance requirements. Competitive dynamics emphasize customer-centric solutions, scalability, and seamless integration with existing enterprise systems. Regional compliance mandates such as GDPR necessitate tailored offerings, further influencing competitive positioning. Future trends indicate increased consolidation, ecosystem collaborations, and innovation in cloud-native architectures to sustain growth and market leadership.

Leading Companies in Business Data Management Software Market

- •SAP SE (Germany)

- •SAS Institute Inc. (United States)

- •Software AG (Germany)

- •Micro Focus International plc (United Kingdom)

- •Talend S.A. (France)

- •Oracle Corporation (United States)

- •Informatica LLC (United States)

- •IBM Corporation (United States)

- •TIBCO Software Inc. (United States)

- •Collibra NV (Belgium)

- •Denodo Technologies (Spain)

- •Alteryx, Inc. (United States)

- •QlikTech International AB (Sweden)

- •Board International SA (Switzerland)

- •Dataiku, Inc. (France)

- •Cloudera, Inc. (United States)

- •Snowflake Inc. (United States)

- •Denodo Technologies (Spain)

- •Hitachi Vantara Corporation (Japan)

- •TIBCO Software Inc. (United States)

- •Ataccama Corporation (Czech Republic)

- •Precisely (United States)

- •Zaloni, Inc. (United States)

- •Informatica LLC (United States)

- •Teradata Corporation (United States)

Market Breakdown

- •By Type

- ◦On-Premise Business Data Management Software

- ◦Cloud-Based Business Data Management Software

- ◦Hybrid Solutions

- ◦Open Source Data Management Software

- ◦SaaS Platforms

- •By Application

- ◦Data Analytics

- ◦Data Integration

- ◦Master Data Management

- ◦Data Governance

- ◦Cloud Data Management

- •By Deployment Model

- ◦Public Cloud

- ◦Private Cloud

- ◦Hybrid Cloud

- •By Industry Vertical

- ◦Financial Services

- ◦Healthcare

- ◦Manufacturing

- ◦Retail

- ◦Telecommunications

Growth Dynamics

- •The Europe Business Data Management Software Market growth is primarily driven by the accelerating digital transformation across enterprises seeking to harness big data for strategic advantage. Implementation of stringent data privacy regulations such as GDPR compels organizations to adopt robust data governance and management solutions to ensure compliance and mitigate risks. Additionally, the rise in cloud adoption, fueled by scalability and cost-effectiveness, propels market expansion, especially for cloud-based and SaaS models. Increasing demand for real-time data analytics to enhance operational efficiency and customer insights further accelerates adoption. Enterprises across finance, healthcare, and manufacturing are investing heavily in integrated platforms to unify disparate data sources, enabling better decision-making and competitive differentiation. This convergence of regulatory pressure and technological innovation forms a robust foundation for sustained market growth throughout the forecast period.

- •Technological advancements such as artificial intelligence, machine learning, and automation embedded within data management software enhance data processing accuracy and predictive capabilities. These innovations enable organizations to uncover deeper insights and drive business agility. The proliferation of IoT devices and increasing data volumes necessitate scalable and flexible data management architectures, further promoting cloud and hybrid solutions. Moreover, the shift towards SaaS platforms offers enterprises faster deployment and reduced upfront investments, attracting small and medium enterprises. Strategic collaborations between software vendors and cloud service providers expand solution portfolios and geographic reach, contributing to market growth. Additionally, growing awareness regarding data-driven decision-making among European enterprises fuels demand for advanced data management tools that support comprehensive analytics and reporting.

- •Despite robust growth, the market faces challenges including complex integration processes with legacy systems, which can delay deployments and increase costs. Data security concerns, particularly with cloud-based solutions, remain significant barriers for conservative sectors such as banking and government. The high initial investment for advanced solutions and scarcity of skilled data management professionals contribute to slower adoption in certain segments. Furthermore, evolving regulatory landscapes demand continuous software updates and compliance certifications, imposing additional operational burdens on vendors and users alike. Market fragmentation with numerous specialized players creates competitive pressure, complicating procurement decisions for end-users. These restraints necessitate ongoing innovation and strategic partnerships to address integration, security, and talent gaps effectively.

- •The Europe Business Data Management Software Market presents significant opportunities in expanding cloud-based and SaaS offerings tailored to sector-specific needs such as healthcare compliance and financial data security. Emerging technologies like blockchain for data integrity and decentralized data management open new avenues for innovation and differentiation. Increasing investments in AI-driven data quality and governance tools offer potential for enhanced customer value and operational efficiency. Moreover, growing digitalization efforts in underpenetrated industries and small and medium-sized enterprises create untapped markets. Expansion into Eastern European countries with developing IT infrastructure represents a strategic growth frontier. Additionally, partnerships between technology vendors and consultancy firms facilitate comprehensive data management solutions, enabling accelerated market penetration and customer acquisition.

- •Market challenges include navigating complex regulatory compliance across multiple European jurisdictions, which can delay product rollouts and increase compliance costs. Intense competition from global and local vendors pressures pricing and margins, requiring continuous innovation. Vendor lock-in concerns and interoperability issues with existing enterprise applications pose adoption barriers. Additionally, the rapid pace of technological change demands continual product upgrades, straining vendor resources. Economic uncertainties and budget constraints in certain sectors may limit IT spending. Talent shortages in data science and management restrict effective implementation and utilization of advanced software. Lastly, data privacy and cyber threats require ongoing investment in security, increasing total cost of ownership and complicating vendor selection processes.

Market Trends

- •A significant trend in the Europe Business Data Management Software Market is the accelerated shift towards cloud-native architectures and SaaS delivery models, facilitating agility, scalability, and cost optimization for enterprises. This is complemented by the integration of AI and machine learning capabilities within data management solutions, enabling predictive analytics and automation of data quality processes. Vendors are increasingly incorporating advanced data governance features to ensure GDPR compliance and enhance data security. The convergence of data management with business intelligence tools streamlines decision-making workflows, driving broader adoption among mid-sized companies. Additionally, there is a rising emphasis on hybrid deployment models to balance data sovereignty concerns with cloud benefits. These trends underscore the market’s adaptation to evolving technological and regulatory landscapes, positioning it for sustained innovation and growth.

- •Another emerging trend is the proliferation of self-service data management platforms empowering business users to access and manipulate data independently, reducing reliance on IT departments. This democratization of data fosters faster insights and response times, enhancing organizational agility. Collaborative data ecosystems and partnerships among technology providers enhance interoperability and create unified data management experiences. Industry-specific vertical solutions with customized compliance and analytics features gain traction, addressing unique sectoral challenges in finance, healthcare, and manufacturing. The focus on sustainable IT practices and energy-efficient data centers also influences vendor strategies, aligning with broader European environmental goals. Overall, these trends reflect a market rapidly evolving towards user-centric, compliant, and green data management paradigms.

- •Strategically, leading vendors are investing in expanding their footprints through acquisitions and partnerships, enhancing their capabilities in cloud integration, AI, and data governance. This consolidation accelerates innovation cycles and broadens product portfolios. Open-source data management tools see increased adoption as cost-effective alternatives, pushing proprietary vendors to enhance value propositions. The integration of blockchain technologies for secure and transparent data provenance gains exploratory interest, promising future market disruption. Vendors are also focusing on enhancing user experience with intuitive interfaces and mobile accessibility, catering to a growing remote workforce. These strategic developments enable participants to address diverse customer needs and maintain competitive advantages in a fast-evolving landscape.

- •Digital transformation initiatives across Europe’s public and private sectors drive investments in modern data management infrastructures, emphasizing real-time analytics and integration. The rise of edge computing complements central data platforms, enabling efficient handling of IoT-generated data streams. Cloud service providers increasingly collaborate with data management software vendors to offer integrated, end-to-end solutions. Regulatory frameworks such as GDPR and the EU Data Act stimulate innovation in privacy-enhancing technologies and data control mechanisms embedded within software offerings. Additionally, the market witnesses growing demand for multi-cloud management capabilities to avoid vendor lock-in and optimize costs. These developments reflect a comprehensive ecosystem evolution fostering resilient and compliant data management environments.

- •Consumer preference shifts towards subscription-based models and pay-as-you-go pricing reshape vendor-go-to-market strategies, lowering barriers for smaller enterprises. Integration with popular enterprise software suites and ERP systems enhances solution stickiness and customer retention. Growing awareness of data ethics and responsible AI influences software design, ensuring transparency and fairness in data handling. The adoption of containerization and microservices architectures improves software scalability and deployment flexibility. Vendors emphasize continuous delivery and DevOps practices to accelerate feature releases and improve customer responsiveness. These trends collectively signal a maturing market increasingly focused on flexibility, compliance, and ethical data management.

Market Opportunities

- •Expanding cloud adoption among European SMEs offers a substantial growth avenue for SaaS-based business data management solutions, enabling cost-effective access to advanced data capabilities without heavy upfront investments. Tailoring offerings to sector-specific compliance and operational needs, particularly in regulated industries like healthcare and finance, opens niche market segments with high entry barriers. Integration of AI and machine learning for automated data quality and governance presents opportunities for innovation and competitive differentiation. Additionally, Eastern European markets with growing digital infrastructure represent untapped potential for market expansion. Collaborations with cloud service providers and system integrators facilitate comprehensive, end-to-end solutions, enhancing customer acquisition and retention. Furthermore, emerging technologies such as blockchain for data provenance and edge data management for IoT integration present future growth pathways.

- •Investment in developing multilingual and localized software versions addresses diverse linguistic and regulatory requirements across Europe, broadening market reach. The rising demand for real-time data analytics and integration with business intelligence platforms creates opportunities for solution enhancement and cross-selling. Growth in remote working trends drives demand for secure, cloud-accessible data management tools, encouraging innovation in mobile and remote access capabilities. Vendors can capitalize on the trend toward data democratization by developing intuitive self-service platforms for business users. Strategic acquisitions and partnerships enable rapid entry into new verticals and regions, leveraging established local expertise. Additionally, government digitalization initiatives and funding programs in Europe support technology adoption within public sector entities, expanding market scope.

- •The increasing focus on data privacy and security under European regulations incentivizes development of advanced compliance and encryption features, enhancing product value. Opportunities exist in offering modular and customizable solutions that can adapt to evolving regulatory landscapes, providing long-term customer loyalty. Expanding cloud interoperability and multi-cloud management capabilities address customer concerns about vendor lock-in and data portability. The intersection of data management with emerging technologies like augmented analytics and AI-driven insights enables creation of differentiated, high-value solutions. Furthermore, the growing importance of sustainable IT practices encourages the design of energy-efficient data management platforms, aligning with corporate social responsibility goals. These factors collectively create a fertile environment for sustained innovation and market penetration.

- •Development of training and certification programs in partnership with academic institutions and industry bodies addresses talent shortages, facilitating broader software adoption. Leveraging open-source communities for collaborative innovation accelerates development cycles and reduces costs. Expansion of embedded analytics within operational applications increases the demand for integrated data management solutions. Emerging data marketplaces and ecosystems enable vendors to monetize data assets and offer value-added services. Additionally, increasing M&A activity creates opportunities for consolidation and market share growth. By capitalizing on these strategic opportunities, stakeholders can enhance their competitive positioning and drive long-term sustainable growth in the Europe Business Data Management Software Market.

- •The convergence of cloud computing, AI, and edge data management technologies opens novel avenues for innovative product offerings, addressing complex data challenges in manufacturing, logistics, and telecommunications. Vendors can explore co-innovation models with customers to tailor solutions for unique operational contexts, enhancing customer satisfaction and retention. The surge in unstructured data volumes necessitates advanced management and analytics tools, driving demand for next-generation software capabilities. Furthermore, growing interest in data monetization strategies encourages development of analytics-as-a-service platforms, creating new revenue streams. Strategic focus on user experience and mobile accessibility caters to evolving workforce dynamics, expanding software adoption. These opportunities position the market for transformative growth aligned with technological advancements and enterprise needs.

Market Challenges

- •Integration complexities with legacy IT infrastructure remain a significant challenge, often requiring customized solutions and prolonging deployment timelines, which can deter potential adopters. The heterogeneous data sources and formats across enterprises complicate data consolidation and quality assurance efforts, increasing project costs and risks. Additionally, stringent and evolving regulatory requirements across various European countries necessitate continuous software updates and compliance verifications, straining vendor resources. The high cost of advanced data management solutions, particularly for SMEs, limits widespread adoption despite growing awareness of their benefits. A shortage of skilled data management and analytics professionals further impedes effective implementation and maintenance, impacting return on investment. Market fragmentation with numerous niche players increases customer evaluation complexity and reduces vendor bargaining power.

- •Data security and privacy concerns, especially related to cloud deployments, pose adoption barriers in sectors with conservative risk profiles such as banking and government. Vendor lock-in fears and interoperability issues with existing enterprise systems reduce flexibility and purchasing confidence. Economic uncertainties and fluctuating IT budgets in certain European regions may lead to postponed investments or scaled-back projects. Rapid technological evolution demands frequent software upgrades and training, increasing operational costs and causing potential disruptions. Competitive pressure from open-source and low-cost alternatives challenges pricing strategies and profitability. Additionally, inconsistent data governance practices among organizations hinder standardized software adoption, creating market entry obstacles. Addressing these multifaceted challenges requires coordinated efforts by vendors, customers, and regulators to foster a conducive growth environment.

- •Resistance to change within organizations often delays digital transformation initiatives, limiting the pace of business data management software adoption. Concerns around data sovereignty and cross-border data transfers complicate cloud solution deployments, impacting scalability and flexibility. The complexity of managing hybrid and multi-cloud environments introduces operational challenges and security vulnerabilities. Lack of unified standards for data quality and governance across industries impedes seamless integration and interoperability. Additionally, the high expectations for ROI and measurable business impact put pressure on vendors to demonstrate clear value propositions. These challenges necessitate enhanced customer education, robust solution design, and proactive stakeholder engagement to ensure market success.

- •Vendor consolidation through mergers and acquisitions can create uncertainty among customers regarding product continuity and support, potentially affecting contract renewals. The increasing sophistication of cyber threats requires continuous investment in security features, increasing total cost of ownership. Market maturity in Western Europe leads to saturation in certain segments, requiring innovation-driven growth strategies. Managing data lifecycle complexities, including archiving and deletion in compliance with regulations, adds operational overhead. Furthermore, balancing customization needs with standardization demands challenges software development and delivery models. These challenges underscore the importance of agile, secure, and customer-centric approaches in this competitive market.

- •Limited awareness among smaller enterprises about the strategic importance of advanced data management software slows market penetration in this segment. Variability in IT infrastructure maturity across European countries results in uneven adoption rates and market fragmentation. The need for continuous training and change management to maximize software benefits imposes additional burdens on organizations. Pricing pressures from emerging vendors and open-source alternatives challenge established players to innovate while maintaining profitability. Regulatory ambiguities related to emerging technologies such as AI and blockchain complicate compliance efforts. Addressing these layered challenges requires comprehensive strategies encompassing technology, education, and policy alignment to sustain market momentum.

Regulatory Framework

- •Between 2020 and 2025, the European Union reinforced the General Data Protection Regulation (GDPR), focusing on enhanced enforcement mechanisms and higher penalties for non-compliance, compelling enterprises to adopt robust data governance and management software to ensure data privacy and security.

- •The EU Cybersecurity Act, enacted in 2021, established an EU-wide cybersecurity certification framework for ICT products and services, including data management software, to standardize security requirements and build consumer trust across member states.

- •In 2023, the European Data Governance Act introduced measures to facilitate data sharing across sectors while ensuring compliance with privacy regulations, encouraging the development of interoperable data management platforms that support secure and compliant data exchange.

- •Country-specific mandates, such as Germany’s Federal Data Protection Act updates in 2022, emphasize data localization and stricter controls on cross-border data transfers, influencing software deployment models and compliance features within business data management solutions.

- •The EU Digital Services Act, effective from 2024, imposes new obligations on digital service providers to enhance transparency and accountability, driving demand for sophisticated data audit and reporting capabilities embedded in management software.

Market Intelligence

- •15th January 2025, SAP SE launched an enhanced cloud-native business data management platform tailored for European enterprises, integrating AI-driven analytics and advanced GDPR compliance tools. This platform aims to streamline data governance and accelerate digital transformation across sectors such as finance and manufacturing, positioning SAP as a leader in scalable, secure data solutions. The launch reflects SAP’s commitment to innovation, addressing growing demand for cloud-based, compliant data management amidst tightening regulatory landscapes. With features supporting multi-cloud environments and real-time data processing, the solution enhances operational agility and decision-making capabilities for customers across Europe. Source: SAP Official Press Release.

- •23rd March 2025, Talend S.A. introduced a next-generation SaaS platform focusing on data integration and master data management with embedded AI automation capabilities. Designed for rapid deployment and scalability, the platform supports hybrid cloud environments and offers enhanced data quality monitoring compliant with EU data privacy mandates. This innovation targets mid-sized enterprises seeking cost-effective, flexible data management solutions, reinforcing Talend’s position in the European market. The platform’s modular architecture enables tailored implementations, supporting industry-specific compliance and analytics requirements, thereby expanding market reach. Source: Talend Corporate News.

- •7th May 2025, Software AG announced a strategic partnership with Microsoft Azure to co-develop integrated data management solutions combining Software AG’s data governance expertise with Azure’s cloud infrastructure. This collaboration aims to deliver end-to-end, compliant data management services optimized for European enterprises navigating complex regulatory environments. The partnership enhances hybrid and multi-cloud deployment capabilities, addressing growing market demand for flexible, secure data ecosystems. Joint marketing and technical initiatives are expected to accelerate adoption across key verticals including healthcare, finance, and public sector. Source: Software AG Press Release.

- •30th August 2025, Collibra NV expanded its European footprint by acquiring a regional data privacy compliance software provider, strengthening its portfolio with enhanced regulatory reporting and audit capabilities. This acquisition supports Collibra’s strategy to deliver comprehensive data intelligence platforms that align with evolving European data protection laws. The move facilitates deeper market penetration in regulated industries and accelerates time-to-market for advanced compliance-driven solutions. Integration plans focus on seamless user experience and expanded service offerings, reinforcing Collibra’s competitive position amid rising demand for transparency and governance. Source: Collibra Corporate Announcement.

Regional Outlook

The Germany currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, France is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Germany

- France

- The United Kingdom

- BeNeLux

- Spain

- Italy

- NORDIC

- CEE

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 10.5 Billion |

| CAGR | 11.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.4% |

| Scope of Report | Market is segmented by Type (On-Premise Business Data Management Software, Cloud-Based Business Data Management Software, Hybrid Solutions, Open Source Data Management Software, SaaS Platforms), Application (Data Analytics, Data Integration, Master Data Management, Data Governance, Cloud Data Management), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Industry Vertical (Financial Services, Healthcare, Manufacturing, Retail, Telecommunications) |

| Regions Covered | Germany, France, The United Kingdom, BeNeLux, Spain, Italy, NORDIC, CEE, Others |

| Key Companies | SAP SE (Germany), SAS Institute Inc. (United States), Software AG (Germany), Micro Focus International plc (United Kingdom), Talend S.A. (France), Oracle Corporation (United States), Informatica LLC (United States), IBM Corporation (United States), TIBCO Software Inc. (United States), Collibra NV (Belgium), Denodo Technologies (Spain), Alteryx, Inc. (United States), QlikTech International AB (Sweden), Board International SA (Switzerland), Dataiku, Inc. (France), Cloudera, Inc. (United States), Snowflake Inc. (United States), Denodo Technologies (Spain), Hitachi Vantara Corporation (Japan), TIBCO Software Inc. (United States), Ataccama Corporation (Czech Republic), Precisely (United States), Zaloni, Inc. (United States), Informatica LLC (United States), Teradata Corporation (United States) |

Europe Business Data Management Software Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.